|

시장보고서

상품코드

2061606

SGLT2 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)SGLT2 - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

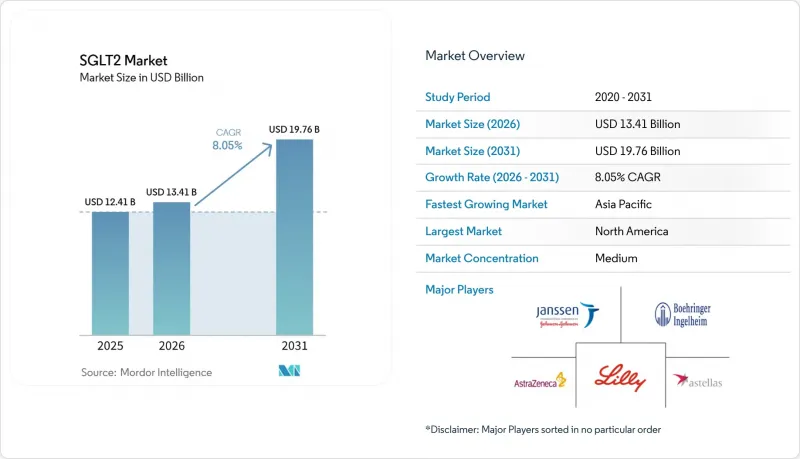

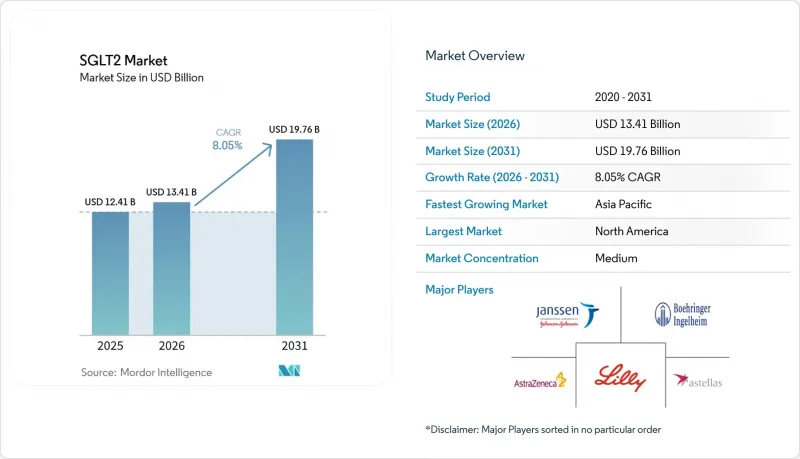

Mordor Intelligence에 의하면, SGLT2 시장 규모는 2025년에 124억 1,000만 달러로 평가되었습니다. 2026년에 134억 1,000만 달러에 달하고, 2031년까지 197억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 8.05%를 나타낼 전망입니다.

본 보고서는 의약품 분자(카나글리플로진, 다파글리플로진 등), 치료 적응증(2형 당뇨병 등), 유통 채널(병원 약국 등) 및 지역(북미, 유럽, 아시아·태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 SGLT2 시장 동향 및 분석

전 세계 당뇨병 부담 증가

유병률의 상승이 SGLT2 시장의 장기적인 판매량 확대를 뒷받침하고 있습니다. 인도에서는 2형 당뇨병 환자의 60.69%가 여전히 이러한 약물을 복용하지 않고 있으며, 그 주된 이유로 41.45%가 비용 장벽을 꼽고 있는 것으로 나타나, 보급에 있어 큰 여지가 있는 것으로 밝혀졌습니다. PLoS Medicine지에 발표된 마이크로 시뮬레이션에 따르면, 저·중소득 국가에서 SGLT2 억제제가 널리 도입될 경우, 장애 조정 생명 연수(DALY)가 2.20에서 1.25로 감소할 것으로 예측됩니다. 태국에서는 다파글리플로진이 국가 보험 급여 기준을 충족하기 위해서는 57.13%의 가격 인하가 필요하다는 사실이 밝혀지면서, 가격 탄력성과 관련된 문제가 부각되었습니다. 일본의 초고령화 사회에서는 허약한 고령자의 유해 사건을 방지하기 위해 엄격한 안전성 선별 검사가 요구되고 있습니다. 전반적으로, 당뇨병 환자 증가로 인해 경제적 부담이라는 장벽이 여전히 존재하는 상황에서도 기초적인 수요는 계속 증가하고 있으며, 이는 SGLT2 시장을 강화하고 있습니다.

심혈관 및 신장에 대한 유익성에 관한 근거의 확대

대규모 무작위 임상시험을 통해, 심장 및 신장 보호 효과가 이 계열 약물의 특징으로 확립되었습니다. KDIGO 2024 지침에서는 당뇨병 유무와 관계없이 신기능 저하 속도가 37% 늦어지고 급성 신장 손상 위험이 23% 감소한다는 연구 결과를 바탕으로, 만성 신장병의 초기 단계에서 SGLT2 제제의 사용을 권장하고 있습니다. 7만 8,607명의 참가자를 대상으로 한 메타분석 결과, 심부전 및 돌연사의 감소에 힘입어 이 약물군에 의한 주요 심혈관 이상반응이 9% 감소한 것으로 나타났습니다. FDA가 박출률이 유지되거나 저하된 심부전 환자에 대한 다파글리플로진 승인을 함에 따라, 대상 환자군이 확대되었습니다. BOLD-MRI 연구에서 카나글리플로진은 5일 이내에 신장의 산소 공급을 개선하여, 장기 수준에서 신속한 효과가 나타났습니다. 이러한 다각적인 성과는 전문 분야를 초월한 폭넓은 처방으로 이어져, 시장 확대와 SGLT2 시장 점유율 확대를 뒷받침하고 있습니다.

신흥 시장의 높은 가격 책정과 진입 장벽

저소득 국가에서는 가격 격차로 인해 치료의 보급이 지연되고 있습니다. 인도에서 엠파글리플로진의 월간 비용은 1,539-1,602 루피인 반면, 다파글리플로진은 326-1,088 루피로, 많은 환자에게 있어 감당할 수 있는 본인 부담 범위를 초과하고 있습니다. 국경없는의사회는 실현 가능한 원가 기준 가격을월1.30-3.45달러로 추정하고 있으며, 이는 소매가보다 한 자릿수 낮아서 가격 책정에 여지가 있음을 보여줍니다. 21개국을 대상으로 한 4제 병용 요법 연구에 따르면, SGLT2 억제제 성분은 저소득 국가에서 가장 구하기 어려웠으며, 파키스탄과 방글라데시가 가장 저렴하고 미국이 가장 비싼 것으로 밝혀졌습니다. 다파글리플로진 5mg의 브랜드 의약품 가격 비율은 10.79에 달하며, 이는 시장 내 가격 변동이 매우 크다는 것을 보여줍니다. 차별화된 가격 책정이나 광범위한 입찰 할인 프로그램이 확대되지 않는 한, 보급 지연이 SGLT2 시장의 연평균 성장률(CAGR)을 억제하게 될 것입니다.

부문별 분석

다파글리플로진은 2025년에도 SGLT2 시장에서 38.12%의 점유율을 유지했으며, 화합물 특허 만료 후에도 에버그린 전략을 통해 중국에서 5억 달러의 매출을 기록했습니다. 에르투그리플로진은 머크의 복합제제 ‘SEGLUROMET’에 힘입어 2031년까지 연평균 성장률(CAGR) 10.02%라는 가장 높은 성장률을 기록하며, 매출액이 12억 7,500만 달러에 달할 것으로 전망됩니다.

엠파글리플로진은 2022년 매출이 58억 유로에 달했으며, 세계 시장에서 52.60%의 분자 점유율을 차지했습니다. 이는 베링거 인겔하임과 일라이 릴리의 공동 영업 활동 규모와 초기 심혈관 결과에 대한 성과가 기여한 결과입니다. 카나글리플로진은 경쟁 압력으로 인해 성장세가 둔화되고 있습니다. 소타글리플로진은 SGLT1/2에 대한 이중 작용을 가지고 있어 독자적인 사건 감소 효과를 기대하게 하고 있지만, 미국에서의 1상 임상시험 실패로 인해 규제 당국의 승인을 얻기 위한 조치가 기다려지고 있습니다. 특허 만료 추이를 살펴보면, 팔시가의 제네릭 위험은 2030년 6월까지, 임보카나의 경우 2031년 11월까지 현실화될 전망이며, 이에 따라 개발 기업들은 고정 용량 복합제나 새로운 적응증으로의 전환을 모색해야할 것입니다. 원료의약품(API) 생산은 여전히 집중되어 있으며, 전 세계 카나글리플로진 원료의약품의 65%가 인도나 중국에서 생산되고 있습니다. 원료의약품 가격은 순도나 계약 조건에 따라 1그램당 20-80달러 범위입니다. 이러한 공급망의 집중화는 비용 절감 효과를 가져오지만, 기업을 지정학적 위험에 노출시키기도 합니다. 기업들은 자유무역협정을 체결한 국가들로부터 이중 조달을 실시함으로써 이러한 위험에 대처하고 있습니다. 신약인 베키사글리플로진은 2025년 1월 FDA 승인을 획득했으며, Cost Plus Drugs를 통해 30일분당 50달러에 판매되고 있어, 본인부담 환자층의 가격 구조에 변화를 가져오고 있습니다. 전반적으로, 분자의 지속적인 진화는 향후 제네릭 의약품에 의한 시장 잠식에 대비해 SGLT2 시장을 공고히 하고 있습니다.

지역별 분석

2025년, 북미는 SGLT2 시장 점유율의 42.75%를 차지했으며, 이는 진료 지침의 일관성, 광범위한 보험 적용, 그리고 심혈관 분야에서의 급속한 보급을 반영하고 있습니다. 메디케어 파트 D 및 주요 민간 보험사들은 심부전 적응증에 대해 동종 계열 약물의 보험 적용을 하고 있으며, 이는 북미 시장에서 지속적인 우위를 뒷받침하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 9.12%로 확대되고 있으며, 당뇨병 환자 수의 높은 증가율과 전략적인 특허 전략이 맞물려 성장을 이어가고 있습니다. 중국의 국가 약가 등재로 인해, 제네릭 의약품의 위협에도 불구하고 다파글리플로진의 매출액은 2024년에 5억 달러에 달했습니다. 아스트라제네카가 1억 9,000만 위안 규모의 생산 라인을 확장함에 따라 국내 공급이 확보되었습니다. 인도에서는 가격 때문에 수요가 억제되고 있지만, 급속한 도시화가 진행 중인 중산층의 존재는 차별화된 가격 책정이나 제네릭 의약품 시장 진입을 통해 비용이 낮아진다면 잠재적인 판매량 확대를 시사하고 있습니다.

유럽에서는 EMA의 등급 승인 및 심혈관계에 대한 유익성과 가격을 비교 검토하는 각국의 HTA 평가를 통해 꾸준히 보급이 확대되고 있습니다. 가격·수량 계약으로 인해 이익률은 낮아지지만, 처방전에서의 높은 보급률이 확보되고 있습니다. 일본에서는 고령화 사회와 엄격한 의약품 안전성 감시 체제 덕분에, 안전성과 유효성 요건의 균형을 맞추면서 신중하면서도 임상적으로 목표를 명확히 한 사용이 이루어지고 있습니다. 라틴아메리카, 중동 및 아프리카에서는 지불 주체의 예산이 제한적이어서 시장 점유율이 낮은 상황이지만, 비용 측면의 장벽이 해소된다면 장기적인 성장의 새로운 영역이 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the sGLT2 market size is projected to be USD 12.41 billion in 2025, USD 13.41 billion in 2026, and reach USD 19.76 billion by 2031, growing at a CAGR of 8.05% from 2026 to 2031.

This report is Segmented by Drug Molecule (Canagliflozin, Dapagliflozin, and More), Therapeutic Indication (Type-2 Diabetes Mellitus, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global SGLT2 Market Trends and Insights

Increasing Global Diabetes Burden

Rising prevalence sustains long-run volume expansion for the SGLT2 market. In India, 60.69% of type 2 diabetes patients still forgo these drugs mainly due to 41.45% cost barriers, revealing wide headroom for uptake A PLoS Medicine microsimulation projected disability-adjusted life years falling from 2.20 to 1.25 when SGLT2 agents are introduced broadly across low- and middle-income countries. Thailand showed 57.13% price cuts are needed for dapagliflozin to clear national reimbursement thresholds, highlighting price elasticity challenges. Japan's super-aged cohort demands strict safety screening to avoid adverse events in frail elders. Collectively, the diabetes wave keeps baseline demand rising even as affordability hurdles persist, strengthening the sglt2 market.

Expanding Cardiovascular and Renal Benefit Evidence

Large randomized trials now cement cardiorenal protection as a class hallmark. KDIGO 2024 guidelines recommend SGLT2 agents early in chronic kidney disease based on 37% slower kidney-function decline and 23% lower acute-kidney-injury risk regardless of diabetes status. A meta-analysis of 78,607 participants showed 9% fewer major adverse cardiovascular events with the class, driven by heart-failure and sudden-death reductions. FDA approvals for dapagliflozin in heart failure with preserved or reduced ejection fraction widened addressable populations. Canagliflozin improved renal oxygenation within five days in BOLD-MRI studies, illustrating rapid organ-level benefits. These multidimensional outcomes encourage wider prescribing across specialties, enlarging the market and reinforcing gains in sglt2 market share.

Premium Pricing and Access Barriers in Emerging Markets

Affordability gaps slow therapeutic penetration in lower-income settings. Monthly empagliflozin runs INR 1,539-1,602 in India versus INR 326-1,088 for dapagliflozin, placing both outside sustainable out-of-pocket levels for many patients. Medecins Sans Frontieres estimated feasible cost-based prices near USD 1.30-3.45 per month-an order of magnitude below retail-exposing pricing latitude. Quadruple therapy studies across 21 countries revealed SGLT2 components least accessible in low-income economies, with Pakistan and Bangladesh lowest and the United States highest in price. Brand cost ratios hit 10.79 for dapagliflozin 5 mg, highlighting extreme intra-market variations. Unless differential pricing or broad tender-discount programs expand, penetration lags will temper the SGLT2 market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Diversifying Therapeutic Indications Beyond Glycemic Control

- Strategic Collaborations and Co-Marketing Alliances

- Ongoing Safety and Tolerability Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dapagliflozin retained a 38.12% SGLT2 market share in 2025 and anchored sales of USD 500 million in China, even after compound-patent expiry, through evergreen portfolio tactics. Ertugliflozin grows fastest at a 10.02% CAGR to 2031, fuelled by Merck's combination product SEGLUROMET with USD 1.275 billion potential forecast.

Empagliflozin, with €5.8 billion in 2022 revenue, supplied a 52.60% global molecule share, benefiting from Boehringer Ingelheim and Eli Lilly's co-detailing scale and early cardiovascular outcome wins. Canagliflozin faces a slower trajectory under competitive pressure. Sotagliflozin's dual SGLT1/2 profile promises unique event-reduction angles, yet it awaits broader regulatory alignment following the U.S. type 1 setback. Patent cliff maps indicate that Farxiga's generic risk will emerge by June 2030 and Invokana's by November 2031, incentivizing innovators to pivot toward fixed-dose combinations and new indications. API production remains concentrated, with 65% of global canagliflozin bulk originating in India or China. The raw prices range from USD 20 to USD 80 per gram, depending on purity and contract terms. Such supply-chain centralization offers cost economies, yet it exposes firms to geopolitical risk, which they counter by dual sourcing within free-trade partners. Emerging bexagliflozin secured FDA approval in January 2025 and retails at USD 50 per 30-day course through Cost Plus Drugs, creating price-point disruption for cash-pay segments . Overall, continual molecule evolution fortifies the SGLT2 market against future generic erosion.

Geography Analysis

North America accounted for 42.75% of SGLT2 market share in 2025, reflecting guideline alignment, broad insurance coverage and rapid cardiology uptake. Medicare Part D and major commercial insurers reimburse class drugs for heart-failure indications, supporting continued dominance.

Asia-Pacific, expanding at 9.12% CAGR, combines high diabetes growth with strategic patent maneuvers. China's national drug reimbursement listing catapulted dapagliflozin to USD 500 million revenue in 2024 despite generic threats; AstraZeneca's 190 million-yuan line expansion ensures domestic supply. India shows unmet demand constrained by price, yet rapidly urbanizing middle-class cohorts signal latent volume potential once differential-pricing or generic entries lower costs.

Europe maintains steady uptake through EMA class approvals and national HTA assessments that weigh cardiovascular benefit against price. Price-volume agreements temper margins yet secure high formulary penetration. Japan's aged demographic and strict pharmacovigilance produce cautious but clinically targeted use, balancing safety and efficacy imperatives. Latin America, Middle East and Africa lag in wallet share due to limited payer budgets but constitute long-term frontier growth arenas once cost hurdles abate.

- Astellas Pharma

- AstraZeneca

- Arena Pharmaceuticals

- Boehringer Ingelheim

- Cipla

- Chong Kun Dang

- Dr Reddy's Laboratories

- Eli Lilly and Company

- Glenmark Pharma

- Janssen

- Lupin

- Merck & Co. (Steglatro)

- Otsuka

- Sun Pharmaceuticals Industries

- Sumitomo Pharma

- Taisho Pharma

- Torrent Pharmaceuticals

- Zydus Lifesciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Global Diabetes Burden

- 4.2.2 Expanding Cardiovascular and Renal Benefit Evidence

- 4.2.3 Diversifying Therapeutic Indications Beyond Glycemic Control

- 4.2.4 Strategic Collaborations and Co-Marketing Alliances

- 4.2.5 Favorable Clinical Practice Guideline Recommendations

- 4.2.6 Growing Adoption of Oral Combination Therapies

- 4.3 Market Restraints

- 4.3.1 Premium Pricing and Access Barriers in Emerging Markets

- 4.3.2 Ongoing Safety and Tolerability Concerns

- 4.3.3 Intensifying Competition from Alternative Incretin Therapies

- 4.3.4 Patent Litigation and Regulatory Uncertainties

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Molecule

- 5.1.1 Canagliflozin

- 5.1.2 Dapagliflozin

- 5.1.3 Empagliflozin

- 5.1.4 Ertugliflozin

- 5.1.5 Ipragliflozin

- 5.1.6 Sotagliflozin

- 5.1.7 Other SGLT2 Inhibitors

- 5.2 By Therapeutic Indication

- 5.2.1 Type-2 Diabetes Mellitus

- 5.2.2 Heart Failure (HFrEF/HFmrEF)

- 5.2.3 Chronic Kidney Disease

- 5.2.4 Obesity / Weight Management

- 5.2.5 Other Therapeutic Indications

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Astellas Pharma

- 6.3.2 AstraZeneca

- 6.3.3 Arena Pharmaceuticals

- 6.3.4 Boehringer Ingelheim

- 6.3.5 Cipla Ltd.

- 6.3.6 Chong Kun Dang

- 6.3.7 Dr Reddy's Laboratories

- 6.3.8 Eli Lilly and Company

- 6.3.9 Glenmark Pharma

- 6.3.10 Janssen Pharmaceuticals

- 6.3.11 Lupin Ltd.

- 6.3.12 Merck & Co. (Steglatro)

- 6.3.13 Otsuka Pharmaceutical

- 6.3.14 Sun Pharma

- 6.3.15 Sumitomo Pharma

- 6.3.16 Taisho Pharma

- 6.3.17 Torrent Pharma

- 6.3.18 Zydus Lifesciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment