|

시장보고서

상품코드

2061636

조직공학 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Tissue Engineering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

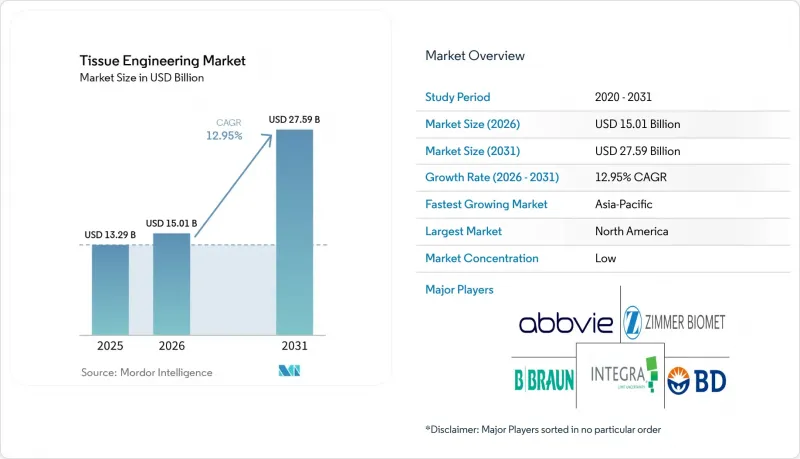

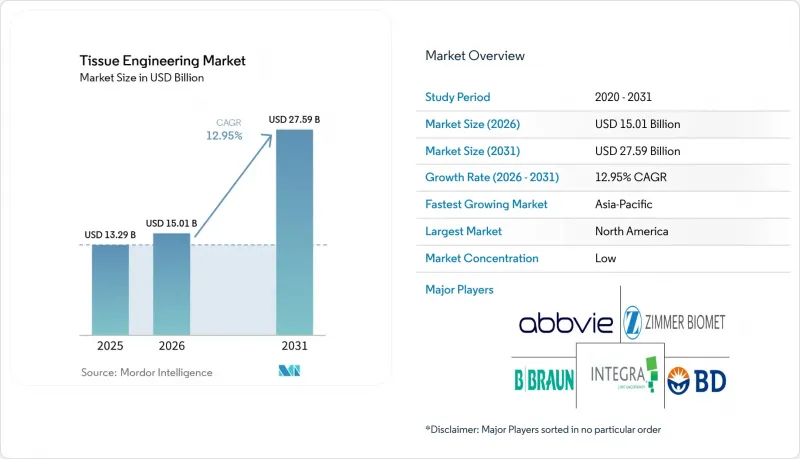

Mordor Intelligence에 의하면, 세계의 조직공학 시장 규모는 2025년에 132억 9,000만 달러로 평가되었습니다. 2026년에 150억 1,000만 달러에 달하고, 2031년까지 275억 9,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 12.95%를 나타낼 전망입니다.

본 보고서에서는 업계를 소재별(합성 폴리머, 생체 유래 스캐폴드 등), 용도별(정형외과·근골격계, 신경학 등), 최종 사용자별(병원·외과 센터, 연구·학술 기관 등), 그리고 지역별(북미, 유럽 등)로 분류하고 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(미 달러)를 제시하고 있습니다.

세계의 조직공학 시장 동향 및 분석

만성 질환 및 외상성 손상의 유병률 증가

퇴행성 관절 질환, 심혈관 합병증 및 대규모 외상으로 인해 재생 의료 솔루션에 대한 기초적인 수요가 증가하고 있으며, 이는 조직 공학 시장을 견인하고 있습니다. 퇴행성 관절염 환자만 전 세계적으로 5억 9,500만 명에 달하며, 이들은 연골 재생용 스캐폴드의 잠재적 수요층을 형성하고 있습니다. 군사 분쟁 현장에서의 경험을 통해, 가혹한 환경에서도 Symvess와 같은 기성 인공 이식편의 유용성이 입증되었습니다. 2025년 1월, 캘리포니아 대학교 어바인 캠퍼스의 연구진은 재건 수술의 적용 범위를 확대할 가능성이 있는 유연한 골격 조직 대체재 ‘리포카르티지(lipocartilage)’를 발표했습니다. 임상적 근거가 빠르게 축적되고 있으며, 최근 임상시험에서 3D 프린팅된 종골 치환편의 생존율이 96.3%에 달했으며, 혈소판 농축 피브린(PRF) 코팅을 적용한 복잡한 후족부 재건술에서 100%의 골유합이 보고됨에 따라, 외과의사들의 조직공학 임플란트에 대한 신뢰도가 높아지고 있습니다.

재생의학을 위한 민관 자금 풀 확대

바이오 제조 분야에서 정부 및 미션 주도형 자금 유입이 활발해지고 있으며, 조직 공학 시장은 장기적인 공급 확대를 위한 체제가 점차 갖춰지고 있습니다. 2024년 미국 국립과학원 보고서는 첨단 치료법의 생산 규모 확대를 위한 미국 연방 정부의 막대한 투자를 수치화했으며, 성장 인자 생산 과정에서 만연한 병목 현상을 부각시켰습니다. 유럽의 ‘호라이즌’ 프로그램이나 중국의 전략적 생명공학 청사진에 기반한 다국간 프로젝트들은 시범 시설에 자금을 투입하고 있는 반면, 벤처 투자자들은 규제 측면의 전망이 명확한 플랫폼 기술을 계속해서 선호하고 있습니다. 자금 조달의 호재는 바이오프로세스 표준화를 목표로 하는 공동 연구도 촉진하고 있으며, 이러한 노력을 통해 2028년까지 전 세계적으로 약 50메트르톤의 생산 능력이 확보될 것으로 예측됩니다.

높은 치료비와 시술비

복잡한 우수 제조 기준(cGMP) 워크플로우와 엄격한 품질 관리로 인해, 단가는 기존의 이식편 대체 요법보다 높은 수준을 유지하고 있습니다. 예를 들어, 새로 승인된 Symvess의 가격은 1단위당 약 2만 9,500달러로, 이는 고품질 생체 재료와 광범위한 임상 검증 요건을 모두 반영한 것입니다. 성장 인자나 사이토카인의 제조에는 cGMP 기준을 준수하는 생산 환경이 필수적입니다. 식품 등급 원료로의 대체를 위한 노력은 유망하게 평가받고 있지만, 아직 초기 검증 단계에 머물러 있습니다. 전용 바이오 제조 인프라에 대한 설비 투자는 스타트업 기업에게는 감당하기 어려운 규모가 되는 경우가 많아, 고정비를 관리하기 위해 파트너십을 맺거나 위탁 생산 계약을 체결해야 하는 상황에 직면해 있습니다. 중기적으로는 플랫폼의 표준화와 생산량 증가로 인해 비용 곡선이 하락할 것으로 예측됩니다.

부문별 분석

2025년 조직공학 시장에서 합성 폴리머는 54.10%의 점유율로 1위를 차지했습니다. 이는 비용 효율적인 대규모 생산, 규제 측면에서의 숙련도, 그리고 외과의사들의 확립된 사용 경험에 힘입은 결과입니다. 폴리젖산과 폴리카프로락톤은 현재 정형외과용 및 연조직용 스캐폴드 시장을 독점하고 있으며, 3D 프린팅 뼈 모델을 통한 증거가 축적됨에 따라 그 임상적 입지가 더욱 공고해지고 있습니다. 한편, 하이브리드 복합재료는 연평균 성장률(CAGR) 14.05%를 기록하며 가장 빠르게 성장하고 있는 부문입니다. 이러한 구조체는 생체활성 세라믹, 성장 인자 또는 천연 고분자를 단일 매트릭스에 통합함으로써 합성 재료의 내구성과 생체학적 신호를 결합하고 있으며, 이러한 능력 덕분에 기능적 설계의 가능성이 확대되고 있습니다. 병원들이 인체 임상시험을 통해 기계적 강도와 조직 통합 프로파일의 개선을 입증함에 따라, 하이브리드 복합 소재를 활용한 조직 공학 시장 규모는 꾸준히 확대될 것으로 전망됩니다.

또한, 탈세포화 세포외 기질(ECM) 공정이 성숙해지고 규제 당국이 보다 명확한 문서 체크리스트를 발표함에 따라, 생체 유래 스캐폴드 기술도 발전하고 있습니다. UPM Biomedicals사의 주사 가능한 나노셀룰로오스 하이드로겔 ‘FibGel’과 같은 혁신은 지속 가능한 식물 유래 원료로의 전환을 시사하고 있습니다. 일관성은 여전히 중요한 과제이며, 배치 간 편차가 다기관 공동 연구 결과를 왜곡할 가능성이 있기 때문에 새로운 품질 관리 분석 기법이 우선적으로 도입되고 있습니다. 표준화가 진행됨에 따라, 생물 유래 매트릭스는 조직 공학 시장에서 확고한 중간 시장 점유율을 확보할 것으로 예측됩니다.

지역별 분석

북미는 2025년에도 조직공학 시장의 45.10% 점유율을 유지했으며, FDA의 신속한 승인 절차, 풍부한 벤처 캐피털, 확립된 보험 급여 규정의 혜택을 누렸습니다. 이 지역의 병원들은 외상 치료 프로토콜에 Symvess를 신속하게 도입하고 있으며, 현재 여러 학술 기관이 국방부 프로그램과 협력하여 차세대 혈관 이식재의 보급을 가속화하고 있습니다. 캐나다는 틈새 시장용 cGMP 제조와 유리한 연구개발 세액 공제를 제공하는 반면, 멕시코는 공급망을 보완하는 저비용 조립 옵션을 제공합니다.

유럽은 첨단 치료 의약품(ATMP)에 대한 규제 체계를 구축해 나가면서 꾸준한 성장을 이루고 있습니다. 독일, 프랑스, 영국은 여전히 연구의 중심지이지만, 여러 지불 주체 간의 보상 협상이 임상 도입을 지연시킬 가능성이 있습니다. 일부 EU 회원국들은 첨단 생물학적 제제의 구매 물량을 공동으로 통합하기 위해 컨소시엄을 출범시켰으며, 이러한 움직임으로 인해 예산상의 장벽이 완화되어 2027년 이후 시술 건수가 증가할 것으로 예측됩니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 13.98%를 나타낼 것으로 전망됩니다. 중국의 ‘제14차 5개년 계획’에서는 조직공학 시범 공장에 막대한 자금이 배정되었으며, 국가약품감독관리국(NMPA)은 스캐폴드 단독 제품 및 복합 제품의 분류를 명확히 하는 지침을 도입했습니다. 일본에서는 고령화가 진행되는 인구 동향에 따라 연골 및 혈관 임플란트에 대한 수요가 증가하고 있으며, 의약품의료기기종합기구(PMDA)는 적격 의료기기 시장 출시 기간을 단축하는 신속 심사 절차를 제공합니다. 인도의 민간 병원 체인들은 의료 관광 수요를 유치하기 위해 모듈식 바이오 프린팅 연구소에 투자하고 있으며, 이는 조직 공학 시장의 지역적 확장을 촉진하고 있습니다. 규제 조화는 여전히 중요한 변수이며, 아세안(ASEAN) 회원국 간 GMP 감사 및 신청 서류 양식을 통일하려는 노력은 향후 5년 동안 더욱 확산될 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the global tissue engineering market size is projected to be USD 13.29 billion in 2025, USD 15.01 billion in 2026, and reach USD 27.59 billion by 2031, growing at a CAGR of 12.95% from 2026 to 2031.

This report Segments the Industry Into by Material (Synthetic Polymers, Biologically-Derived Scaffolds, and More), by Application (Orthopedics & Musculoskeletal, Neurology, and More), by End User (Hospitals & Surgical Centers, Research & Academic Institutes, and More) and Geography (North America, Europe, and More). The Market Provides the Value (in USD) for the Above-Mentioned Segments.

Global Tissue Engineering Market Trends and Insights

Rising Prevalence of Chronic Diseases & Trauma Injuries

Degenerative joint disease, cardiovascular complications, and large-scale trauma are lifting baseline demand for regenerative solutions, strengthening the tissue engineering market. Osteoarthritis alone affects 595 million people worldwide, creating a sizable cohort for cartilage repair scaffolds. Field experience from military conflicts has confirmed the utility of off-the-shelf engineered grafts such as Symvess in austere settings. In January 2025, UC Irvine researchers introduced lipocartilage, a flexible skeletal tissue substitute that may broaden indications in reconstructive surgery. Clinical evidence is maturing quickly; recent trials reported 96.3% survivorship of 3-D printed talus replacements and 100% union in complex hindfoot reconstructions when platelet-rich fibrin coatings were employed, reinforcing surgeon confidence in tissue-engineered implants.

Expanding Public-Private Funding Pools for Regenerative Medicine

Government and mission-driven capital flows are intensifying around biomanufacturing, positioning the Tissue Engineering market for long-term supply expansion. A 2024 National Academies report quantified sizeable US federal commitments to scale advanced therapy manufacturing and highlighted persistent bottlenecks in growth-factor production. Multilateral projects under Europe's Horizon program and China's strategic biotech blueprint are channeling funds into pilot facilities, while venture investors continue favoring platform technologies with clear regulatory visibility. Funding tailwinds are also prompting collaborations that target bioprocess standardization, an effort expected to unlock nearly 50 metric tons of global capacity by 2028.

High Therapy and Procedure Costs

Complex good-manufacturing workflows and stringent quality controls keep unit prices above conventional graft alternatives. For instance, the newly approved Symvess is priced around USD 29,500 per unit, reflecting both high-grade biomaterials and extensive clinical validation requirements. Growth factors and cytokines necessitate cGMP production environments; efforts to substitute food-grade inputs show promise but remain in early validation. Capital outlays for dedicated biomanufacturing infrastructure often sit beyond the reach of start-ups, compelling partnerships or contract manufacturing agreements to manage fixed costs. Over the medium term, platform standardization and rising production volumes are expected to compress cost curves

Other drivers and restraints analyzed in the detailed report include:

- Rapid Advances in 3-D Bioprinting & High-Throughput Scaffold Design

- Accelerated Regulatory Pathways

- Fragmented Reimbursement Coverage Architecture

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic polymers led with a 54.10% share of the Tissue Engineering market in 2025, underpinned by cost-efficient scale, regulatory familiarity, and established surgeon comfort. Polylactic acid and polycaprolactone dominate today's orthopedic and soft-tissue scaffolds, and mounting evidence from 3-D printed bone models is reinforcing their clinical staying power. Hybrid composites, however, are the fastest-growing segment at a 14.05% CAGR. These constructs merge synthetic durability with biologic cues by integrating bioactive ceramics, growth factors, or natural polymers into a single matrix, a capability that broadens the functional design landscape. The Tissue Engineering market size for hybrid composites is forecast to widen steadily as hospitals validate improved mechanical strength and integration profiles in human trials.

Biologically derived scaffolds are also advancing as decellularized extracellular matrix processes mature and regulators issue clearer documentation checklists. Innovations such as UPM Biomedicals' injectable nanocellulose hydrogel FibGel signal a shift toward sustainable, plant-based inputs news. Consistency remains the gating factor; batch-to-batch variability can derail multicenter trial outcomes, so new quality-control analytics are gaining priority. As standardization improves, biologically derived matrices are expected to secure a solid mid-tier share of the Tissue Engineering market.

Geography Analysis

North America retained 45.10% of the Tissue Engineering market share in 2025 and benefits from the FDA's responsive pathways, deep venture capital pools, and established reimbursement codes. The region's hospitals moved quickly to integrate Symvess into trauma protocols, and multiple academic centers are now partnering with Defense Department programs to accelerate next-generation vascular graft deployment. Canada contributes niche cGMP manufacturing and favorable R&D tax credits, whereas Mexico offers lower-cost assembly options that complement supply chains.

Europe posts steady growth while refining its Advanced Therapy Medicinal Product regulatory framework. Germany, France, and the United Kingdom remain research powerhouses, yet multi-payer reimbursement negotiations can delay clinical adoption. Several EU member states are launching consortia to pool purchasing volumes for advanced biologics, a move expected to ease budgetary hurdles and increase procedure counts starting 2027.

Asia-Pacific is the fastest-rising region with a projected 13.98% CAGR through 2031. China's 14th Five-Year Plan earmarked substantial funds for tissue-engineering pilot plants, and the National Medical Products Administration has introduced guidance to clarify scaffold-only and combination-product categories. Japan's aging demographics drive high demand for cartilage and vascular implants, while its PMDA agency provides fast-track review channels that shorten time-to-market for qualified devices. India's private hospital chains are investing in modular bioprinting labs to capture inbound medical-tourism flows, expanding the regional footprint of the Tissue Engineering market. Regulatory harmonization remains the critical variable; initiatives to align GMP audits and dossier templates across ASEAN economies could unlock additional adoption over the next five years.

- Abbvie

- Integra LifeSciences

- Beckton Dickinson

- Zimmer Biomet

- Organogenesis

- Smith & Nephew (Osiris)

- Biotime

- B. Braun

- Bio Tissue Technologies

- ACell

- Athersys

- Tissue Regenix Group

- Medtronic

- Stryker

- Johnson & Johnson

- Vericel

- Organovo

- CollPlant

- Humacyte

- MiMedx

- Cyfuse Biomedical

- TissUse

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases & Trauma Injuries

- 4.2.2 Rapid Advances in 3-D Bio-printing & High-throughput Scaffold Design

- 4.2.3 Expanding Public-private Funding Pools for Regenerative Medicine

- 4.2.4 Accelerated Regulatory Pathways

- 4.2.5 Corporate ESG Mandates Replacing Animal Testing with Human-cell Tissue Models

- 4.3 Market Restraints

- 4.3.1 High Therapy & Procedure Costs

- 4.3.2 Fragmented Reimbursement Coverage Architecture

- 4.3.3 Supply-chain Shortages of cGMP-grade Growth Factors & Cytokines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Synthetic Polymers

- 5.1.2 Biologically-derived Scaffolds

- 5.1.3 Hybrid / Composite

- 5.2 By Application

- 5.2.1 Orthopedics & Musculoskeletal

- 5.2.2 Neurology

- 5.2.3 Cardiology & Vascular

- 5.2.4 Skin & Integumentary

- 5.2.5 Dental & Cranio-maxillofacial

- 5.2.6 Others

- 5.3 By End User

- 5.3.1 Hospitals & Surgical Centers

- 5.3.2 Research & Academic Institutes

- 5.3.3 Specialty Regenerative Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 AbbVie (Allergan)

- 6.3.2 Integra LifeSciences

- 6.3.3 BD (C.R. Bard)

- 6.3.4 Zimmer Biomet

- 6.3.5 Organogenesis

- 6.3.6 Smith & Nephew (Osiris)

- 6.3.7 Biotime Inc.

- 6.3.8 B. Braun Melsungen

- 6.3.9 Bio Tissue Technologies

- 6.3.10 ACell Inc.

- 6.3.11 Athersys Inc.

- 6.3.12 Tissue Regenix Group

- 6.3.13 Medtronic

- 6.3.14 Stryker

- 6.3.15 Johnson & Johnson (DePuy Synthes)

- 6.3.16 Vericel

- 6.3.17 Organovo

- 6.3.18 CollPlant

- 6.3.19 Humacyte

- 6.3.20 MiMedx

- 6.3.21 Cyfuse Biomedical

- 6.3.22 TissUse

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment