|

시장보고서

상품코드

2061616

자동차용 필름 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

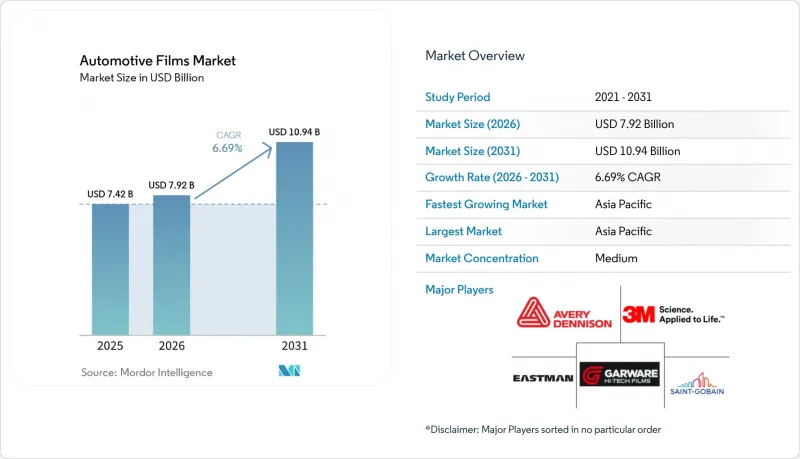

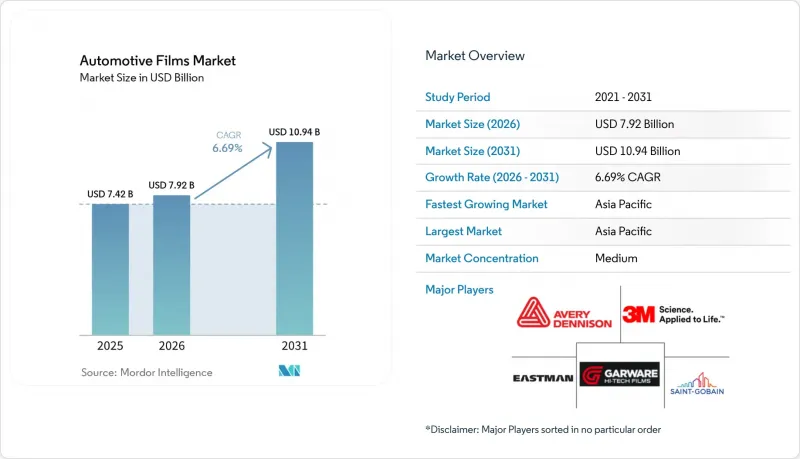

Mordor Intelligence에 의하면, 자동차용 필름 시장 규모는 2025년 74억 2,000만 달러로 평가되었습니다. 2026년에는 79억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 6.69%를 나타내, 2031년에는 109억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 필름 유형(윈도우 필름/틴트(염색, 메탈라이즈, 세라믹, 카본, 기타), 페인트 보호 필름, 랩핑 필름), 차종(승용차 및 상용차), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차용 필름 시장 동향과 분석

차량의 외관 미학과 표면 보호에 대한 수요 증가

고급차 소유주들은 돌튐이나 스월 마크로부터 차량을 보호하기 위한 수단으로 페인트 보호 필름(PPF)을 점점 더 중요하게 여기고 있습니다. 그들은 재판매 가치 상승의 가능성을 인식하고, 차체 전체에 시공하는 데 주저하지 않습니다. 2023년, 대규모 인수를 통해 200곳에 달하는 시공 거점으로 구성된 유통 네트워크가 즉시 구축되었으며, 외관 유지가 구매 결정에 큰 영향을 미치는 시장에서 입지를 강화했습니다. 이에 대응하여, 수명이 8-10년인 자가 복원형 필름이 출시되었습니다. 경쟁력 있는 가격 책정을 통해 기존 대형 기업들의 보증료를 상회하는 가격 책정이 가능해지면서, 유럽 내 경쟁 구도가 격화되고 있습니다. 독자적인 탑코트를 보유하지 않은 중소규모의 컨버터에게는 보증 기간 단축이 과제로 대두되고 있지만, 소비자에게는 선택의 폭이 넓어지고 가격 변동이 억제된다는 이점이 주어지고 있습니다. 그 결과, 자동차용 필름 시장은 바벨 구조로 진화하고 있습니다. 즉, 고급형과 보급형 솔루션이 번창하는 반면, 중급형 메탈라이즈드 제품은 점차 입지를 잃어가고 있습니다.

엄격한 차열 및 자외선 규제

미국 도로교통안전국(NHTSA)의 FMVSS 205는 미국 내 전면 유리의 가시광선 투과율(VLT)에 대한 최소 기준을 규정하고 있습니다. 이에 따라 유리를 어둡게 하지 않으면서도 적외선을 차단할 수 있는 나노 세라믹 필름 수요가 증가하고 있습니다. 한편, 유럽에서는 이러한 기준의 이행 상황에 차이가 있습니다. 예를 들어, 독일에서는 적외선 성능이 중시되는 반면, 스칸디나비아 국가들에서는 엄격한 가시광선 투과율(VLT) 검사에 중점을 두고 있습니다. 이러한 비일관성으로 인해 공급업체들은 지역별로 특화된 SKU(재고 관리 단위)를 생산하게 되었습니다. 특정 제품은 금속을 사용하지 않음으로써 무선 주파수 간섭을 방지하는 동시에, 총 태양에너지 차단에 있어 뛰어난 성능을 발휘하고 있습니다. 이러한 시장의 세분화는 배합의 유연성과 인증 프로그램을 모두 갖추고, 시공업체가 항상 최신 상태를 유지할 수 있도록 지원하는 수직 통합형 제조업체에게 유리하게 작용하고 있습니다. 한편, 중동에서는 특히 자외선(UV) 기준치에 관한 규제가 강화되기 시작했습니다. 이러한 움직임은 수요의 급증을 시사하며, 특히 폭염으로 고통받는 도시에서는 장시간 운행되는 카셰어링 차량의 부담을 줄이는 것을 목표로 하고 있습니다.

가시광선 투과율에 관한 규제 기준

시공 업체들은 FMVSS 205의 가시광선 투과율(VLT) 규정 및 주마다 상이한 규제로 인해 복잡한 상황에 직면해 있으며, 벌금 부과 위험을 감수해야 할 뿐만 아니라 많은 소비자가 선호하는 짙은 색상의 필름 사용이 제한되고 있습니다. 유럽 역시 비슷한 과제에 직면해 있으며, 스칸디나비아 국가들의 경찰은 규정을 준수하지 않는 필름을 단속하기 위해 도로변 검문에서 광도계를 적극적으로 활용하고 있습니다. 적외선을 차단하면서도 가시광선을 투과하는 세라믹 나노 입자 필름은 규제를 준수하는 해결책을 제공하지만, 염색 방식의 대체재에 비해 비용이 높아 보급이 저해되고 있습니다. 게다가, 금속 코팅 제품은 전파 간섭 문제를 안고 있어, 전자 요금 징수 시스템이나 GPS의 신뢰성이 최우선으로 요구되는 지역에서는 그 매력이 떨어지고 있습니다. 그 결과, 신흥 지역에서는 규제가 완화되는 반면, 성숙한 시장에서는 수익 창출 가능성이 한계에 다다르고 있습니다.

부문별 분석

2025년, 자동차용 필름 시장에서 윈도우 필름 및 착색 필름이 49.22%의 점유율을 차지하며 시장을 주도했습니다. 그러나 페인트 보호 필름 시장은 2031년까지 연평균 성장률(CAGR)이 7.12%를 나타낼 것으로 예측되며, 모든 카테고리를 능가하는 성장이 전망됩니다. 이러한 급속한 성장은 엔진의 열 사이클 동안 미세한 흠집을 능숙하게 제거하는 혁신적인 자가 복원형 TPU 기술에 힘입은 것입니다. 세라믹 윈도우 틴트는 프리미엄 시장에서 큰 점유율을 차지하고 있지만, 염색 필름에 비해 평방피트당 가격이 훨씬 비쌉니다. 이러한 가격 동향으로 인해 수익은 이러한 고사양 제품에 크게 쏠려 있습니다. 한편, 착색 필름은 프라이버시 유리의 부상으로 인해 그 존재감이 희미해지고 있다는 점과, 열 차단 능력이 제한적이라는 두 가지 과제에 직면해 있습니다. 한편, 메탈라이즈드 층은 5G 및 GPS에 대한 의존도가 높아짐에 따라 발생하는 RF 간섭 문제로 인해 시장 점유율이 하락하고 있습니다. 하이브리드 결정 필름은 비용과 성능의 균형이 뛰어나지만, 시장 보급에는 어려움을 겪고 있습니다. 이러한 한계는 시공자가 기술을 습득하기 어렵고, 단층 제품에 비해 작업 시간이 길어지기 때문입니다.

페인트 보호 필름은 시공 범위에 따라 딜러의 매출이 변동합니다. 이러한 수치와 기여 이익률을 종합해 보면, 업계 선두 기업들에게 안성맞춤인 표적이 됩니다. 탄소 함유 착색 필름은 전도성 문제를 해결하면서도, 염색 필름보다 높은 가격대에서 적절한 적외선 차단 성능을 제공하여 균형을 이루고 있습니다. 자동차 래핑 필름은 브랜드 인지도라는 경제적 이점을 활용하고 있습니다. 배송용 밴 1대가 하루에 수천 번의 노출 기회를 창출하기 때문에 특히 조달 팀이 디자인 템플릿을 승인할 경우, 사업자당 차량 도입 대수가 수백 대까지 급증할 가능성이 있습니다. 나노 세라믹 필름이 보급됨에 따라 공급업체들은 보증 기간을 10년 또는 지정 주행 거리까지 연장하고 있는데, 이는 다양한 기후 조건 하에서 제품의 변색 저항성과 접착 내구성에 대한 자신감을 보여주는 것이라고 할 수 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 44.43%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.02%를 나타낼 것으로 전망됩니다. 이러한 성장은 중국, 인도 및 동남아시아에서 농촌 지역의 자동차 보유가 확대되고 있는 데 힘입은 것입니다. 2024년, 중국 내 NEV(신에너지차) 판매 확대가 열 관리에 대한 수요 증가를 견인하고 있습니다. 이는 차내 온도를 낮출 수 있는 필름이 600km 배터리 팩의 주행 거리를 늘릴 가능성을 지니고 있기 때문입니다. 현재 인도의 체계화된 디테일링 시장은 잠재 고객층의 극히 일부만을 확보하고 있습니다. 그러나 2026년 2월에 출시된 가웨어사의 신제품(그래핀 세라믹 다층 키트)은 이러한 격차를 해소하는 것을 목표로 하고 있습니다. 이 키트들은 PPF(페인트 보호 필름), 코팅, 전면 유리 필름을 하나의 서비스로 매끄럽게 통합하고 있습니다. 한편, 일본과 한국은 OEM 채널에 주력하고 있습니다. 예를 들어, 린텍(Lintec)사가 전면 유리 필름을 공장 출하 시의 유리 포장에 포함시킴으로써 매출이 증가했으며, 가치가 조립 공장으로 크게 이동하고 있음이 드러나고 있습니다.

세계 매출에서 큰 비중을 차지하는 북미는 애프터마켓 PPF 및 세라믹 착색 필름 분야에서 차량당 지출액이 가장 높은 지역입니다. 그러나 성장 속도는 완만해지고 있습니다. 이러한 성장 둔화는 프라이버시 유리로 인해 착색 필름 수요가 감소하고 있으며, 각 주의 가시광선 투과율(VLT) 규제로 인해 차양 선택의 폭이 좁아지고 있기 때문으로 분석됩니다. 캐나다에서는 계절적 요인도 영향을 미치고 있어, 겨울철 도로 제설제 사용으로 인해 로커 패널용 PPF 수요가 증가하고 있습니다. 한편, 멕시코에서는 과나후아토주의 OEM 거점이 미국 수출 기준을 충족하기 위해 공장 출하 시 시공되는 착색 필름에 주력하고 있습니다. 3M의 운송·전자 부문은 2024년에 부진을 보였습니다. 그러나 PFAS(퍼플루오로알킬 물질) 관련 사업 철수의 영향을 제외하면, 해당 부문은 칭찬할 만한 유기적 성장을 보이고 있으며, 환경 규제 강화 속에서 비불소계 화학물질로의 전략적 전환이 진행되고 있다는 점이 강조되고 있습니다.

유럽은 시장에서 상당한 점유율을 차지하고 있지만, 지역 간 격차가 뚜렷합니다. 독일에서는 뒷유리의 짙은 색상이 허용되지만, 요금 징수 센서를 보호하기 위해 메탈릭 코팅의 사용은 제한되어 있습니다. 반면 영국에서는 앞유리에 특정 가시광선 투과율(VLT)을 의무화하고 있어, 사실상 대부분의 애프터마켓용 착색 필름이 배제되고 있습니다. 이스트먼사가 2026년 헨트에서 진행할 투자는 전면 유리 라미네이션 공정 중에 필름 기판을 통합하는 것을 목적으로 하며, 애프터마켓의 잠재적 축소에 대한 완충 역할을 수행할 것입니다. 브라질, 사우디아라비아, 남아프리카공화국을 합치면, 전 세계 매출에서 차지하는 비중은 작지만 중요한 부분을 차지하고 있습니다. 리야드나 제다와 같은 사우디아라비아의 도시에서는 무더위로 인해 적외선(IR) 차단 필름에 대한 수요가 증가하고 있습니다. 그러나 검사 기준이 완만하기 때문에 유럽보다 색상이 진한 필름이 허용되고 있으며, 이는 수익성이 높은 나노 세라믹 필름 수입에 있어 호재가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 동향

KTH 26.06.19According to Mordor Intelligence, the automotive films market size is expected to grow from USD 7.42 billion in 2025 to USD 7.92 billion in 2026 and is forecast to reach USD 10.94 billion by 2031 at a 6.69% CAGR over 2026-2031.

This report is Segmented by Film Type (Window Films/Tints [Dyed, Metallized, Ceramic, Carbon, and Other], Paint Protection Films, and Wrapping Films), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Films Market Trends and Insights

Rising Demand for Vehicle Aesthetics and Surface Protection

Owners of premium vehicles are increasingly viewing Paint Protection Film (PPF) as a safeguard against stone chips and swirl marks. They're willing to invest in full-body installations, recognizing the potential boost in resale value. In 2023, a major acquisition established an immediate distribution network spanning 200 installer hubs, propelling presence in a market where cosmetic preservation heavily influences purchasing decisions. In response, a self-healing film with a lifespan of 8 to 10 years was launched. Priced competitively, it undercuts the warranty premiums of established players, intensifying the competitive landscape in Europe. While warranty compression poses challenges for smaller converters without proprietary top coats, consumers are reaping the rewards with a wider selection and reduced price variability. As a result, the automotive films market is evolving into a barbell structure: luxury-grade and entry-grade solutions are flourishing, while mid-tier metallized variants are fading into obscurity.

Stringent Heat-Reduction and UV Regulations

The NHTSA's FMVSS 205 mandates a minimum visible light transmission (VLT) for front windshields in the U.S. This drives up the demand for nano-ceramic films, which can reject infrared radiation without darkening the glass. In Europe, enforcement of these standards is inconsistent. For instance, while Germany places a premium on infrared performance, Scandinavian countries focus on stringent VLT checks. This inconsistency has led suppliers to produce jurisdiction-specific stock-keeping units (SKUs). A specific product avoids radio-frequency interference by not using metals, yet it achieves commendable rejection of total solar energy. Such market fragmentation benefits vertically integrated producers who possess both formulation flexibility and certification programs, ensuring their installers remain updated. Meanwhile, the Middle East has started tightening regulations, particularly on UV thresholds. This move indicates a burgeoning demand, especially as cities, grappling with extreme heat, aim to alleviate stress on rideshare fleets operating for extended hours.

Visible-Light-Transmission Regulatory Limits

Installers face a complex landscape due to FMVSS 205's VLT rule and varying state regulations, risking fines and limiting the darker shades favored by many consumers. Europe faces similar hurdles; Scandinavian police actively use photometers in roadside checks to combat non-compliant films. While ceramic nano-particle films, blocking infrared radiation and transmitting visible light, offer a compliant solution, their higher cost compared to dyed alternatives stifles widespread adoption. Additionally, metallized products grapple with signal interference, diminishing their appeal in areas where e-toll and GPS reliability is paramount. As a result, while emerging regions ease regulations, mature markets see their revenue potential capped.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Vehicle-Parc Growth Across Asia-Pacific

- Shift From Repainting to Color-Change Wraps

- Volatile PET and TPU Raw-Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, window films and tints dominated the automotive films market, claiming a 49.22% share. Paint protection films, however, are set to outpace all categories with a projected 7.12% CAGR through 2031. This surge is driven by the innovative self-healing TPU technology, which adeptly removes micro-scratches during engine heat cycles. Ceramic window tints, while holding a significant stake in premium sales, command prices per square foot that are significantly higher than their dyed counterparts. This pricing dynamic skews revenue heavily towards these high-spec formulations. Dyed films face a dual challenge: they are overshadowed by the rise of privacy glass and their limited heat rejection capabilities. On the other hand, metallized layers are losing ground due to RF interference issues, which conflict with the growing reliance on 5G and GPS. Hybrid crystalline films, though they offer a balance of cost and performance, struggle to penetrate the market significantly. This limitation is attributed to the steeper learning curve for installers, which extends job times compared to single-layer products.

Paint protection films boast dealer ticket sizes that vary depending on coverage. These figures, coupled with their contribution margins, make them prime targets for industry giants. Carbon-infused tints strike a balance, offering moderate IR blockage at a premium over dyed films, all while sidestepping conductivity issues. Automotive wrapping films tap into the economics of brand visibility. With each delivery van racking up thousands of daily impressions, fleet roll-outs can soar to hundreds of units per operator, especially once procurement teams greenlight design templates. As nano-ceramic films gain traction, suppliers are bolstering their warranties to a decade or a specified mileage, a testament to their faith in the product's fade resistance and adhesive durability across varied climates.

Geography Analysis

Asia-Pacific anchors 44.43% of 2025 revenue and is forecast to post a 7.02% CAGR to 2031. This growth is driven by China, India, and Southeast Asia expanding vehicle ownership into rural areas. In 2024, China's sales of NEVs (New Energy Vehicles) are spurring a heightened demand for thermal management. This is because films that can reduce cabin temperatures potentially extend the vehicle's range on a 600-km battery pack. Currently, India's organized detailing market taps into a small fraction of its potential clientele. However, Garware's upcoming launch in February 2026, featuring graphene-ceramic multi-layer kits, aims to bridge this gap. These kits seamlessly integrate PPF, coatings, and windshield films into a singular service. Meanwhile, Japan and South Korea are honing in on OEM channels. For instance, LINTEC's integration of windshield films into factory glazing packages has bolstered its turnover, highlighting a significant shift of value towards assembly plants.

North America, contributing a substantial share to global revenue, boasts the highest per-vehicle expenditure on aftermarket PPF and ceramic tints. However, growth is tapering to a moderate pace. This slowdown is attributed to privacy glass diminishing the demand for dyed films and state VLT regulations limiting shade options. Seasonal dynamics play a role in Canada, where winter road salt boosts PPF demand on rocker panels. Concurrently, in Mexico, OEM hubs in Guanajuato are delving into factory-applied tints to align with U.S. export standards. 3M's Transportation and Electronics segment faced a dip in 2024. Yet, when excluding the impacts of PFAS exits, the segment showcases commendable organic growth, emphasizing a strategic shift towards non-fluorinated chemistries amidst tightening environmental regulations.

Europe, while contributing a notable share to the market, reveals pronounced regional disparities. Germany allows darker shades on rear windows but limits metallized layers to safeguard toll-collection sensors. In contrast, the UK mandates a specific VLT on windscreens, effectively sidelining most aftermarket tints. Eastman's 2026 investment in Ghent aims to embed film substrates during windshield lamination, serving as a buffer against potential aftermarket declines. Collectively, Brazil, Saudi Arabia, and South Africa account for a small but significant portion of global revenue. In Saudi cities like Riyadh and Jeddah, extreme heat drives demand for IR-blocking films. However, lenient inspection practices permit darker shades than those in Europe, presenting an opportunity for higher-margin nano-ceramic imports.

- 3M

- ADS Window Films Ltd.

- All Pro Window Films

- Avery Dennison Corporation

- Eastman Chemical Company

- FILMTACK PTE LTD.

- Garware Suncontrol Film

- Global Window Films

- HEXIS SAS

- Johnson Window Films Inc.

- LINTEC Corporation

- Nexfil USA

- Saint-Gobain

- Sun Tint

- TORAY INDUSTRIES INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising demand for vehicle aesthetics and surface protection

- 4.1.2 Stringent heat-reduction and UV regulations

- 4.1.3 Rapid vehicle-parc growth across Asia-Pacific

- 4.1.4 Shift from repainting to color-change wraps

- 4.1.5 Commercialisation of smart electro-chromic window films

- 4.2 Restraints

- 4.2.1 Visible-light-transmission (VLT) regulatory limits

- 4.2.2 Volatile PET and TPU raw-material prices

- 4.2.3 Factory-fitted tinted glass reducing aftermarket demand

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Film Type

- 5.1.1 Window Films/Tints

- 5.1.1.1 Dyed Window Tint

- 5.1.1.2 Metallized Window Tint

- 5.1.1.3 Ceramic Window Tint

- 5.1.1.4 Carbon Window Tint

- 5.1.1.5 Other Window Films/ Tints (Hybrid, Crystalline, etc.)

- 5.1.2 Automotive Paint Protection Films

- 5.1.3 Automotive Wrapping Films

- 5.1.1 Window Films/Tints

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Commercial Vehicles

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 ADS Window Films Ltd.

- 6.4.3 All Pro Window Films

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Eastman Chemical Company

- 6.4.6 FILMTACK PTE LTD.

- 6.4.7 Garware Suncontrol Film

- 6.4.8 Global Window Films

- 6.4.9 HEXIS SAS

- 6.4.10 Johnson Window Films Inc.

- 6.4.11 LINTEC Corporation

- 6.4.12 Nexfil USA

- 6.4.13 Saint-Gobain

- 6.4.14 Sun Tint

- 6.4.15 TORAY INDUSTRIES INC.

7 Market Opportunities and Future Trends

- 7.1 White-space and Unmet-Need Assessment