|

시장보고서

상품코드

2061626

경도 외상성뇌손상 치료 시장: 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mild Traumatic Brain Injury Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

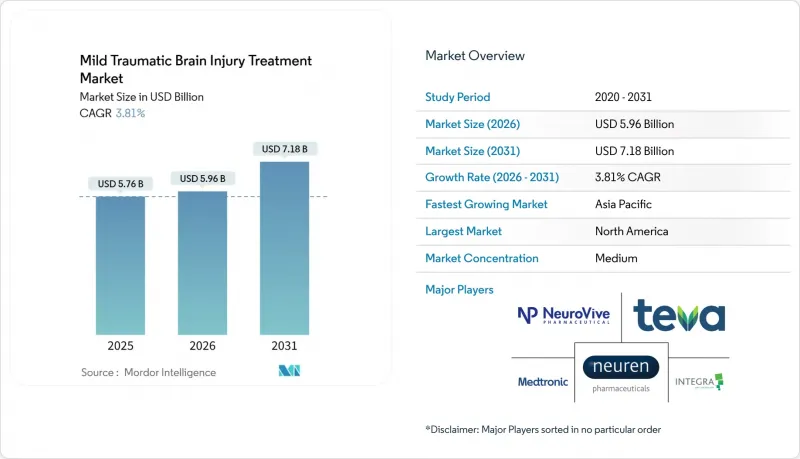

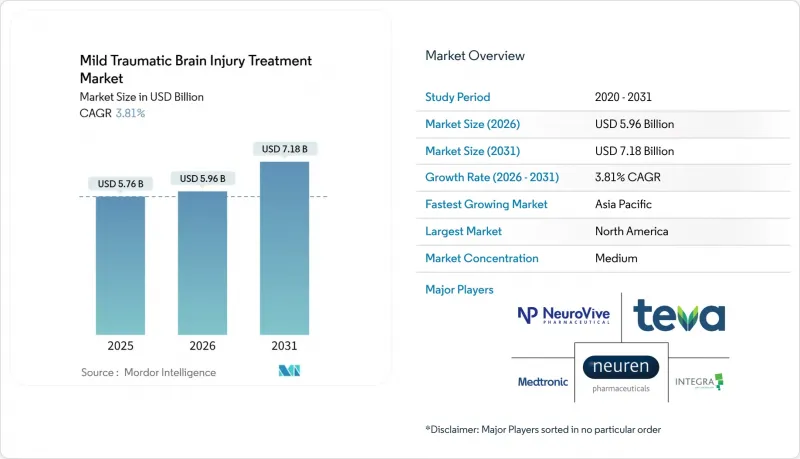

Mordor Intelligence에 의하면, 경도 외상성뇌손상 치료 시장 규모는 2025년 57억 6,000만 달러로 평가되었고, 2026년에는 59억 6,000만 달러로 추정되고, 2026-2031년 CAGR 3.81%로 성장을 지속할 전망이며, 2031년까지 71억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 치료 유형별(약물 요법, 외과적 개입, 재활 및 보조 기술), 외상 원인별(낙상, 자동차 사고 등), 최종 사용자별(병원 및 외상 센터 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 경도 외상성뇌손상(mTBI) 치료 시장 동향 및 인사이트

낙상 및 도로 교통사고로 인한 경도 외상성뇌손상(mTBI) 발생률 증가

낙상 및 자동차 사고는 전 세계적으로 경도 외상성뇌손상(mTBI)의 70% 이상을 차지하지만, 그 역학적 양상은 소득 수준에 따라 다릅니다. 북미, 유럽 및 일본에서는 노인의 낙상이 병원 입원의 주요 원인이 되는 반면, 인도, 중국 및 사하라 이남 아프리카에서는 생산 연령층이 도로 교통사고의 피해를 입고 있습니다. 세계보건기구(WHO)는 2023년에 도로 교통사고로 인한 사망자가 119만 명에 달했으며, 2,000만-5,000만 명의 생존자 중 최대 절반이 두부 외상을 입은 것으로 추정하고 있습니다. 일본에서는 2020-2024년 75세 이상 시민의 낙상 관련 두부 외상으로 인한 입원 건수가 31% 증가한 것으로 보고되었습니다. 이러한 추세로 인해, 발병 후 1시간 이내에 환자를 경과 관찰, 영상 진단 또는 뇌신경외과적 치료로 이끄는 신속한 분류 도구에 대한 수요가 높아지고 있습니다.

첨단 영상 진단 및 혈액 검사를 통한 진단법의 급속한 보급

현장 진단(POC) 바이오마커 패널은 응급실의 경제성을 근본적으로 변화시키고 있습니다. FDA의 승인을 받아 메디케어에서 검체당 135달러를 보상받는 애보트의 i-STAT TBI 검사는 2024년 조사 대상이었던 미국 내 11개 병원에서 CT 검사 사용량을 38% 줄이고, 평균 입원 시간을 4.2시간에서 2.8시간으로 단축했습니다. 군용 프로토타입은 견고하고 고속이라는 점이 입증되었으며, 2025년 전방 외과 팀에서 92%의 민감도와 87%의 특이도를 보였습니다. 유럽 규제 당국이 2027년까지 동반진단 승인 절차를 통일하는 방향으로 나아가고 있기 때문에 현재 보험 급여의 확실성이 도입의 중요한 원동력이 되고 있습니다.

FDA 승인을 받은 질병 수정 치료법의 부재

FDA는 아직 TBI에 대한 질병 수정 치료제의 승인을 하지 않았으며, 미국 내 처방약은 대증요법제로만 제한되어 있어 성장 가능성이 제한적입니다. 2025년, 전 세계적으로 경도 외상성뇌손상(mTBI) 치료제 후보물질 중 2/3상 임상시험 단계에 있는 것은 불과 14건에 불과한 반면, 알츠하이머병 치료제는 87건에 달했고, 투자자들의 신중한 태도가 두드러지게 나타나고 있습니다. CMS(미국 의료보험 및 의료서비스 센터)는 임상시험용 의약품에 대한 보험 적용을 허용하지 않아, 조기 도입을 목표로 하는 병원들의 의욕을 꺾고 있습니다.

부문별 분석

2025년, 경도 외상성뇌손상(mTBI) 치료 시장에서 약물 요법은 63.02%의 점유율을 차지했습니다. 이는 환자 수가 많고, 보험이 적용되는 대증요법 때문인 것입니다. 그러나 질병 진행 억제제가 없어 성장세가 주춤하고 있으며, 보험사는 처방 횟수가 아닌 기능 회복을 평가하는 포괄 지급 제도의 도입을 모색하고 있습니다. 재활 및 보조 기술 시장은 규모가 작지만, 2031년까지 연평균 성장률(CAGR) 5.85%로 성장할 것으로 전망됩니다. 이는 원격의료 인프라의 정착과, 자립 보행까지 걸리는 기간을 평균 18일 단축하는 로봇 플랫폼에 힘입은 것입니다. 외과적 개입은 혈종 제거나 난치성 두개내압 상승증에 대한 특수한 치료법에 그치고 있으며, 트리아지 개선으로 불필요한 처치가 억제되고 있어 그 비중은 안정적입니다.

EksoNR을 도입한 시설 수는 2024년 54곳에서 2025년 중반에는 89곳으로 증가했습니다. 이는 일본에서 2025년부터 로봇 치료 1회당 1만 2,000엔(80달러)에 대한 보험 적용이 시작된 것이 뒷받침하고 있습니다. 보험사들의 성과 연계형 모델에 대한 지지가 높아짐에 따라, 자본 예산은 의약품 라인 확대보다는 디지털 및 웨어러블 솔루션으로 전환될 것으로 예측됩니다.

지역별 분석

북미는 2025년 매출의 46.18%를 차지했으며, 미국이 이를 주도했습니다. 미국에서는 127개 병원 시스템이 애보트의 i-STAT을 도입하여 CT 피폭량을 38% 줄이고, 환자 1인당 420달러의 비용을 절감했습니다. 캐나다는 2025년 3월, 이에 이어 주립 외상 센터에서 검사 1회당 180캐나다 달러(133달러)를 보상했습니다. 멕시코에서는 IMSS를 통해 신경 재활 서비스가 확대되고 있지만, 진단 비용은 여전히 본인 부담에 의존하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 9.34%를 기록하며, 세계에서 가장 빠른 성장이 예상됩니다. 중국의 2025년 선별검사 의무화 정책은 1,400개 3차 병원과 연간 210만 건의 두부 외상 사례를 대상으로 합니다. 일본에서는 트로피네티드의 승인과 로봇 재활 치료의 보험 적용이 국내 도입을 촉진하고 있는 반면, 호주와 한국에서는 조건부 의약품 승인 절차가 마련되어 있습니다. 인도는 여전히 양극화되어 있어, 대도시의 민간 병원에는 바이오마커 검사실이 설치되어 있는 반면, 지방 지역에서는 CT 검사를 받기 어려운 실정입니다.

유럽에서는 보험사의 감독이 강화되는 가운데, 완만한 성장이 예상됩니다. 독일에서는 2025년 6월 기준으로 바이오마커 검사 1건당 120유로(130달러)가 보험 적용되며, 89개 병원에서 도입이 시작되었습니다. NHS의 '버추얼 운즈(Virtual Wounds)' 프로그램은 2025년에 외상성 뇌손상 환자 8,900명에게 원격 의료 서비스를 제공하여 재입원율을 19% 감소시켰습니다. 남유럽 및 동유럽에서는 고비용 로봇 시스템의 도입이 더딘 편이지만, 2027년 이후에는 EU의 구조기금을 통해 격차가 줄어들 가능성이 있습니다.

중동 및 아프리카 및 남미에서는 보급률이 낮은 상황입니다. 브라질에서는 바이오마커 검사와 로봇 치료에 대한 보험 적용이 상파울루와 리우데자네이루의 사립 병원으로 한정되어 있지만, 사우디아라비아는 2024년에 3억 2,000만 달러를 투입해 18개 외상 센터의 장비를 첨단 모니터로 교체했습니다. 현지에서 조립하거나 기부자로부터의 자금 지원이 확대되기 전까지는 가격 문제와 공급망에 부과되는 관세가 더 광범위한 보급을 가로막고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the mild traumatic brain injury treatment market size is expected to grow from USD 5.76 billion in 2025 to USD 5.96 billion in 2026 and is forecast to reach USD 7.18 billion by 2031 at 3.81% CAGR over 2026-2031.

This report is Segmented by Treatment Type (Pharmacological Therapy, Surgical Intervention, Rehabilitation & Assistive Technologies), Cause of Injury (Falls, Motor-Vehicle Traffic, and More), End User (Hospitals & Trauma Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Mild Traumatic Brain Injury Treatment Market Trends and Insights

Rising Incidence of mTBI From Falls & Road Traffic Accidents

Falls and vehicle crashes generate more than 70% of mild TBI globally, but the epidemiology diverges by income level. Geriatric falls dominate hospital admissions in North America, Europe, and Japan, whereas road-traffic collisions afflict working-age populations in India, China, and sub-Saharan Africa. The World Health Organization recorded 1.19 million road-traffic deaths in 2023 and estimated that up to half of the 20-50 million survivors sustain head trauma. Japan reported a 31% increase in fall-related TBI hospitalizations among citizens aged 75+ between 2020 and 2024. These patterns fuel demand for rapid triage tools that direct patients to observation, imaging, or neurosurgical care within the first hour.

Rapid Adoption of Advanced Imaging & Blood-Based Diagnostics

Point-of-care biomarker panels are rewriting the economics of emergency departments. Abbott's i-STAT TBI test, cleared by FDA and reimbursed by Medicare at USD 135 per assay, cut CT use by 38% and reduced median stay from 4.2 hours to 2.8 hours across 11 U.S. hospitals studied in 2024. Military prototypes proved rugged and fast, demonstrating 92% sensitivity and 87% specificity in forward surgical teams in 2025. Reimbursement certainty is now the critical catalyst for adoption as European regulators move to harmonize companion diagnostic pathways by 2027.

Absence of FDA-Approved Disease-Modifying Therapies

The FDA has yet to authorize a disease-modifying drug for TBI, confining U.S. prescribing to symptomatic agents and capping growth potential. Only 14 mTBI compounds were in Phase II/III globally in 2025 versus 87 for Alzheimer's, underscoring investor caution. CMS denies coverage for investigational agents, deterring early adopter hospitals.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Clinical Pipeline of Neuro-Protective & Regenerative Drugs

- Post-COVID Surge in Remote Neuro-Rehabilitation & Tele-Health Demand

- High Cost of Advanced Treatment & Rehabilitation Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pharmacological therapy accounted for 63.02% of the Mild Traumatic Brain Injury Treatment market share in 2025, driven by large patient volumes and reimbursed symptom control. Growth, however, is muted without disease-modifying agents, and payers are testing bundled payments that reward functional recovery rather than prescription counts. Rehabilitation & Assistive Technologies have a smaller base but will compound at a 5.85% CAGR to 2031, supported by persistent telehealth infrastructure and robotic platforms that shorten time to independent ambulation by 18 days on average. Surgical Intervention remains niche for hematoma evacuation or refractory intracranial pressure, and its share is stable as improved triage curtails unnecessary procedures.

EksoNR deployments rose from 54 centers in 2024 to 89 in mid-2025, aided by Japan's 2025 insurance coverage of JPY 12,000 (USD 80) per robotic session. Payer alignment with outcome-based models is expected to tilt capital budgets toward digital and wearable solutions more than pharmacological line extensions.

Geography Analysis

North America generated 46.18% of 2025 revenue, led by the United States, where 127 hospital systems adopted Abbott's i-STAT and reduced CT exposure by 38%, saving USD 420 per patient. Canada followed in March 2025, reimbursing CAD 180 (USD 133) per assay in provincial trauma centers. Mexico is expanding neuro-rehab under IMSS, but still relies on out-of-pocket diagnostics.

Asia-Pacific will post a 9.34% CAGR, the fastest worldwide. China's 2025 screening mandate covers 1,400 tertiary hospitals and 2.1 million annual TBI cases. Japan's trofinetide approval and robotic rehab reimbursement spur local adoption, while Australia and South Korea align conditional drug pathways. India remains two-tiered, with private metros installing biomarker labs and rural districts lacking CT access.

Europe presents moderate growth amid payer scrutiny. Germany reimburses EUR 120 (USD 130) per biomarker test as of June 2025, launching adoption in 89 hospitals. The NHS Virtual Wards program served 8,900 TBI patients remotely in 2025, cutting readmissions by 19%. Southern and Eastern Europe lag in high-cost robotic setups, though EU structural funds may narrow gaps post-2027.

Middle East & Africa and South America are underpenetrated. Brazil restricts biomarker and robotic coverage to private hospitals in Sao Paulo and Rio, while Saudi Arabia earmarked USD 320 million in 2024 to upgrade 18 trauma centers with advanced monitors. Affordability and supply-chain tariffs limit broader uptake until local assembly and donor funding expand.

- Abbott Laboratories

- Bioness (Bioventus)

- BrainScope Company

- Ekso Bionics

- GE Healthcare

- Hope Biosciences

- InfraScan

- Integra LifeSciences

- Johnson & Johnson

- Medtronic

- Natus Medical

- Neuren Pharmaceuticals

- NeuroVive Pharmaceutical

- Novartis

- Oragenics

- Oxeia Biopharmaceuticals

- Pfizer

- Koninklijke Philips

- Raumedic

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of mTBI From Falls & Road Traffic Accidents

- 4.2.2 Rapid Adoption of Advanced Imaging & Blood-Based Diagnostics

- 4.2.3 Expanding Clinical Pipeline of Neuro-Protective & Regenerative Drugs

- 4.2.4 Post-COVID Surge in Remote Neuro-Rehabilitation & Tele-Health Demand

- 4.2.5 Japan's AKUUGO Conditional Approval Spurring Global Regulatory Momentum

- 4.2.6 Military-Funded AI Point-of-Care Biomarker Programs Accelerating Translation

- 4.3 Market Restraints

- 4.3.1 Absence of FDA-Approved Disease-Modifying Therapies

- 4.3.2 High Cost of Advanced Treatment & Rehabilitation Technologies

- 4.3.3 Low Clinician Adoption of CT-Substituting Biomarker Tests

- 4.3.4 US Tariffs Inflating Neuro-Monitor Device Supply-Chain Costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Treatment Type

- 5.1.1 Pharmacological Therapy

- 5.1.2 Surgical Intervention

- 5.1.3 Rehabilitation & Assistive Technologies

- 5.2 By Cause of Injury

- 5.2.1 Falls

- 5.2.2 Motor-Vehicle Traffic

- 5.2.3 Sports & Recreation

- 5.2.4 Violence & Others

- 5.3 By End User

- 5.3.1 Hospitals & Trauma Centers

- 5.3.2 Specialty / Neurology Clinics

- 5.3.3 Rehabilitation Centers & Home-care Settings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Bioness (Bioventus)

- 6.3.3 BrainScope Company

- 6.3.4 Ekso Bionics

- 6.3.5 GE Healthcare

- 6.3.6 Hope Biosciences

- 6.3.7 InfraScan

- 6.3.8 Integra LifeSciences Corporation

- 6.3.9 Johnson & Johnson

- 6.3.10 Medtronic

- 6.3.11 Natus Medical

- 6.3.12 Neuren Pharmaceuticals Ltd.

- 6.3.13 NeuroVive Pharmaceutical AB

- 6.3.14 Novartis

- 6.3.15 Oragenics

- 6.3.16 Oxeia Biopharmaceuticals

- 6.3.17 Pfizer

- 6.3.18 Philips Healthcare

- 6.3.19 Raumedic AG

- 6.3.20 TEVA Pharmaceutical Industries Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment