|

시장보고서

상품코드

2061689

북미의 자동차용 AHSS : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Automotive AHSS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

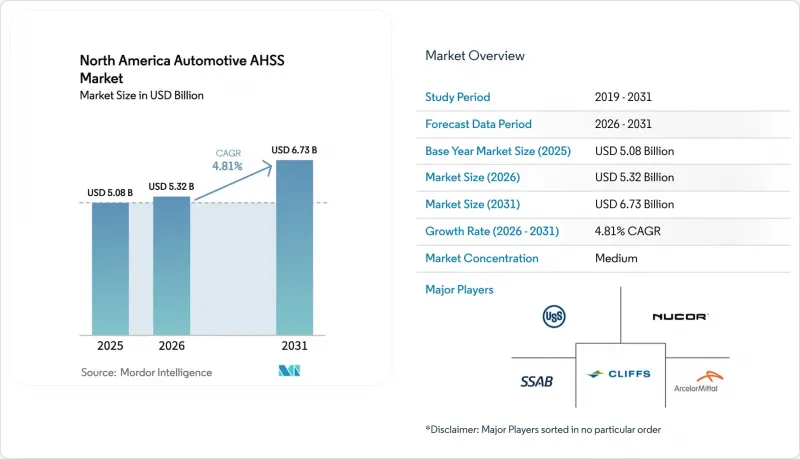

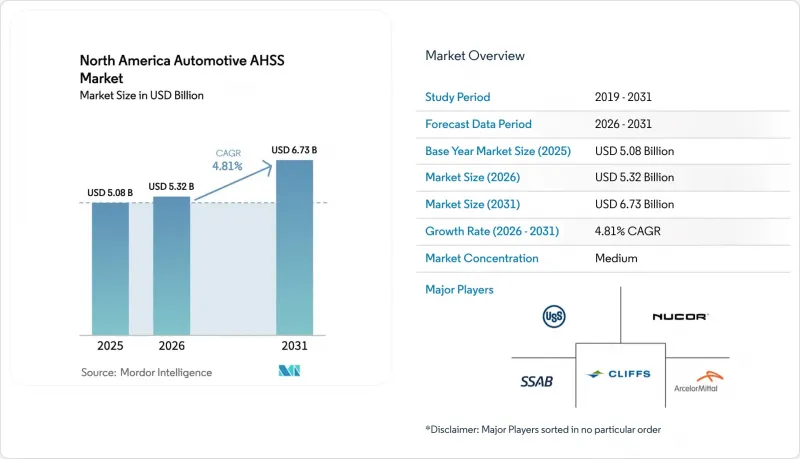

Mordor Intelligence에 의하면, 북미의 자동차용 AHSS 시장 규모는 2025년 50억 8,000만 달러로 평가되었습니다. 2026년 53억 2,000만 달러로 확대되어 2031년까지 67억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 4.81%를 나타낼 전망입니다.

본 보고서는 제품 유형(듀얼 페이즈, TRIP, 복합 페이즈, 마르텐사이트계, 기타), 차종(승용차, 기타), 용도(바디 인 화이트, 섀시, 서스펜션, 도어·펜더·해치, 기타), 제조 공정(냉간 압연, 열간 압연, 아연 도금), 최종 사용자(OEM 및 애프터마켓), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

북미의 자동차용 AHSS 시장 동향 및 인사이트

미국과 캐나다의 엄격한 연비 및 온실가스 규제가 경량화를 가속화하고 있습니다.

미국 환경보호청(EPA) 및 미국 도로교통안전국(NHTSA)은 2024-2025년형 모델에 대해 연평균 8%의 연비 개선을, 2026년에는 10%의 단계적 인상을 최종 결정하고, 2032년까지 차량 평균 연비를 58 mpg 수준으로 끌어올릴 방침입니다. 차량 총중량이 1파운드 감소할 때마다 연료 절약 효과가 크게 증가합니다. 그 결과, 차체(BIW) 제조업체들은 연강에서 듀얼 페이즈 강 및 복합 페이즈 강으로의 전환을 추진하고 있습니다. 이러한 첨단 소재를 통해 비틀림 강성을 저하시키지 않으면서 판 두께를 얇게 만들 수 있습니다. 캐나다도 이와 유사한 조치를 채택하여, 완전 도입을 목표로 하는 제로 에미션 차량 판매 할당제를 도입하고 있습니다. 이러한 움직임은 특히 배터리 추가로 인해 차량 중량이 증가하는 상황에서 구조적 강성의 필요성을 강조하는 것입니다. 연방준비제도이사회(FRB)의 조사에 따르면, 규제 준수 비용이 차량 가격에서 차지하는 비중이 산출되었습니다. 이러한 연구 결과를 바탕으로 자동차 제조업체(OEM)들은 비용이 더 많이 드는 추진 시스템 변경보다는 소재 변경을 우선시하고 있습니다. 티센크루프사의 HCT980XG 이상강은 연강에 비해 대폭적인 경량화를 실현하는 동시에, 소음·진동·불쾌감(NVH) 대책에 필수적인 비틀림 강성을 유지하고 있습니다.

IIHS 및 NCAP의 충돌 안전 평가 기준 강화가 더욱 견고한 차체 구조를 촉진

미국 도로안전보험협회(IIHS)는 측면 충돌 기준을 강화하여, ‘Good’ 등급을 받기 위한 B필러의 변형량에 상한선을 설정했습니다. 이 기준을 충족하기 위해 제조업체들은 케이지 구조에 프레스 경화 마르텐사이트강을 채택하는 경우가 많아지고 있습니다. 이는 기존에 충분하다고 여겨졌던 부품에서 전환하는 것을 의미합니다. 앞으로 미국 도로교통안전국(NHTSA)은 정면 비스듬한 충돌 시험 및 반대편 충돌 시험을 도입할 예정이며, 이에 따라 로커 패널과 루프 레일에는 더 높은 인장 강도가 요구될 것입니다. ‘탑 세이프티 픽+(Top Safety Pick+)’ 등급 획득을 목표로, 닛산은 ‘로그’의 AHSS(고장력강) 사용 비율을 높이고 테일러 용접 필러를 채택했습니다. 한편, AHSS와 UHSS(초고장력강)를 통합한 쉐보레의 ‘블레이저 EV’는 업계의 입장을 여실히 보여주고 있습니다. 즉, 주류 전기차라 하더라도 비용보다 충돌 안전성을 우선시하고 있다는 뜻입니다.

기존 철강 및 알루미늄에 비해 지속적으로 높은 가격

일정 강도 수준을 초과하는 AHSS 등급은 저강도 등급에 비해 가격 프리미엄이 부과됩니다. 한편, 마르텐사이트계 프레스 경화 강재의 경우, 더 높은 프리미엄이 책정되는 경우가 있습니다. 알루미늄의 낮은 밀도 덕분에 제조업체는 비구조 부재인 뚜껑의 무게를 대폭 줄일 수 있습니다. 이러한 제약으로 인해 AHSS의 사용은 주로 무게보다 강성이 우선시되는 구조 부위에 한정되어 있습니다. 관세로 인해 수입 알루미늄의 비용 경쟁력은 떨어졌지만, 보닛 및 리프트게이트 제조업체들은 여전히 복합 소재 방식을 채택하고 있습니다. 그러나 소형이고 가격에 민감한 배터리 전기자동차(BEV)의 경우, 균형은 다시 철강 쪽으로 기울고 있습니다. 이는 AHSS가 요구하는 경량화의 상당 부분을 원자재 단위당 비용을 대폭 절감하면서 실현할 수 있기 때문입니다. 주목할 만한 움직임으로, 클리블랜드 클리프스(Cleveland Cliffs)사는 금형을 약간만 조정하는 것만으로 AHSS 블랭크를 알루미늄용 프레스 라인에서 가공할 수 있음을 입증했습니다. 이러한 발전으로 인해 자동차 제조업체(OEM)의 경우, 소재 간 전환이 용이해질 것입니다.

부문별 분석

2025년, 듀얼 페이즈 강은 성형성과 강도의 균형이 최적이라는 점 덕분에 북미의 자동차용 AHSS 시장에서 39.33%의 점유율을 유지했습니다. TRIP 등급은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.78%를 나타낼 것으로 예측되며, 이는 제품 라인업 중 가장 높은 성장률입니다. 충돌 구역에서는 그 자리에서 경화되어 변형을 분산시키는 능력이 매우 중요합니다. 복합상 강재는 서스펜션 링크에서 특수한 역할을 담당하는 반면, 마르텐사이트계 강종은 특히 IIHS의 기준치가 허용 오차를 허용하지 않는 고강도 필러에 우선적으로 채택되고 있습니다. 쌍정 유도 소성(TIP) 강이나 온간 성형강은 틈새 시장 제품이지만, METAKUS사의 수상 경력이 있는 SIBORA가 보여주듯이, 연구 개발 분야에서 큰 주목을 받고 있습니다.

특정 강재는 높은 인장 강도와 뛰어난 연신율을 겸비하고 있어, 충돌 시험용 캔에서 상당한 성형 비율을 실현합니다. 펀칭 클리어런스 조정을 통해 HER(고효율 성형률)을 향상시킬 가능성이 제시되어, 광범위한 금형 규격에 영향을 미치고 있습니다. 이 강재를 하이드로포밍 성형된 필러에 활용하는 특정 설계 개념에서는 프레스 경화 성형 방식에 비해 비용을 절감하면서도 최고 수준의 안전 기준을 충족하는 성능을 제공했습니다. 이러한 발전에도 불구하고, 측면 충돌 시 하중 경로에서 내구성이 뛰어난 부품에 대한 지속적인 수요에 힘입어 특정 고장력 강재는 꾸준히 성장할 것으로 예측됩니다.

승용차는 2025년 북미의 자동차용 AHSS 시장 점유율의 62.29%를 차지하며 가장 큰 점유율을 유지했지만, 플랫폼이 비용 중심의 BEV 아키텍처로 전환됨에 따라 그 성장세는 둔화되고 있습니다. 한편, 소형 상용차는 택배 및 서비스용 차량의 전기화와 적재량 증가에 따라 연평균 성장률(CAGR) 7.54%를 나타낼 것으로 전망됩니다. 중형 및 대형 트럭에서는 운전실과 섀시 레일에 고강도 강판(AHSS)이 선택적으로 채택되고 있지만, 그 사용량은 차량 총 중량의 극히 일부에 그치고 있습니다.

GM의 ‘BrightDrop Zevo’는 넉넉한 적재 공간을 확보하면서도 무거운 배터리의 무게 균형을 맞추기 위해 AHSS의 적용 비율을 높였습니다. 포드의 신형 ‘E-Transit’은 적재량을 줄이지 않으면서 더 큰 배터리 팩을 탑재할 수 있도록 AHSS의 적용 비율을 높였습니다. 리비안의 ‘EDV’는 주행 거리 효율을 높이기 위해 핫 스탬핑 공법으로 제작된 도어 빔을 채택하고 있습니다. 승용차 부문에서는 혼다의 시빅이 ACE 케이지에 대량의 AHSS를 채택하고 있는 반면, 보다 저렴한 가격대의 모델에서는 비용 경쟁력을 유지하기 위해 고급 소재의 사용을 제한하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the north american automotive AHSS (Advanced High-Strength Steel) market size is projected to grow from USD 5.08 billion in 2025 to USD 5.32 billion in 2026, and is forecast to reach USD 6.73 billion by 2031, growing at a CAGR of 4.81% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dual Phase, TRIP, Complex Phase, Martensitic, and Others), Vehicle Type (Passenger Cars, and More), Application (BIW, Chassis, Suspension, Closures, and More), Manufacturing Process (Cold Rolled, Hot Rolled, and Galvanized), End User (OEMs and Aftermarket), and Country. The Market Forecasts are Provided in Value (USD).

North America Automotive AHSS Market Trends and Insights

Strict U.S./Canada Fuel-Economy and GHG Mandates Accelerate Light Weighting

The Environmental Protection Agency and the National Highway Traffic Safety Administration finalized 8% annual fuel-economy gains for model years 2024-2025 and a 10% step-up for 2026, pushing fleet averages toward 58 mpg-equivalent by 2032 . For every reduction in curb weight, fuel savings increase significantly. As a result, Body-in-White (BIW) manufacturers are transitioning from mild steel to dual-phase or complex-phase grades. These advanced materials enable a reduction in gauge without compromising torsional rigidity. Canada is adopting similar measures, introducing a zero-emission vehicle sales quota that aims to achieve full adoption. This move underscores the need for structural stiffness, especially as battery additions increase vehicle mass. A Federal Reserve study pegged the compliance cost as a percentage of a vehicle's price. This insight has led Original Equipment Manufacturers (OEMs) to prioritize material changes over more expensive propulsion modifications. Thyssenkrupp's HCT980XG dual-phase steel offers significant weight reduction compared to mild steel, all while maintaining a torsional stiffness critical for Noise, Vibration, and Harshness (NVH).

Rising IIHS and NCAP Crash-Rating Targets Spur Stronger Body Structures

The Insurance Institute for Highway Safety tightened side-impact standards, setting a limit on B-pillar intrusion for a "Good" rating. To meet this benchmark, manufacturers often turn to press-hardened martensitic steel in cage structures. This marks a shift from the previously adequate components. Looking ahead, the NHTSA plans to introduce frontal-oblique and far-side tests, necessitating higher tensile targets in rocker and roof rails. In a bid for a Top Safety Pick+ rating, Nissan boosted AHSS content in its Rogue and incorporated tailor-welded pillars. Meanwhile, Chevrolet's Blazer EV, with its AHSS and UHSS integration, underscores the industry's stance: even mainstream EVs prioritize crashworthiness over cost.

Persistent Cost Premium Versus Conventional Steels and Aluminum

AHSS grades above certain strength levels command a price premium over lower-strength grades. Meanwhile, martensitic press-hardened stock can fetch an even heftier premium. Thanks to aluminum's low density, manufacturers can achieve significant weight reduction in non-structural lids. This limitation confines AHSS usage primarily to structures where stiffness is prioritized over weight. While tariffs have diminished the cost advantage of imported aluminum, manufacturers of hoods and liftgates continue to adopt a mixed-material approach. However, for smaller, price-sensitive battery electric vehicles (BEVs), the scales tip back in favor of steel. This is because AHSS provides most of the desired weight reduction at a significantly lower cost per unit of raw material. In a notable move, Cleveland-Cliffs demonstrated that, with only minor adjustments to the dies, AHSS blanks can be processed on aluminum press lines. This development simplifies the transition between materials for original equipment manufacturers (OEMs).

Other drivers and restraints analyzed in the detailed report include:

- Surge in North American EV Output Lifts AHSS Demand for Battery Protection

- Domestic EAF Buildouts Widen Local Supply of Advanced Grades

- Capital-Intensive Forming / Welding Upgrades Slow Adoption at Smaller Tier-2s

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dual-phase steels maintained a 39.33% of the North America automotive AHSS market share in 2025, owing to their formability-versus-strength sweet spot. TRIP grades are forecast to post a 7.78% CAGR over 2026-2031, the fastest among the product slate. In crumple zones, the ability to harden on the fly and distribute deformation is crucial. Complex-phase steels occupy specialized roles in suspension links, while martensitic grades take precedence in high-strength pillars, especially where IIHS thresholds leave no room for error. Although twinning-induced plasticity and warm-formed steels are niche players, they are drawing significant R&D attention, as evidenced by METAKUS's award-winning SIBORA.

A specific type of steel offers high tensile strength and notable elongation, enabling significant draw ratios in crush cans. Adjustments to punching clearance have shown potential to boost HER, impacting die standards across a broad region. A particular concept, utilizing this steel in hydro-formed pillars, achieved cost savings compared to press-hardened alternatives while delivering performance aligned with top safety standards. Despite these advancements, certain high-strength steels are expected to grow steadily, driven by the continued need for durable components in side-impact load paths.

Passenger cars remain the tonnage leader at 62.29% of the North America automotive AHSS market share in 2025, but growth is slow as platforms migrate to cost-conscious BEV architectures. Light commercial vehicles are set for a 7.54% CAGR as parcel and service fleets electrify and increase payload. Medium- and heavy-duty trucks selectively incorporate Advanced High-Strength Steel (AHSS) in their cabs and chassis rails, limiting its use to a small percentage of the vehicle's total mass.

GM's BrightDrop Zevo uses a higher proportion of AHSS to counterbalance a heavy battery, while maintaining a spacious cargo bay. Ford's updated E-Transit increased its AHSS content to accommodate a larger battery pack without reducing payload capacity. Rivian's EDV utilizes hot-stamped door beams to enhance range efficiency. In the passenger car segment, Honda's Civic incorporates a significant amount of AHSS within its ACE cage, while more affordable models limit the use of premium materials to keep costs competitive.

List of Companies Covered in this Report:

- ArcelorMittal NA

- United States Steel Corporation

- Nucor Corporation

- Cleveland-Cliffs Inc. (AK Steel)

- SSAB AB

- Tata Steel Ltd.

- POSCO

- Thyssenkrupp AG

- Baoshan Iron and Steel Co. Ltd.

- Nippon Steel Corporation

- JFE Steel Corporation

- Hyundai Steel Company

- Kobe Steel Ltd.

- Voestalpine AG

- Steel Dynamics Inc.

- JSW Steel USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict U.S./Canada Fuel-Economy and GHG Mandates Accelerate Lightweighting

- 4.2.2 Rising IIHS and NCAP Crash-Rating Targets Spur Stronger Body Structures

- 4.2.3 Surge In North American EV Output Lifts AHSS Demand for Battery Protection

- 4.2.4 Domestic EAF Buildouts Widen Local Supply of Advanced Grades

- 4.2.5 Commercial Roll-Out of Guaranteed HER Grades Eliminates Edge-Crack Scrap

- 4.2.6 USMCA Rules-of-Origin Drive Tier-1 Hot-Stamping Near-Shoring

- 4.3 Market Restraints

- 4.3.1 Persistent Cost Premium Versus Conventional Steels and Aluminum

- 4.3.2 Capital-Intensive Forming/Welding Upgrades Slow Adoption at Smaller Tier-2s

- 4.3.3 Supply Risk for Critical Alloying Elements (Ni, Mo) Amid Geopolitical Tension

- 4.3.4 Limited Galvanizing-Line Capacity for UHSS Coatings Delays Programs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Product Type

- 5.1.1 Dual Phase (DP) Steels

- 5.1.2 Transformation-Induced Plasticity (TRIP) Steels

- 5.1.3 Complex Phase (CP) Steels

- 5.1.4 Martensitic Steels

- 5.1.5 Others (including TWIP, Hot-Formed Steels)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCVs)

- 5.2.3 Medium and Heavy Commercial Vehicles (MHCVs)

- 5.3 By Application

- 5.3.1 Body Structure (BIW)

- 5.3.2 Chassis

- 5.3.3 Suspension

- 5.3.4 Closures (Doors, Hoods, Trunk Lids)

- 5.3.5 Bumpers

- 5.3.6 Other Components

- 5.4 By Manufacturing Process

- 5.4.1 Cold Rolled

- 5.4.2 Hot Rolled

- 5.4.3 Galvanized

- 5.5 By End User

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 ArcelorMittal NA

- 6.4.2 United States Steel Corporation

- 6.4.3 Nucor Corporation

- 6.4.4 Cleveland-Cliffs Inc. (AK Steel)

- 6.4.5 SSAB AB

- 6.4.6 Tata Steel Ltd.

- 6.4.7 POSCO

- 6.4.8 Thyssenkrupp AG

- 6.4.9 Baoshan Iron and Steel Co. Ltd.

- 6.4.10 Nippon Steel Corporation

- 6.4.11 JFE Steel Corporation

- 6.4.12 Hyundai Steel Company

- 6.4.13 Kobe Steel Ltd.

- 6.4.14 Voestalpine AG

- 6.4.15 Steel Dynamics Inc.

- 6.4.16 JSW Steel USA