|

시장보고서

상품코드

2061664

과황산염 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Persulfates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

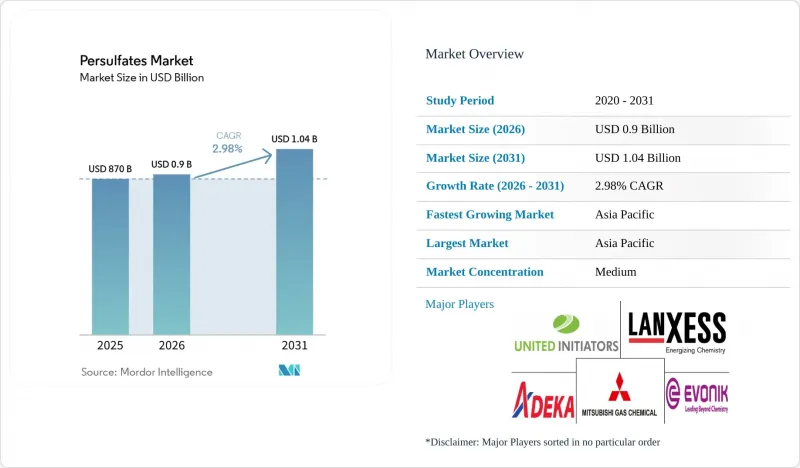

Mordor Intelligence에 의하면, 2026년 과황산염 시장 규모는 8억 9,590만 달러에 달할 것으로 추정됩니다. 2025년 8억 7,000만 달러에서 성장하여 2031년에는 10억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 2.98%를 나타낼 것으로 전망됩니다.

본 보고서는 유형(과황산나트륨, 과황산칼륨, 과황산암모늄), 용도(폴리머 개시제, 석유 증진 회수(EOR) 등), 최종 사용자 산업(폴리머, 펄프 및 종이 및 섬유 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 과황산염 시장 동향 및 분석

첨단 노드 반도체 팹에서 고성능 PCB 세정제에 대한 수요 증가

5nm 이하의 로직 및 3D 메모리 노드에서는 트렌치를 손상시키지 않으면서 나노 규모의 폴리머 잔류물을 제거할 수 있는 초고순도 과황산염 용액이 필요합니다. 대만 및 한국의 팹 운영사는 수율 목표를 달성하기 위해 금속 이온 농도가 0.1 ppm 미만인 과황산나트륨 등급을 지정하고 있습니다. 2024년 전 세계 PCB 생산량이 6.3% 회복되면서 과황산염 공급업체들의 수주 전망이 개선된 반면, 미국, 일본, 유럽의 국가 차원 AI 및 반도체 주권 프로그램으로 인해 수요는 지역화되는 추세입니다. 현재, 단일 웨이퍼용 습식 벤치에 대한 투자에는 과황산염 공급 시스템이 포함되어 있으며, 이 화학 약품이 자본 설비 계약에 포함됨으로써 경기 변동의 영향을 완화하고 있습니다. 파브가 ‘제로 리퀴드 디차지(ZLD)’ 목표 달성을 추진하는 가운데, 분석 지원 및 폐쇄형 순환 재활용 서비스를 제공하는 공급업체들은 보다 안정적인 수익원을 확보하고 있습니다.

수성 아크릴 수지에서의 과황산염계 폴리머 개시제 소비 확대

VOC(휘발성 유기 화합물)의 단계적 감축을 요구하는 환경 규제로 인해 수성 도료로의 전환이 가속화되고 있으며, 과황산염은 중성 pH 조건에서 분자량을 정밀하게 제어할 수 있습니다. 과황산암모늄은 콘크리트 혼화제나 건축용 도료에서 잔류 모노머를 감소시켜, 작업 안전과 실내 공기질을 개선합니다. 전 세계 아크릴산 생산 능력은 2025년 816만 톤에서 2030년에는 1,041만 톤으로 확대될 것으로 예상되며, 이는 막대한 발효제 수요를 뒷받침하고 있습니다. 중국과 태국에 위치한 아시아의 메가 플랜트에서는 실시간 산화환원 모니터링 기능을 갖춘 분산형 제어 시스템을 도입하고 있으며, 기존의 유기 과산화물 대신 과황산염의 사용이 점차 정착되고 있습니다. 유럽의 도료 제조업체들은 모노머 정제 보조제까지 공급하는 통합형 과황산염 제조업체를 우선적으로 선정하는 이중 조달 계약을 통해 공급 리스크를 헤지하고 있습니다.

주요 원료인 과산화수소공급망에서 발생하는 병목 현상

과산화수소는 과황산염 제조 비용의 최대 60%를 차지하며, 4개의 다국적 기업이 전 세계 생산 능력의 70% 이상을 장악하고 있습니다. 2024년 동아시아의 과산화수소 공장에서 발생한 가동 중단으로 인해 현물 가격이 22% 상승하면서 과황산염의 이익률이 압박을 받았습니다. 전해법을 이용한 과산화수소 프로젝트는 80%의 에너지 효율을 보장하지만, 수년에 걸친 설비 투자가 필요합니다. 반도체 등급 과산화수소의 부족은 고순도 과황산염공급에도 영향을 미쳐, 리드 타임을 4주에서 8주로 늘리고 있습니다. 배터리용 황산의 부족이 문제를 더욱 심각하게 만들고 있습니다. 변환기 제조업체들이 산화제 시장보다 음극 재료를 우선시하고 있어, 과황산염 제조업체들은 불가항력 조항을 발동할 수밖에 없는 상황입니다.

부문별 분석

과황산나트륨은 과황산염 시장 규모에서 가장 큰 점유율을 차지하고 있으며, 2025년에는 56.20%를 나타낼 것으로 전망됩니다. 이러한 비용 대비 성능은 대량 생산되는 PCB 에칭, 폴리머 개시제 및 산업용 세정 용도에 적합합니다. 과황산암모늄은 시장 규모는 작지만, 저pH 환경에서 분해가 용이한 헤어 블리치, EOR(증진유전회수), 에멀션 중합과 같은 틈새 시장 덕분에 2031년까지 연평균 성장률(CAGR) 3.65%를 기록하며 제품별 성장을 주도하고 있습니다. 과황산칼륨 수요는 식품 접촉용 필름이나 나트륨 혼입을 최소화해야 하는 전해질에 민감한 공정 등에 힘입어 틈새 시장에 국한되어 있습니다. 광미 저수지의 복원 및 리튬 배터리 재활용 라인의 증설은 과황산염 시장을 더욱 다각화시키고, 벌크 등급보다 높은 수익률을 실현하는 특수 블렌드를 추가하고 있습니다. 공급업체들은 프리미엄 가격을 정당화하고 상품화를 방지하기 위해 미량 금속 관리 및 입자 크기 최적화를 강조하고 있습니다.

지역별 분석

아시아태평양의 과황산염 시장의 우위는 견조한 반도체 팹, 증가하는 폴리머 생산 능력, 그리고 확대되는 섬유 표백 시장에 힘입고 있습니다. 중국 수요는 범용 등급부터 특수 등급에 이르기까지 다양하지만, 반덤핑 조사로 인해 수출 흐름이 바뀔 가능성이 있습니다. 대만과 한국의 팹에서는 5nm 이하 공정을 위해 초고순도 과황산염이 소비되고 있는 반면, 동남아시아 국가들은 공급망 다각화를 추진하기 위해 새로운 화학 허브를 육성하고 있습니다. 급속한 도시화로 인해 지역 수처리 분야에 대한 투자가 증가하고 있으며, 이것이 수요의 또 다른 축을 이루고 있습니다.

북미에서는 비전통 석유 및 가스의 강점을 살려, EOR(증진 채유) 시범 사업이 실험실 검증 단계에서 상업 지역으로 단계적으로 확대되고 있습니다. 반도체의 국내 생산 복귀와 더불어 주 정부의 인센티브가 전자 등급 과황산염에 대한 새로운 수요를 뒷받침하고 있으며, 아시아태평양 공급에 대한 기존 의존도를 낮추고 있습니다. 환경 규제로 인해 지하수 정화 및 산업 폐수 처리 분야에서 과황산염을 이용한 산화 공정이 꾸준히 확대되고 있으며, 거시경제 사이클의 영향을 받지 않는 기초적인 수요가 확보되고 있습니다.

유럽 시장의 성장은 완만하지만 꾸준하며, 엄격한 배출 기준과 순환형 경제의 추진으로 활기를 띠고 있습니다. 독일, 프랑스, 스웨덴의 배터리 재활용 공장에서는 EU의 핵심 원자재 정책에 따라 과황산염을 사용하여 리튬과 코발트를 용출하고 있습니다. 브라운필드 재개발 프로그램에서의 토양 정화는 예측 가능한 수요를 창출하고 있으며, 지역 화학 업계 내의 재편은 기술 감사, 현장 시범 작업, 폐쇄형 공급 계약을 제공할 수 있는 대규모 과황산염 제조업체에 유리하게 작용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, persulfates market size in 2026 is estimated at USD 895.9 million, growing from 2025 value of USD 870 million with 2031 projections showing USD 1.04 billion, growing at 2.98% CAGR over 2026-2031.

This report is Segmented by Type (Sodium Persulfate, Potassium Persulfate, and Ammonium Persulfate), Application (Polymer Initiator, Enhanced Oil Recovery, and More), End-User Industry (Polymer, Pulp Paper and Textile, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Persulfates Market Trends and Insights

Increasing Demand for High-Performance PCB Cleaning Agents in Advanced Node Semiconductor Fabs

Sub-5 nm logic and 3-D memory nodes require ultra-pure persulfate solutions that lift nanoscale polymer residues without trench damage. Fab operators in Taiwan and South Korea specify sodium persulfate grades with metal ions below 0.1 ppm to meet yield targets. A 6.3% rebound in global PCB output during 2024 improved order visibility for persulfate suppliers, while national AI and chip-sovereignty programs in the United States, Japan, and Europe are regionalizing demand. Investments in single-wafer wet benches now bundle persulfate feed systems, embedding the chemical in capital equipment contracts and dampening cyclical swings. Suppliers offering analytical support and closed-loop recycling services capture stickier revenue streams as fabs strive for zero-liquid-discharge goals.

Rising Consumption of Persulfate-Based Polymer Initiators in Water-Borne Acrylics

Environmental directives that phase down VOCs are accelerating the shift toward water-borne coatings, where persulfates deliver tight molecular-weight control at neutral pH. Ammonium persulfate enables low-residual monomer profiles in concrete admixtures and architectural paints, improving labor safety and indoor air quality. Global acrylic acid capacity is forecast to grow from 8.16 million tons in 2025 to 10.41 million tons in 2030, underpinning large-volume initiator needs. Asian mega-plants in China and Thailand are installing distributed control systems with real-time redox monitoring, cementing persulfate usage over legacy organic peroxides. Paint producers in Europe are hedging supply risk via dual-sourcing agreements that prefer integrated persulfate manufacturers who also supply monomer purification aids.

Supply-Chain Bottlenecks for Key Raw Material Hydrogen Peroxide

Hydrogen peroxide accounts for up to 60% of persulfate production cost, and four multinationals control more than 70% of global capacity. Outages in East Asian peroxide plants during 2024 lifted spot prices by 22%, squeezing persulfate margins. Electrolytic peroxide projects promise 80% energy efficiency yet require multi-year capital outlays. Semiconductor-grade peroxide shortages ripple through high-purity persulfate supply, hiking lead times from four weeks to eight. Battery-grade sulfuric acid scarcity compounds the problem, as converters prioritize cathode materials over oxidizer markets, forcing persulfate makers to implement force-majeure clauses.

Other drivers and restraints analyzed in the detailed report include:

- Strong Growth of Pulp, Paper and Textile Bleaching Operations in Developing Countries

- Demand Uptick from Enhanced Oil Recovery (EOR) Pilots in Shale Plays

- Safety and Handling Concerns Driving Stricter Warehousing Codes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sodium persulfate controlled the largest slice of the persulfates market size, equating to 56.20% in 2025. Its cost-to-performance ratio aligns with high-volume PCB etching, polymer initiation, and industrial cleaning duties. Ammonium persulfate, although holding a smaller base, leads type-level growth at a 3.65% CAGR through 2031 thanks to hair-bleach, EOR, and emulsion-polymer niches where low pH decomposition is beneficial. Demand for potassium persulfate stays niche, driven by food-contact films and electrolyte-sensitive processes requiring minimal sodium carryover. Rising tailings-pond remediation and lithium-battery recycling lines further diversify the persulfates market, adding specialty blends that achieve higher margins than bulk grades. Suppliers spotlight trace-metal control and tailored particle size to justify premiums and discourage commoditization.

Geography Analysis

Asia-Pacific's persulfates market dominance draws on robust semiconductor fabs, rising polymer capacity, and expanding textile bleaching. Chinese demand spans commodity and specialty grades, though anti-dumping reviews may redirect export flows. Taiwanese and South Korean fabs consume ultra-clean persulfate for sub-5 nm processes, while Southeast Asian nations cultivate new chemical hubs to capture supply-chain diversification. Rapid urbanization increases local water-treatment investment, adding another demand pillar.

North America leverages its unconventional oil and gas strength, with EOR pilots gradually scaling from laboratory validation to commercial zones. Semiconductor reshoring plus state incentives undergird new demand for electronic-grade persulfates, lessening historical reliance on Asia-Pacific supply. Environmental regulations steadily promote persulfate oxidation in groundwater remediation and industrial wastewater treatment, securing baseline offtake independent of macro cycles.

Europe's market growth is slower yet steadier, animated by strict discharge norms and the circular-economy agenda. Battery recycling plants in Germany, France, and Sweden apply persulfates to leach lithium and cobalt, aligning with EU critical-materials policy. Soil remediation in Brownfield redevelopment programs adds predictable volumes, and consolidation within the regional chemical industry favors large persulfate producers able to offer technical audits, on-site pilot work, and closed-loop supply agreements.

- Adeka Corporation

- Arkema

- Calibre Chemicals Pvt. Ltd.

- Evonik Industries AG

- Fujian ZhanHua Chemical Co., Ltd

- HEBEI JIHENG GROUP CO.,LTD.

- KANTO KAGAKU.

- LANXESS

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Powder Pack Chem

- San Yuan Chemical Co., Ltd.

- Shanghai Ansin Chemical Co. Ltd

- Stars Chemical (YongAn) Co., Ltd.

- United Initiators GmbH

- VR Persulfates Pvt Ltd

- Yatai Electrochemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for High-Performance PCB Cleaning Agents in Advanced Node Semiconductor Fabs

- 4.2.2 Rising Consumption of Persulfate-Based Polymer Initiators in Water-Borne Acrylics

- 4.2.3 Strong Growth of Pulp, Paper and Textile Bleaching Operations in Developing Countries

- 4.2.4 Demand Uptick from Enhanced Oil Recovery (EOR) Pilots in Shale Plays

- 4.2.5 Shift Toward On-Site Persulfate Generation Modules at Industrial Wastewater Plants

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Bottlenecks for Key Raw Material Hydrogen Peroxide

- 4.3.2 Safety and Handling Concerns Driving Stricter Warehousing Codes

- 4.3.3 Regulatory Scrutiny on Sulphate Discharge

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Sodium Persulfate

- 5.1.2 Potassium Persulfate

- 5.1.3 Ammonium Persulfate

- 5.2 By Application

- 5.2.1 Polymer Initiator

- 5.2.2 Enhanced Oil Recovery

- 5.2.3 Oxidation, Bleaching and Sizing Agent

- 5.2.4 Other Applications (Electronic etching, etc.)

- 5.3 By End-user Industry

- 5.3.1 Polymer

- 5.3.2 Pulp, Paper and Textile

- 5.3.3 Electronics

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Oil and Gas

- 5.3.6 Water Treatment

- 5.3.7 Soil Remediation

- 5.3.8 Other End-user Industries (Mining, Ashesives, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adeka Corporation

- 6.4.2 Arkema

- 6.4.3 Calibre Chemicals Pvt. Ltd.

- 6.4.4 Evonik Industries AG

- 6.4.5 Fujian ZhanHua Chemical Co., Ltd

- 6.4.6 HEBEI JIHENG GROUP CO.,LTD.

- 6.4.7 KANTO KAGAKU.

- 6.4.8 LANXESS

- 6.4.9 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.10 Powder Pack Chem

- 6.4.11 San Yuan Chemical Co., Ltd.

- 6.4.12 Shanghai Ansin Chemical Co. Ltd

- 6.4.13 Stars Chemical (YongAn) Co., Ltd.

- 6.4.14 United Initiators GmbH

- 6.4.15 VR Persulfates Pvt Ltd

- 6.4.16 Yatai Electrochemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing application in premium hair-bleaching formulations

- 7.3 Rising demand for persulfate-activated soil and groundwater remediation