|

시장보고서

상품코드

2061659

2-에틸헥산올 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)2-Ethyl Hexanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

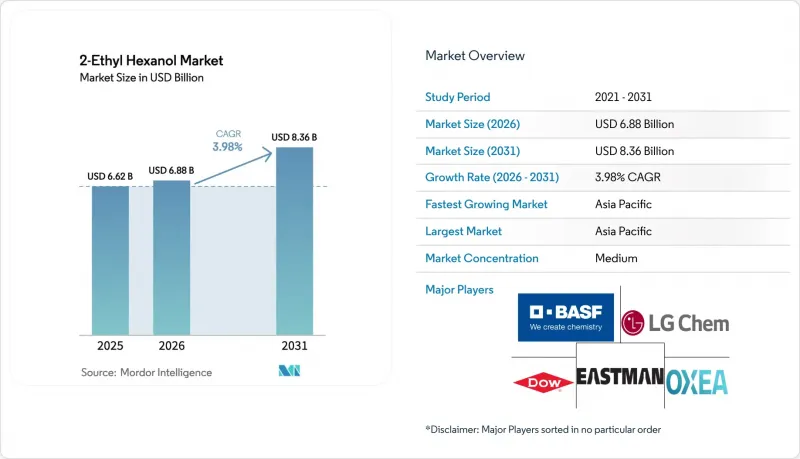

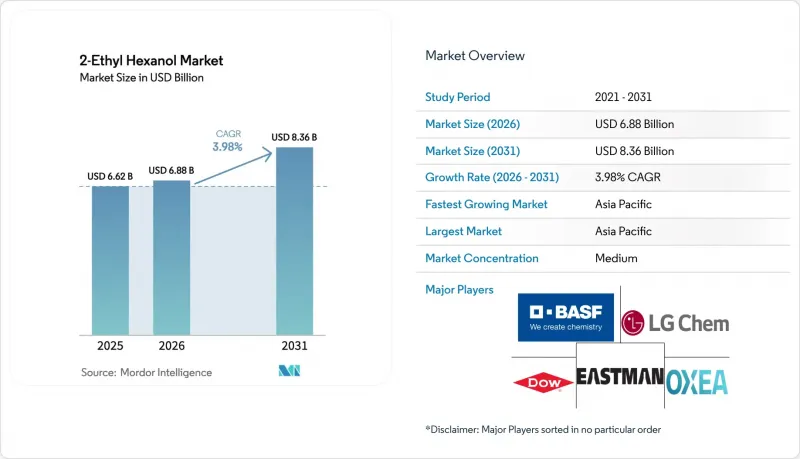

Mordor Intelligence에 의하면,2-에틸헥산올 시장 규모는 2025년 66억 2,000만 달러로 평가되었습니다. 2026년에는 68억 8,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 3.98%를 나타내, 2031년까지 83억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도별(가소제, 2-EH 아크릴레이트, 2-EH 질산염, 기타), 최종 사용자별(페인트 및 코팅, 접착제, 산업용 화학제품, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 2-에틸헥사놀 시장 동향 및 분석

가소화된 PVC에 대한 가소제 수요 증가(건설 및 자동차)

가소화된 PVC는 전선 및 케이블, 바닥재, 필름, 내장재 분야에서 여전히 필수적인 소재이며, 2024년에는 유연성 PVC용 가소제가 전 세계 가소제 사용량의 38.6%를 차지했습니다. 인도에서 진행 중인 370억 달러 규모의 석유화학 플랜트 건설은 DEHP(디(2-에틸헥실)프탈레이트)와 새로운 테레프탈산 에스테르에 대한 국내 수요를 촉진하고 있습니다. 한편, 자동차 경량화로 인해 OEM(원청 브랜드 제조업체)은 프로포지션 65 및 REACH의 이행 제한을 충족할 수 있는 DOTP(디옥틸테레프탈산)와 같은 비프탈레이트계 대체재로 전환하고 있습니다. 배터리식 전기차(BEV)의 보급은 하네스 및 배터리 팩 외장재에 사용되는 난연성이며 저이동성인 가소제에 대한 수요를 더욱 확대시키고 있으며, 고품질의 트리메틸산 에스테르 및 시클로헥사노에이트 에스테르에 대한 관심을 높이고 있습니다. 따라서 각 제조업체는 기존 프탈산 에스테르의 배합을 변경해 나가는 과정에서도, 알코올 성분으로서 2-에틸헥사놀에 계속 의존하고 있습니다.

고고형분·저VOC 도료의 채택 확대가 2-EH 아크릴레이트 사용을 견인

건축 및 산업용 배합 제조업체들은 EU 지침 2004/42/EC 및 미국 환경보호청(EPA)의 대기 유해 물질 규제를 충족하기 위해, VOC 배출량을 30-50% 감축하는 고고형분 수지로의 전환을 추진하고 있습니다. 2-에틸헥실 아크릴레이트는 더 긴 알킬 사슬을 가지고 있어, 내마모성을 저해하지 않으면서 필름의 유연성과 ? 에지 시간을 향상시키기 때문에 부틸 아크릴레이트를 대체하고 있습니다. BASF는 에너지 비용 및 규정 준수 비용의 상승을 상쇄하기 위해 2026년 3월 아시아태평양 전체에서 2-EHA 가격을 톤당 최대 100달러 인상하며, 수급 균형의 긴박함을 여실히 드러냈습니다. 해상 풍력 발전 타워나 해양 자산의 경우, ISO 12944 부식 규격을 충족하기 위해 2-EHA 기반 수지가 채택되고 있는 반면, 전자상거래(EC)용 포장 분야에서는 2-EHA 공중합체에 기반한 속경화·저취성 감압 접착제에 대한 수요가 증가하고 있습니다.

기존 가소제 공급망을 제한하는 프탈레이트 관련 규제

캘리포니아주의 AB 2300 법안은 2030년까지 수액백, 2035년까지 튜브에서 DEHP 사용을 금지하고 있는 반면, 유럽화학물질청(ECHA)은 대부분의 제품에 대해 4가지 주요 프탈레이트 에스테르의 함유량을 중량 기준 0.1% 미만으로 제한하고 있습니다. 그 결과, 프탈산 에스테르 계열 이외의 가소제 시장은 2024년 39억 9,000만 달러에서 2025년에는 43억 달러로 확대되었고, 연평균 성장률(CAGR) 7.47%를 기록하며, 2030년까지 61억 5,000만 달러에 달할 것으로 전망됩니다. 독일과 미국에서의 생산 능력 확충으로 인해 DOTP 및 DINCH의 프리미엄은 10% 미만으로 축소되었으나, 프탈산계와 비프탈산계 공급망을 병행하여 유지하는 것은 생산자의 영업 비용을 약 29% 가중시키고 있습니다.

부문별 분석

2025년, 가소제는 2-에틸헥사놀 시장 점유율의 58.65%를 차지했으며, 유연성 PVC는 케이블, 바닥재, 필름 용도에서 계속해서 주류를 이루었습니다. 아크릴레이트 관련 2-에틸헥사놀 시장 규모는 2031년까지 연평균 성장률(CAGR) 6.31%로 확대될 것으로 전망됩니다. 이는 저VOC 도료와 감압 접착제가 유연성과 경화 균형을 위해 2-EHA의 긴 알킬 사슬에 의존하고 있기 때문에 다른 모든 용도를 능가하는 성장률을 보일 것입니다.

규제에 따른 전환 상한선으로 인해 수요는 DEHP에서 DOTP와 같은 테레프탈산 에스테르나 DINCH와 같은 시클로헥사노에이트로 점차 전환되고 있지만, 이들 역시 여전히 알코올 성분으로서 2-에틸헥사놀에 의존하고 있습니다. BASF와 에보닉은 2024년부터 2025년에 걸쳐 독일에서 DINCH 생산 능력을 확대하여, 기존 공급 병목 현상을 해소하는 동시에 기존 프탈산 에스테르와의 가격 차이를 한 자릿수 수준으로 줄였습니다.

지역별 분석

아시아태평양은 2025년 매출의 53.12%를 차지했으며, 인도의 수십억 달러 규모 정유시설 확장 및 중국에서 진행 중인 인프라 건설이 유연성 PVC 및 코팅재 수요를 뒷받침함에 따라 2031년까지 연평균 성장률(CAGR) 5.98%를 나타낼 것으로 전망됩니다. 중국 정부의 구형 나프타 크래커 통합 및 2026년 2월 한국이 태산의 연간 110만 톤 규모 공장을 폐쇄할 예정인 점으로 미루어 볼 때, 해당 지역 내 올레핀 공급이 부족해질 것으로 예상되며, 단기적으로는 2-EH 가격이 강세를 보일 가능성이 있습니다. 동시에, 2026년 가동을 예정하고 있는 새로운 폴리에틸렌 및 폴리프로필렌 프로젝트 덕분에, 2025년 PDH의 수익성을 압박했던 프로파일렌 부족 현상이 완화될 전망입니다.

북미에서는 셰일가스에서 추출한 에탄을 활용하고 있지만, 건설 시장의 성숙과 관세 변동에 직면해 있습니다. 이스트먼사의 텍사스주 롱뷰에 위치한 통합 옥소 플랫폼은 현지 프로파일렌 공급을 확보하고 마진 변동을 완화하는 한편, 캘리포니아주에서 다가오는 DEHP 금지 조치로 인해 의료기기 분야에서 DOTP 및 DINCH로의 전환이 가속화되고 있습니다. 멕시코와 캐나다는 USMCA 규정에 따라 자동차 내장재와 하네스를 공급하고 있으며, 저이동성 가소제 및 고고형분 접착제에 대한 수요가 증가하고 있습니다.

유럽은 가장 엄격한 프탈레이트 규제를 시행하고 있지만, 재생 가능 원료의 도입에 있어서는 주도적인 입장에 있습니다. BASF는 루트비히스하펜에서 DINCH 생산량을 두 배로 늘렸으며, 에보닉도 2024년에 마를에서 DINCH/DINCD 생산 능력을 확대했습니다. 이는 비프탈레이트계 제품의 생산량이 DEHP 수요 감소를 상쇄할 것이라는 확신을 반영한 것입니다. 페르스토프의 ISCC PLUS 인증을 획득한 재생 가능 2-EH는 의료기기 제조업체의 Scope 3 배출량 감축을 목표로 하고 있습니다. 그러나 저가 아시아산 가소제의 수입으로 인해 이익률이 압박받고 있으며, 서유럽 전역에서 크래커가 폐쇄되는 가운데 생산 능력의 합리화가 진행될 가능성이 있습니다.

남미 및 중동 및 아프리카은 여전히 규모는 작지만, 계속해서 성장하고 있습니다. 브라질의 연질 PVC 제조업체와 사우디아라비아의 에탄 기반 크래커가 수요 증가를 견인하고 있는 반면, 남아프리카공화국의 디젤 발전기 군이 2-EH 질산염의 연간 5% 성장을 뒷받침하고 있습니다. 호르무즈 해협을 경유하는 원료 공급 차질에 대한 지역적 취약성은 지정학적 긴장이 고조될 때마다 전 세계 2-에틸헥사놀 가격을 지지하는 요인으로 작용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the 2-Ethyl hexanol market size is expected to grow from USD 6.62 billion in 2025 to USD 6.88 billion in 2026 and is forecast to reach USD 8.36 billion by 2031 at 3.98% CAGR over 2026-2031.

This report is Segmented by Application (Plasticizers, 2-EH Acrylate, 2-EH Nitrate, and Other Applications), End-User (Paint and Coatings, Adhesives, Industrial Chemicals, and Other End-Users), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Size and Forecasts are Provided in Terms of Value (USD).

Global 2-Ethyl Hexanol Market Trends and Insights

Plasticizers Demand Growth in Flexible PVC (Construction and Automotive)

Plasticized PVC remains essential for wire-and-cable, flooring, films, and interior trim, and flexible PVC plasticizers captured 38.6% of global plasticizer use in 2024. India's USD 37 billion petrochemical build-out is reinforcing domestic demand for both DEHP (Di(2-ethylhexyl)phthalate) and newer terephthalate esters, while automotive lightweighting is steering OEMs (original equipment manufacturers) toward non-phthalate alternatives such as DOTP (dioctyl terephthalate) that can satisfy Proposition 65 and REACH migration limits. Battery-electric vehicles further amplify the need for flame-retardant, low-migration plasticizers in harnesses and pack enclosures, fostering interest in premium trimellitate and cyclohexanoate esters. Producers, therefore, continue to rely on 2-ethylhexanol as an alcohol component even as they reformulate away from legacy phthalates.

Rising Adoption of High-Solids / Low-VOC Coatings Driving 2-EH Acrylate Usage

Architectural and industrial formulators are shifting to high-solids resins that cut VOC emissions 30-50% to meet EU Directive 2004/42/EC and U.S. EPA (Environmental Protection Agency) air-toxics rules. 2-Ethylhexyl acrylate replaces butyl acrylate because its longer alkyl chain improves film flexibility and wet-edge time without sacrificing scrub resistance. BASF raised 2-EHA prices by as much as USD 100 per tonne across Asia-Pacific in March 2026 to offset rising energy and compliance costs, underscoring tight supply-demand balances. Offshore wind towers and marine assets are adopting 2-EHA-based resins to satisfy ISO 12944 corrosion standards, while e-commerce packaging fuels demand for fast-curing, low-odor pressure-sensitive adhesives that depend on 2-EHA copolymers.

Phthalate-Related Regulations Restricting Traditional Plasticizer Chain

California's AB 2300 outlaws DEHP in IV bags by 2030 and tubing by 2035, while the European Chemicals Agency restricts four major phthalates below 0.1 wt% in most goods. As a result, non-phthalate plasticizers advanced from USD 3.99 billion in 2024 to USD 4.30 billion in 2025 and should attain USD 6.15 billion by 2030 at 7.47% CAGR. Premiums for DOTP and DINCH have narrowed to under 10% thanks to capacity additions in Germany and the United States, but maintaining parallel phthalate and non-phthalate supply chains inflates producer operating costs by roughly 29%.

Other drivers and restraints analyzed in the detailed report include:

- Diesel Performance Additives (2-EH Nitrate) Demand in Emerging Markets

- Capacity Expansions in Asia-Pacific Improving Price Competitiveness

- Volatile Propylene Feedstock Prices Squeezing Producer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plasticizers maintained 58.65% of the 2-Ethylhexanol market share in 2025 as flexible PVC continued to dominate cable, flooring, and film applications. The 2-Ethylhexanol market size tied to Acrylates is forecast to expand at a 6.31% CAGR through 2031, outpacing every other application because low-VOC coatings and pressure-sensitive adhesives rely on 2-EHA's long alkyl chain for flexibility and cure balance.

Regulatory migration caps are shifting demand away from DEHP toward terephthalate esters such as DOTP and cyclohexanoates like DINCH, yet these still depend on 2-ethylhexanol as the alcohol component. BASF and Evonik upgraded DINCH capacity in Germany during 2024 and 2025, removing previous supply bottlenecks and narrowing the price gap with legacy phthalates to single-digit percentages.

Geography Analysis

Asia-Pacific captured 53.12% of 2025 revenue and should post 5.98% CAGR through 2031 as India's multi-billion-dollar refinery expansions and China's ongoing infrastructure build sustain flexible PVC and coatings demand. Beijing's consolidation of older naphtha crackers and South Korea's shuttering of a 1.1 million tons per year unit at Daesan in February 2026 will tighten regional olefins and potentially firm 2-EH pricing in the near term. Concurrently, fresh polyethylene and polypropylene projects due online in 2026 promise to ease the propylene deficit that weighed on PDH economics in 2025.

North America leverages shale-advantaged ethane but contends with mature construction markets and tariff volatility. Eastman's Longview, Texas, integrated Oxo platform secures local propylene and cushions margin swings, while California's looming DEHP bans accelerate the pivot to DOTP and DINCH in medical devices. Mexico and Canada supply automotive interiors and harnesses under USMCA rules, intensifying demand for low-migration plasticizers and high-solids adhesives.

Europe enforces the tightest phthalate regulations, yet it is leading on renewable content. BASF doubled DINCH output at Ludwigshafen, and Evonik boosted DINCH/DINCD capacity at Marl in 2024, reflecting confidence that non-phthalate volumes will offset shrinking DEHP demand. Perstorp's ISCC PLUS-certified renewable 2-EH targets scope-3 emission cuts for medical-device firms. However, imports of low-cost Asian plasticizers compress margins, and capacity rationalizations are likely as crackers close across Western Europe.

South America and the Middle East & Africa remain smaller but expanding. Brazil's flexible-PVC manufacturers and Saudi Arabia's ethane-based crackers support incremental demand, while South Africa's diesel generator fleet underpins 5% annual growth in 2-EH nitrate. Regional exposure to feedstock shocks via the Strait of Hormuz continues to set a floor under global 2-ethylhexanol prices when geopolitical tensions escalate.

- BASF

- Bharat Petroleum Corporation Ltd.

- Dow

- Eastman Chemical Company

- Elekeiroz

- Formosa Plastics Group

- Gazprom Neftekhim Salavat

- Grupa Azoty

- Hanwha Solutions Chemical Division

- INEOS Corporation

- KH Neochem Co. Ltd.

- LG Chem

- Mitsubishi Chemical Corporation

- NAN YA PLASTICS CORPORATION

- OQ Chemicals GmbH

- Perstorp

- SABIC

- Shandong Qilu Petrochemical Engineering Co. Ltd

- Soveuk Chemical Co.,Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plasticizers demand growth in flexible PVC (construction and automotive)

- 4.2.2 Rising adoption of high-solids/low-VOC coatings driving 2-EH acrylate usage

- 4.2.3 Diesel performance additives (2-EH nitrate) demand in emerging markets

- 4.2.4 Capacity expansions in Asia-Pacific improving price competitiveness

- 4.2.5 Bio-based 2-EH pilot plants gaining regulatory incentives

- 4.3 Market Restraints

- 4.3.1 Phthalate-related regulations restricting traditional plasticizer chain

- 4.3.2 Volatile propylene feedstock prices squeezing producer margins

- 4.3.3 EU REACH evaluation may tighten occupational exposure limits

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Applications

- 5.1.1 Plasticizers

- 5.1.2 2-EH Acrylate

- 5.1.3 2-EH Nitrate

- 5.1.4 Other Applications

- 5.2 By End User

- 5.2.1 Paint and Coatings

- 5.2.2 Adhesives

- 5.2.3 Industrial Chemicals

- 5.2.4 Other End-Users

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Southeast Asia

- 5.3.1.6 Australia and New Zealand

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 BASF

- 6.4.2 Bharat Petroleum Corporation Ltd.

- 6.4.3 Dow

- 6.4.4 Eastman Chemical Company

- 6.4.5 Elekeiroz

- 6.4.6 Formosa Plastics Group

- 6.4.7 Gazprom Neftekhim Salavat

- 6.4.8 Grupa Azoty

- 6.4.9 Hanwha Solutions Chemical Division

- 6.4.10 INEOS Corporation

- 6.4.11 KH Neochem Co. Ltd.

- 6.4.12 LG Chem

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 NAN YA PLASTICS CORPORATION

- 6.4.15 OQ Chemicals GmbH

- 6.4.16 Perstorp

- 6.4.17 SABIC

- 6.4.18 Shandong Qilu Petrochemical Engineering Co. Ltd

- 6.4.19 Soveuk Chemical Co.,Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment