|

시장보고서

상품코드

2061643

일회용 내시경 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Disposable Endoscope - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

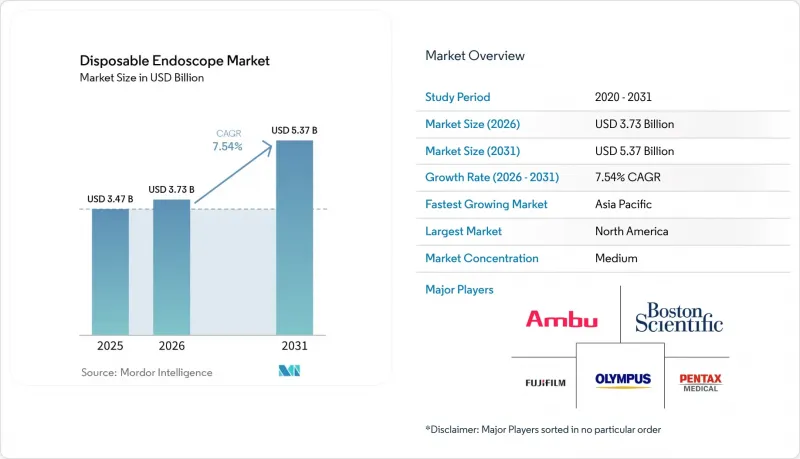

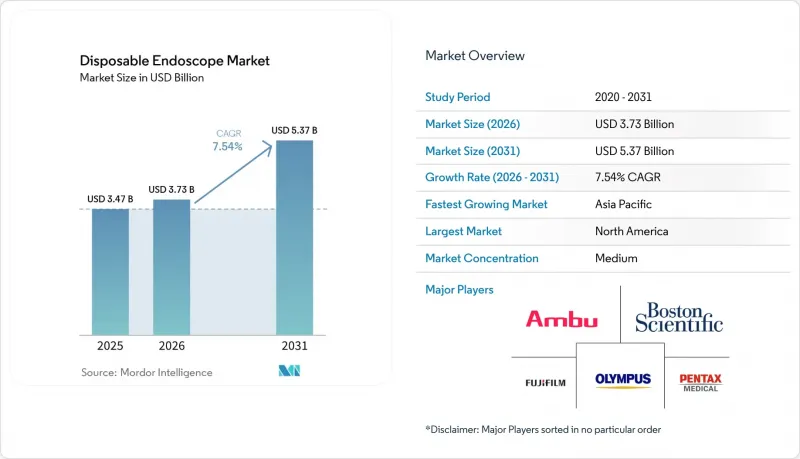

Mordor Intelligence에 의하면, 2026년 일회용 내시경 시장 규모는 37억 3,000만 달러에 달할 것으로 추정됩니다. 2025년 34억 7,000만 달러에서 성장하여 2031년에는 53억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.54%를 나타낼 것으로 전망됩니다.

본 보고서는 제품 유형별(위내시경, 기관지경, 십이지장내시경 등), 용도별(소화기내과, 호흡기내과, 비뇨기과 등), 시술별(진단용 및 치료용), 최종 사용자별(병원 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 일회용 내시경 시장 동향 및 분석

일회용 CMOS 이미징 센서의 기술적 손익분기점

저비용 CMOS 모듈은 현재 2022년 대비 35.0% 낮은 제조 비용으로 진단 수준의 해상도를 구현하고 있어, 지역 병원이 재사용 가능한 타워형 장비를 플러그 앤 플레이 방식의 일회용 제품으로 교체할 수 있게 해줍니다. 공장에서 펌웨어를 업그레이드함으로써 콘솔 가동 중단 시간이 해소되었으며, 조달 팀은 연간 화소 수 향상을 기준으로 내시경을 평가하게 되었습니다. 이는 가전제품의 교체 주기를 반영한 변화입니다. 그 결과, 일회용 내시경 시장은 3차 의료기관을 넘어 확대되고 있으며, 지방의 의료기관에서도 재처리 과정의 병목 현상을 해소하고 세척기 도입에 따른 설비 투자를 피할 수 있는 일회용 모델이 도입되고 있습니다.

병원 인증 기준의 조기 도입

2024년에 도입된 개정판 조인트 커미션 규정에서는 모든 고강도 소독 주기에 대한 실시간 추적이 의무화됨에 따라, 중규모 내시경실은 규정 준수용 하드웨어에 5만 달러 이상을 투자할 수밖에 없게 되었습니다. 이러한 설비 투자 덕분에 사용 빈도가 높은 시설에서는 일회용 내시경의 투자 회수 기간이 최단 12개월로 단축되었으며, 이는 재무위원회에 일회용 제품이 감염 관리 문제와 급증하는 인건비 문제를 모두 해결할 수 있다는 확신을 심어주고 있습니다. 멸균 처리 담당 직원을 환자 대응 업무로 재배치함으로써, 병원은 지출을 가치 기반 의료(Value-Based Care)의 목표와 일치시키고, 임상 현장에서의 활용도를 높이고 있습니다.

이용률이 낮은 지역 병원의 불투명한 비용 대비 효과

연간 500건 미만의 수술을 수행하는 의료기관에서는 기존 재처리실이 충분히 활용되지 않고 있어, 일회용 제품으로 전환할 경우 건당 비용이 20% 증가합니다. 많은 의료기관에서는 하이브리드 방식을 채택하고 있으며, 고위험 ERCP나 중환자실(ICU)에서의 기관지 내시경 검사에는 일회용 제품을, 일상적인 검진에는 재사용 가능한 대장 내시경을 각각 사용하고 있습니다. 이 이중 재고 모델은 폐기물 감사나 구매 업무를 복잡하게 만들지만, 관리자 입장에서는 감염 관리 요구 사항과 예산상의 현실 사이에서 균형을 맞출 수 있게 해줍니다.

부문별 분석

2025년, 기관지경은 일회용 내시경 시장 점유율의 31.62%를 차지하며, 영상의 선명도를 저하시키지 않으면서 말초 기관지 내부를 이동할 수 있는 슬림한 형태 덕분에 이 부문에서 확고한 주도적 위치를 굳혔습니다. 교육 병원에서는 공유 장비로 인한 일정 조정 문제가 해소되고 교육 효율이 향상되기 때문에 일회용 기관지경이 훈련용 장비로 선호되고 있습니다. 인공호흡기 관련 폐렴에 대한 감시가 강화되면서 시술 건수가 유지되고, 건당 비용을 예측할 수 있다는 점도 더해져, 기관지경 일회용 내시경 시장 규모는 견조한 성장세를 보이고 있습니다. 이에 대응하여 공급업체는 모니터, 트롤리, 클라우드 스토리지를 세트로 판매함으로써 혼잡한 중환자실의 설치 공간 부족 문제를 해결하고 있습니다.

십이지장 내시경은 여전히 매출 비중이 작지만, 엘리베이터를 통한 오염 우려로 인해 ERCP실에서 고가의 일회용 내시경을 도입하는 추세가 확산되면서, 2031년까지 연평균 성장률(CAGR) 9% 이상을 나타낼 것으로 전망됩니다. 각 제조업체는 현재 FDA 지침을 충족하는 일회용 엘리베이터를 출하하고 있으며, 조달 부서는 유지보수 계약 해지로 인한 비용 절감 효과를 인지하고 있습니다. 3차 의료기관에서 진행된 시범 프로젝트를 통해 재처리 업무의 적체가 해소됨에 따라 일정 관리가 개선된다는 사실이 입증되었으며, 부속품의 호환성이 확대된다면 지역 거점 병원들도 이에 동참할 것으로 예측됩니다.

2025년 기준으로 소화기내과 분야는 일회용 내시경 시장 규모의 39.85%를 차지했으며, 이는 ERCP 시술 시 교차 감염에 대한 우려와 외래 대장내시경 검사에서 일회용 제품 사용이 확대되고 있는 것이 주된 요인입니다. 소화기내과 검사실에서는 재처리 과정으로 인한 지연이 줄어들고 있으며, 이로 인해 검사 일정을 더욱 빡빡하게 잡을 수 있게 되어, 고액 본인부담형 보험 시장에서 환자 유치로 이어지고 있습니다. 이러한 업무 효율화뿐만 아니라 치료 분야로의 진출 로드맵이 마련되어 있는 만큼, 각 공급업체들은 소화기 분야에 특화된 혁신 기술 개발에 지속적으로 주력하고 있습니다.

호흡기내과 분야가 가장 빠른 성장세를 보이고 있습니다. 이는 폐렴 진단이나 폐암 병기 판정을 위한 기관지경 검사 건수가 꾸준히 유지되고 있으며, 이는 일회용 내시경의 특성과 부합하기 때문입니다. 임상의들은 경기관지적 바늘 생검(TBNA) 시 회복 기간 단축과 오염 위험 감소를 결정적인 요인으로 꼽고 있습니다. 병원에서는 일회용 기관지경을 품질 개선 지표에 포함시키고 있으며, 이를 통해 당일 생검률이 향상되고, 얇은 직경의 채널에 대응하는 일회용 회수 바스켓에 대한 수요가 증가하고 있습니다.

지역별 분석

2025년, 북미는 44.92%의 점유율로 일회용 내시경 시장을 주도했습니다. 미국의 통합 의료 네트워크는 구매를 통합하고 대량 구매 할인을 협상하는 한편, 조인트 커미션(Joint Commission) 및 CMS의 규제로 인해 감염 예방이 경영진 차원의 최우선 과제가 되고 있습니다. 많은 병원에서는 세척 소독기의 연간 유지보수 비용이 리스 비용의 기준치를 초과하면, 기기 교체를 미루고 그 자금을 일회용 제품으로 전환하는 프로그램에 사용하고 있습니다. 캐나다 역시 이와 유사한 임상적 근거에 기반을 두고 있지만, 주 정부의 기술 지원금에 의존하고 있어 조달 주기가 길어지고 있습니다. 2024년 FDA가 올림푸스의 RenaFlex와 같은 일회용 요관경에 대해 510(k) 승인 절차를 승인함에 따라, 임상 팀은 규제 측면에서 확신을 갖게 되었습니다.

아시아태평양은 8.61%라는 지역별 최고 연평균 성장률(CAGR)을 기록하고 있습니다. 중국 각 성에서 진행하는 입찰에서는 국가위생건강위원회의 지침에 따른 감염 관리 목표를 달성하기 위해 일회용 내시경이 대상에 포함되어 있으며, 수입 관세를 피할 수 있는 현지 제조업체가 우대받고 있습니다. 인도의 민간 병원 체인은 재처리 대기 시간 제로를 차별화의 핵심 요소로 내세우고 있으며, 클라우드 연결형 처리 장치는 복잡한 소화기 질환 사례에 대한 원격 지도를 효율화하고 있습니다. 일본은 국내에서 재사용 가능한 내시경 제조의 경쟁력과 일회용 내시경의 임상적 이점을 모두 확보하는 선택적 접근 방식을 채택하고 있습니다. 후난 바틴(Hunan Vathin) 등 한국 기업들은 경쟁을 촉발시키며, 이익률 압박에도 불구하고 판매량을 늘리고 있습니다. 한편, 호주에서는 화학 소독제의 수명 주기 전반에 걸친 환경적 영향을 파악하기 위한 탄소 회계 정보의 공시가 의무화되어 있습니다. 유럽에서는 도입 양상이 제각각입니다. 북유럽 국가들은 탄소 수명 주기 지표를 우선시하는 ‘그린 수술실(Green OR)’ 지침을 활용하여 1인당 사용량이 가장 높은 수준입니다. 현재, 내시경 재활용 물류가 조달 평가 점수에 영향을 미치고 있습니다. 독일과 프랑스에서는 주로 고위험 ERCP나 중환자실(ICU)에서의 기관지 내시경 검사에서 일회용 제품을 대체하고 있으며, 자본 예산을 절감하기 위해 기타 분야에서는 재사용 가능한 장비의 도입을 확대되고 있습니다. 영국의 NHS는 일회용 내시경을 ‘감염 제로’ 목표 달성을 위한 수단으로 보고 있지만, 이를 더 광범위하게 도입하기 위해서는 예산 조정이 필요합니다. 남유럽 및 동유럽에서는 하이브리드 방식이 도입되어 있으며, 치료 목적의 ERCP에는 일회용 제품을, 대규모 대장내시경 검진에는 재사용 가능한 제품이 사용되고 있습니다. EU 의료기기 규정(MDR)으로 인한 비용 부담이 중소 공급업체들을 압박하고 있어, 브랜드 다양성이 축소될 우려가 있을 뿐만 아니라, 병원 그룹이 기존의 세계 공급업체와 다년 계약을 체결하는 요인이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the disposable endoscopes market size in 2026 is estimated at USD 3.73 billion, growing from 2025 value of USD 3.47 billion with 2031 projections showing USD 5.37 billion, growing at 7.54% CAGR over 2026-2031.

This report is Segmented by Product (Gastroscopes, Bronchoscopes, Duodenoscopes, and More), Application Type (Gastroenterology, Pulmonology, Urology, and More), Procedure Type (Diagnostic and Therapeutic), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Disposable Endoscope Market Trends and Insights

Technological Break-Even of Single-Use CMOS Imaging Sensors

Low-cost CMOS modules now deliver diagnostic-grade resolution at a production cost 35.0% lower than in 2022, enabling community hospitals to replace reusable towers with plug-and-play disposables. Firmware upgrades performed at the factory eliminate console downtime and push procurement teams to evaluate scopes on annual pixel gains, a shift mirroring consumer-electronics replacement cycles. As a result, the disposable endoscopes market is widening beyond tertiary centers, with rural facilities adopting single-use models that remove reprocessing bottlenecks and avoid capital outlays on washers.

Implementation of Accelerated Hospital Accreditation Standards

Revised Joint Commission rules introduced in 2024 mandate real-time tracking of every high-level disinfection cycle, forcing mid-size endoscopy suites to invest over USD 50,000 in compliance hardware. The capital strain has shortened the payback period on single-use scopes to as little as 12 months in high-volume centers, convincing finance committees that disposables solve both infection-control gaps and escalating labor costs. By redeploying sterile-processing staff to patient-facing roles, hospitals align spending with value-based-care objectives and boost clinical availability.

Uncertain Cost-Benefit Equation for Low-Volume Community Hospitals

Facilities performing under 500 procedures per year face 20% higher per-case costs when moving to disposables because their existing reprocessing rooms stand under-utilized. Many adopt hybrid fleets, reserving disposables for high-risk ERCP or ICU bronchoscopy while retaining reusable colonoscopes for routine screenings. The dual-inventory model complicates waste audits and purchasing but allows administrators to reconcile infection-control imperatives with budget realities.

Other drivers and restraints analyzed in the detailed report include:

- Increased Demand for Bronchoscopy in ICU Settings Post-COVID

- Reimbursement Code Expansion for Category III Single-Use Endoscopes

- Restricted Lumen Size Limits Advanced Therapeutic Interventions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bronchoscopes generated 31.62% of the disposable endoscopes market share in 2025, underpinning the segment's leadership with their slim profiles that navigate distal bronchi without compromising image fidelity. Teaching hospitals favor single-use bronchoscopes as training devices because scheduling conflicts linked to shared equipment vanish, improving educational throughput. Elevated ventilator-associated pneumonia surveillance sustains procedural volume, and combined with predictable per-case costs, cements the disposable endoscopes market size for bronchoscopes on a solid growth path. Suppliers respond by bundling screens, trolleys, and cloud storage, shrinking the operational footprint in crowded ICUs.

Duodenoscopes remain a smaller slice of revenue but are projected to post a >9% CAGR to 2031 as elevator-contamination worries push ERCP suites to adopt premium-priced single-use scopes. Manufacturers now ship disposable elevators that satisfy FDA guidelines, and procurement teams see cost offsets from canceled maintenance contracts. Pilot projects in tertiary centers demonstrate scheduling gains because reprocessing backlogs disappear, encouraging regional hubs to follow once accessory compatibility widens.

Gastroenterology commanded 39.85% of the disposable endoscopes market size in 2025, driven by cross-contamination fears in ERCP and rising single-use adoption for outpatient colonoscopies. GI suites report fewer reprocessing delays, enabling denser scheduling that attracts patients in high-deductible insurance markets. The resulting operational efficiencies, paired with the availability of therapeutic channel expansion roadmaps, keep suppliers focused on developing GI-specific innovations.

Pulmonology shows the fastest growth because sustained bronchoscopy volumes for pneumonia diagnostics and lung-cancer staging fit well with disposable scope attributes. Clinicians cite reduced downtime and lower contamination risk during transbronchial needle aspiration as decisive factors. Hospitals integrate single-use bronchoscopy into quality-improvement metrics, boosting same-day biopsy rates and driving complementary demand for disposable retrieval baskets that match narrow channels.

Geography Analysis

North America led the disposable endoscopes market with a 44.92% share in 2025. U.S. integrated delivery networks consolidate purchasing and negotiate volume rebates, while Joint Commission and CMS regulations elevate infection prevention to board-level priorities. Many hospitals defer washer-disinfector replacement once annual service costs exceed lease thresholds, channeling funds into single-use conversion programs. Canada follows a similar clinical rationale but relies on provincial technology grants that lengthen procurement cycles. The FDA's 510(k) clearance pathway for single-use ureteroscopes like Olympus RenaFlex in 2024 gives clinical teams regulatory confidence.

Asia Pacific posts the highest regional CAGR at 8.61%. China's provincial tenders include disposable scopes to meet infection-control targets under National Health Commission directives, favoring local manufacturers who avoid import duties. Private hospital chains in India advertise zero reprocessing backlogs as a differentiation lever, and cloud-connected processors streamline tele-mentoring for complex GI cases. Japan applies a selective approach, balancing its domestic reusable manufacturing dominance with the clinical benefits of disposables. South Korean firms such as Hunan Vathin trigger price competition that expands unit volumes despite margin compression, while Australia mandates carbon-accounting disclosures that recognize the lifecycle burden of chemical disinfectants. Europe shows fragmented adoption patterns. Nordic countries top per-capita usage, leveraging "Green OR" directives that prioritize carbon lifecycle metrics; scope recycling logistics now influence tender scores. Germany and France substitute disposables mainly for high-risk ERCP and ICU bronchoscopy, extending reusable fleets elsewhere to protect capital budgets. The UK's NHS labels single-use scopes a tool for hitting zero-infection targets, yet broader adoption awaits budgetary alignment. Southern and Eastern Europe implement hybrid fleets: disposables for therapeutic ERCP, reusables for mass colonoscopy screenings. EU Medical Device Regulation costs strain small suppliers, potentially narrowing brand diversity and prompting hospital groups to lock multi-year deals with incumbent global vendors.

- Ambu

- Boston Scientific

- Olympus Corp.

- Fujifilm Holdings Corp.

- Pentax Medical (HOYA)

- Baxter

- Verathon

- Karl Storz

- STERIS

- Flexible Medical Systems Ltd.

- 3NT Medical Ltd.

- Coloplast

- ScoutCam Inc.

- OTU Medical Inc.

- Innovex Medical Co.

- Micro-tech

- Prunus Medical Co.

- Hunan Vathin Medical Instrument Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Break-Even of Single-Use CMOS Imaging Sensors Lowering Unit Costs.

- 4.2.2 Implementation of Accelerated Hospital Accreditation Standards for Endoscope Re-Processing.

- 4.2.3 Increased Demand for Bronchoscopy in ICU Settings for Pneumonia Diagnostics Post-COVID.

- 4.2.4 Reimbursement Code Expansion for Category III Single-Use Endoscopes

- 4.2.5 Shift toward OGreen ORO Initiatives Driving Adoption of Fully Recyclable Polymer Scopes (Nordics)

- 4.2.6 Chinese Volume-based Procurement (VBP) Policy Favouring Domestic Disposable Brands

- 4.3 Market Restraints

- 4.3.1 Uncertain Cost-benefit Equation for Low-Procedure-Volume Community Hospitals

- 4.3.2 Restricted Lumen Size Limits Advanced Therapeutic Interventions

- 4.3.3 Evolving EU Medical-Device Regulation (MDR) Raising Time-to-Market for New SKUs

- 4.3.4 Clinical Evidence Gaps on Image Quality vs. Re-usable HD Scopes among ENT Surgeons

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Gastroscopes

- 5.1.2 Bronchoscopes

- 5.1.3 Duodenoscopes

- 5.1.4 Laryngoscopes

- 5.1.5 Colonoscopes

- 5.1.6 Ureteroscopes

- 5.1.7 Other Endoscopes

- 5.2 By Application Type

- 5.2.1 Gastroenterology

- 5.2.2 Pulmonology

- 5.2.3 Urology

- 5.2.4 ENT

- 5.2.5 Other Application Types

- 5.3 By Procedure Type

- 5.3.1 Diagnostic

- 5.3.2 Therapeutic

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Ambu A/S

- 6.4.2 Boston Scientific Corp.

- 6.4.3 Olympus Corp.

- 6.4.4 Fujifilm Holdings Corp.

- 6.4.5 Pentax Medical (HOYA)

- 6.4.6 Baxter (Hillrom Services Inc.)

- 6.4.7 Verathon Inc.

- 6.4.8 KARL STORZ SE & Co. KG

- 6.4.9 STERIS

- 6.4.10 Flexible Medical Systems Ltd.

- 6.4.11 3NT Medical Ltd.

- 6.4.12 Coloplast A/S

- 6.4.13 ScoutCam Inc.

- 6.4.14 OTU Medical Inc.

- 6.4.15 Innovex Medical Co.

- 6.4.16 Micro-Tech Endoscopy

- 6.4.17 Prunus Medical Co.

- 6.4.18 Hunan Vathin Medical Instrument Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment