|

시장보고서

상품코드

2061661

오디오 앰프 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Audio Amplifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

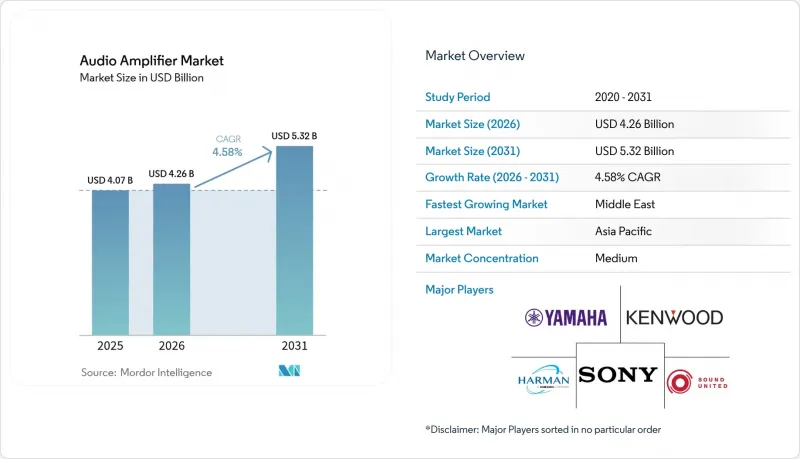

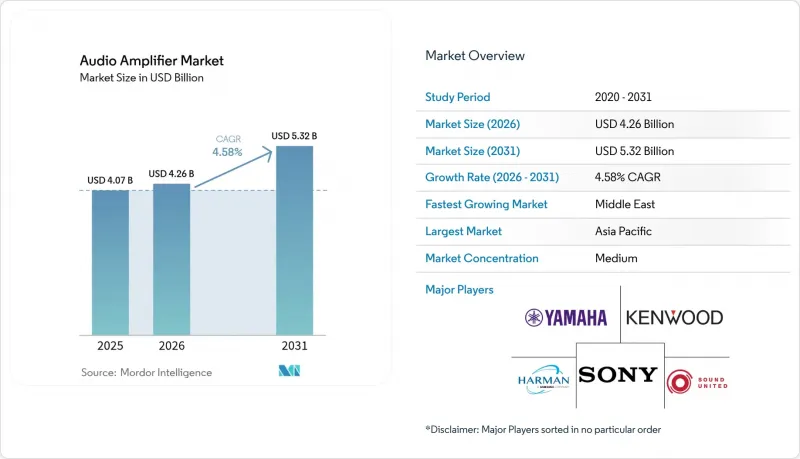

Mordor Intelligence에 의하면, 오디오 앰프 시장 규모는 2025년에 40억 7,000만 달러로 평가되었습니다. 2026년 42억 6,000만 달러에서 2031년까지 53억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.58%를 나타낼 전망입니다.

본 보고서는 채널 구성(2채널, 4채널, 6채널, 기타), 디바이스 통합/폼 팩터(독립형 오디오 앰프 IC, 기타), 반도체 소재(실리콘, 질화갈륨(GaN), 실리콘카바이드(SiC), 기타), 최종 사용자용도(소비자 가전, 자동차, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 오디오 앰프 시장 동향과 인사이트

전기차 및 커넥티드카로의 전환이 차량용 인포테인먼트 오디오 앰프 시장을 견인하고 있습니다.

전기 구동 시스템으로 인해 엔진 소리가 사라짐에 따라, 자동차 제조업체들은 멀티채널 Class-D 앰프와 구역별 사운드 관리를 통해 차량 내 오디오 경험을 향상시키려 하고 있습니다. BMW의 HypersonX 사운드스케이프는 43가지의 서로 다른 신호를 활용해, 자사의 Neue Klasse EV 라인을 위한 브랜드 고유의 사운드 시그니처를 창출하고 있습니다. HARMAN의 SeatSonic 솔루션은 각 좌석 구역 전용 앰프를 활용하여 승객별로 오디오를 더욱 개인화합니다. 소프트웨어 정의 차량이 보급됨에 따라 앰프의 펌웨어 업그레이드를 통해 제품 수명이 연장되고 있으며, 텍사스 기기의 1인덕터 변조 기술은 부품 수를 줄여 자동차 제조업체의 비용 절감 목표를 달성하고 있습니다.

TWS 및 웨어러블 기기에서 소형화에 대한 수요가 고효율 집적 증폭기 시장을 견인하고 있습니다.

완전 무선 스테레오 이어폰과 스마트 워치는 기판 공간과 배터리 사용 시간에 엄격한 제약이 따르기 때문에 제조업체들은 DSP, 연결 기능, 증폭 기능을 통합한 SoC로 전환하고 있습니다. 아날로그 디바이스의 ADAU1797은 DSP 성능을 2배로 높이는 동시에 클래스 D 단계를 통합하여 배터리 구동 시간을 연장했습니다. 마찬가지로, 노르딕 세미컨덕터의 nRF54L15는 22nm 공정 노드 위에 1.5MB의 NVM, 256KB의 RAM 및 LE Audio 지원을 통합하여 시스템 통합의 부담을 줄여줍니다. 실리콘 인터벤션의 프랙탈 클래스 D 토폴로지는 강압 레귤레이션과 출력 단계를 결합하여 대기 상태에서의 손실을 줄여주며, 이는 하루 종일 착용하는 웨어러블 기기에 있어 매우 중요한 지표가 됩니다.

스마트폰 SoC로의 통합으로 인해, 디스크리트 앰프의 잠재 시장이 축소되고 있습니다.

애플리케이션 프로세서에 클래스 D 출력 기능이 내장됨에 따라, 중급형 스마트폰 시장에서 독립형 IC에 대한 수요가 감소하고 있습니다. Qorvo의 2025년 3분기 매출은 12.4% 감소했습니다. 이는 안드로이드 OEM 업체들이 RF 및 오디오 프런트엔드를 단일 칩 제품으로 통합했기 때문입니다. 태블릿이나 초슬림 경량 PC에서 이와 유사한 설계 선택이 이루어짐에 따라, 개별 부품 공급업체들은 압박을 받고 있으며, 열 및 출력 전력 제약으로 인해 SoC로의 대체가 어려운 자동차, 스마트 홈 허브, 프로 오디오 랙과 같은 분야로 사업을 전환할 수밖에 없는 상황에 처해 있습니다.

부문별 분석

8채널 이상의 부문은 홈 시네마 및 차량 내 공간에서의 Dolby Atmos 도입을 견인하는 역할을 하며, 2031년까지 연평균 5.71%의 성장률을 보일 것으로 전망됩니다. 전용 하이 및 서라운드 경로를 통해 섀시당 앰프 수가 증가하는 한편, DSP 펌웨어 내의 동적 채널 매핑이 스테레오 컨텐츠와의 하위 호환성을 지원합니다. 대조적으로, 가격을 중시하는 사운드바와 데스크톱 스피커는 2025년 오디오 앰프 시장 점유율의 41.65%를 차지한 2채널 시장의 입지를 유지하고 있습니다.

스마트 홈 허브가 AV, 조명, 보안 제어를 통합하고, 중앙 집중형 앰프 노드가 선호됨에 따라 멀티채널 오디오 앰프 시장 규모는 확대될 것으로 예측됩니다. 전문 투어 장비 공급업체들은 모노 서브우퍼 용도부터 몰입형 페스티벌용 장비 구성까지 가능한 모듈식 랙 앰프를 도입하여, 다양한 규모의 이벤트에 걸쳐 자산 활용을 최적화하고 있습니다. 이러한 아키텍처의 유연성은 클래스 D 토폴로지에 유리하게 작용하며, 채널 밀도가 높아질수록 그 효율성의 이점은 더욱 커집니다.

자동차 및 프로 오디오 설치 환경에서는 더 높은 전압 레일과 더 큰 열적 여유도가 요구되기 때문에 2025년 매출의 54.75%는 독립형 IC가 차지했습니다. 그러나 웨어러블 기기나 초슬림 노트북의 경우 기판 공간과 단일 패키지 내 부품 구성이 중요시되기 때문에 SoC 시장은 연평균 성장률(CAGR) 5.99%로 성장하고 있습니다. 각 벤더사는 첨단 공정 노드를 활용하여 DSP 코어, Bluetooth LE 무선, 클래스 D 출력을 단일 패키지에 집적함으로써 I/O 배선으로 인한 손실을 최소화하고 있습니다.

SoC에 의한 오디오 앰프 시장의 확대는 TWS 이어폰 분야에서 특히 두드러집니다. 여기서는 엔벨로프 트래킹 및 하이브리드 ANC 알고리즘이 온다이 메모리 대역폭의 이점을 누리고 있습니다. 반면, 기판 수준의 방열이나 교체 가능한 스테이지가 서비스 요건으로 요구되는 경우, 특히 콘서트용 렌탈 장비의 경우, 디스크리트 멀티칩 모듈이 여전히 유효합니다. 공급업체는 공유 실리콘 IP를 활용하는 한편, 기존 고객을 위해 핀 호환이 가능한 디스크리트 업그레이드 제품을 제공함으로써 두 포트폴리오 간의 균형을 맞추고 있습니다.

지역별 분석

아시아태평양은 수직 통합된 가전제품 공급망과 급증하는 국내 전기차 판매량을 배경으로, 2025년 매출의 47.85%를 차지했습니다. 중국 본토가 판매량의 기반을 이루고 있는 반면, 일본과 한국은 클래스 D 실리콘 및 GaN 웨이퍼 가공 분야에서 선도적인 혁신을 주도하고 있습니다. 지역 내 주요 스마트폰 제조업체들의 자체 SoC 로드맵은 지역 전체의 개별 부품 수요 변동에 막대한 영향을 미치고 있습니다.

북미는 프로 오디오 및 홈 시어터 분야에서 큰 비중을 차지하고 있으며, 팬데믹 이후 라이브 이벤트와 투어가 회복됨에 따라 랙 앰프의 업그레이드가 촉진되고 있습니다. 규제의 확실성과 강력한 특허 집행 덕분에, 전 세계 OEM 업체에 칩을 라이선싱하는 GaN 스타트업들이 성장하고 있습니다. 유럽 역시 비슷한 수준의 성숙도를 보이고 있지만, 에코디자인에 따른 전력 예산 상한선이 엄격하게 적용되고 있어, 규정 준수를 위한 노력의 일환으로 에너지 절약형 펌웨어가 시범 도입된 후 전 세계적으로 확대되는 경우가 많습니다.

중동은 절대 규모로는 작지만, 경기장, 호텔, 엔터테인먼트 지구에 몰입형 사운드 시스템을 도입하는 호스피탈리티 분야의 메가 프로젝트에 힘입어 2031년까지 연평균 성장률(CAGR) 5.03%를 나타낼 것으로 전망됩니다. 정부의 다각화 정책에 따라 공공 정보 서비스를 위한 분산형 오디오를 통합한 스마트 시티 건설에 자금이 지원되고 있으며, 이에 따라 상업용 AV 채널용 앰프 출하가 가속화되고 있습니다. 아프리카와 라틴아메리카에서는 주로 가격에 민감한 가전제품 수입이 주도하고, 휴대용 PA 시스템 수요를 뒷받침하는 지역의 라이브 음악 문화가 더해져, 꾸준한 한 자릿수 성장을 기록하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the audio amplifier market size was valued at USD 4.07 billion in 2025 and estimated to grow from USD 4.26 billion in 2026 to reach USD 5.32 billion by 2031, at a CAGR of 4.58% during the forecast period (2026-2031).

This report is Segmented by Channel Configuration (2-Channel, 4-Channel, 6-Channel, and More), Device Integration/Form Factor (Stand-Alone Audio-Amplifier IC, and More), Semiconductor Material (Silicon, Gallium Nitride (GaN), Silicon Carbide (SiC), and More), End-User Application (Consumer Electronics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Audio Amplifier Market Trends and Insights

Transition to Electric and Connected Vehicles Boosting In-Vehicle Infotainment Audio Amplifiers

Electric drivetrains eliminate engine noise, prompting automakers to enhance cabin audio experiences through multi-channel Class-D amplifiers and zone-specific sound management. BMW's HypersonX soundscape uses 43 distinct signals to craft a branded acoustic signature for its Neue Klasse EV line. HARMAN's SeatSonic solution further personalizes audio per passenger, harnessing dedicated amplifiers for each seating zone. As software-defined vehicles proliferate, amplifier firmware upgrades extend product lifecycles, and Texas Instruments' one-inductor modulation cuts component count to meet automakers' cost targets

Miniaturization Needs in TWS and Wearables Driving High-Efficiency Integrated Amplifiers

True wireless stereo earbuds and smartwatches impose severe board-space and battery-life constraints, steering vendors toward SoCs that merge DSP, connectivity, and amplification. Analog Devices' ADAU1797 doubled DSP horsepower while integrating a class-D stage to extend battery runtime. Nordic Semiconductor's nRF54L15 similarly packages 1.5 MB NVM, 256 KB RAM, and LE Audio support on a 22 nm node, easing system-integration overhead. Silicon Intervention's fractal class-D topology couples buck regulation with the output stage to trim idle losses, a critical metric for all-day wearable usage.

Smartphone SoC Integration Shrinking Discrete Amplifier Addressable Market

Application processors now embed class-D outputs, eroding unit demand for standalone ICs in mid-tier phones. Qorvo's Q3 2025 revenue slid 12.4% as Android OEMs consolidated RF and audio front-ends into single die offerings. Similar design choices in tablets and thin-and-light PCs squeeze discrete suppliers, compelling them to pivot toward automotive, smart-home hubs, and pro-audio racks where thermal and output-power constraints inhibit SoC replacement.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Home Audio Ecosystem Adoption Fueling Multi-Channel Amplifier Demand

- GaN-Based Switching Devices Enabling High-Power Professional-Audio Efficiency Gains

- GaN Substrate Supply Constraints Elevating BOM Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 8-channel-and-above segment is forecast to grow at 5.71% through 2031, driven by the rollout of Dolby Atmos in both home cinema and automotive cabins. Dedicated height and surround pathways raise amplifier counts per chassis, while dynamic channel mapping inside DSP firmware supports backward compatibility with stereo content. In contrast, cost-sensitive soundbars and desktop speakers sustain the 2-channel foothold that captured 41.65% audio amplifier market share in 2025.

The audio amplifier market size for multi-channel models is expected to expand as smart-home hubs integrate AV, lighting, and security control, favoring centralized amplifier nodes. Professional touring vendors deploy modular rack amps that are configurable from monaural subwoofer duty to immersive festival rigs, optimizing asset utilization across various event scales. These architectural flexibilities favor class-D topologies, whose efficiency advantages grow with channel density.

Stand-alone ICs still account for 54.75% of 2025 revenue, as automotive and pro-audio installations require higher voltage rails and greater thermal headroom. Yet SoCs are advancing at 5.99% CAGR as wearables and ultra-slim laptops prize PCB real estate and single-package bill of materials. Vendors utilize advanced process nodes to co-locate DSP cores, Bluetooth LE radios, and Class-D outputs, thereby minimizing I/O routing losses.

Audio amplifier market size gains from SoCs are evident in TWS earbuds, where envelope tracking and hybrid ANC algorithms benefit from on-die memory bandwidth. Conversely, discrete multichip modules remain viable where board-level heat spreading and replaceable stages are service requirements, notably in concert rental gear. Suppliers balance dual portfolios, leveraging shared silicon IP while offering pin-compatible discrete upgrades for legacy clients.

Geography Analysis

Asia Pacific commanded 47.85% of 2025 revenue on the strength of vertically integrated consumer-electronics supply chains and surging domestic EV deliveries. Mainland China anchors volume, while Japan and South Korea push premium innovation in class-D silicon and GaN wafer processing. Local smartphone champions' in-house SoC roadmaps heavily influence discrete-component demand swings throughout the region.

North America accounts for sizable professional-audio and home-theater consumption, with live-event touring recovering post-pandemic and driving rack-amplifier upgrades. Regulatory certainty and robust patent enforcement foster GaN start-ups that license dies to global OEMs. Europe displays similar maturity but imposes stringent Ecodesign power-budget ceilings; compliance efforts often pilot energy-saving firmware, which is later rolled out worldwide.

The Middle East, although smaller in absolute terms, is projected to post a 5.03% CAGR through 2031, underpinned by hospitality megaprojects that outfit stadiums, hotels, and entertainment districts with immersive sound systems. Government diversification agendas fund smart-city builds that integrate distributed audio for public information services, accelerating amplifier shipments in commercial AV channels. Africa and Latin America record steady single-digit growth, mostly driven by price-sensitive consumer electronics imports, supplemented by regional live-music cultures that sustain demand for portable PA systems.

- Yamaha Corporation

- Harman International (Crown, JBL, Mark Levinson)

- Sound United LLC (Marantz, Denon, Polk)

- Kenwood Corporation

- Sony Corporation

- Cambridge Audio (Audio Partnership PLC)

- Vervent Audio Group (Naim Audio, Focal)

- Bryston Ltd

- Allen and Heath Limited

- QSC LLC

- Bose Corporation

- DD Audio (Resonance Inc.)

- JL Audio

- Dynacord (Bosch Sicherheitssysteme GmbH)

- Luxman Corporation

- NAD Electronics International

- Peachtree Audio

- Pioneer Corporation (Onkyo)

- Rotel

- Mark Levinson Laboratories

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transition to Electric and Connected Vehicles Boosting In-Vehicle Infotainment Audio Amplifiers

- 4.2.2 Miniaturization Needs in TWS and Wearables Driving High-Efficiency Integrated Amplifiers

- 4.2.3 Smart-Home Audio Ecosystem Adoption Fueling Multi-Channel Amplifier Demand

- 4.2.4 GaN-Based Switching Devices Enabling High-Power Professional-Audio Efficiency Gains

- 4.2.5 Immersive Audio (Dolby Atmos) Uptake Pushing Above 8-Channel Amplifier Sales

- 4.2.6 Live-Events Infrastructure Incentives Accelerating Professional-Amplifier Purchases

- 4.3 Market Restraints

- 4.3.1 Smartphone SoC Integration Shrinking Discrete Amplifier Addressable Market

- 4.3.2 GaN Substrate Supply Constraints Elevating BOM Costs

- 4.3.3 Bluetooth Headphones Cannibalizing Traditional Hi-Fi Amplifier Demand

- 4.3.4 EU Ecodesign Stand-by-Power Limits Raising Legacy Redesign Costs

- 4.4 industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Channel Configuration

- 5.1.1 Mono

- 5.1.2 2-Channel

- 5.1.3 4-Channel

- 5.1.4 6-Channel

- 5.1.5 8-Channel and Above

- 5.2 By Device Integration/Form Factor

- 5.2.1 Stand-Alone Audio-Amplifier IC

- 5.2.2 Integrated Audio SoC/Codec

- 5.2.3 Amplifier Modules and Boards

- 5.3 By Semiconductor Material

- 5.3.1 Silicon

- 5.3.2 Gallium Nitride (GaN)

- 5.3.3 Silicon Carbide (SiC)

- 5.3.4 Others (GaAs, etc.)

- 5.4 By End-User Application

- 5.4.1 Consumer Electronics

- 5.4.1.1 Smartphones and Tablets

- 5.4.1.2 Laptops and PCs

- 5.4.1.3 Smart TVs and Set-Top Boxes

- 5.4.1.4 Wearables and Hearables

- 5.4.1.5 Portable Speakers and Home Audio

- 5.4.2 Automotive

- 5.4.2.1 Passenger Vehicles

- 5.4.2.2 Commercial Vehicles

- 5.4.2.3 Electric Vehicles

- 5.4.3 Professional Audio and Broadcasting

- 5.4.3.1 PA Systems and Touring Sound

- 5.4.3.2 Studio and Recording Equipment

- 5.4.3.3 Broadcasting Equipment

- 5.4.4 Telecommunications Infrastructure

- 5.4.5 Industrial and IoT Devices

- 5.4.6 Others

- 5.4.1 Consumer Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Yamaha Corporation

- 6.4.2 Harman International (Crown, JBL, Mark Levinson)

- 6.4.3 Sound United LLC (Marantz, Denon, Polk)

- 6.4.4 Kenwood Corporation

- 6.4.5 Sony Corporation

- 6.4.6 Cambridge Audio (Audio Partnership PLC)

- 6.4.7 Vervent Audio Group (Naim Audio, Focal)

- 6.4.8 Bryston Ltd

- 6.4.9 Allen and Heath Limited

- 6.4.10 QSC LLC

- 6.4.11 Bose Corporation

- 6.4.12 DD Audio (Resonance Inc.)

- 6.4.13 JL Audio

- 6.4.14 Dynacord (Bosch Sicherheitssysteme GmbH)

- 6.4.15 Luxman Corporation

- 6.4.16 NAD Electronics International

- 6.4.17 Peachtree Audio

- 6.4.18 Pioneer Corporation (Onkyo)

- 6.4.19 Rotel

- 6.4.20 Mark Levinson Laboratories

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment