|

시장보고서

상품코드

2061613

알부민 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Albumin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

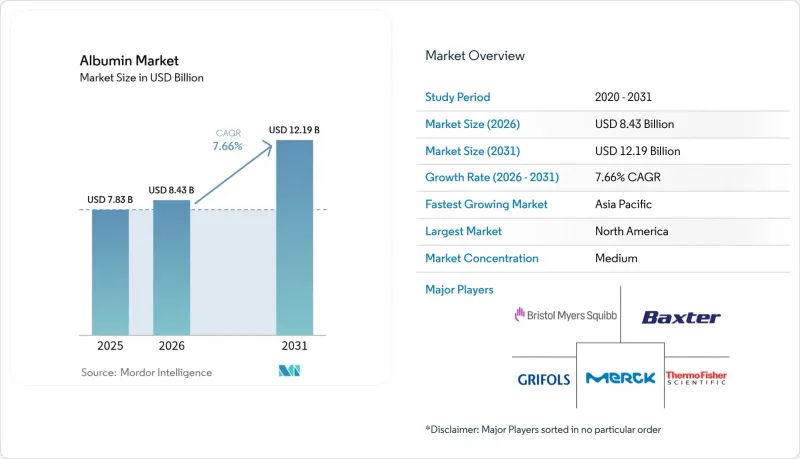

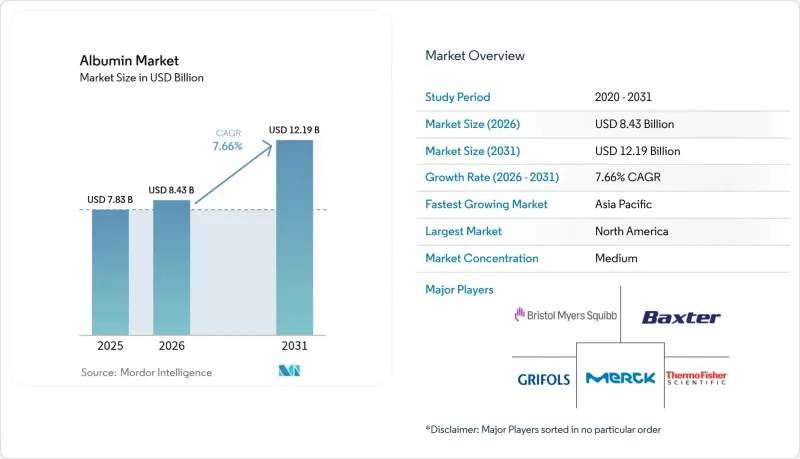

Mordor Intelligence에 의하면, 알부민 시장 규모는 2025년 78억 3,000만 달러로 평가되었습니다. 2026년에는 84억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 7.66%를 나타내, 2031년까지 121억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형(인간 혈청 알부민 등), 원료(혈장 유래, 재조합), 용도(약물 전달, 치료제 등), 최종 사용자(제약·바이오기술 기업, 연구기관·CRO, 병원 및 클리닉 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 알부민 시장 동향 및 분석

백신 제조 분야에서 알부민계 안정제에 대한 수요 증가

백신 제조업체들은 동결건조 및 유통 과정에서 항원을 보호하기 위해 알부민 안정제의 사용을 확대되고 있습니다. 이러한 움직임은 에볼라 출혈열용 생백신인 ERVEBO가 그 제제에 미국산 재조합 알부민을 포함시킨 것을 계기로 더욱 탄력을 받았습니다. 이러한 노력은 콜드체인에 대한 의존도를 낮추고, 고위험군을 대상으로 한 중요한 예방접종 프로그램의 안정성을 유지하기 위한 노력과 일치합니다. 재조합 알부민은 기증자 유래 병원체 위험을 제거합니다. 이는 면역 결핍 환자나 물류 체계가 취약한 지역을 지원하는 프로그램에 있어 핵심적인 장점이 됩니다. 중국 내 알부민 수요의 급증과 쌀 유래 재조합 인간 혈청 알부민이 후기 임상시험 단계에 접어들면서, 혈장 조달상의 제약을 피할 수 있는 국내 공급 옵션에 대한 관심이 높아지고 있습니다. 공중보건 당국은 변동성을 줄이고 승인 후 규제 문서의 변경을 용이하게 하기 위해, 가능한 한 미리 정의된 동물 유래 성분이 포함되지 않은 첨가제의 사용을 권장하고 있습니다. 이러한 수요 패턴은 예측 기간 내에 바이러스 벡터 및 단백질 서브유닛 플랫폼 프로그램이 제품 포트폴리오를 확대함에 따라, 백신 안정화 과정에서 알부민의 사용이 꾸준히 증가할 것으로 전망됩니다.

생물학적 제제 제조 시 알부민을 부형제로서 활용하는 사례 확대

개발자들이 제조, 보관, 투여의 전 단계에 걸쳐 제품의 품질 안정성에 주력함에 따라, 생물학적 제제에서 알부민의 안정화제 및 용해성 향상제로서의 역할은 확대되고 있습니다. 피하 투여 제제나 고농도 주사제는 알부민이 응집과 산화를 억제하는 특성 덕분에 이점을 얻으며, 이를 통해 보관 기간 내내 일관된 성능을 유지하는 데 도움이 됩니다. 루센티스 등의 안과용 주사제는 활성을 잃지 않고 냉장 보관을 견뎌야 하는 프리필드 제제에서 부형제의 선택이 내구성을 뒷받침하는 좋은 사례입니다. 인간용 알부민의 규제 관련 실적은 예측 가능한 신청 절차를 가능하게 하며, 광범위한 안전성 이력이 부족한 새로운 부형제와 비교할 때 특정 제제의 개발 기간을 단축시킵니다. 재조합 알부민의 배치 간 일관성은 변동성을 더욱 낮추고 문서화 부담을 줄여줍니다. 이는 라이프사이클 관리에 있어 필수적인 요소입니다. 바이오의약품 프로그램이 공급망의 회복탄력성과 효율적인 변경 관리 워크플로우에 중점을 두면서, 검증된 첨가제인 알부민의 위상은 특정 고부가가치 치료 분야에서 점점 더 중요해지고 있습니다.

혈장 유래 알부민을 통한 병원체 전파에 대한 안전성 우려

혈장 유래 알부민은 바이러스 양을 감소시키는 용매 및 계면활성제 처리, 저온 살균, 나노 여과와 같은 검증된 공정을 거쳤음에도 불구하고, 병원체 전파의 잔류 위험이 따릅니다. 기증자 선별 및 기증 중단 기준을 통해 위험은 줄어들지만, 특정 감염증의 윈도우 기간으로 인해 조사가 필요한 경우에는 재조사나 추가적인 모니터링 조치로 이어질 수 있습니다. FDA는 21 CFR Part 640에서 혈액 및 혈액 성분에 관한 기준을 정하고 있으며, 여기에는 미국 내 혈장 공급과 관련된 채취, 가공 및 검사 요건이 규정되어 있습니다. FDA가 2024년에 발표한 인간용 소 유래 재료에 관한 지침안은 BSE(소 해면상 뇌증) 위험 관리의 지속적인 중요성을 강조하고 있습니다. 이로 인해 추적성과 조달 관리에 대한 기대가 높아지고 있지만, 동물 유래 성분을 사용할 경우 이는 비용과 복잡성을 가중시키는 요인이 됩니다. 이러한 제약으로 인해, 백신 및 생물학적 제제 제조업체들은 환자의 안전성과 치료 순응도 측면에서 재조합 알부민 도입을 검토하고 있습니다. 그 결과, 기존 의료 현장에서는 혈장 유래 알부민에 대한 수요가 유지되고 있는 반면, 고성장 분야의 용도에서는 위험을 줄이기 위해 동물성 성분이 포함되지 않은 대안으로 전환되고 있습니다.

부문별 분석

인간 혈청 알부민은 2025년에 59.14%를 차지하며, 이는 임상 현장에서의 체액 보충, 화상 치료, 저알부민혈증 관리에 있어 핵심적인 역할을 하고 있음을 반영했습니다. 이러한 용도는 확립된 프로토콜에 기반을 두고 있으며, 임상의들은 검증된 안전성과 보험 급여 체계에 의존하여 안정적인 사용을 뒷받침하고 있습니다. 재조합 알부민 시장은 2031년까지 연평균 성장률(CAGR) 11.80%를 나타낼 것으로 전망됩니다. 이는 배치 간 일관성과 병원체가 없는 원료 공급이 중요시되는 백신, 생물학적 제제, 특수 세포 배양 배지에서 수요가 확대됨에 따라 주도되는 현상입니다. 이러한 상황에서 알부민 시장은 기존의 치료 현장과, 공급의 예측 가능성 및 규정된 첨가제가 중요한 첨단 용도 사이에서 양극화되고 있습니다. 소 혈청 알부민의 성장세가 둔화되고 있습니다. 이는 주류 단일클론 항체 제조 과정에서 단백질 보충제가 화학적으로 정의된 배지로 대체되고 있기 때문입니다. 그러나 동물 유래 성분의 배제를 요구하는 규제 압력의 영향을 덜 받는 진단 및 실험실 프로토콜 분야에서는 여전히 중요한 역할을 수행하고 있습니다. 유형 선호도의 변화에 따라, 공급업체들은 임상 및 비임상 분야의 요구 사항을 모두 충족하고, 규정 준수를 준수하는 확장 가능한 제조 경로로 생산 체계를 조정해야 하는 상황에 직면해 있습니다.

2025년에는 미국의 광범위한 채혈 네트워크와 북미 및 유럽에 구축된 분획 시설의 지원에 힘입어, 혈장 유래 알부민이 공급량의 82.02%를 차지했습니다. 미국은 전 세계 혈장 공급의 대부분을 담당하고 있으며, 이는 국내 분획 생산 및 수입 의존 지역에 대한 수출을 촉진하고 있습니다. 미국에서는 빈번한 혈장 기증을 허용하는 규제 체계 덕분에 생산 능력이 유지되고 있지만, 유럽과 아시아 일부 지역에서는 정책상의 제한으로 인해 수집량이 제약을 받아 급증하는 수요에 대응하는 데 어려움을 겪고 있습니다. 이러한 제약으로 인해 혈장 유래 원료의 가격 변동성이 커지면서, 듀얼 소싱 전략에 대한 관심이 높아지고 있습니다. 효모, 쌀 및 기타 발현 플랫폼에서 유래한 재조합 알부민은 규제가 엄격한 용도에서공급 충격과 규정 준수 복잡성을 완화하려는 제조업체들의 노력에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 10.65%를 나타낼 것으로 전망됩니다.

지역별 분석

북미는 2025년에 35.50%의 점유율을 차지했습니다. 이는 미국 내 광범위한 혈장 채취망과 안정적인 치료용 알부민 공급을 보장하는 확립된 분획 인프라에 힘입은 결과입니다. 해당 지역의 첨단 중환자 치료 환경과 성숙한 보험 급여 제도는 중환자 치료, 외과 수술, 응급 의료에 사용되는 수액에 대한 수요 유지에 기여하고 있습니다. 미국의 규제 당국은 전 세계 관행에 영향을 미치는 혈액 및 혈액 성분 기준을 수립하고 있으며, 이러한 체계 덕분에 국내 수요와 수출을 모두 뒷받침하는 빈번한 혈장 기증이 가능해졌습니다. 또한, 북미의 연구 및 바이오의약품 생태계는 알부민 기반 기술을 활용한 백신의 안정화 및 약물 전달 시스템의 재설계 분야에서도 성장을 이끌고 있습니다. 그 결과, 해당 지역의 알부민 시장은 기존의 치료 용도와 혁신 주도형 수요 증가가 결합되어 있습니다.

아시아태평양에서는 각국이 혈장 단백질 인프라에 투자하고 알부민 공급을 위한 재조합 경로 개발을 촉진하고 있어, 2031년까지 연평균 성장률(CAGR) 8.03%를 나타낼 것으로 전망됩니다. 중국과 인도의 내수 수요가 지역 성장의 중심이 되고 있으며, 수입 의존도를 낮추고 밸류체인의 더 많은 부분을 국내로 환원하기 위한 노력이 진행되고 있습니다. 중국에서 진행 중인 미국산 유래 유전자 재조합 인간 혈청 알부민의 후기 개발은 승인이 이루어지는 대로 백신, 첨가제 및 기타 규제 대상 용도를 뒷받침할 미래공급원이 될 것입니다. ViNS Bioproducts의 2026년 PlasmaGen에 대한 자금 지원 등, 인도 내 혈장 분획 능력에 대한 투자는 알부민 및 관련 혈장 단백질의 자급률 향상이라는 목표를 반영하고 있습니다. 이 지역의 알부민 시장은 강력한 정책 지원의 혜택을 받고 있으며, 이에 따라 혈장 유래 및 재조합 제품 공급업체 모두 현지 수요에 맞추어 생산 능력을 확대할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the albumin market size is expected to grow from USD 7.83 billion in 2025 to USD 8.43 billion in 2026 and is forecast to reach USD 12.19 billion by 2031 at 7.66% CAGR over 2026-2031.

This report is Segmented by Type (Human Serum Albumin, and More), Source (Plasma-Derived, Recombinant), Application (Drug Delivery, Therapeutics, and More), End-User (Pharmaceutical & Biotechnology Companies, Research Institutes & CROs, Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Albumin Market Trends and Insights

Growing Demand for Albumin-Based Stabilizers in Vaccine Manufacturing

Vaccine manufacturers are increasing the use of albumin stabilizers to protect antigens during lyophilization and distribution, which gained momentum when ERVEBO for Ebola, a live vaccine, incorporated rice-derived recombinant albumin in its formulation. This practice aligns with efforts to reduce cold-chain sensitivity and maintain stability for critical immunization programs serving high-risk populations. Recombinant albumin removes donor-derived pathogen risks, which is a core advantage for programs that support immunocompromised patients and regions with fragile logistics. China's significant albumin needs and the advancement of rice-derived recombinant human serum albumin through late-stage clinical trials are prompting greater attention to domestic supply options that bypass plasma sourcing constraints. Public-health agencies encourage the use of defined, animal-component-free excipients where feasible because they reduce variability and ease post-approval changes to regulated filings. This demand pattern supports a steady expansion of albumin use in vaccine stabilization as programs for viral-vector and protein-subunit platforms broaden their portfolios in the forecast window.

Expanding Use of Albumin as an Excipient in Biologic Drug Formulations

Albumin's role as a stabilizer and solubility enhancer in biologic formulations is expanding as developers focus on product integrity across manufacturing, storage, and administration. Subcutaneous and high-concentration injectable formats benefit from albumin's ability to reduce aggregation and oxidation, thereby helping maintain consistent performance throughout shelf life. Ophthalmology injectables, such as Lucentis, are examples in which excipient choices support durability in prefilled presentations that must withstand refrigerated storage without loss of activity. The regulatory track record of albumin in human use supports predictable filings, which shorten development timelines for specific formulations compared with newer excipients that lack extensive safety histories. Recombinant albumin's batch-to-batch consistency further reduces variability and documentation burden, which is essential for lifecycle management. As biologics programs focus on supply resilience and lean change-control workflows, albumin's position as a proven excipient is becoming more central across select high-value therapy classes.

Safety Concerns Around Pathogen Transmission from Plasma-Derived Albumin

Plasma-derived albumin carries a residual risk of pathogen transmission despite validated steps such as solvent-detergent treatment, pasteurization, and nanofiltration that reduce viral load. Donor screening and deferral criteria reduce risk, yet window periods for certain infections can still lead to recalls or added oversight in cases that demand investigation. The FDA maintains standards for blood and blood components in 21 CFR Part 640, which frames collection, processing, and testing requirements for the U.S. plasma supply. FDA's 2024 draft guidance on cattle-derived materials for human use underscores ongoing BSE risk management. It strengthens expectations for traceability and sourcing controls, which add cost and complexity when animal derivatives are used. These constraints motivate vaccine and biologics makers to consider recombinant albumin for patient safety and compliance reasons. As a result, plasma-based albumin retains demand in well-established care settings, while high-growth applications turn to animal-component-free options to mitigate risk.

Other drivers and restraints analyzed in the detailed report include:

- Rising Plasma-Fractionation Capacity in Asia-Pacific (China and India)

- Uptake of Recombinant Albumin in Cell-Culture Media for Cultivated-Meat R&D

- Rapid Shift Toward Chemically Defined, Protein-Free Media in Bioprocessing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Human Serum Albumin accounted for 59.14% in 2025, reflecting its central role in volume expansion, burn care, and the management of hypoalbuminemia in clinical practice. These uses remain anchored in established protocols, where clinicians rely on known safety and reimbursement pathways to support steady utilization. Recombinant Albumin is set to grow at an 11.80% CAGR through 2031, driven by gains in vaccines, biologics formulations, and specialized cell-culture media, where batch consistency and pathogen-free sourcing are preferred. In this context, the albumin market is splitting between legacy therapeutic settings and advanced applications where supply predictability and defined excipients matter. Bovine Serum Albumin is seeing slower growth as chemically defined media replace protein supplements in mainstream monoclonal antibody manufacturing. However, it retains roles in diagnostics and lab protocols that are less sensitive to regulatory pressure to eliminate animal components. The evolution of type preferences is driving suppliers to align production with compliant, scalable routes that meet both clinical and non-clinical needs.

Plasma-derived albumin held 82.02% of the supply in 2025, supported by extensive U.S. collection networks and established fractionation hubs in North America and Europe. The United States supplies a large share of global plasma, which promotes domestic fractionation output and exports to import-dependent regions. Regulatory frameworks in the United States that allow frequent plasma donations help maintain capacity, while policy limits in parts of Europe and Asia constrain collection volumes and slow response to demand spikes. These constraints reinforce price swings for plasma-derived inputs and increase interest in dual sourcing strategies. Recombinant albumin from yeast, rice, and other expression platforms is projected to grow at a 10.65% CAGR from 2026 to 2031 as manufacturers seek to limit supply shocks and compliance complexity for tightly regulated applications.

Geography Analysis

North America captured 35.50% in 2025, supported by the United States' large plasma-collection footprint and established fractionation base that ensures a steady therapeutic albumin supply. The region's high-acuity care settings and mature reimbursement systems help sustain demand for infusions used in critical care, surgery, and emergency medicine. U.S. regulators set standards for blood and blood components that influence global practices, and these frameworks enable frequent plasma donations that support both domestic demand and exports. North America's research and biopharma ecosystems also contribute to growth in vaccine stabilization and drug-delivery reformulations that utilize albumin-based technologies. As a result, the albumin market in the region combines legacy therapeutic use with growing innovation-led demand.

Asia-Pacific is projected to grow at an 8.03% CAGR through 2031 as countries invest in plasma-protein infrastructure and encourage the development of recombinant routes for albumin supply. Domestic needs in China and India are central to regional growth, with initiatives to reduce import dependence and to bring more of the value chain onshore. Late-stage development of rice-derived recombinant human serum albumin in China adds a future source of supply that can support vaccines, excipients, and other regulated uses once approvals are secured. India's investments in fractionation capacity, such as ViNS Bioproducts' 2026 funding for PlasmaGen, reflect this goal of greater self-sufficiency in albumin and related plasma proteins. The albumin market in the region benefits from strong policy support, which should attract both plasma-derived and recombinant suppliers to scale capabilities in step with local demand.

- Akron Biotechnology, LLC

- Albumedix Ltd.

- Albumin Therapeutics LLC

- Baxter

- Bio Products Laboratory

- CSL Behring GmbH

- Grifols SA (Biotest AG)

- HiMedia Laboratories Pvt. Ltd.

- Hualan Biological

- Kedrion Biopharma

- Medxbio Pte Ltd.

- Merck

- Novozymes A/S

- Octapharma

- Shanghai RAAS Blood Products Co., Ltd.

- Takeda Pharmaceuticals

- Thermo Fisher Scientific

- Ventria Bioscience

- ViruSure GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Albumin-Based Stabilizers in Vaccine Manufacturing

- 4.2.2 Expanding Use of Albumin as an Excipient in Biologic Drug Formulations

- 4.2.3 Rising Plasma-Fractionation Capacity in Asia-Pacific (China & India)

- 4.2.4 Uptake of Recombinant Albumin in Cell-Culture Media for Cultivated-Meat R&D

- 4.2.5 Adoption of Albumin Nanoparticles in Next-Gen Targeted Drug-Delivery Platforms

- 4.2.6 Regulatory Push for Safer Blood-Product Handling (EU MDR & U.S. CGMP Upgrades)

- 4.3 Market Restraints

- 4.3.1 Safety Concerns Around Pathogen Transmission from Plasma-Derived Albumin

- 4.3.2 Price Volatility Due To Plasma-Collection Bottlenecks

- 4.3.3 Rapid Shift Toward Chemically Defined, Protein-Free Media in Bioprocessing

- 4.3.4 Competition From Plant-Derived Albumin Mimetics in Food & Cosmetics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Human Serum Albumin

- 5.1.2 Bovine Serum Albumin

- 5.1.3 Recombinant Albumin

- 5.2 By Source

- 5.2.1 Plasma-derived

- 5.2.2 Recombinant (Yeast, Rice, Transgenic Plants)

- 5.3 By Application

- 5.3.1 Drug Delivery

- 5.3.2 Therapeutics

- 5.3.3 Culture-Media Ingredient

- 5.3.4 Vaccine Ingredient

- 5.3.5 Diagnostics

- 5.3.6 Other Applications

- 5.4 By End-user

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Research Institutes & CROs

- 5.4.3 Hospitals & Clinics

- 5.4.4 Diagnostic Centers

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Akron Biotechnology, LLC

- 6.3.2 Albumedix Ltd.

- 6.3.3 Albumin Therapeutics LLC

- 6.3.4 Baxter International Inc.

- 6.3.5 Bio Products Laboratory Limited

- 6.3.6 CSL Behring GmbH

- 6.3.7 Grifols SA (Biotest AG)

- 6.3.8 HiMedia Laboratories Pvt. Ltd.

- 6.3.9 Hualan Biological Engineering Inc.

- 6.3.10 Kedrion Biopharma

- 6.3.11 Medxbio Pte Ltd.

- 6.3.12 Merck KGaA (Sigma-Aldrich)

- 6.3.13 Novozymes A/S

- 6.3.14 Octapharma AG

- 6.3.15 Shanghai RAAS Blood Products Co., Ltd.

- 6.3.16 Takeda Pharmaceutical Company Limited

- 6.3.17 Thermo Fisher Scientific Inc.

- 6.3.18 Ventria Bioscience Inc.

- 6.3.19 ViruSure GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment