|

시장보고서

상품코드

2061660

산업용 냉동 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Refrigeration System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

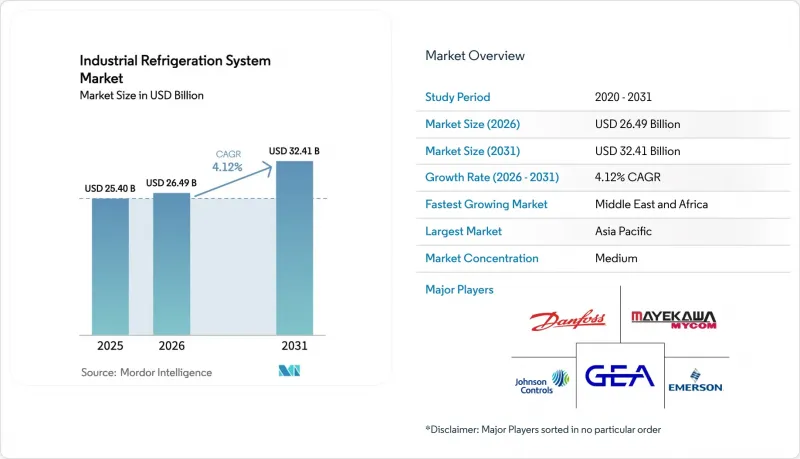

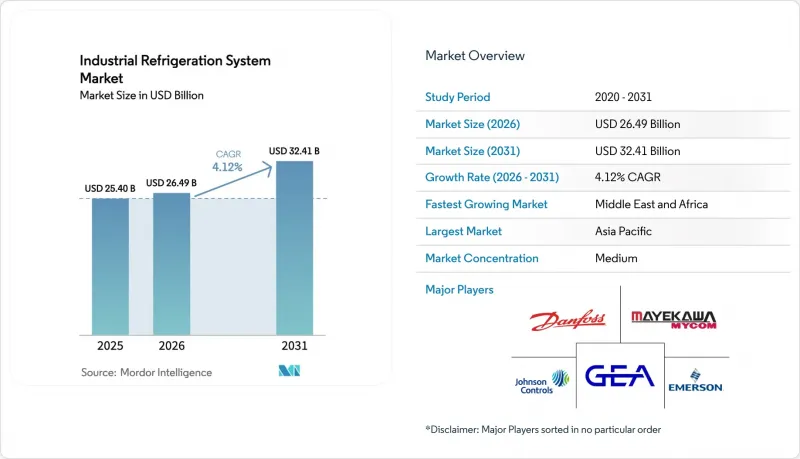

Mordor Intelligence에 의하면, 산업용 냉동 시스템 시장 규모는 2025년에 254억 달러로 평가되었고, 2026년 264억 9,000만 달러로 추정되고, 2031년까지 324억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.12%를 나타낼 전망입니다.

본 보고서는 장비별(압축기, 응축기, 증발기 등), 냉매별(암모니아, 이산화탄소 등), 용도별(식품 및 음료 가공, 냉장 및 물류 등), 시스템 용량별(100kW 미만 등), 시스템 유형별(단단식, 2단식 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 산업용 냉동 시스템 시장 동향과 인사이트

자동화 콜드체인 창고의 급증

자동화된 콜드체인 물류센터는 영하의 온도에서 24시간 가동되는 소수의 대용량 허브로 처리량을 집중시키기 때문에 2메가와트 이상의 암모니아 시스템 수요를 견인하고 있습니다. 주요 업체들의 투자 발표는 이러한 추세를 뒷받침하고 있으며, 대규모 냉동식품 시설에서는 ±0.5℃라는 더욱 엄격한 온도 제어가 요구됨에 따라 다단 압축 및 캐스케이드 방식의 도입이 확대되고 있습니다. 아시아 식료품 전자상거래의 성장은 기존 설비의 개조를 더욱 가속화하고 있으며, 물류 업체들은 가변속 스크류 압축기 및 IoT 지원 증발기 팬의 도입을 추진하고 있습니다. 자동 창고용 크레인 제조업체들도 로봇에 결로가 생기는 것을 방지하기 위해 기계적 이송과 냉동 제어를 연동하여, 더욱 엄격한 온도 허용 범위를 설정하고 있습니다. 그 결과, 산업용 냉동 시스템 시장에서는 프로젝트의 평균 규모가 커지고 장기 서비스 계약이 증가하면서 애프터마켓의 수익원을 확대되고 있습니다.

F-가스 규제 및 키갈리 협정 준수 기한의 강화

규제에 따른 단계적 감축 일정에 따라 신규 HFC 장비의 도입 가능 기간이 단축되면서, 자연 냉매로의 전환이 급증하고 있습니다. 유럽연합(EU)은 현재 2030년까지 HFC 사용량을 95% 감축하도록 의무화하고 있으며, 한편 미국에서는 2025년 1월부터 신규 산업용 공정 냉동 설비에 HFC 사용이 금지됩니다. 누출 추적에 관한 문서화 규정은 관리 비용을 증가시키기 때문에 충전 및 기밀 시험이 완료된 상태로 납품되는 공장 출하 시의 암모니아 및 CO2 랙이 선호되고 있습니다. 일본의 이산화탄소 환산 톤당 3,000엔의 탄소 가격으로 인해 HFC 누출의 직접 비용이 증가하는 가운데, 벌금에 따른 제재가 규정 위반의 위험을 더욱 높이고 있습니다. 이러한 정책들의 조합으로 인해, 성숙한 경제권에서는 총 설치 용량이 안정적임에도 불구하고 산업용 냉동 시스템 시장의 성장을 뒷받침하는 교체 주기가 가속화되고 있습니다.

천연 냉매에 따른 높은 설비 투자 비용 및 숙련된 인력 부족

천연 냉매 플랜트는 스테인리스제 열교환기, 강화된 환기 시스템, 이중화된 안전 인터록 등의 이유로 HFC 제품보다 20-40% 더 높은 비용이 듭니다. 예산상의 압박은 공인 암모니아 기술자공급 부족으로 인해 더욱 심화되고 있습니다. 특히 북미에서는 은퇴자가 연수 참가자 수를 웃돌고 있습니다. 인증 기관은 2년간의 지도 하에 이루어지는 실무 경험을 요건으로 하고 있으며, 이로 인해 인력 충원이 지연되고 프로젝트 일정이 연장되고 있습니다. 미국의 주요 대도시권에서는 인건비가 시간당 150달러에 달하고 있으며, 이러한 추가 비용으로 인해 투자 회수 기간이 길어지면서 중소기업의 산업용 냉동 시스템 시장 도입이 주춤하고 있습니다. 장비 공급업체들은 현장 작업을 줄여주는 공장 제작형 스키드 장착 모듈로 대응하고 있지만, 당분간 인력 부족은 프로젝트 진행 속도를 늦추는 요인이 될 것입니다.

부문별 분석

제어 장비는 이미 산업용 냉동 시스템 시장에서 가장 빠르게 성장하고 있는 분야입니다. 압축기는 2025년에도 매출 점유율 36.18%를 유지하며 그 핵심적인 역할을 입증하고 있지만, 프로그래머블 로직 컨트롤러(PLC), 가변 주파수 드라이브, 그리고 클라우드 대시보드는 2031년까지 연평균 성장률(CAGR) 4.93%로 성장하고 있습니다. 이러한 확대는 시스템 용량이 100kW를 초과할 경우 수요 반응(Demand Response) 통합을 의무화하는 캘리포니아주 ‘타이틀 24’ 개정안 등의 규제를 반영한 것입니다. 첨단 구동 장치는 압축기의 에너지 소비를 최대 50%까지 줄여주어, 시설 소유주가 18개월 이내에 투자 비용을 회수할 수 있도록 합니다. 또한, 이러한 에너지 절감 효과로 인해 연기되었던 프로젝트가 실현되어 산업용 냉동 시스템 시장 전체의 규모가 확대될 것입니다. 응축기와 증발기는 설계 발전이 획기적인 효율 향상보다는 단계적인 열전달 효율 향상에 중점을 두고 있기 때문에 시장 평균보다 낮은 수준입니다. 리시버와 열교환기는 캐스케이드 설계나 트랜스크리티컬 설계에서 중간 열교환이 필요하기 때문에 수요가 증가하고 있으며, 설치당 부품 원가(BOM) 가치를 높이고 있습니다. 제어 장비 공급업체들은 분석 서비스 구독권도 함께 제공함으로써, 거시경제 사이클 전반에 걸쳐 수익을 안정화시키는 정기 수입원을 창출하고 있습니다.

디지털 개조는 기존 플랜트(브라운필드)를 점점 더 주요 대상으로 삼고 있습니다. 성숙한 경제권의 사업자들은 기존 압축기에 새로운 구동 장치나 센서 키트를 결합함으로써, 이미 투자된 하드웨어 비용을 활용하는 동시에 전력 회사로부터 에너지 환급금을 받고 있습니다. 이러한 조합을 통해 기존 자산의 활용도가 향상되어, 상품 가격 변동에 직면해 자금 조달에 어려움을 겪는 가공업체에게 이점이 됩니다. 시장 조사에 따르면, 북미에서 설치 후 15년 이상 경과한 압축기의 30%가 향후 3년 이내에 제어 시스템 업그레이드 대상이 될 것으로 예상되며, 이는 애프터마켓의 성장 여지가 상당히 크다는 것을 시사합니다. 하드웨어 공급업체들은 사이버 보안 규정 준수를 보장하기 위해 IT 플랫폼 업체들과 협력하며, 이전에 도입을 주저하게 만들었던 랜섬웨어에 대한 구매자들의 우려를 해소하고 있습니다. 전반적으로, 사용자들이 데이터 기반의 효율성을 우선시함에 따라 제어 및 자동화 분야는 산업용 냉동 시스템 시장 전체의 성장률을 계속해서 상회할 것으로 보입니다.

암모니아는 GWP가 0이라는 특성과 대규모 플랜트에서의 뛰어난 열역학적 성능을 바탕으로, 2025년 설치 건수의 42.41%를 차지했습니다. 그럼에도 불구하고, 초임계 이산화탄소(CO2) 설계 시장은 2031년까지 연평균 성장률(CAGR) 4.51%로 성장할 전망입니다. 유럽이 기준을 마련하고 슈퍼마켓과 물류 허브에 수천 대의 저탄소 CO2 랙을 도입하고 있는 가운데, 2028년 규제 준수 기한을 앞두고 이러한 도입이 현재 북미의 물류 센터로도 확대되고 있습니다. 수소불화탄소(HFC)는 초저온이 필요한 분야나 개조 예산이 제한적인 분야에서 여전히 사용되고 있지만, 법적 규제의 장벽으로 인해 새로운 HFC 프로젝트는 극히 제한적입니다. 탄화수소, 주로 프로판은 가연성 위험을 관리할 수 있는 50kW 미만의 소규모 시스템에서 틈새 시장을 확보하고 있습니다. 기기 제조업체들은 듀얼 냉매 플랫폼을 제공함으로써 위험을 분산시키고 있으며, 이를 통해 최종 사용자는 지역 규제가 변화함에 따라 냉매를 전환할 수 있게 됩니다.

이산화탄소(CO2) 관련 산업용 냉동 시스템 시장 규모는 패키징의 표준화를 배경으로 확대되고 있습니다. 이 공급업체는 가스 쿨러와 열회수 모듈이 완비된 사전 설계된 랙을 공급함으로써, 현장별 맞춤형 설계 작업을 생략하고 시운전을 신속하게 진행할 수 있도록 합니다. 사례 연구에 따르면, 수산 가공 공장에서 R-507A에서 CO₂ 부스터 랙으로 전환한 후 총 에너지 소비량이 35% 감소한 것으로 기록되어 있으며, 이러한 성과는 CO₂의 가치를 입증하는 근거가 되고 있습니다. 온난한 기후 조건에서는 병렬 압축과 단열식 가스 쿨러가 CO₂ 효율 저하를 완화하여 가동 가능 범위를 넓혀줍니다. 보험사들은 고객과 직접 접촉하는 소매 공간에서 암모니아보다 이산화탄소(CO2)에 대한 보상에 더 적극적인 태도를 보이고 있으며, 이러한 요인이 슈퍼마켓의 사양 목록을 트랜스크리티컬 설계 쪽으로 기울게 하고 있습니다. 이러한 추세에 따라, 보다 광범위한 산업용 냉동 시스템 시장에서 이산화탄소의 적용 범위가 확실히 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년 산업용 냉동 시스템 시장 매출의 41.22%를 차지했으며, 이는 콜드체인 구축 및 유제품 가공 시설 현대화를 위한 정부의 보조금 지원 덕분입니다. 중국이 시행하는 500억 위안 규모의 농촌 콜드체인 계획은 내륙 지방의 성에서 암모니아 저장고 건설을 촉진하고 있습니다. 인도의 협동조합 계열 유제품 제조업체는 2시간 이내에 4℃ 미만으로 냉각해야 하는 냉장 우유의 생산 능력을 확대했으나, 이러한 사양은 고효율 스크류 압축기를 통해서만 달성할 수 있습니다. 일본은 2025년 HCFC 사용 금지에 앞서 R-22 시스템의 개조에 주력하고 있는 반면, 호주 및 뉴질랜드에서는 신규 점포에서 HFC를 완전히 배제하기 위해 초임계 CO₂ 방식을 활용한 슈퍼마켓 개조 작업이 진행되고 있습니다. 동남아시아의 수산물 수출업체들은 급속 냉동 라인을 확충하고 있으며, 2024년 베트남과 태국으로의 압축기 출하량은 18% 증가했습니다. 이러한 프로젝트들이 맞물려, 인구 증가에 따른 식량 수요 증가세와 맞먹는 속도로 해당 지역의 산업용 냉동 시스템 시장 규모가 확대되고 있습니다.

중동 및 아프리카는 5.23%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 식량 안보 문제가 항만과 내륙 허브를 연결하는 냉장 물류 회랑의 구축을 촉진하고 있습니다. 두바이는 제벨 알리 인근에 10곳의 신규 창고 건설에 5억 달러를 투자할 예정이며, 각 창고에는 주변 온도 45℃의 환경에 적합한 CO2 냉각기가 도입될 예정입니다. DP 월드는 EU의 우수 유통 기준(GDP)에 부합하는 의약품 수입을 지원하기 위해 이집트에 2,900만 달러를 투자해 시설을 개설함으로써, 지역 물류 서비스에 대한 신뢰도를 높이고 있습니다. 사우디아라비아의 NEOM 구역은 수직 농업 계획을 지원하기 위해 암모니아 콜드체인에 투자하고 있으며, 한편 마스크와 현지 파트너는 리야드에 10만 제곱미터 규모의 냉장 시설을 건설 중입니다. 2025년 1월부터 시행되는 누출 보고 의무는 자연 냉매의 도입을 가속화하고 제어 시스템의 업그레이드를 촉진하며, 걸프 연안 전역의 산업용 냉동 시스템 시장의 성장세를 더욱 강화하고 있습니다.

북미와 유럽은 여전히 기술 동향을 주도하고 있으며, 규제가 업데이트 주기를 촉진하고 있습니다. 미국의 '기술 전환 규정(Technology Transitions Rule)'은 낙농업이 발달한 주에서 HFC에서 암모니아로 전환하는 것을 장려하고 있으며, 유틸리티 사업자의 리베이트 제도가 가변속 드라이브의 투자 회수를 유리하게 만들고 있습니다. 유럽의 개정된 F-가스 계획에 따라, 냉장 창고 소유주의 62%가 2027년까지 개보수 예산을 편성하고 있습니다. 성장률은 신흥 지역에 뒤처지고 있지만, 높은 단가 덕분에 이들 대륙은 여전히 중요한 수익원이 되고 있습니다. 남미에서는 브라질의 육류 수출에서 차지하는 지배적인 지위에 힘입어 수요가 견조한 흐름을 보이고 있습니다. JBS사는 85곳의 암모니아 공장을 운영하고 있으며, 건설 중인 시설도 있습니다. 아프리카는 여전히 규모가 작지만, 남아프리카의 와인 산업 체인과 케냐의 원예 산업에서 나타나는 틈새 냉장 물류 시장이 향후 성장 가능성을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the industrial refrigeration system market size was valued at USD 25.40 billion in 2025 and is estimated to grow from USD 26.49 billion in 2026 to reach USD 32.41 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

This report is Segmented by Equipment (Compressors, Condensers, Evaporators, and More), Refrigerant (Ammonia, Carbon Dioxide, and More), Application (Food and Beverage Processing, Cold-Storage and Logistics, and More), System Capacity (Less Than 100 KW, and More), System Type (Single-Stage, Two-Stage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Refrigeration System Market Trends and Insights

Surge in Automated Cold-Chain Warehouses

Automated cold warehouses concentrate throughput in fewer, high-capacity hubs that operate around the clock at sub-zero temperatures, driving demand for ammonia systems sized above 2 megawatts. Investment announcements from major operators confirm the trend, with large frozen-food sites requiring tighter +-0.5 °C control that favours multi-stage compression and cascade architectures. Asian grocery e-commerce growth further accelerates retrofits, prompting logistics providers to add variable-speed screw compressors and IoT-ready evaporator fans. Manufacturers of automated storage and retrieval cranes also set stricter thermal tolerances, aligning mechanical handling with refrigeration controls to prevent condensation on robotics. As a result, the industrial refrigeration system market sees higher average project values and longer-term service contracts, lifting aftermarket revenue streams.

Tightening F-Gas and Kigali Compliance Deadlines

Regulatory phase-down schedules shorten the viable window for new HFC equipment, prompting a surge in natural-refrigerant conversions. The European Union now mandates a 95% cut in HFC use by 2030, while the United States bars HFCs from new industrial process refrigeration from January 2025. Documentation rules on leak tracking add administrative cost, favouring factory-packaged ammonia and CO2 racks that arrive pre-charged and hermetically tested. Financial penalties compound non-compliance risk, as Japan's carbon price of JPY 3,000 per ton of CO2-equivalent raises the direct cost of HFC leaks. This policy mix accelerates a replacement cycle that sustains industrial refrigeration system market growth even as total installed capacity stabilizes in mature economies.

High Capex and Skilled-Labor Scarcity for Natural Refrigerants

Natural-refrigerant plants cost 20%-40% more than HFC equivalents because of stainless-steel heat exchangers, enhanced ventilation, and redundant safety interlocks. Budget pressures are compounded by a shrinking pool of certified ammonia technicians, especially in North America where retirements outpace training enrolment. Certification bodies require two years of supervised field experience, delaying workforce replenishment and extending project schedules. Labor premiums reach USD 150 per hour in major U.S. metro areas, a surcharge that elongates payback periods and slows industrial refrigeration system market adoption in smaller enterprises. Equipment vendors respond with factory-built, skid-mounted modules that reduce on-site work, but labour scarcity will remain a near-term drag on project velocity.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Ultra-Low-Charge NH3 and CO2 Systems

- AI-Enabled Predictive Maintenance Lowering Lifecycle Cost

- Volatile Steel and Copper Prices Inflating Equipment Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Controls already represent the fastest-growing slice of the industrial refrigeration system market. Compressors retained a 36.18% revenue share in 2025, underscoring their central function, yet programmable logic controllers, variable-frequency drives, and cloud dashboards are climbing at a 4.93% CAGR to 2031. This expansion mirrors mandates such as California's Title 24 update that requires demand-response integration in systems capacity above 100 kilowatts. Advanced drives trim compressor energy by up to 50%, allowing site owners to recover investment within 18 months, and the energy savings improve the overall industrial refrigeration system market size by unlocking deferred projects. Condensers and evaporators trail the market average as their design advances focus on incremental heat-transfer gains rather than radical efficiency jumps. Receivers and heat exchangers gain traction because cascade and transcritical designs need intermediate heat exchange, adding bill-of-materials value per installation. Controls vendors also bundle analytics subscriptions, producing annuity revenue that stabilizes earnings across macro cycles.

Digital retrofits increasingly target brownfield plants. Operators in mature economies pair existing compressors with new drives and sensor kits, leveraging sunk hardware cost while capturing energy rebates from utilities. The pairing boosts legacy asset utilization, a benefit for cash-constrained processors navigating commodity price swings. Market surveys show 30% of installed compressors above 15 years old in North America are now candidates for control upgrades within three years, suggesting a sizable aftermarket runway. Hardware suppliers form alliances with IT platforms to ensure cybersecurity compliance, addressing buyer concerns over ransomware that previously stalled adoption. In aggregate, controls and automation will continue to outpace aggregate industrial refrigeration system market growth as users prioritize data-driven efficiency.

Ammonia held 42.41% of 2025 installations, buoyed by zero-GWP credentials and superior thermodynamic performance in large plants. Nevertheless, transcritical carbon dioxide designs are advancing at a 4.51% CAGR through 2031. Europe sets the standard, deploying thousands of low-charge CO2 racks in supermarkets and distribution hubs, yet uptake now spreads to North American distribution centers ahead of 2028 compliance deadlines. Hydrofluorocarbons linger in pockets that demand ultra-low temperatures or have limited retrofit budgets, but legislative barriers render new HFC projects marginal. Hydrocarbons, chiefly propane, capture niche demand in small systems capacity below 50 kilowatts where flammability risk is manageable. Equipment makers hedge bets by offering dual-refrigerant platforms, allowing end-users to switch refrigerants as local codes evolve.

The industrial refrigeration system market size attached to carbon dioxide expands on the back of packaging standardization. Vendors supply pre-engineered racks complete with gas coolers and heat reclaim modules, removing site-specific engineering and accelerating commissioning. Case studies record 35% total energy savings in seafood processing plants after switching from R-507A to CO2 booster racks, an outcome that bolsters the value narrative. In warmer climates, parallel compression and adiabatic gas coolers mitigate CO2 efficiency penalties, broadening feasible operating zones. Insurance carriers are more comfortable covering CO2 than ammonia in customer-facing retail spaces, a factor that tips supermarket specification lists toward transcritical designs. These dynamics ensure a widening footprint for carbon dioxide within the broader industrial refrigeration system market.

Geography Analysis

Asia Pacific accounted for 41.22% of 2025 revenue in the industrial refrigeration system market, reflecting government subsidies for cold-chain buildouts and dairy-processing upgrades. China's CNY 50 billion rural cold-chain scheme spurs ammonia warehouse construction in interior provinces. India's cooperative dairies added chilled-milk capacity requiring sub-4 °C cooling within two hours, a spec achievable only with high-efficiency screw compressors. Japan focuses on retrofitting R-22 systems ahead of its 2025 HCFC ban, while Australia and New Zealand roll out transcritical CO2 supermarket upgrades to fully remove HFCs from new stores. Southeast Asian seafood exporters boost blast-freezing lines, and compressor shipments to Vietnam and Thailand rose 18% in 2024. These projects combine to expand the regional industrial refrigeration system market size at a pace that matches population-driven food demand.

The Middle East and Africa have the highest forecast CAGR at 5.23%. Food security agendas fuel cold-storage corridors linking ports to inland hubs. Dubai earmarked USD 500 million for ten new warehouses near Jebel Ali, each designed with CO2 chillers suitable for 45 °C ambient conditions. DP World opened a USD 29 million facility in Egypt to serve pharmaceutical imports under EU Good Distribution Practice, adding credibility to regional logistics offerings. Saudi Arabia's NEOM zone invests in ammonia cold chain to back vertical farming schemes, while Maersk and local partners build a 100,000-square-meter refrigerated site in Riyadh. Leak-reporting mandates starting January 2025 accelerate natural-refrigerant adoption and pull in controls upgrades, reinforcing industrial refrigeration system market momentum across the Gulf.

North America and Europe remain technology trendsetters, with regulations sparking replacement cycles. The United States Technology Transitions Rule propels HFC-to-ammonia retrofits in dairy states, and utility rebates sweeten the payback for variable-speed drives. Europe's revised F-Gas plan has 62% of cold-store owners budgeting retrofits by 2027. While growth rates trail emerging regions, high unit values keep these continents significant revenue contributors. South America shows steady demand anchored in Brazil's meat-export dominance, and JBS runs 85 ammonia plants with more in build stage. Africa remains modest yet pockets in South Africa's wine chain and Kenya's floriculture add niche refrigerated logistics, pointing to future upside.

- Johnson Controls International plc

- Emerson Electric Co.

- GEA Group AG

- Danfoss A/S

- Mayekawa Mfg. Co., Ltd.

- Ingersoll Rand plc

- Carrier Global Corp.

- Daikin Industries Ltd.

- BITZER Kuhlmaschinenbau GmbH

- Star Refrigeration Ltd.

- Dover Corporation

- LU-VE Group

- Guntner GmbH and Co. KG

- EVAPCO, Inc.

- Alfa Laval AB

- Mitsubishi Heavy Industries Thermal Systems

- Baltimore Aircoil Company

- Industrial Frigo S.r.l.

- Tecumseh Products Company

- Kirloskar Pneumatic Co. Ltd.

- SANDEN Holdings Corp.

- Bock GmbH

- Howden Group

- Frascold S.p.A.

- Carnot Refrigeration

- Hillphoenix, Inc.

- Trane Technologies plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Automated Cold-Chain Warehouses

- 4.2.2 Tightening F-Gas and Kigali Compliance Deadlines

- 4.2.3 Rapid Adoption of Ultra-Low-Charge NH3 and CO2 Systems

- 4.2.4 AI-Enabled Predictive Maintenance Lowering Lifecycle Cost

- 4.2.5 Green-Hydrogen Plants Requiring Large-Scale Chilling

- 4.2.6 Demand from Immersion-Cooled Data Centres for Heat-Reuse Chillers

- 4.3 Market Restraints

- 4.3.1 High Capex and Skilled-Labour Scarcity for Natural Refrigerants

- 4.3.2 Volatile Steel and Copper Prices Inflating Equipment Costs

- 4.3.3 Cyber-Insurance Premiums for IoT-Linked Refrigeration Systems

- 4.3.4 Rare-Earth Magnet Supply Risk for VSD Compressors

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Equipment

- 5.1.1 Compressors

- 5.1.2 Condensers

- 5.1.3 Evaporators

- 5.1.4 Heat-Exchangers and Receivers

- 5.1.5 Controls and Automation

- 5.1.6 Others, Equipment

- 5.2 By Refrigerant

- 5.2.1 Ammonia (R-717)

- 5.2.2 Carbon Dioxide (R-744)

- 5.2.3 Hydro-Fluorocarbons (HFC/HFO)

- 5.2.4 Hydro-Carbons (Propane, Isobutane)

- 5.3 By Application

- 5.3.1 Food and Beverage Processing

- 5.3.2 Cold-Storage and Logistics

- 5.3.3 Chemicals and Pharmaceuticals

- 5.3.4 Oil and Gas / LNG

- 5.3.5 Data Centres and Electronics

- 5.4 By System Capacity

- 5.4.1 Less Than 100 kW (Small)

- 5.4.2 100 - 1,000 kW (Medium)

- 5.4.3 Greater Than 1 MW (Large)

- 5.5 By System Type

- 5.5.1 Single-Stage Compression

- 5.5.2 Two-Stage Compression

- 5.5.3 Cascade & Transcritical

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Johnson Controls International plc

- 6.4.2 Emerson Electric Co.

- 6.4.3 GEA Group AG

- 6.4.4 Danfoss A/S

- 6.4.5 Mayekawa Mfg. Co., Ltd.

- 6.4.6 Ingersoll Rand plc

- 6.4.7 Carrier Global Corp.

- 6.4.8 Daikin Industries Ltd.

- 6.4.9 BITZER Kuhlmaschinenbau GmbH

- 6.4.10 Star Refrigeration Ltd.

- 6.4.11 Dover Corporation

- 6.4.12 LU-VE Group

- 6.4.13 Guntner GmbH and Co. KG

- 6.4.14 EVAPCO, Inc.

- 6.4.15 Alfa Laval AB

- 6.4.16 Mitsubishi Heavy Industries Thermal Systems

- 6.4.17 Baltimore Aircoil Company

- 6.4.18 Industrial Frigo S.r.l.

- 6.4.19 Tecumseh Products Company

- 6.4.20 Kirloskar Pneumatic Co. Ltd.

- 6.4.21 SANDEN Holdings Corp.

- 6.4.22 Bock GmbH

- 6.4.23 Howden Group

- 6.4.24 Frascold S.p.A.

- 6.4.25 Carnot Refrigeration

- 6.4.26 Hillphoenix, Inc.

- 6.4.27 Trane Technologies plc

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment