|

시장보고서

상품코드

2061657

영양유전체학 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Nutrigenomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

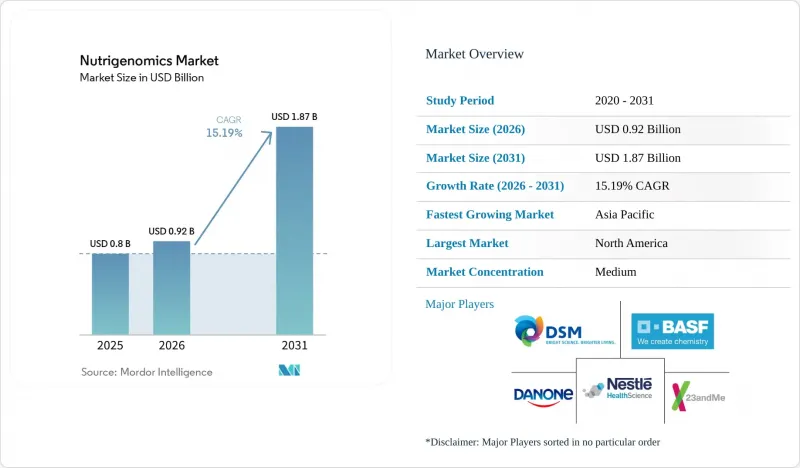

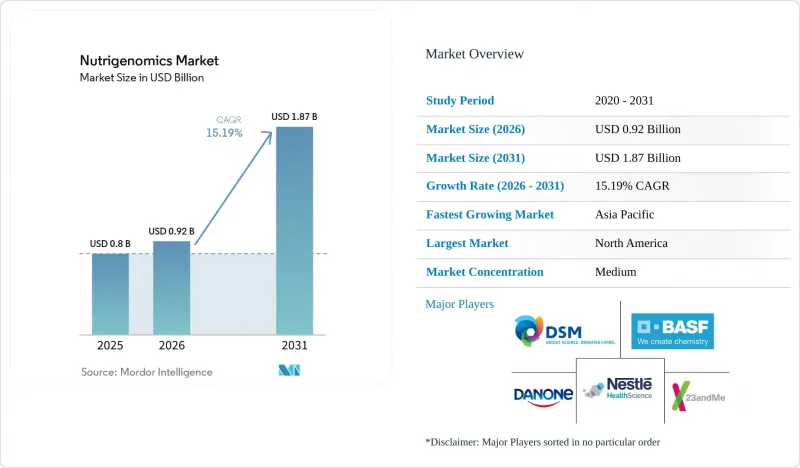

Mordor Intelligence에 의하면, 2026년 영양유전체학 시장 규모는 9억 2,000만 달러로 추정되고, 2025년 8억 달러에서 성장하여 2031년에는 18억 7,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 15.19%로 성장할 것으로 전망됩니다.

본 보고서는 용도별(심혈관 질환, 비만, 기타), 제품별(진단 키트 및 시약, 영양제(비타민 및 미네랄 등)), 최종 사용자별(병원 및 클리닉, 연구 기관 등), 유통 채널별(소비자 직접 판매 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 영양유전체학 시장 동향 및 인사이트

생활습관병으로 인한 부담 증가

현재, 식생활과 관련된 질환이 의료 예산의 상당 부분을 차지하고 있어, 보험사들은 예방 대책을 모색해야 하는 상황에 놓여 있습니다. 미국 국립보건원(NIH)은 유전자와 미생물군집의 상호작용을 규명하기 위해, 1만 명의 참가자를 대상으로 한 정밀영양학 연구에 1억 5,600만 달러를 지원했습니다. 초기 연구 결과에 따르면, FADS1 변이체가 오메가-3에 대한 반응을 변화시키는 것으로 나타났으며, 이를 바탕으로 한 표적형 보충제 섭취가 권장되고 있습니다. 의료계에서는 영양유전체학 시장을 당뇨병 전단계 환자의 발병을 지연시키기 위한 확장 가능한 도구로 자리매김하려는 움직임이 점점 더 강해지고 있습니다. 고용주는 결근을 줄이기 위해 유전자 기반 식단 계획에 자금을 지원하고 있으며, 보험사는 개인 맞춤형 영양 섭취 준수 정도에 따라 보험료를 할인해 주는 제도를 시범적으로 도입하고 있습니다. 이러한 노력에 힘입어, 유전자 데이터를 실용적인 식이 요법으로 전환해 주는 임상적으로 검증된 플랫폼에 대한 수요가 증가하고 있습니다.

차세대 염기서열 분석 기술의 비용 절감

전체 유전체 시퀀싱 비용은 10년 동안 1만 달러에서 600달러로 하락했으며, 업계 로드맵에 따르면 2030년까지 100달러 미만의 검사가 실현될 것으로 예측되고 있습니다. 3세대 장비는 더 긴 리드 길이를 구현하고, 증폭 바이어스를 최소화함으로써 메틸화, 지질 흡수, 카페인 대사를 관장하는 유전자의 분석 정확도를 높이고 있습니다. 진입 장벽이 낮아짐에 따라, 벤더들은 광범위한 다유전자 위험 점수를 구독 서비스에 통합할 수 있게 되었으며, 이를 통해 뉴트리제노믹스 시장의 타겟층을 피트니스 애호가에서 일반 웰니스 소비자로 확대되고 있습니다. 지속 혈당 모니터 및 마이크로바이옴 검사와의 원활한 통합을 통해 서비스의 차별화가 더욱 진전되고 있습니다.

세계 각국의 규제 체계가 제각각인 점

규제의 차이로 인해 기업은 여러 분류에 대응할 수밖에 없습니다. FDA는 신규 식품 성분에 대한 신고를 의무화하고 있지만, EU에서는 동등한 제품을 영양보조식품 규정에 따라 취급하고 있습니다. 중국에서는 기능성 식품과 건강식품의 신청 서류가 중복되어 비용과 시간이 증가하고 있습니다. 상호 인정이 이루어지지 않아 중복된 시험이 발생하고, 연구개발비가 증가함에 따라 소규모 진출기업들은 그 부담을 감당하기 어렵습니다. 규제 준수의 복잡성은 제품 출시를 18-24개월 지연시킬 가능성이 있어, 뉴트리제노믹스 시장의 단기 수익 잠재력을 축소시키는 한편, 견고한 거버넌스 시스템에 투자하는 초기 진입자들에게는 보상을 안겨줄 것입니다.

부문별 분석

2025년, 고용주들이 의료보험료 절감을 목적으로 맞춤형 식단 프로그램을 요구하는 가운데, 비만 관련 용도가 영양유전체학 시장 점유율의 35.10%를 차지했습니다. 이 부문의 방대한 규모 덕분에, 2025년 체중 관리 서비스 분야의 영양유전체학 시장 규모는 2억 8,000만 달러를 넘어섰습니다. 프레시전 종양는 규모는 작지만, 다유전자 위험 점수가 종양과 영양소 경로에 대한 표적화를 개선함에 따라 연평균 성장률(CAGR) 12.55%로 성장하고 있습니다. 심혈관 및 대사성 질환 관련 연구 포트폴리오는 충분히 검증된 지질과 유전자의 상관관계를 기반으로 하는 반면, 신경학 분야 연구에서는 유전자형과 신경전달물질 합성을 연결하는 장-뇌 메커니즘을 탐구하고 있습니다.

검사의 추세는 단일 질환 전용 패널에서 비만, 심혈관 및 대사 질환, 그리고 종양학적 위험 요인을 동시에 포괄하는 통합 검사로 전환되고 있습니다. 이러한 질환 전반에 걸친 접근 방식은 여러 가지 개입 방안을 제시하는 단일 보고서를 제공함으로써 고객 생애 가치(CLV)를 높입니다. 유전자 기반 오메가-3 섭취 계획을 뒷받침하는 CAPFISH-3 임상시험의 증거는 사례 보고 데이터에 회의적인 임상 의사들 사이에서 종양학 분야를 중심으로 한 도입을 가속화하고 있습니다. 임상 지침이 발전함에 따라, 용도의 다양화는 환급 제도의 변동에 대한 뉴트리제노믹스 시장 전체의 내성을 강화하는 방향으로 나아가고 있습니다.

2025년에는 확고히 자리 잡은 소비자 신뢰와 간소화된 규제 절차 덕분에 비타민 및 미네랄이 매출 점유율 30.85%로 1위를 차지했습니다. 이 부문의 매출액은 완제품 부문의 영양유전체학 시장 규모의 38%에 해당했습니다. 메타유전체 연구를 통해 유전자와 미생물군집의 시너지 효과가 입증됨에 따라, 프로바이오틱스와 프리바이오틱스가 연평균 성장률(CAGR) 12.18%로 성장을 주도하고 있습니다. 단백질 및 아미노산 제제는 액티브 에이징 트렌드의 수혜를 입고 있는 반면, 피토케미컬은 후성유전학적 조절 가능성 덕분에 주목을 받고 있습니다.

제품 혁신은 단일 영양소에 의존하는 해결책에서 벗어나, 유전적 변이 클러스터에 대응하는 복합 성분 배합으로 전환되고 있습니다. 프로바이오틱스와 포스트바이오틱스를 결합한 DSM-Firmenich사의 ‘Humiome’ 시리즈는 장내 환경을 중심으로 한 맞춤형 접근 방식으로의 전환을 상징합니다. 현재, AI 기반 엔진이 개개인의 다형성 프로파일에 맞추어 미량 영양소의 비율을 최적화하여, 매월 배송되는 맞춤형 영양제 플랜을 구성하고 있습니다. 이러한 발전은 영양유전체학 업계에서 차별화의 수준을 높이는 한편, 과학적 근거에 대한 기대감을 높이고 있습니다.

지역별 분석

북미는 FDA의 명확한 지침과 높은 가처분 소득에 힘입어 2025년 매출의 39.10%를 차지했습니다. 23andMe 등 미국의 업체들은 잘 갖춰진 원격의료 인프라를 활용하여 유전자 검사와 GLP-1 체중 감량 프로그램의 회원제 서비스를 결합함으로써 지속적인 수익 구조를 강화하고 있습니다. 캐나다에서는 임상 수준의 증거가 중시되고 있으며, 공급업체들은 의사와 제휴한 제공 모델로 전환하고 있습니다. 한편, 멕시코에서는 확대되는 중산층이 국경을 넘어 D2C 키트의 수입을 뒷받침하고 있습니다.

아시아태평양은 13.42%라는 가장 높은 연평균 성장률(CAGR)을 기록했습니다. 중국의 ‘건강중국 2030’ 계획은 정밀 영양 시범 사업에 자금을 지원하고 있으며, 현지 대기업들은 슈퍼 앱 생태계를 활용해 유전자 기반 식사 키트를 대규모로 추진하고 있습니다. 인도는 규제 환경이 제각각이지만, 의료 종사자들의 관심은 높으며, 조사 대상이었던 영양사들은 거의 전원이 유전체 정보 활용에 대한 의욕을 보이고 있습니다. 일본은 기능성 식품의 전통을 살려 유전자형에 특화된 발효 식품을 판매하고 있는 반면, 한국에서는 당뇨병 예방 캠페인에서 유전자 기반 메뉴 플랫폼이 도입되고 있습니다. 규제 환경은 지역마다 차이가 있지만, 각 지역의 스마트폰 보급률과 예방 의학에 대한 문화적 수용성이 영양유전체학 시장의 지속적인 성장을 뒷받침하고 있습니다.

유럽은 성숙해 가고 있음에도 불구하고, 세심하고 정교한 환경을 보여주고 있습니다. GDPR(EU 개인정보보호규정)은 데이터 거버넌스 기준을 의무화하고 있으며, 투명성이 높은 동의 획득 체계를 구축한 기업에 유리하게 작용하고 있습니다. 독일과 영국은 임상 현장에서의 도입을 주도하고 있는 반면, 지중해 국가들은 전통적인 식이 조사를 활용하여 상황에 맞는 유전자 기반 조언을 제공합니다. EU 회원국 간의 상호 인정을 통해 제품의 패스포트화 절차는 간소화되지만, 국가별 표시 규정의 미묘한 차이로 인해 모듈식 패키지 전략이 요구됩니다. EU가 무작위 대조 시험을 강력히 요구하고 있기 때문에 시장 출시까지 걸리는 기간은 길어지겠지만, 승인을 받게 되면 소비자의 신뢰는 높아질 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, nutrigenomics market size in 2026 is estimated at USD 0.92 billion, growing from 2025 value of USD 0.80 billion with 2031 projections showing USD 1.87 billion, growing at 15.19% CAGR over 2026-2031.

This report is Segmented by Application (Cardiovascular Diseases, Obesity, and Other Applications), Product (Diagnostic Kits and Reagents, and Nutrition {Vitamins & Minerals, and More}), End-User (Hospitals & Clinics, Research Institutes, and More), Distribution Channel (Direct To Consumer, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Nutrigenomics Market Trends and Insights

Growing Burden of Lifestyle-Related Chronic Diseases

Diet-linked illnesses now command most healthcare budgets, prompting payers to explore prevention. The NIH allocated USD 156 million to a precision-nutrition study covering 10,000 participants to map gene-microbiome interactions. Early findings show FADS1 variants alter omega-3 response, supporting targeted supplementation. Health systems increasingly position the Nutrigenomics market as a scalable tool for delaying diabetes onset in pre-diabetic groups. Employers finance genetic-guided meal plans to reduce absenteeism, while insurers pilot premium discounts tied to personalized nutrition adherence. These initiatives elevate demand for clinically validated platforms that translate gene data into actionable diet protocols.

Declining Costs of Next-Generation Sequencing Technologies

Whole-genome sequencing fell from USD 10,000 to USD 600 within a decade, and industry roadmaps forecast sub-USD 100 tests before 2030. Third-generation instruments yield longer reads and minimize amplification bias, increasing accuracy for genes governing methylation, lipid uptake, and caffeine metabolism. Lower barriers let vendors bundle broad polygenic risk scores into subscription services, expanding the Nutrigenomics market's addressable base beyond fitness enthusiasts to mainstream wellness consumers. Seamless integration with continuous glucose monitors and microbiome assays further differentiates offerings.

Lack Of Harmonized Global Regulatory Framework

Divergent rules force companies to navigate multiple classifications. The FDA requires new dietary ingredient notifications, whereas the EU treats comparable products under food supplement codes. China layers functional-food and health-food dossiers, adding cost and time. Absence of mutual recognition triggers redundant trials, inflating R&D expenses that smaller entrants struggle to absorb. Compliance complexities can delay launches by 18-24 months, trimming the Nutrigenomics market's near-term revenue potential but also rewarding early movers investing in robust governance systems.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Consumer Awareness of Gene-Diet Interactions

- Proliferation Of Digital Health Platforms Integrating Nutrigenomic Data

- Limited Clinical Utility Evidence Supporting Nutrigenomic Recommendations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Obesity applications accounted for 35.10% of the nutrigenomics market share in 2025 as employers sought personalized diet programs to curb healthcare premiums. The segment's sheer volume ensured that the Nutrigenomics market size for weight-management services surpassed USD 0.28 billion in 2025. Precision oncology, though smaller, is expanding at 12.55% CAGR because polygenic risk scores improve tumor-nutrient pathway targeting. Cardiovascular and metabolic disorder portfolios ride on well-validated lipid-gene correlations, while neurological research explores gut-brain mechanisms linking genotype to neurotransmitter synthesis.

Research momentum is moving from single-condition panels toward integrated tests covering obesity, cardiometabolic, and oncologic risks simultaneously. This cross-condition architecture boosts customer lifetime value by offering one report that informs multiple interventions. Evidence from CAPFISH-3 supporting gene-guided omega-3 regimens accelerates oncology-focused adoption among clinicians wary of anecdotal data. As clinical guidelines evolve, application diversification is poised to fortify overall Nutrigenomics market resilience against reimbursement shocks.

Vitamins and minerals led with 30.85% revenue share in 2025, owing to established consumer trust and streamlined regulatory pathways. Segment revenue equated to 38% of the Nutrigenomics market size for finished products. Probiotics and prebiotics capture growth at 12.18% CAGR as metagenomic studies validate gene-microbiome synergies. Protein and amino acid formulations benefit from active-aging trends, whereas phytochemicals gain attention for epigenetic modulation potential.

Product innovation is tilting toward multi-compound blends that address clusters of genetic variants instead of one-nutrient solutions. DSM-Firmenich's Humiome line, which pairs probiotics with postbiotics, exemplifies the shift toward gut-centric personalization. AI formulation engines now optimize micronutrient ratios to match individual polymorphism profiles, creating bespoke supplement schemes shipped monthly. These developments broaden differentiation levels within the Nutrigenomics industry while raising expectations for scientific substantiation.

Geography Analysis

North America contributed 39.10% of 2025 revenue, anchored by clear FDA guidance and high discretionary income. United States operators such as 23andMe leverage a robust telehealth infrastructure to bundle genetic tests with GLP-1 weight-loss memberships, reinforcing recurring revenue loops. Canada emphasizes clinical-grade evidence, nudging vendors toward physician-partnered delivery models, while Mexico's expanding middle class fuels cross-border D2C kit imports.

Asia Pacific recorded the fastest CAGR at 13.42%. China's Healthy China 2030 blueprint funds precision nutrition pilots, and local giants use super-app ecosystems to push gene-driven meal kits at scale. India faces heterogeneous regulations yet shows strong practitioner interest, with nearly all surveyed dietitians keen to integrate genomic insights. Japan leverages its functional-food heritage to market genotype-specific fermented products, whereas South Korea's anti-diabetes campaigns embrace gene-guided menu platforms. Despite regulatory patchwork, regional smartphone penetration and cultural openness to preventive health underpin sustained momentum for the Nutrigenomics market.

Europe presents a mature but meticulous environment. GDPR mandates data-governance thresholds, rewarding firms with transparent consent architectures. Germany and the United Kingdom lead uptake inside clinical settings, whereas Mediterranean countries leverage traditional diet research to contextualize gene advice. Mutual recognition across EU states simplifies product passporting, yet country-specific labeling nuances compel modular packaging strategies. The bloc's insistence on randomized trials prolongs time-to-market but yields high consumer trust once approvals are obtained.

- DSM

- BASF

- Danone

- Nestle

- Unilever

- 23andMe

- Viome

- Metagenics

- Genova Diagnostics

- Nutrigenomix

- GX Sciences

- Xcode Life

- Cell-Logic

- DayTwo

- Prenetics

- Persona Nutrition

- Herbalife Nutrition

- Amway

- Perrigo Company

- CuraLife

- GeneSmart

- Holistic Heal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Lifestyle-Related Chronic Diseases

- 4.2.2 Declining Costs of Next-Generation Sequencing Technologies

- 4.2.3 Expanding Consumer Awareness of Gene-Diet Interactions

- 4.2.4 Proliferation of Digital Health Platforms Integrating Nutrigenomic Data

- 4.2.5 Strategic Alliances Between Nutraceutical, Biotech, And Big-Data Companies

- 4.2.6 Employer And Insurer Adoption of Preventive Nutrition Genomics Programs

- 4.3 Market Restraints

- 4.3.1 Lack of Harmonized Global Regulatory Framework

- 4.3.2 Limited Clinical Utility Evidence Supporting Nutrigenomic Recommendations

- 4.3.3 Rising Data-Privacy and Cybersecurity Concerns Around Genomic Databases

- 4.3.4 Low Physician Awareness and Education in Nutrigenomics Principles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Cardiovascular Diseases

- 5.1.2 Obesity

- 5.1.3 Cancer Research

- 5.1.4 Metabolic Disorders

- 5.1.5 Neurological Disorders

- 5.1.6 Other Applications

- 5.2 By Product

- 5.2.1 Diagnostic Kits and Reagents

- 5.2.2 Nutrition

- 5.2.2.1 Vitamins & Minerals

- 5.2.2.2 Probiotics & Prebiotics

- 5.2.2.3 Proteins & Amino Acids

- 5.2.2.4 Phytochemicals

- 5.2.2.5 Others

- 5.3 By End-User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Research Institutes & Universities

- 5.3.3 Direct-to-Consumer Companies

- 5.3.4 Pharmaceutical & Biotech Firms

- 5.3.5 Nutrition & Fitness Centers

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales

- 5.4.2 Online Platforms

- 5.4.3 Retail Pharmacies

- 5.4.4 Healthcare-Practitioner Sales

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.3.1 DSM

- 6.3.2 BASF SE

- 6.3.3 Danone

- 6.3.4 Nestle Health Science

- 6.3.5 Unilever Group

- 6.3.6 23andMe

- 6.3.7 Viome

- 6.3.8 Metagenics Inc.

- 6.3.9 Genova Diagnostics

- 6.3.10 Nutrigenomix Inc.

- 6.3.11 GX Sciences Inc.

- 6.3.12 Xcode Life

- 6.3.13 Cell-Logic

- 6.3.14 DayTwo

- 6.3.15 Prenetics

- 6.3.16 Persona Nutrition

- 6.3.17 Herbalife Nutrition

- 6.3.18 Amway Corporation

- 6.3.19 Perrigo Company

- 6.3.20 CuraLife

- 6.3.21 GeneSmart

- 6.3.22 Holistic Heal

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment