|

시장보고서

상품코드

2061619

항공기 화물 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Cargo Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

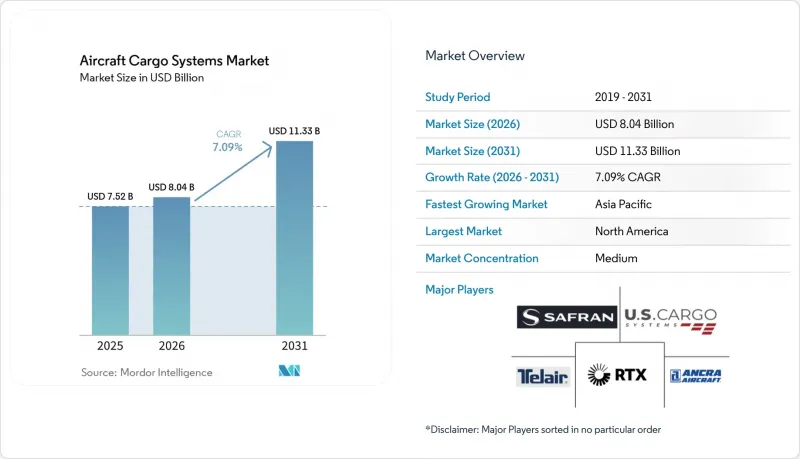

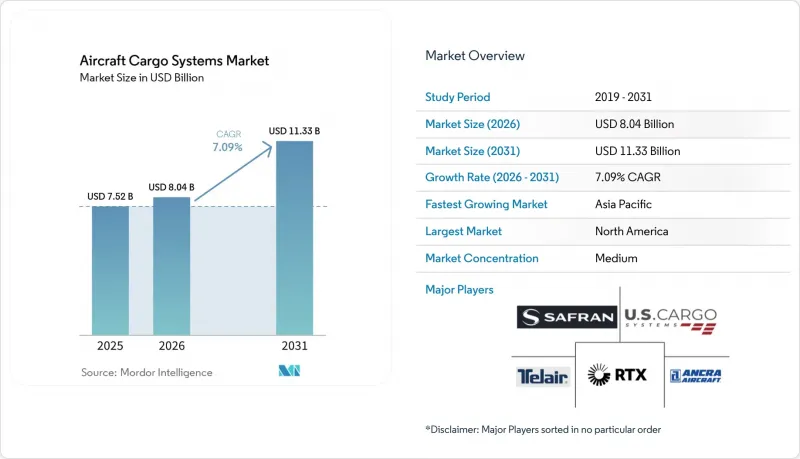

Mordor Intelligence에 의하면, 항공기 화물 시스템 시장 규모는 2025년 75억 2,000만 달러로 평가되었고, 2026년에는 80억 4,000만 달러로 추정되고, 2026-2031년 CAGR 7.09%로 성장을 지속할 전망이며, 2031년까지 113억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(화물 적재 시스템 및 기내 화물 장비), 항공기 유형별(민간 항공기, 군용기 및 일반 항공기), 최종 사용자별(OEM 및 애프터마켓), 그리고 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카) 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공 화물 시스템 시장 동향 및 분석

전용 화물기로의 개조가 급증하고 있습니다.

2025년에는 2020년대 후반에 걸쳐 신규 화물기 인도 지연으로 인한 수송 능력 부족을 메우려는 항공사들의 움직임에 힘입어 개조 작업이 활발해졌습니다. 운항사 및 통합업체들은 좁은 동체 노선에서는 B737-800BCF 및 A321P2F 프로그램으로, 고밀도 노선에서는 B777-300ER 기반 프로그램으로 중점을 옮기면서, 화물 적재용 하드웨어 및 내장 부품에 대한 수요가 집중되었습니다. 규제 및 공급망의 시기가 여전히 제약 요인으로 작용하고 있어, 일부 대형 와이드바디 항공기의 STC(특별형식인증)가 2026년 승인을 목표로 하고 있을 뿐만 아니라, 리드타임이 긴 부품들로 인해 개조 일정이 지연되고 있습니다. 또한, 리스 계약 연장으로 인해 부품 공급용 항공기 수가 감소하면서 기체 가격이 상승했고, 노선 차원의 세심한 계획이 필요해짐에 따라 원자재의 경제성도 악화되었습니다. 와이드바디 기종의 생산 여력이 한계에 달했고, 당분간 B777F가 대형 화물기의 역할을 맡게 될 예정인 만큼, 개조는 전체 기단을 아우르는 시스템 개량 및 업그레이드를 뒷받침하는 기반이 되고 있습니다.

시간 지정 항공 화물이 필요한 크로스보더 전자상거래의 성장

소매업체와 플랫폼들이 장거리 노선에서 24-48시간 내 확실한 배송 시간을 요구하는 가운데, 전자상거래의 흐름이 항공 화물의 역할을 더욱 확대시켰습니다. 2025년 중반 미국의 정책 변경으로 중국발 화물 흐름이 재편된 후, 운송 능력과 재고는 유럽행 노선으로 이동했으며, 항공사들은 아시아-유럽 노선에서 높은 탑승률을 기록했습니다. IATA는 2025년 유럽 및 아시아 노선의 화물 수송량이 힘차게 회복된 추세를 파악하고 있으며, 이는 수요가 집중되는 지역으로 화물기를 신속하게 재배치한 항공사들의 기동력 덕분입니다. 2026년에 예정된 유럽의 저가 화물 관련 정책 조정에 따라 규정 준수에 대한 중요성이 더욱 부각될 전망이며, 이는 속도와 추적성을 중시하는 혼재 운송을 촉진할 것으로 보입니다. 항공사와 공항은 처리 시간을 단축하기 위해 디지털화와 추적 시스템에 대한 투자를 확대하고 있으며, 이를 통해 새로운 무역 경로에서 화물량이 정상화되는 상황에서도 항공 네트워크는 서비스 수준을 유지할 수 있게 됩니다.

제트유 가격 변동이 항공사의 이익률을 압박하고 있습니다.

2026년 초까지 제트유 가격이 급등하면서 항공사 및 화물기의 영업이익률에 압박을 가하고, 재량적 개조 투자 여지를 좁히고 있습니다. 분쟁 지역을 우회하기 위한 경로 조정으로 인해 많은 장거리 노선의 비행 거리가 늘어나고, 연료 소비량이 증가하여 주요 항공 회랑의 실질적인 수송 능력이 저하되고 있습니다. 규제에 따른 탄소 배출 프로그램과 지속 가능한 항공 연료의 도입으로 인해 항공사의 평균 연료비는 상승하고 있으며, 현물 가격이 정점에서 하락하더라도 비용 압박은 여전히 높은 수준을 유지할 것으로 보입니다. IATA는 2024년과 2025년에 규정 준수 및 지속가능성 관련 비용이 증가할 것이라고 지적했으며, 2026년에는 더 많은 노선이 해당 제도의 적용 대상이 될 예정이므로 이러한 추세는 계속해서 중요한 이슈가 될 것입니다. 이러한 연료비 및 규제 동향에 따라 항공사들은 자본 투자 프로젝트의 속도를 조절하고, 신뢰성 향상이나 정비 소요 시간 단축과 같이 투자 회수 기간이 더 짧은 업그레이드를 우선시하고 있습니다.

부문별 분석

화물 적재 시스템은 2025년에 51.67%의 시장 점유율을 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.76%로 성장할 것으로 전망됩니다. 이는 표준화된 ULD(유닛 적재 컨테이너) 취급을 위한 롤러 트랙, 볼 매트, 잠금 장치의 현대화가 전체 기단에서 최우선 과제로 자리 잡고 있음을 반영합니다. 이 부문은 항공사들이 가동 중단 시간을 단축하고 수요 급증 시 유연한 스케줄링이 가능하도록 퀵 체인지 구성을 도입하는 추세에 힘입어 호황을 누리고 있습니다. 시장 점유율 48.33%를 차지하는 기내 화물 시설은 특히 의약품 및 고가 화물의 운송에 있어 엄격한 방화 안전 및 온도 관리 요건을 충족하고 있습니다. 온도 관리 모듈, 라이너 업그레이드 및 규정을 준수하는 화재 감지 시스템은 장거리 노선에서 일관된 서비스 수준을 뒷받침하고 있습니다. 팔레트 및 컨테이너 취급의 표준화는 램프 시간을 단축하고 회전 성능을 향상시켜, 이를 통해 항공사는 혼잡한 노선에서 항공기 이용률을 높이고 있습니다. 디지털 모니터링 및 중량·균형 분석이 운항 업무에 도입됨에 따라, 규정 준수 수준이 향상되고 화물이 빈번하게 이동하는 허브 공항에서의 인적 오류가 감소하고 있습니다.

항공기 화물 시스템 시장에서는 전동 액추에이터 및 복합재료 부품으로의 전환이 꾸준히 진행되고 있으며, 이를 통해 바닥, 그물망, 화물문 등의 경량화가 가능해졌습니다. 또한, 각 항공사는 유지보수 및 재고 데이터를 통합된 관제탑으로 전송하는 RFID 및 센서가 탑재된 하드웨어의 도입도 추진하고 있습니다. 화물칸 및 라이너 인증 체계에 따라, B737-800BCF 및 A321P2F 등 현역 기종을 포함한 기체군에서 지속적인 업그레이드 주기가 추진되고 있습니다. 항공사들은 기내 외관 개선보다는 회전 시간 단축 및 정비 빈도 감소를 통해 비용을 절감할 수 있는 화물 서브시스템에 투자하고 있습니다. 여러 허브에서 혼합 기단을 운영하는 항공사에게 있어, 지상 설비와의 상호 운용성은 여전히 중요한 선정 기준입니다. IATA의 CEIV 기준과 항공 적합성 지침은 조달 체크리스트를 구성하고 있으며, 이로 인해 라인 핏 및 레트로핏 솔루션에 대한 기술적 장벽이 높아지고 있습니다.

지역별 분석

2025년에는 항공사 및 방위 프로그램이 높은 가동률과 꾸준한 업그레이드 주기를 유지함에 따라 북미가 42.53%로 1위를 차지했습니다. 북미 항공 화물 시스템 시장 규모는 전술적 및 전략적 플랫폼에서의 시스템 신뢰성, 표준화된 팔레트, 그리고 더욱 안전한 화물칸에 대한 지속적인 투자를 반영하고 있습니다. 미국과 캐나다 전역에서는 자격을 갖춘 인력과 인증에 대한 전문 지식이 처리 능력을 뒷받침하고 있으며, 개조 및 MRO 생태계는 계속해서 견조한 모습을 보이고 있습니다. 2026년에는 규제 당국이 관제 구역 내 시야 외(BVLOS) 운항을 위한 길을 단계적으로 열어줌에 따라, 드론 및 eVTOL의 시험 운용이 지속적으로 확대되었습니다. 상업용 화물기 네트워크는 특송 및 전자상거래 노선에 중점을 두고, 회전 시간과 신뢰성을 향상시키기 위한 시스템 업그레이드가 이루어졌습니다. 이 지역의 방위 유지 예산은 광범위하게 책정되어, 가혹한 환경에서 운용되는 수송기의 바닥, 안전벨트 및 라이너에 대한 유지보수 작업을 지원하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 7.32%로 가장 빠르게 성장하고 있는 지역이며, 전자상거래 시장 확대, 항공기 개조 능력, 그리고 방위용 항공기 증강이라는 혜택을 누리고 있습니다. 개조된 협폭동체 항공기는 아시아 지역 내의 고밀도 노선망을 뒷받침하는 한편, 대형 광폭동체 항공기는 유럽 및 중동으로 향하는 주요 노선을 담당하고 있습니다. 화물 드론의 도입은 2025년 중국에서 인증을 받은 플랫폼이 운항을 시작하면서 진전을 보였으며, 도시 지역 내 배송 및 외딴 지역의 물류 분야에서 새로운 활용 사례가 등장했습니다. 지역별 MRO(정비·수리·오버홀) 및 개조 활동이 지속적으로 확대됨에 따라, 개별 화물 사양에 맞춘 롤러 및 고정 장치의 업그레이드를 처리할 수 있는 현지 역량이 강화되었습니다. 정부와 공항은 화물 처리 과정의 디지털화에 주력하여, 주요 관문에서의 처리 시간이 단축되는 속도가 빨라졌습니다. 각 항공사가 수송 능력을 확대하고 노선을 다양화함에 따라, 연료 효율과 운항 신뢰성 간의 균형을 맞추기 위해 더욱 가볍고 스마트한 화물 시스템의 도입이 진행되고 있습니다.

유럽은 전자상거래 허브, 특송 통합 사업자, 그리고 운송 차량을 강화하는 방위 재군비에 힘입어 여전히 큰 시장 점유율을 유지하고 있습니다. 주요 화물 공항들은 자동화 및 디지털 추적 시스템에 투자함으로써, 더욱 엄격해진 규정 준수 체계 하에서도 처리량이 증가했습니다. 중형 수송기를 포함한 전술·전략 공수기 조달에 힘입어, 팔레타이징, 고정 장치, 방화 시스템 관련 공급업체들의 수주 실적이 호조를 유지하고 있습니다. 유럽 각국의 규제 인증 절차가 복잡해지면서 신시스템 도입 일정이 계속 지연되고 있으며, 이는 첨단 작동·감시 시스템의 구축 계획에 영향을 미치고 있습니다. 항공기 제조업체(OEM)는 기단 교체 주기를 계획하는 항공사들에게 여전히 주목받고 있습니다. 또한, 컨소시엄 프로그램을 통한 혼합 기단이라는 유럽의 구조 역시 예측 기간 동안 꾸준한 개조 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약 및 주요 조사 결과

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the aircraft cargo systems market size is expected to grow from USD 7.52 billion in 2025 to USD 8.04 billion in 2026 and is forecasted to reach USD 11.33 billion by 2031 at a 7.09% CAGR over 2026-2031.

This report is Segmented by Product Type (Cargo Loading Systems and Interior Cargo Fittings), Aircraft Type (Commercial Aircraft, Military Aircraft, and General Aviation Aircraft), End User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Cargo Systems Market Trends and Insights

Surge in Dedicated Freighter Conversions

Conversion activity strengthened in 2025 as airlines sought to cover capacity gaps caused by delays in new-build freighter deliveries into the late 2020s. Operators and integrators pivoted to B737-800BCF and A321P2F programs on narrowbody routes and to B777-300ER-based programs on high-density lanes, concentrating demand for cargo-loading hardware and interior fittings. Regulatory and supply-chain timing remains the gating factor as several large widebody STCs target 2026 decisions and long-lead items stretch conversion calendars. Feedstock economics also tightened as lease extensions reduced the number of aircraft available for part-out, raising airframe prices and requiring closer route-level planning. With widebody production slots constrained and the B777F covering the large freighter role in the near term, conversions are underpinning system retrofits and upgrades across fleets.

Growth of Cross-Border E-Commerce Requiring Time-Definite Air Cargo

E-commerce dynamics accelerated air cargo's role as retailers and platforms sought reliable 24-48 hour delivery windows across long-haul corridors. After policy changes in the US reshaped flows from China in mid-2025, capacity and inventory shifted into Europe-bound channels, where carriers reported higher load factors on Asia-Europe lanes. IATA tracked a strong rebound in 2025 cargo traffic on Europe-Asia routes, reflecting airlines' agility in redeploying freighters to demand hotspots. European policy adjustments planned for 2026 on low-value shipments are set to raise compliance emphasis, which supports consolidated air moves that favor speed and traceability. Carriers and airports are extending digital and tracking investments that compress processing timelines, allowing air networks to hold service levels while volumes normalize along new trade lanes.

Volatile Jet-Fuel Prices Compressing Airline Margins

Jet fuel prices rose sharply through early 2026, putting pressure on airline and freighter operating margins and narrowing the room for discretionary retrofit spending. Route adjustments around conflict zones add miles to many long-haul charts, increasing consumption and reducing effective capacity on key corridors. Regulatory carbon programs and the introduction of sustainable aviation fuel raise carriers' average fuel bills, keeping cost pressure elevated even if spot prices ease from their peaks. IATA has outlined higher compliance and sustainability costs during 2024 and 2025, which remain relevant as more routes fall under the scheme in 2026. These fuel and compliance dynamics prompt carriers to pace capital projects and to prioritize upgrades that deliver faster payback in reliability and turnaround time.

Other drivers and restraints analyzed in the detailed report include:

- Rising Defense Spending on Rapid-Deploy Logistics Aircraft

- OEM Shift Toward Lighter, Electric Floor-Actuated Systems

- Limited Widebody Production Slots Through 2030

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cargo loading systems captured 51.67% share in 2025 and are projected to grow at 7.76% CAGR through 2031, reflecting fleet-wide priorities to modernize roller tracks, ball mats, and locking mechanisms for standardized ULD handling. This segment benefits from the conversion wave as airlines specify quick-change configurations that compress downtime and support flexible scheduling during demand spikes. Interior cargo fittings at 48.33% share address stringent fire safety and thermal control requirements, particularly in pharmaceutical and high-value shipments. Temperature-controlled modules, liner upgrades, and compliant fire detection support consistent service levels on long-haul missions. Standardization in pallet and container handling reduces ramp time and improves turn performance, which carriers translate into higher aircraft utilization on busy corridors. Digital monitoring and weight-and-balance analytics flow into line operations to improve compliance and reduce manual error in high-velocity hubs.

The aircraft cargo systems market continues to see a progressive shift toward electric actuation and composite components, enabling lighter floors, nets, and cargo doors. Airlines are also introducing RFID and sensor-enabled hardware that feeds maintenance and inventory data into unified control towers. Certification frameworks for cargo compartments and liners drive rolling upgrade cycles, including for B737-800BCF and A321P2F fleets in commercial service. Operators route capital to cargo subsystems that deliver cost savings with faster turns and fewer maintenance events rather than aesthetic cabin upgrades. Interoperability with ground equipment remains a critical selection criterion for carriers operating mixed fleets across multiple hubs. IATA CEIV standards and airworthiness directives shape procurement checklists, which raise the technical bar for linefit and retrofit solutions.

Geography Analysis

North America led with 42.53% in 2025 as carriers and defense programs sustained high utilization and steady upgrade cycles. The aircraft cargo systems market size in North America reflects consistent investment in system reliability, standardized pallets, and safer cargo compartments on tactical and strategic platforms. Conversion and MRO ecosystems remain strong across the US and Canada, where qualified labor and familiarity with certifications support throughput. Drone and eVTOL pilots continued to expand in 2026 as regulators incrementally opened pathways for beyond-visual-line-of-sight (BVLOS) operations within controlled areas. Commercial freighter networks focused on express and e-commerce lanes, with system upgrades to improve turnaround and reliability. Defense sustainment budgets in the region are broad-based and support floor, restraint, and liner workscopes on transports operating in austere environments.

Asia-Pacific is the fastest-growing region, with a 7.32% CAGR, and benefits from e-commerce scale, conversion capacity, and expanding defense fleets. Converted narrowbodies support dense intra-Asia networks, while larger widebodies handle trunk routes into Europe and the Middle East. Cargo drone adoption advanced with certified platforms entering service in China in 2025, which opened new use cases in urban delivery and remote logistics. Regional MRO and conversion activity continued to grow, extending local capacity to handle package-specific roller and restraint upgrades. Governments and airports focused on digital cargo processes, which accelerated cycle times at major gateways. As carriers add capacity and diversify routes, they specify lighter and smarter cargo systems to balance fuel efficiency with service reliability.

Europe maintains a significant share supported by e-commerce hubs, express integrators, and defense rearmament that reinforces transport aircraft fleets. Major cargo airports invested in automation and digital traceability, which lifted throughput under stricter compliance regimes. Procurement of tactical and strategic airlift, including medium transports, has kept supplier order books active for palletization, restraints, and fire safety systems. Certification complexity across European jurisdictions continues to extend timelines for new systems, which shapes rollout calendars for advanced actuation and monitoring. OEMs remain a focus for airlines planning replacement cycles. Europe's structure of mixed fleets across consortium programs also sustains steady retrofit demand through the forecast period.

- Telair International GmbH

- Collins Aerospace (RTX Corporation)

- Safran SA

- Ancra International, LLC

- Cargo Systems, Inc.

- Davis Aircraft Products Co.

- KieTek International, Inc.

- Onboard Systems International, LLC

- CEF Industries, LLC.

- U.S. Cargo Systems

- AAR CORP.

- Honeywell International Inc.

- Pemco Conversions (Air Transport Services Group, Inc.)

- Aircraft Cabin Modification GmbH

- Elektro-Metall Export GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of cross-border e-commerce requiring time-definite air cargo

- 4.2.2 Surge in dedicated freighter conversions

- 4.2.3 Rising defense spending on rapid-deploy logistics aircraft

- 4.2.4 OEM shift toward lighter, electric floor-actuated systems

- 4.2.5 AI-enabled predictive maintenance reducing AOG time

- 4.2.6 Formation of cargo-focused eVTOL/ UAV ecosystems

- 4.3 Market Restraints

- 4.3.1 Volatile jet-fuel prices compressing airline margins

- 4.3.2 Limited widebody production slots through 2030

- 4.3.3 Lengthy certification cycles for new cargo hardware

- 4.3.4 High up-front retrofit CAPEX for legacy fleets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Cargo Loading Systems

- 5.1.2 Interior Cargo Fittings

- 5.2 By Aircraft Type

- 5.2.1 Commercial Aircraft

- 5.2.1.1 Narrowbody Passenger Aircraft

- 5.2.1.2 Widebody Passenger Aircraft

- 5.2.1.3 Freighter Aircraft

- 5.2.1.4 Regional Jets

- 5.2.2 Military Aircraft

- 5.2.2.1 Military Transport/Cargo Aircraft

- 5.2.3 General Aviation Aircraft

- 5.2.3.1 Cargo eVTOL and Large UAV

- 5.2.1 Commercial Aircraft

- 5.3 By End User

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telair International GmbH

- 6.4.2 Collins Aerospace (RTX Corporation)

- 6.4.3 Safran SA

- 6.4.4 Ancra International, LLC

- 6.4.5 Cargo Systems, Inc.

- 6.4.6 Davis Aircraft Products Co.

- 6.4.7 KieTek International, Inc.

- 6.4.8 Onboard Systems International, LLC

- 6.4.9 CEF Industries, LLC.

- 6.4.10 U.S. Cargo Systems

- 6.4.11 AAR CORP.

- 6.4.12 Honeywell International Inc.

- 6.4.13 Pemco Conversions (Air Transport Services Group, Inc.)

- 6.4.14 Aircraft Cabin Modification GmbH

- 6.4.15 Elektro-Metall Export GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment