|

시장보고서

상품코드

2061656

자기 수혈 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Autotransfusion Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

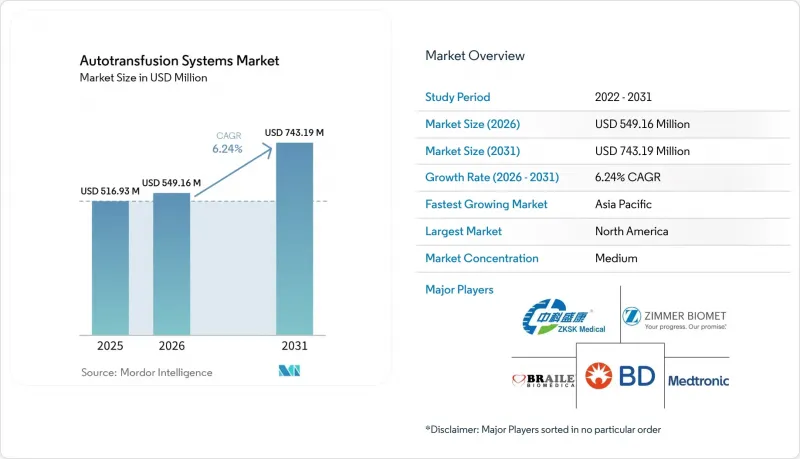

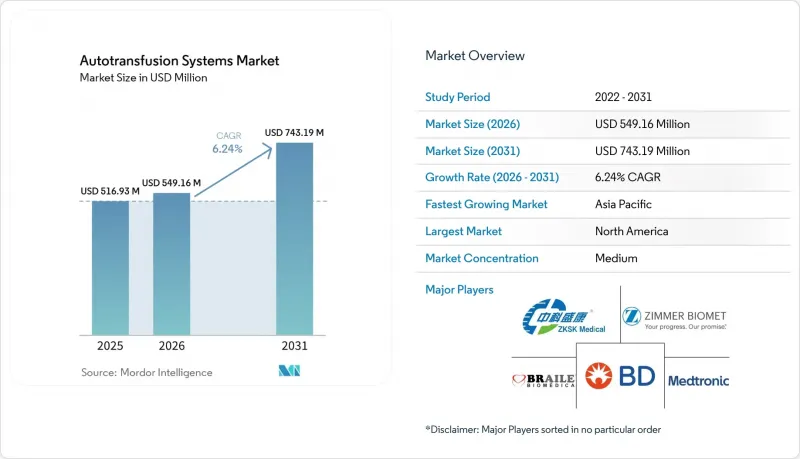

Mordor Intelligence에 의하면, 자기 수혈 시스템 시장 규모는 2025년에 5억 1,693만 달러로 평가되었고, 2026년 5억 4,916만 달러로 추정되고, 2031년까지 7억 4,319만 달러에 이를 것으로 예측되며, 예측 기간 중에 CAGR 6.24%로 성장할 것으로 전망됩니다(2026-2031년).

본 보고서는 제품 유형별(기기 및 소모품), 용도별(심장 외과 수술, 정형외과 수술, 장기 이식, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 기타) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 본 보고서에서는 상기 각 부문 시장 규모(단위 : 백만 달러)를 제시하고 있습니다.

세계의 자기 수혈 시스템 시장 동향 및 인사이트

심장 및 정형외과 수술 건수와 수술의 복잡성 증가

심장 및 정형외과 수술이 점점 더 복잡해지고, 다량의 출혈을 동반하기 때문에 혈액 회수가 필수적입니다. 경카테터 대동맥판막 치환술과 다추간 척추 재건술의 보급에 힘입어, 2024년 수요의 38.75%를 심장 수술실만으로도 차지했습니다. 현재 유럽의 외상 지침에서는 중증 출혈에 대해 세포 회수를 실시하도록 팀에 지시하고 있으며, 이는 모범 사례로 공식적으로 확립되어 있습니다. 기증자 공급원이 줄어드는 반면, 고령화로 인해 환자 수는 증가하고 있습니다. 메타분석에 따르면, 전문 분야를 불문하고 회수가 실시될 경우 동종 수혈이 39% 감소하는 것으로 확인되었습니다. 그 결과, 자기 수혈 시스템 시장은 단순한 선택적 추가 장비가 아닌, 수술실의 기반이 되는 인프라로 변화하고 있습니다.

전 세계 헌혈 혈액 부족과 점점 더 엄격해지는 수혈 지침

세계보건기구(WHO)의 환자 혈액 관리 프레임워크는 자가혈 보존을 최우선 선택지로 규정하고 있으며, 의료 제공업체들에게 살베이지 시스템을 비상용이 아닌 일상적인 조치로 도입할 것을 요구하고 있습니다. 많은 아프리카 및 아시아 국가에서는 연간 헌혈 부족량이 20만 단위를 넘어, 병원들은 1밀리리터도 낭비할 수 없는 상황에 몰려 있습니다. 회수된 혈액은 보관된 혈액에 비해 더 신선한 적혈구를 제공하며, 면역 반응도 적다는 장점이 있는데, 이는 대조 시험을 통해 입증되었습니다. 경제적인 관점에서 볼 때, 수혈 1회를 줄임으로써 병원은 조달비와 합병증 치료비 등으로 500달러 이상을 절약할 수 있으며, 이 프로그램을 전면적으로 도입할 경우 환자 1인당 1,367달러의 이익을 창출할 가능성이 있습니다. 상환 제도의 정비가 진행되는 가운데, 자기 수혈 시스템 시장은 임상적, 경제적, 규제적 요구가 유례없이 일치하고 있다는 점의 혜택을 누리고 있습니다.

장비 및 소모품 일체의 높은 초기 비용

턴키 시스템의 가격은 5만 달러에서 15만 달러에 달하며, 예산이 제한적인 진료소에게는 막대한 지출이 됩니다. 소모품 비용은 1건당 200-400달러가 추가로 발생하며, 보험금 지급이 지연되는 의료기관에서는 이익률을 압박합니다. 리스나 종량제 모델은 고액의 초기 비용 부담을 줄여주지만, 이러한 자금 조달 수단이 보급되기 전까지는 소규모 병원이나 공립병원에서의 도입이 더딘 임베디드니다. 메디케어에 의한 잠정적인 보험 적용은 위험을 상쇄할 수 있지만, 전 세계적인 보급을 위해서는 보험사 간의 보다 광범위한 협력이 필수적입니다. 모순된 상황은 여전히 남아 있습니다. 즉, 자가수혈이 가장 절실한 곳, 즉 기증자가 현저히 부족한 시설일수록 자금이 부족한 경우가 많으며, 이것이 단기적인 시장 확대를 억제하고 있는 것입니다.

부문별 분석

2025년 매출액 중 기기가 61.72%를 차지했으며, 병원이 내구성이 뛰어난 자본 설비 플랫폼에 의존하고 있음이 드러나고 있습니다. 한편, 소모품은 연평균 성장률(CAGR) 7.03%를 나타낼 것으로 예측되며, 이는 시술 건수 증가와 ‘면도기와 면도날’ 방식의 가격 전략을 반영한 것입니다. 2025년 기준으로, 기기에 기인한 자기 수혈 시스템 시장 규모는 3억 1,907만 달러에 달한 반면, 소모품 시장은 1억 9,786만 달러에 달했습니다. 각 제조업체는 소형화와 직관적인 사용자 인터페이스에 투자하고 있으며, 안전성을 저해하지 않으면서 가격을 낮추기 위해 선택 사양인 하드웨어 기능을 제거하고 있습니다. 소모품 분야에서는 인쇄 가능한 리저버와 색상별로 구분된 튜브 세트를 통해 설정이 간소화되고 폐기물이 줄어듭니다. 예측 기간 동안 광범위한 도입 기반이 예측 가능한 반복 수요를 창출할 것이며, 이는 연구개발(R&D) 투자 회수를 뒷받침하게 될 것입니다.

2차적인 성장 요인은 유연한 자금 조달과 소모품 계약의 연계에 있습니다. 병원 네트워크에서는 사용량에 따라 규모를 조정할 수 있는 저약속형 장비 리스를 선호하는 경향이 강해지고 있으며, 이 모델은 동시에 협상된 가격으로 소모품 공급을 보장하는 방식입니다. 이러한 조합을 통해 수익이 안정화되고, 의료 서비스 제공업체는 일시적인 자본 부담으로부터 보호받게 되므로, 지역 병원의 자기 수혈 시스템 시장 확대가 촉진될 것입니다.

수술 중 회수는 2025년 매출의 35.42%를 차지했으며, 대량 출혈 사례에서 그 확고한 역할을 입증하고 있습니다. 그러나 수술 전 자가 채혈이나 급성 정상 혈액량성 혈액 희석과 같은 예방적 전략은 연평균 성장률(CAGR) 6.79%로 증가하고 있으며, 이는 외과 팀이 첫 절개 전에 동종 수혈에 대한 의존도를 줄이려고 노력하고 있음을 보여줍니다. 수술 전 모듈을 도입한 병원에서는 수혈량이 두 자릿수 감소했으며, 수술실 업무 흐름이 원활해졌습니다는 보고가 있습니다. 수술 전 솔루션 분야의 자기 수혈 시스템 시장 점유율은 여전히 소규모이지만, 근거가 명확해짐에 따라 점차 확대되고 있습니다.

수술 후 배액 회수는 흉강 배액관이나 상처 흡입 장치에서 배출되는 양이 증가하는 노력에 상응하는 효과를 기대할 수 있는 심장외과나 인공관절 치환술 병동에서 꾸준히 보급되고 있습니다. 전 수술 과정 전반에 걸쳐 회수 절차를 표준화함으로써, 환자의 혈액 관리를 최대한 효율적으로 관리할 수 있으며, 가치 기반 보상 제도 하에서 더욱 엄격해지는 심사에 대비할 수 있습니다.

지역별 분석

북미는 확립된 임상 프로토콜, 메디케어에 의한 보험 급여, 그리고 향후 10년간 576억 달러의 비용 절감이 예상되는 신중한 ASC(외래수술센터(ASC)) 확장에 힘입어, 2025년에도 매출 점유율 42.78%를 유지했습니다. 미국의 병원에서는 종합적인 환자 혈액 관리 이니셔티브를 통해 연간 200만 달러의 비용 절감 효과가 입증되어, 첨단 회수 장비에 대한 지속적인 투자가 정당화되고 있습니다. 캐나다에서도 각 주가 주 차원의 혈액 관리 목표를 설정하는 가운데, 공공 자금으로 운영되는 의료 시스템 내에서 이와 유사한 제도가 도입되고 있습니다.

아시아태평양은 성장의 견인차 역할을 하고 있으며, 2031년까지의 연평균 성장률(CAGR)은 8.53%로 예측됩니다. 중국의 산부인과 병원에서는 세포 회수 시스템 도입에 성공하여 동종 수혈을 절반으로 줄였습니다. 일본은 헤모글로빈 소포 대체제 개발을 선도하고 있으며, 현재 인간 대상 임상시험이 진행 중입니다. 이는 2030년까지 회수 시스템을 대체하는 것이 아니라, 이를 보완할 잠재적인 수단이 될 것입니다. 인도, 인도네시아, 베트남은 2급 도시에 모듈식 수술실을 도입하기 위한 개발 자금을 배정하고 있으며, 보급형이지만 업그레이드가 가능한 장비에 대한 수요가 예상됩니다.

유럽에서는 외상학 및 마취학 분야의 통합 지침에 따라 살베이지 요법이 표준 치료법으로 자리 잡았으며, 한 자릿수 중반대의 성장세를 유지하고 있습니다. EU 의료기기 규정에 따른 재인증으로 인해 공급업체들은 품질 시스템의 업데이트를 요구받고 있으며, 규격에 부합하지 않는 구형 기기는 시장에서 퇴출되고, 자동화 기능을 갖춘 최신 모델이 선호되는 추세입니다.

중동 및 아프리카 및 남미 지역은 여전히 시장 침투율이 낮은 편이지만, 혈액 관리의 자급자족을 목표로 한 인도적 지원과 개발은행으로부터의 자금 조달을 유치하고 있습니다. 기증자 확보가 불안정한 분쟁 지역에서는 휴대용 배터리 구동 키트가 점차 보급되고 있습니다. 장기적으로는 전 세계 제조업체와 현지 간호학교 간에 체결되는 기술 향상을 위한 제휴가 이러한 신흥 시장의 개척을 가능하게 할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the autotransfusion systems market size was valued at USD 516.93 million in 2025 and is estimated to grow from USD 549.16 million in 2026 to reach USD 743.19 million by 2031, at a CAGR of 6.24% during the forecast period (2026-2031).

This report is Segmented by Product Type (Devices and Consumables), Application (Cardiac Surgeries, Orthopedic Surgeries, Organ Transplantation, and Others), End-User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (in USD Million) for the Above Segments.

Global Autotransfusion Systems Market Trends and Insights

Rising Volume & Complexity of Cardiac and Orthopedic Surgeries

Cardiac and orthopedic procedures grow in complexity, generating sizeable blood-loss volumes that make cell salvage indispensable. Cardiac operating rooms alone created 38.75% of 2024 demand, buoyed by uptake of transcatheter aortic valve replacements and multi-level spinal reconstructions. European trauma guidelines now instruct teams to deploy cell-salvage in severe bleeding, formalizing best practice . Aging populations amplify case volumes even as donor pools contract. Meta-analysis confirms a 39% cut in allogeneic transfusions when salvage is used across specialties. Consequently, the autotransfusion systems market becomes foundational operating-room infrastructure rather than an elective add-on.

Global Shortfall of Donor Blood and Stricter Transfusion Guidelines

The World Health Organization's patient-blood-management framework elevates autologous conservation to first-line status, compelling providers to adopt salvage systems as routine rather than contingency. In many African and Asian nations, annual donation deficits exceed 200,000 units, forcing hospitals to conserve every milliliter. Salvaged blood delivers fresher red cells and fewer immune reactions than stored alternatives, a benefit validated in controlled trials. Economically, each avoided unit saves hospitals upward of USD 500 in acquisition and complication costs, and full programs can return USD 1,367 per patient. With reimbursement aligning, the autotransfusion systems market benefits from a rare overlap of clinical, economic, and regulatory imperatives.

High Upfront Cost of Devices & Consumables Bundles

Turn-key systems range from USD 50,000 to USD 150,000, a steep outlay for budget-constrained clinics. Consumables add USD 200-400 per case, straining margins where reimbursement lags. Leasing and pay-per-use models mitigate sticker shock, yet adoption slows in smaller and public hospitals until such financing scales. Transitional Medicare coverage can offset risk, but global diffusion depends on broader payer alignment. The paradox remains: the sites that most need autotransfusion, those with severe donor shortages, often lack funds, tempering near-term market acceleration.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Containment Pressures in Hospitals

- Technological Shift to Fully Automated, Low-Volume Cell-Salvage Devices

- Additive-Manufactured Disposables Lowering Device Capex

- Lack of Skilled Perfusionists or Technicians in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices contributed 61.72% of 2025 revenue, underscoring hospitals' reliance on durable capital platforms. Meanwhile, consumables are projected to deliver a 7.03% CAGR, reflecting rising procedure counts and razor-and-blade pricing. The autotransfusion systems market size attributed to devices reached USD 319.07 million in 2025, whereas consumables reached USD 197.86 million. Manufacturers invest in miniaturization and intuitive user interfaces, removing elective hardware features to lower prices without compromising safety. On the consumables side, printable reservoirs and color-coded tubing sets simplify setup and cut waste. Over the forecast horizon, widespread installed bases will create predictable repeat demand that underwrites R&D returns.

Second-order growth stems from the alignment of flexible financing with consumable contracts. Hospital networks increasingly prefer low-commitment device leases that scale to volume, a model that simultaneously locks in consumable supply at negotiated rates. This combination stabilizes revenue and shields providers from one-time capital hits, fueling expansion of the autotransfusion systems market among community hospitals.

Intraoperative salvage delivered 35.42% of 2025 revenue, validating its entrenched role during high-blood-loss cases. Yet proactive strategies-preoperative autologous donation and acute normovolemic hemodilution-are climbing at 6.79% CAGR, an indicator that surgical teams aim to curb allogeneic exposure before the first incision. Hospitals that integrate preoperative modules report double-digit declines in transfusion volume and smoother OR workflows. The autotransfusion systems market share for preoperative solutions remains modest but is widening as evidence crystallizes.

Post-operative drainage recovery sees steady uptake in cardiac and joint replacement wards where chest-tube or wound-vac outputs justify the incremental effort. Standardizing salvage across the perioperative continuum maximizes patient blood management, preparing institutions for heightened scrutiny under value-based reimbursement.

Geography Analysis

North America retained 42.78% revenue share in 2025 thanks to entrenched clinical protocols, Medicare reimbursement, and measured ASC expansion that generated USD 57.6 billion in projected savings over the next decade . U.S. hospitals documented USD 2 million in annual savings from comprehensive patient-blood-management initiatives, justifying continued investment in advanced salvage hardware. Canada exhibits parallel uptake within its publicly funded system as provinces set provincial blood-management targets.

Asia-Pacific is the growth locomotive, with an 8.53% CAGR projected through 2031. China's maternity hospitals demonstrate successful cell-salvage rollouts that halve allogeneic transfusions. Japan pioneers hemoglobin-vesicle substitutes now in human trials, a potential adjunct to, rather than replacement for, salvage systems by 2030. India, Indonesia, and Vietnam allocate development funds to equip tier-2 cities with modular ORs, creating prospects for entry-level but upgradeable devices.

Europe sustains mid-single digit growth as unified trauma and anesthesiology guidelines cement salvage as standard of care. Re-certification under the EU Medical Device Regulation spurs suppliers to update quality systems, weeding out non-compliant legacy equipment and favoring modern, automation-rich models.

The Middle East & Africa and South America remain under-penetrated but attract humanitarian and development-bank funding aimed at blood-security self-sufficiency. Portable, battery-operated kits gain traction in conflict-affected zones where donor pools are unstable. Over time, skill-building alliances between global manufacturers and local nursing schools will unlock these frontier markets.

- Haemonetics

- LivaNova

- Medtronic

- Beckton Dickinson

- Fresenius

- Zimmer Biomet

- Beijing ZKSK Technology

- Braile Biomedica

- Redax S.p.A.

- Gen World Medical Devices

- Teleflex

- Soma Tech INTL

- Terumo Cardiovascular Systems

- Brightwake Ltd (Hemosep)

- SARSTEDT AG & Co.

- Atrium Medical (Getinge)

- Vascular Solutions (Teleflex)

- Stryker

- Fresenius

- Johnson & Johnson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume & Complexity Of Cardiac And Orthopedic Surgeries

- 4.2.2 Global Shortfall Of Donor Blood And Stricter Transfusion Guidelines

- 4.2.3 Cost-Containment Pressures In Hospitals Encouraging Blood-Conservation Technologies

- 4.2.4 Technological Shift To Fully Automated, Low-Volume Cell-Salvage Devices

- 4.2.5 Additive-Manufactured (3-D-Printed) Disposables Lowering Device Capex

- 4.2.6 Military & Disaster-Medicine Protocols Mandating Portable Autotransfusion Kits

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Of Devices & Consumables Bundles

- 4.3.2 Lack Of Skilled Perfusionists/Or Technicians In Emerging Markets

- 4.3.3 Haemolysis Risk In Haemolytic-Anemia & Paediatric Cohorts

- 4.3.4 Limited Clinical Evidence & Reimbursement In Obstetrics / Low-Resource Settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD Million)

- 5.1 By Product Type

- 5.1.1 Devices

- 5.1.2 Consumables

- 5.2 By Procedure Phase

- 5.2.1 Intra-operative

- 5.2.2 Post-operative

- 5.2.3 Pre-operative (PAD & ANH)

- 5.3 By Application

- 5.3.1 Cardiac Surgeries

- 5.3.2 Orthopedic Surgeries

- 5.3.3 Organ Transplantation

- 5.3.4 Trauma Procedures

- 5.3.5 Others

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty & Orthopedic Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Haemonetics Corporation

- 6.3.2 LivaNova PLC

- 6.3.3 Medtronic plc

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Fresenius Kabi AG

- 6.3.6 Zimmer Biomet

- 6.3.7 Beijing ZKSK Technology

- 6.3.8 Braile Biomedica

- 6.3.9 Redax S.p.A.

- 6.3.10 Gen World Medical Devices

- 6.3.11 Teleflex Incorporated

- 6.3.12 Soma Tech INTL

- 6.3.13 Terumo Cardiovascular Systems

- 6.3.14 Brightwake Ltd (Hemosep)

- 6.3.15 SARSTEDT AG & Co.

- 6.3.16 Atrium Medical (Getinge)

- 6.3.17 Vascular Solutions (Teleflex)

- 6.3.18 Stryker Corporation

- 6.3.19 Fresenius Medical Care

- 6.3.20 Johnson & Johnson (DePuy Synthes)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment