|

시장보고서

상품코드

2061596

하이브리드 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hybrid Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

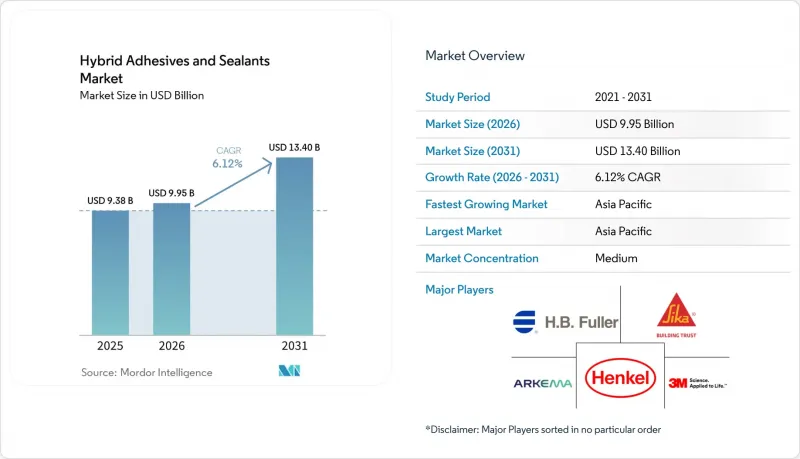

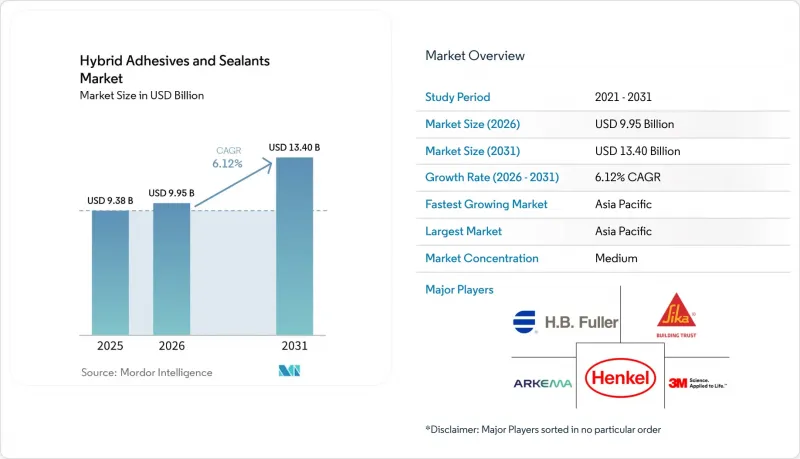

Mordor Intelligence에 의하면, 하이브리드 접착제 및 실란트 시장 규모는 2025년 93억 8,000만 달러로 평가되었습니다. 2026년 99억 5,000만 달러로 확대되어 2031년까지 134억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.12%를 나타낼 것으로 전망됩니다.

본 보고서는 수지 유형별(MS 폴리머 하이브리드, 에폭시·폴리우레탄, 에폭시·시아노아크릴레이트, 기타 수지), 최종 사용자 산업별(건축 및 건설, 운송, 전자, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 하이브리드 접착제 및 실란트 시장 동향과 인사이트

자동차 및 건설 분야 수요 급증

현재 전기차 배터리 팩에는 셀-투-팩(Cell-to-Pack) 구조가 채택되어 있으며, 이 구조에는 방열성이 있고 150°C의 온도 변동을 견딜 수 있으며, 재활용을 위해 지시에 따라 박리할 수 있는 접착제가 필요합니다. 듀폰의 ‘베타포스(Betaforce)’ 탄성 구조용 시리즈는 표면 전처리 없이 알루미늄 라미네이트 파우치 셀을 접착하여, 각 모듈 조립 주기를 15-20분 단축합니다. 아시아의 고층 건축 프로젝트에서도 이와 같은 추세가 나타나고 있으며, 속경화형 MS 폴리머 하이브리드를 통해 외벽 설치와 방수 처리를 같은 날에 진행할 수 있게 되어, 크레인 임대료와 인건비를 절감하고 있습니다. 북미의 주택 건설업체들은 2액형 폴리우레탄 시스템으로 접합된 조립식 패널을 선호하여 채택하고 있습니다. 스틸 스터드로 인한 열교를 제거함으로써 벽의 U값이 개선되어, 프로젝트가 그린빌딩 인증 요건을 충족하게 됩니다. H.B. 풀러가 2024년에 HS 부틸을 인수함에 따라 방수 테이프가 제품 라인업에 추가되었고, 이로 인해 유럽 전역의 커튼월 시공업체들의 생산성이 2배로 향상되었습니다. 전기화와 모듈식 건축이 융합되는 가운데, 조달 팀은 초기 자재 가격이 아닌 총소유비용(TCO)을 기준으로 접착제를 평가하는 경향이 강해지고 있습니다.

전 세계 VOC 및 이소시아네이트 규제 강화

유럽연합(EU)의 REACH 규정 부속서 XVII 개정에 따라, 디이소시아네이트 함유량이 0.1%를 초과하는 물질을 취급하는 모든 작업자는 인증 교육 이수가 의무화되었으며, 컨버터는 이소시아네이트를 포함하지 않는 MS 폴리머나 에폭시·아크릴계 하이브리드로의 전환을 강요받고 있습니다. 이와 동시에, EU의 포장 및 포장 폐기물 규정에 따라 2026년 8월부터 불소 총 함유량을 50ppm으로 제한하게 되어, 재활용성을 저해하는 불소계 이형제에서 다른 성분으로의 변경이 요구되고 있습니다. 캘리포니아주의 ‘더 안전한 소비자 제품 프로그램’에서는 유럽의 규제와 마찬가지로, 일부 이소시아네이트가 우선 관리 화학물질로 지정되어 있습니다. 3M사는 2025년 말까지 모든 PFAS 생산에서 철수함으로써 책임을 회피하고, 연간 8억 9,000만 달러 규모의 접착제 매출을 희생했지만, 2025년 9월에는 위험성이 낮은 아크릴계 대체 제품인 ‘Scotch-Weld DP8507NS’를 출시했습니다. VOC 및 이소시아네이트가 함유되지 않은 하이브리드 제품임을 입증할 수 있는 공급업체들은 공장 환기 설비의 업그레이드나 대규모 직원 재교육을 강요받지 않고도 사양서를 확보하고 있습니다.

원자재 및 실란 가격 변동

와커사는 백금 촉매 비용이 두 배로 증가한 데 따라, 2026년 2월에 실리콘 제품 가격을 최대 25% 인상할 것이라고 발표했습니다. 이로 인해 접착제의 매출총이익률은 최대 400 베이시스 포인트 하락할 것으로 예측됩니다. 중국의 태양광 발전 붐이 새로운 전자 등급 생산 능력을 흡수했고, 미국의 최대 245% 관세로 인해 수입이 제한되면서 실란의 현물 가격은 높은 수준을 유지했습니다. 접착제 배합 제조업체들은 가격 인상분을 자체적으로 흡수할지, 아니면 이를 원가 전가하여 시장 점유율을 잃을 위험을 감수할지 선택해야 하는 상황에 놓여 있습니다. 수직 통합은 이 문제를 완화할 수 있는 한 가지 방법입니다. 시카사는 원료의 안정적인 공급을 확보하기 위해 텍사스주의 지붕용 시트 공장에 9,000만 달러를 투자하고, 쑤저우에서는 폴리우레탄 기술 확충에 힘썼습니다. 그렇긴 하지만, 백금 및 특수 실란의 가격 변동을 예측하기 어렵다는 점은 추가 생산 능력으로 인해 시장이 안정될 때까지 단기적인 수익성을 저해할 것으로 보입니다.

부문별 분석

MS 폴리머 하이브리드는 2025년에 하이브리드 접착제·실런트 시장의 56.87% 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.30%를 기록하며 성장할 전망입니다. 이 부문의 급속한 성장은 규제 측면에서의 우대 조치를 반영한 것입니다. 이는 습기 경화형 실릴 골격이 VOC나 이소시아네이트를 방출하지 않기 때문입니다. 2025년 12월에 발표된 헨켈의 ‘Loctite MS 9650’은 차량용 디스플레이 접착을 목표로 하며, REACH 부속서 XVII의 규제 요건을 회피하고 있습니다. 에폭시·폴리우레탄 상호 침투 네트워크는 풍력 터빈 및 항공우주 구조물 분야에서 여전히 확고한 입지를 유지하고 있으며, 자가 복구 능력과 내피로성을 갖춘 대신 가격이 15-25% 더 높게 책정되어 있습니다. 에폭시·시아노아크릴레이트 혼합물은 60초 이하의 경화 시간이 필요한 의료 및 전자 분야의 틈새 시장을 충족시키고 있습니다. H.B. 풀러가 2024년에 메디필과 GEM을 인수함에 따라, 상처 봉합용 접착제가 추가되면서 이 회사의 외과 사업 부문이 확대되었습니다.

2026년부터 2031년에 걸쳐, 배합 제조업체들이 랩 전단 강도의 역사적인 격차를 해소하고 상온 경화 시험에서 2 MPa를 초과하게 됨에 따라, 판매량은 MS 폴리머로 전환될 전망입니다. 에폭시계 하이브리드는 초고탄성률이나 극도의 내열성이 규제상의 제약을 상회하는 분야에서 전문적인 영역을 유지하고 있습니다. 핫멜트계 하이브리드 및 에폭시·폴리설파이드계 선박용 실란트는 용도별 고유한 성능 요건에 제약을 받기 때문에 더욱 제한적인 역할밖에 수행할 수 없습니다.

지역별 분석

아시아태평양은 2025년에 하이브리드 접착제 및 실란트 시장 매출의 45.44%를 차지했으며, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 8.41%를 나타낼 것으로 전망됩니다. 와커사의 장자강 투자로 인해 해당 지역의 실리콘 생산 능력은 약 20퍼센트 포인트 증가했으며, 현지 OEM 제조업체들은 건설용 실란트와 전기차(EV) 열 관리용 고순도 유체를 더 신속하게 조달할 수 있게 되었습니다. 인도의 1,200억 달러 규모 인프라 계획과 인도네시아의 1,500억 달러 예산 배정으로 인해 프리캐스트 교량 상판, 지하철 시스템, 유리 파사드에 사용되는 접착제 수요가 증가하고 있습니다. 일본과 한국이 츠쿠바와 진천에서 생산을 확대함에 따라, 아시아 기능성 실리콘 시장에서의 지배력은 더욱 강화되고 있습니다.

북미와 유럽에서는 이소시아네이트가 함유되지 않은 하이브리드 제품을 뒷받침하는 엄격한 배출 규제의 영향으로 한 자릿수 중반대의 성장이 예상됩니다. EU의 포장 및 포장 폐기물 규제로 인해, 변환업체들은 재활용성을 고려하여 다층 라미네이트를 재설계할 수밖에 없게 되었으며, 이로 인해 수성 테이프 및 무용제 라미네이트용 접착제에 대한 수요가 증가하고 있습니다. 헨켈이 2026년에 펼친 인수 붐, 즉 슈타르 그룹 및 ATP 애드헤시브 시스템즈의 인수는 12억 유로의 매출을 창출했으며, 두 지역에 서비스를 제공하는 수성 기술 플랫폼을 강화했습니다. 한편, 3M은 PFAS 사업에서 완전히 철수함에 따라, 보다 안전한 아크릴계 제품을 중심으로 제품 포트폴리오를 재구성하고 있습니다.

중동 및 아프리카는 사우디아라비아의 ‘비전 2030’의 혜택을 누리고 있습니다. 이 계획에 따르면, 2030년까지 670만 톤의 특수 화학제품 생산 능력과 연간 935억 사우디아라비아 리얄의 매출을 목표로 하고 있으며, 이를 통해 2035년까지 해당 지역의 하이브리드형 접착제 및 실란트 시장 점유율이 약 22%를 나타낼 것으로 전망됩니다. 시카의 모로코, 탄자니아, 남아프리카공화국 각 공장은 재생에너지, 수처리, 교통 회랑 분야의 인프라 투자에 대비하고 있습니다. 남미는 환율 변동의 영향으로 여전히 성장세가 가장 둔한 지역이지만, 시카와 H.B. 풀러가 브라질과 아르헨티나에서 생산 능력을 확대함에 따라, 이 지역은 경기 순환적 회복을 위한 기반을 마련하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the hybrid adhesives and Sealants Market size is expected to increase from USD 9.38 billion in 2025 to USD 9.95 billion in 2026 and reach USD 13.40 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Resin Type (MS Polymer Hybrid, Epoxy-Polyurethane, Epoxy-Cyanoacrylate, and Other Resins), by End-User Industry (Building and Construction, Transportation, Electronics, and Other End-User Industries), and by Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Hybrid Adhesives And Sealants Market Trends and Insights

Rapid Automotive and Construction Demand

Electric-vehicle battery packs now incorporate cell-to-pack architectures that require adhesives to dissipate heat, tolerate 150°C excursions, and debond on command for recycling. DuPont's Betaforce elastic structural series bonds aluminum-laminated pouch cells without surface pretreatment, trimming 15-20 minutes from each module assembly cycle. Parallel momentum is visible in high-rise Asian projects where rapid-cure MS polymer hybrids let facades be hung and waterproofed on the same day, cutting crane rental and labor expense. North American residential builders favor prefabricated panels held together with two-component polyurethane systems; eliminating steel-stud thermal bridges improves wall U-values and qualifies projects for green-building credits. H.B. Fuller's 2024 purchase of HS Butyl added waterproofing tapes that double the throughput of curtain-wall installers across Europe. As electrification and modular construction converge, procurement teams increasingly evaluate adhesives on total cost of ownership rather than upfront material price.

Stricter Global VOC and Isocyanate Regulations

The European Union's REACH Annex XVII amendment obliges any worker handling more than 0.1% diisocyanate content to complete certified training, pushing converters toward isocyanate-free MS polymer and epoxy-acrylic hybrids. Concurrently, the EU Packaging and Packaging Waste Regulation caps total fluorine at 50 ppm from August 2026, compelling reformulation away from fluorinated release agents that hinder recyclability. California's Safer Consumer Products program flags several diisocyanates as priority chemicals, echoing European pressure. 3M pre-empted liability by exiting all PFAS production by end-2025, sacrificing USD 890 million in annual adhesive revenue but launching a low-hazard acrylic replacement, Scotch-Weld DP8507NS, in September 2025. Suppliers able to certify VOC-free, isocyanate-free hybrids win specifications without forcing plant ventilation upgrades or extensive worker retraining.

Raw-Material and Silane Price Volatility

Wacker announced up to 25% price hikes on silicone goods in February 2026 after platinum catalyst costs doubled, pressuring adhesive gross margins by as much as 400 basis points. Spot silane prices stayed elevated when China's photovoltaic boom absorbed new electronic-grade capacity and US tariffs of up to 245% restricted imports. Adhesive formulators must either swallow the increases or risk share loss by passing them through. Vertical integration is one mitigation path: Sika invested USD 90 million in a roofing-membrane plant in Texas and expanded polyurethane technologies in Suzhou to secure feedstock flows. Nonetheless, unpredictability in platinum and specialty silanes will restrain short-run profitability until additional capacity stabilizes the market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Multifunctional Bonding

- APAC Infrastructure Boom

- Higher Unit Cost Versus Commodity Sealants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MS polymer hybrids captured 56.87% of the Hybrid Adhesives and Sealants market share in 2025 and are set to grow at 7.30% CAGR to 2031. The segment's leap reflects regulatory favor, because moisture-cure silyl backbones release no VOCs or isocyanates. Henkel's Loctite MS 9650, unveiled in December 2025, targets in-car display bonding and sidesteps REACH Annex XVII training mandates. Epoxy-polyurethane interpenetrating networks retain a foothold in wind-turbine and aerospace structures, trading 15-25% higher prices for self-healing and fatigue resistance. Epoxy-cyanoacrylate blends fill medical and electronics niches demanding less than or equal to 60-second fixture speeds; H.B. Fuller's 2024 purchase of Medifill and GEM added wound-closure adhesives that expand its surgical franchise.

Across 2026-2031, volume tilts toward MS polymers as formulators close the historic gap in lap-shear strength, now surpassing 2 MPa in ambient-cure tests. Epoxy-based hybrids keep a specialized territory where ultra-high modulus or extreme heat resistance outweigh regulatory constraints. Hot-melt hybrids and epoxy-polysulfide marine sealants serve even narrower roles, constrained by application-specific performance envelopes.

Geography Analysis

Asia-Pacific retained 45.44% of the Hybrid Adhesives and Sealants market revenue in 2025 and is projected to expand at an 8.41% CAGR during the forecast period (2026-2031). Wacker's Zhangjiagang investment boosted regional silicone capacity by roughly 20 percentage points, giving local OEMs faster access to high-purity fluids for construction sealants and EV thermal management. India's USD 120 billion infrastructure pipeline and Indonesia's USD 150 billion allocation funnel adhesive demand into precast bridge decks, metro systems, and glass facades. Japanese and South Korean expansions in Tsukuba and Jincheon further tighten Asia's grip on functional silicones.

North America and Europe exhibit mid-single-digit growth, buoyed by strict emissions caps that favor isocyanate-free hybrids. The EU Packaging and Packaging Waste Regulation forces converters to redesign multilayer laminates for recyclability, boosting demand for water-based tapes and solvent-free laminating adhesives. Henkel's 2026 acquisition spree, Stahl Group, and ATP Adhesive Systems, added EUR 1.2 billion in revenue and deepened water-based technology platforms serving both regions. Meanwhile, 3M's complete PFAS exit repositions its portfolio around safer acrylics.

The Middle East and Africa benefit from Saudi Arabia's Vision 2030, which earmarks 6.7 million tons of specialty-chemical capacity and SAR 93.5 billion annual revenue by 2030, raising the region's share of Hybrid adhesives and sealants market to an estimated 22% by 2035. Sika's Moroccan, Tanzanian, and South African plants prepare for infrastructure spending in renewable energy, water treatment, and transit corridors. South America remains the slowest-growing territory, restrained by currency swings, yet capacity builds in Brazil and Argentina by Sika and H.B. Fuller position the region for cyclical rebounds.

- 3M

- American Sealants Inc.

- Arkema

- Dymax Corporation

- Forgeway

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Hermann Otto GmbH

- Hodgson Sealants

- Kisling AG

- MAPEI SpA

- Master Bond Inc.

- Sika AG

- Permabond LLC

- TREMCO ILLBRUCK

- Wacker Chemie AG

- Merz+benteli AG

- McCoy Soudal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rapid automotive and construction demand

- 4.1.2 Stricter global VOC and isocyanate regulations

- 4.1.3 Shift toward multifunctional bonding (mechanical fastener replacement)

- 4.1.4 APAC infrastructure boom

- 4.1.5 Modular and prefabricated building uptake

- 4.2 Market Restraints

- 4.2.1 Raw-material and silane price volatility

- 4.2.2 Higher unit cost vs. commodity sealants

- 4.2.3 Bottlenecks in specialty silane capacity

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 MS Polymer Hybrid

- 5.1.2 Epoxy-Polyurethane

- 5.1.3 Epoxy-Cyanoacrylate

- 5.1.4 Other Resins (Epoxy - Polysulfide, and more)

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Transportation

- 5.2.3 Electronics

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 American Sealants Inc.

- 6.4.3 Arkema

- 6.4.4 Dymax Corporation

- 6.4.5 Forgeway

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Jowat SE

- 6.4.9 Hermann Otto GmbH

- 6.4.10 Hodgson Sealants

- 6.4.11 Kisling AG

- 6.4.12 MAPEI SpA

- 6.4.13 Master Bond Inc.

- 6.4.14 Sika AG

- 6.4.15 Permabond LLC

- 6.4.16 TREMCO ILLBRUCK

- 6.4.17 Wacker Chemie AG

- 6.4.18 Merz+benteli AG

- 6.4.19 McCoy Soudal

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment