|

시장보고서

상품코드

2061672

유럽의 전투기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Fighter Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

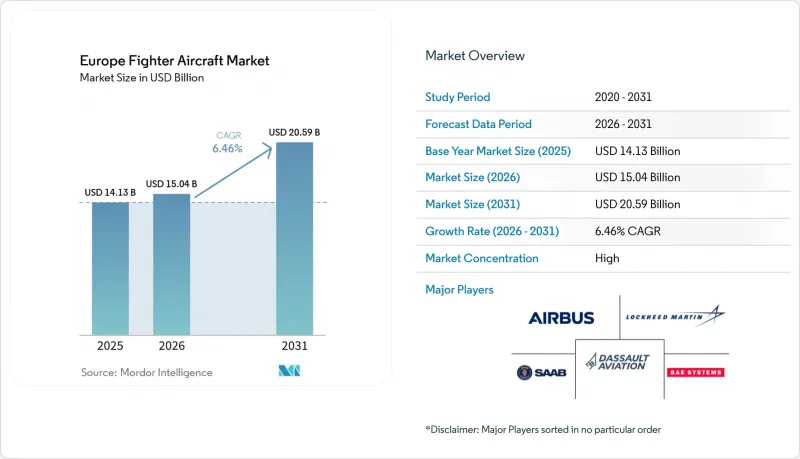

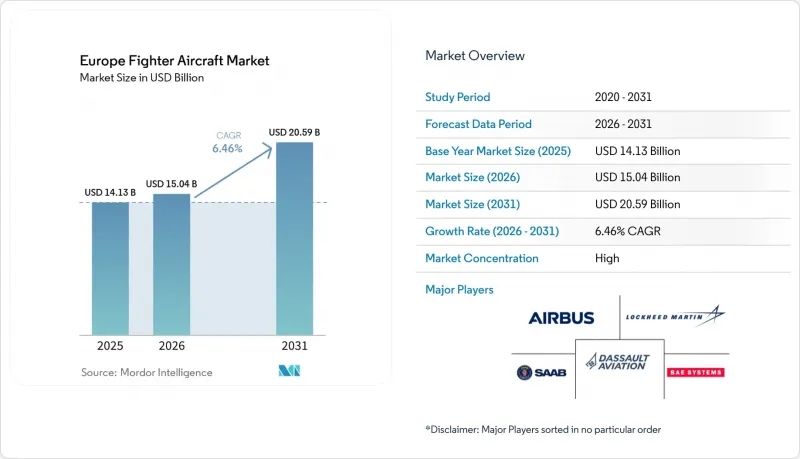

Mordor Intelligence에 의하면, 유럽의 전투기 시장 규모는 2025년에 141억 3,000만 달러로 평가되었습니다. 2026년 150억 4,000만 달러에서 2031년까지 205억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.46%를 나타낼 전망입니다.

본 보고서는 이착륙 방식(기존 이착륙 등), 전투기 세대(4세대, 4.5세대 등), 엔진 구성(단발 및 쌍발), 임무 역할(제공권 확보 등), 최종 사용자(공군 등), 그리고 지역(영국, 프랑스 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 전투기 시장 동향과 분석

우크라이나 사태 이후 유럽 방위 예산의 급증

EU의 SAFE 규정에 따라 공동 역량 확보 전용으로 1,500억 유로(1,758억 5,000만 달러) 규모의 대출 보증이 허용되면서, 냉전 이후 해당 지역에서 평시 기준으로 최대 규모의 지출 물결이 일고 있습니다. 독일이 GDP의 5%를 지원하겠다고 약속한 것만으로도, 유럽의 전투기 시장 전체에서 신규 제조 및 유지보수에 대한 달러화 표시 수요가 급증하고 있습니다. 각 회원국이 2029년까지 GDP의 1.5%에 해당하는 재정 규칙을 초과하는 지출을 허용하는 ‘이탈 조항(Escape Clause)’ 예산 메커니즘 덕분에 연속적인 발주를 위한 여지가 확대되고 있습니다. 나토(NATO)의 2024년 능력 재검토에서 공중 우세 능력의 격차가 중대한 문제라고 지적됨에 따라, 전투기가 최우선 조달 항목으로 선정되었습니다. 따라서 단기적인 지출로 인해 유럽의 전투기 시장은 적어도 2030년까지 이어질 조달 슈퍼사이클로 접어들고 있습니다.

가속화되는 5세대 F-35의 도입

핵 공유 임무를 목적으로 한 독일의 F-35A 35대 계약은 2030년까지 300억 유로(351억 6,000만 달러)를 초과하는 지역 전체 조달 계획을 주도하고 있습니다. 벨기에, 루마니아, 체코 공화국도 이에 발맞추어 개발 위험보다는 NATO와의 상호 운용성을 중시하며 기체 교체를 추진하고 있습니다. 미국의 ITAR(국제무기거래규정) 제재가 주권 문제에 대한 우려를 불러일으키고 있는 반면, 소규모 군들은 단기적으로 5세대 전투기의 작전 능력을 확보하기 위해 이러한 의존을 수용하고 있습니다. 그 결과 발생하는 발주량은 단발기 수요를 끌어올리고, 향후 6세대기의 비용 대비 효과에 관한 논의에 영향을 미치는 ‘비행 시간당 비용’이라는 기준을 강화시키고 있습니다.

급등하는 조달 비용과 수명 주기 비용

F-35A의 단가는 8,000만 달러를 넘으며, 반면 개량형 유로파이터는 개발비 상각을 포함하면 1억 2,000만 달러에 육박합니다. 유지비는 일반적으로 총 소유 비용의 60-70%를 차지하며, 각국 정부는 수십 년에 걸친 자금 조달에 얽매이게 되어 다른 국방 예산을 압박하게 됩니다. 유럽방위청(EDA)의 추산에 따르면, 각국의 분산 구매는 단가를 20-30% 상승시키고 있지만, 현지에서의 업무 분담을 우선시하는 정치적 의향이 규모의 경제 효과를 능가하는 경우가 적지 않습니다. 그 결과, 현재의 급증기가 지나면 비용 대비 효과에 대한 우려로 인해 생산 대수가 억제되어, 유럽의 전투기 시장의 장기적인 성장세가 둔화될 가능성이 있습니다.

부문별 분석

2025년 기준, 유럽의 전투기 시장에서 CTOL 기종의 점유율은 62.25%를 차지했습니다. 이는 확립된 기지 인프라와 NATO STANAG 규격에 부합하는 활주로에 기반을 두고 있습니다. 도입국들은 STOVL 기종에 비해 조달 비용과 유지비가 저렴하다는 점을 중시하고 있으며, 이를 통해 보다 광범위한 부대 구성에 대응할 수 있게 됩니다. 유럽의 전투기 시장에서는 수명 연장 기한이 다가옴에 따라 독일, 스페인, 폴란드로부터의 CTOL 기종 추가 발주가 예상됩니다.

VTOL/STOVL 기종은 낮은 수준에서 연평균 성장률(CAGR) 7.54%를 나타낼 것으로 전망됩니다. 이탈리아는 2024년, 카부르급 항공모함에서 F-35B의 초기 작전 능력(IOC)을 달성했다고 발표했습니다. 이는 통합 프로세스의 유효성을 보여주는 한편, 갑판 공간 및 정비 부담과 같은 문제점도 부각시키고 있습니다. 영국의 엘리자베스 여왕급 항공모함은 해당 지역 최대 규모의 STOVL 항공단을 배치하고 있지만, 65% 미만에 그치는 운용 준비율은 유지 관리의 부담을 여실히 드러내고 있습니다. 스페인이 2025년 F-35B 도입을 보류하기로 결정한 것은 장기적인 보급을 제한할 수 있는 재정적·운용적 타협점을 부각시키는 것입니다. 그럼에도 불구하고, 항공모함의 억지력 필요성과 분산 배치 개념으로 인해, 유럽의 전투기 시장에서 VTOL에 대한 수요는 여전히 주목받고 있습니다.

현역 기체의 80% 이상을 4세대 및 4.5세대 기종이 차지하고 있으며, 2025년에는 4.5세대 기종만으로도 유럽의 전투기 시장 점유율의 43.12%를 차지했습니다. 유로파이터 타이푼은 가장 광범위한 도입 실적을 자랑하며, 2025년 3월 이탈리아가 최대 24대를 추가 발주한 28억 유로(32억 8,000만 달러) 규모의 계약에 따라 생산이 2028년까지 연장됩니다.

6세대 프로그램은 FCAS(미래 전투 항공 시스템) 및 GCAP(차세대 전투 항공 플랫폼)이 구상 단계에서 실증기 시험 단계로 넘어감에 따라 연평균 성장률(CAGR) 8.18%로 성장을 지속하고, 있습니다. 2035년 이후까지 이어지는 일정, 공통 추진 시스템, 적응형 엔진 및 협업 전투 센서에 대한 선정 절차는 이미 공급업체 생태계를 형성해 나가고 있습니다. 이에 따라 유럽의 전투기 시장에서는 6세대 전투기가 운용 가능해질 때까지 4세대 및 5세대 전투기가 능력 격차를 메우는 이중 구조의 조달 환경이 조성되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe fighter aircraft market size was valued at USD 14.13 billion in 2025 and estimated to grow from USD 15.04 billion in 2026 to reach USD 20.59 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031).

This report is Segmented by Take-Off and Landing (Conventional Take-Off and Landing, and More), Fighter Generation (4th Generation, 4. 5th Generation, and More), Engine Configuration (Single-Engine and Twin-Engine), Mission Role (Air-Superiority, and More), End User (Air Force, and More), and Geography (United Kingdom, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Fighter Aircraft Market Trends and Insights

Post-Ukraine Surge in European Defense Budgets

The EU's SAFE regulation unlocks EUR 150 billion (USD 175.85 billion) in loan guarantees dedicated to joint capability acquisition, marking the region's most enormous peacetime spending wave since the Cold War. Germany's 5% of GDP pledge alone sends USD-level demand surging for new builds and sustainment across the Europe fighter aircraft market. National "escape-clause" budget mechanisms let Member States exceed fiscal rules by 1.5% of GDP through 2029, widening headroom for back-to-back orders. NATO's 2024 capability review called air-superiority gaps critical, turning fighters into top-priority line items. Near-term disbursements, therefore, push the Europe fighter aircraft market toward a procurement super-cycle that extends at least through 2030.

Accelerated 5th-Generation F-35 Procurements

Germany's 35-aircraft F-35A contract for nuclear-sharing roles anchors a regional commitment exceeding EUR 30 billion (USD 35.16 billion) to 2030. Belgium, Romania, and the Czech Republic follow with fleet conversions, valuing NATO interoperability over developmental risk. While US ITAR constraints raise sovereignty alarms, smaller forces accept dependency to secure near-term, 5th-generation capability envelopes. Resulting volume propels single-engine demand and reinforces a cost-per-flight-hour benchmark that influences future 6th-generation affordability discussions.

Soaring Acquisition and Life-Cycle Costs

F-35A unit prices exceed USD 80 million, while an upgraded Eurofighter approaches USD 120 million when development amortization is included. Sustainment typically accounts for 60-70% of total ownership, locking governments into multi-decade funding streams that squeeze other readiness accounts. The European Defence Agency (EDA) estimates that fragmented national buys add 20-30% to unit costs, yet political preferences for local workshare often trump economies of scale. Consequently, affordability pressures may moderate volumes after the current surge, tempering the long-run growth curve for the European fighter aircraft market.

Other drivers and restraints analyzed in the detailed report include:

- Launch of 6th-Generation Programs FCAS and GCAP

- Ageing Legacy Fleets Approaching End of Life

- Export-Control/ITAR Constraints on Subsystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CTOL aircraft accounted for 62.25% of the European fighter aircraft market in 2025, underpinned by well-established basing infrastructure and NATO STANAG-compliant runways. Fleet operators prize lower acquisition and sustainment costs versus STOVL peers, enabling broader force structure coverage. The European fighter aircraft market anticipates incremental CTOL orders from Germany, Spain, and Poland as life-extension deadlines converge.

VTOL/STOVL jets chart a 7.54% CAGR from a low base. Italy declared F-35B initial operating capability aboard the Cavour in 2024, validating integration pathways yet exposing deck-space and maintenance intensity challenges. The UK's Queen Elizabeth-class carriers field the region's largest STOVL air wing, but readiness rates below 65% spotlight sustainment burdens. Spain's 2025 decision to forgo F-35B acquisitions underscores fiscal and operational trade-offs that could cap long-term penetration. Even so, carrier-based deterrence needs and dispersed-basing concepts keep VTOL demand visibly on the radar of the European fighter aircraft market.

4th- and 4.5th-generation aircraft make up more than 80% of active inventories; 4.5th-gen alone held 43.12% of Europe's fighter aircraft market share in 2025. Eurofighter Typhoon commands the most extensive installed base, and Italy's March 2025 EUR 2.8 billion (USD 3.28 billion) order for up to 24 additional units extends production through 2028.

6th-generation programs exhibit an 8.18% CAGR as FCAS and GCAP progress from concept stage to demonstrator testing. While timelines stretch beyond 2035, down-selects on common propulsion, adaptive engines, and collaborative combat sensors are already shaping supplier ecosystems. For the European fighter aircraft market, this creates a dual-track procurement landscape where 4th-and 5th-generation aircraft bridge capability gaps until 6th-generation units become operational.

List of Companies Covered in this Report:

- Lockheed Martin Corporation

- Airbus SE

- Saab AB

- Dassault Aviation SA

- BAE Systems plc

- United Aircraft Corporation

- The Boeing Company

- Textron Inc.

- United Aircraft Corporation

- Leonardo S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Ukraine surge in European defense budgets

- 4.2.2 Accelerated 5th-generation (F-35) procurements

- 4.2.3 Launch of 6th-generation programs (FCAS and GCAP)

- 4.2.4 Ageing legacy fleets reaching end of life

- 4.2.5 EU joint-procurement mechanism unlocking scale buys

- 4.2.6 Rise of manned-unmanned teaming requirements

- 4.3 Market Restraints

- 4.3.1 Soaring acquisition and life-cycle costs

- 4.3.2 Export-control/ITAR constraints on subsystems

- 4.3.3 Lengthy development and certification timelines

- 4.3.4 Engine-core production bottlenecks in Europe

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Take-off and Landing

- 5.1.1 Conventional Take-off and Landing (CTOL)

- 5.1.2 Short Take-off and Landing (STOL)

- 5.1.3 Vertical Take-off and Landing (VTOL/STOVL)

- 5.2 By Fighter Generation

- 5.2.1 4th Generation

- 5.2.2 4.5th Generation

- 5.2.3 5th Generation

- 5.2.4 6th Generation/NGAD

- 5.3 By Engine Configuration

- 5.3.1 Single-Engine

- 5.3.2 Twin-Engine

- 5.4 By Mission Role

- 5.4.1 Air-Superiority

- 5.4.2 Multi-Role

- 5.4.3 Close-Air-Support/Strike

- 5.5 By End User

- 5.5.1 Air Force

- 5.5.2 Naval Aviation

- 5.5.3 Marine/Army Aviation

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Russia

- 5.6.5 Spain

- 5.6.6 Sweden

- 5.6.7 Austria

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lockheed Martin Corporation

- 6.4.2 Airbus SE

- 6.4.3 Saab AB

- 6.4.4 Dassault Aviation SA

- 6.4.5 BAE Systems plc

- 6.4.6 United Aircraft Corporation

- 6.4.7 The Boeing Company

- 6.4.8 Textron Inc.

- 6.4.9 United Aircraft Corporation

- 6.4.10 Leonardo S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment