|

시장보고서

상품코드

2061695

재사용 발사체 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Reusable Launch Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

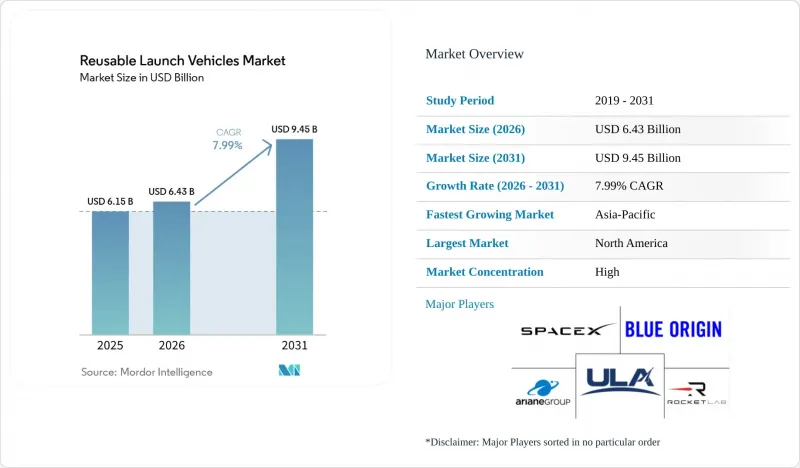

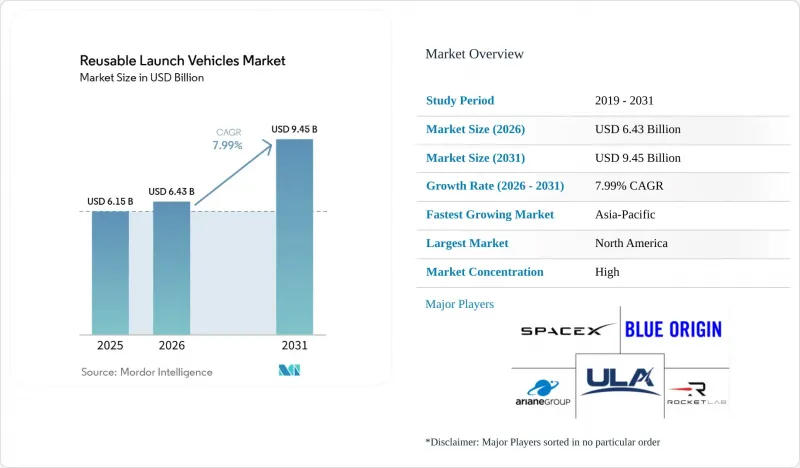

Mordor Intelligence에 의하면, 재사용 발사체 시장 규모는 2025년에 61억 5,000만 달러로 평가되었고, 예측 기간(2026-2031년)에서 CAGR 7.99%로 확대될 전망이며, 2026년 64억 3,000만 달러에서 2031년에는 94억 5,000만 달러에 이를 것으로 추정되고 있습니다.

본 보고서는 유형별(부분 재사용형 및 완전 재사용형), 구성별(단일 단계 궤도 투입형 등), 페이로드 등급별(소형, 중형, 대형), 최종 사용자별(민간, 국방 및 정부), 임무별(위성 배치, 유인 우주 비행 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 재사용 발사체 시장 동향 및 분석

부스터의 재사용을 통해 kg당 비용이 2,500달러 미만으로 낮아졌습니다.

재사용 가능한 부스터 덕분에 평균 발사 비용은 과거 많은 상업 임무의 걸림돌이었던 Kg당 2,500달러라는 기준선을 밑돌고 있습니다. 사업자들이 라인 생산 방식의 엔진 제조 및 표준화된 개조 절차로 전환함에 따라 한계 비용은 감소하고 있습니다. 이러한 경제성은 프리미엄 항공 화물 운임과 경쟁하는 지점 간 화물 운송이나 저궤도 물류 서비스와 같은 새로운 경로를 개척합니다. 하드웨어 배출량 감축은 새로운 환경 기준 준수를 통해 도입을 촉진함으로써, 경제적 이익과 지속가능성이라는 두 가지 이점을 동시에 창출합니다. 비용의 전환점으로 인해 광대역, 원격 감지, 우주 물류 분야의 잠재적 수요가 확대될 것입니다.

컨스텔레이션 붐이 요구하는 고빈도 발사

400건 이상의 상업용 위성군 프로젝트가 다양한 구축 단계에 있지만, 실제로 발사를 진행하고 있는 것은 그 5분의 1도 채 되지 않습니다. 각 전개 단계는 18-36개월로 압축되어 있으며, 서비스 제공업체들은 매주 또는 매일 발사 가능한 로켓을 확보해야 하는 상황에 놓여 있습니다. 국가 광대역 네트워크 및 지구관측 위성 배열을 위한 예정된 발사 건수는 이미 일회용 로켓의 잔여 발사 슬롯 수를 초과하고 있습니다. 부스터 1기당 매월 여러 차례의 임무를 수행할 수 있는 재사용 가능한 기체군은 사업자에게 비용 절감과 일정 안정성을 모두 제공하며, 향후 수년에 걸친 발사 계약을 확정할 수 있게 해줍니다.

초기 설비 투자 및 인프라 구축

대량 재사용 프로그램에는 전용 시험 베이, 비파괴 검사 실험실, 극저온 추진제 처리 셀이 필요하며, 이 모든 것을 고려할 때 초기 시설 투자 비용은 수억 달러 규모에 달할 전망입니다. 자금 소모는 비행으로 인한 수익을 얻기 시작하는 몇년전에 정점에 달하기 때문에 신규 진출기업의 재무 상황에 있어 큰 과제가 됩니다. 오래된 기업들은 검사 주기를 효율화하는 수직 통합형 엔진 공장이나 모듈식 격납고를 통해 이러한 과제를 완화하고 있지만, 발사 시장이 아직 성숙하지 않은 지역에게는 여전히 높은 진입 장벽으로 작용하고 있습니다.

부문별 분석

2025년 수익의 93.80%는 부분적으로 재사용 가능한 부스터에서 창출되었으며, 이는 1단 로켓의 회수가 로켓 비용 구조의 상당 부분을 차지하고 있음을 입증합니다. 재사용성 목표(예 : 팰컨 9 코어 1기당 40회 비행)는 하드웨어의 소규모 교체를 통해 정기적인 재비행을 가능하게 합니다. 따라서 재사용 발사체 시장은 부스터의 재가동 기간을 2주 미만으로 최적화한 업체들이 주도하고 있습니다. 그러나 기술 실증기가 상단 단계를 손상 없이 회수하는 방향으로 진전됨에 따라, 완전 재사용형 아키텍처는 11.17%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 열 차폐 및 추진제 관리 문제가 해결된다면, 종단 간 재사용을 통해 발사 한계 비용은 추진제 비용 수준에 근접할 정도로 낮아질 가능성이 있습니다.

2025년에 자금을 조달한 2세대 프로그램은 투자자들의 열의를 여실히 보여주고 있습니다. 한 완전 재사용형 스타트업이 2억 6,000만 달러를 조달했으며, 2026년 궤도 진입을 목표로 하고 있습니다. 기존의 주요 기업들은 턴어라운드 시간을 단축하기 위해, 바닥 충돌 후 재진입 프로파일 및 공중에서의 단계 포착에 관한 비행 시험을 실시했습니다. 양산 라인이 성숙해짐에 따라, 재사용 발사체 시장에서는 부분적 재사용 방식보다 완전 재사용 방식이 비용 측면에서 더욱 유리해질 것으로 예측됩니다.

2025년에는 2단식 궤도 투입(TSTO) 시스템이 88.90%의 점유율을 차지할 것으로 예상되며, 2031년까지 연평균 성장률(CAGR) 8.17%라는 최고 수준으로 성장하고 있습니다. 이는 공기역학적 여유와 추진 시스템의 유연성 사이의 균형을 반영한 것입니다. 1단 로켓의 회수는 페이로드 질량을 소량만 소모하는 데 그치며, 상단은 일회용으로 사용되거나 향후 회수 시험을 위해 대기 상태가 됩니다. 첨단 에어로스파이크 엔진이나 경량 복합재료 실험에 착수한 기업들은 지상 운용이 간편하고 필요한 기체 수가 적다는 장점을 보이고 있지만, 재진입 시의 부하와 추진제 예비량이 상업적 수익성을 저해하지 않는다는 점을 입증해야 합니다.

엔진의 추력 대 중량 비율 향상과 고효율 폐쇄 사이클 설계의 도입으로 인해, 2020년대 말까지 성능 격차는 줄어들 가능성이 있습니다. SSTO(단일 단계) 프로토타입이 내구성이 뛰어난 열차폐 타일과 신속한 재급유 및 재발사 절차를 입증해 냅니다면, 재사용 발사체 시장은 설계 측면에서 두 번째 혁신의 물결을 맞이하게 될 것입니다.

지역별 분석

북미는 성숙한 발사대, 수직 통합된 엔진 라인, 수십억 달러 규모의 정부 발사 계약에 힘입어 2025년 매출의 83.61%를 차지했습니다. 이 지역에 본사를 둔 기업들은 전 세계 궤도 비행의 절반 이상을 차지하며, 검증된 재비행 실적과 신속한 발사대 회전 능력을 통해 시장에서 주도권을 확보하고 있습니다. 수출관리 규정에 따라 동맹국의 군사 임무는 미국 공급업체로 배정되어, 공장 가동률을 유지하기 위한 국내 수주 잔고를 강화하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 17.77%를 기록하며 가장 빠르게 성장하는 지역이 될 전망입니다. 중국의 민간 기업은 2025년에 부스터 착륙 비행 시험을 실시했으며, 국내 메가 콘스텔레이션 계획과 연안 지역 우주항 건설을 연계했습니다. 인도의 차세대 발사체(NGLV) 프로그램은 회수 및 재사용 계획을 채택하고 있는 반면, 민간 스타트업 기업들은 비용 효율적인 공급망을 활용하여 국내에서 메탄 엔진을 제조하고 있습니다. 일본, 한국, 호주는 저경사 궤도에 대한 지역적 고객 수요를 예상하여, 적도 부근의 발사대 및 추진제 저장 시설에 대한 투자를 추진하고 있습니다.

유럽에서는 재사용 기술의 도입이 더딥니다. 발사 횟수가 적고 단일 대형 로켓 계획에 대한 의존도가 높기 때문에 전용 정비 시설의 설치를 정당화하기 위해 필요한 규모의 경제를 달성하지 못하고 있는 것입니다. 접이식 열차폐막을 갖춘 소형 로켓 개발에 착수한 신규 진출기업들은 기술 혁신을 보여주고 있지만, 국내 페이로드 프로젝트가 제한적이어서 재사용의 경제성이 저해되고 있습니다. ESA의 재사용 촉진 캠페인과 시험대 구축을 위한 민관 공동 출자 등 정책적 노력은 이러한 격차를 줄이는 것을 목표로 하고 있지만, 시장 점유율의 대폭적인 확대는 2030년 이후로 미뤄질 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the reusable launch vehicles market size was valued at USD 6.15 billion in 2025 and is estimated to grow from USD 6.43 billion in 2026 to USD 9.45 billion by 2031, at a CAGR of 7.99% during the forecast period (2026-2031).

This report is Segmented by Type (Partially Reusable and Fully Reusable), Configuration (Single-Stage-To-Orbit, and More), Payload Class (Small, Medium, and Heavy), End User (Commercial and Defense and Governments), Mission (Satellite Deployment, Human Spaceflight, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Reusable Launch Vehicles Market Trends and Insights

Cost-per-kg Drop to Less than USD 2,500 Driven by Booster Reuse

Reusable booster fleets are pushing average launch costs below the USD 2,500-per-kilogram threshold that once constrained many commercial missions. Marginal pricing falls as operators pivot to line-style engine production and standardized refurbishment procedures. These economics open new routes such as point-to-point cargo delivery and low-orbit logistics services that compete with premium air freight rates. Lower hardware emissions reinforce adoption by aligning with emerging environmental standards, creating a dual economic and sustainability benefit. The cost tipping point widens addressable demand across broadband, remote sensing, and in-space logistics.

Constellation Boom Demanding High-Cadence Launches

More than 400 commercial constellation projects are in various stages of build-out, yet fewer than one-fifth are actively launching. Each roll-out phase compresses into an 18- to 36-month window, forcing providers to seek vehicles able to fly weekly or even daily. Scheduled flights for national broadband networks and earth-observation arrays already exceed available slots on expendable rockets. Reusable fleets that can complete multiple missions per booster each month provide operators with both cost relief and schedule certainty, locking in launch contracts several years in advance.

Up-Front Capex and Refurbishment Infrastructure

High-volume reuse programs require specialized test bays, non-destructive evaluation labs, and cryogenic propellant handling cells, all of which push initial facility spending into the hundreds of millions of USD. Cash burn peaks years before flight revenue, challenging newcomers' balance sheets. Mature players are mitigating this through vertically integrated engine shops and modular hangars that streamline inspection cycles, yet the barrier remains formidable for regions with fledgling launch markets.

Other drivers and restraints analyzed in the detailed report include:

- Government and DoD Multi-Year Service Contracts

- Emergence of Heavy-Lift Fully Reusable Systems (Greater than 100 tons)

- Safety-Driven Regulatory Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Partially reusable boosters generated 93.80% of 2025 revenue, confirming that recovering the first stage captures most of a launch vehicle's cost base. Reusability milestones-40 flights per Falcon 9 core, for example, support routine reflights with minor hardware swaps. The reusable launch vehicles market is thus dominated by operators that have optimized booster turnarounds to fewer than two weeks. Fully reusable architectures, however, are registering the highest CAGR of 11.17% as technology demonstrators progress toward returning upper stages intact. Once thermal shielding and propellant management hurdles are solved, end-to-end reuse may bring marginal launch costs close to propellant costs alone.

Second-generation programs funded in 2025 underscore investor appetite: one fully reusable startup secured USD 260 million and booked a 2026 orbital debut. Established players are flight-testing belly-flop re-entry profiles and in-air stage grabs to shave turnaround times. As mass-production lines mature, the reusable launch vehicles market will likely see the cost curve bend further in favor of full reuse over partial schemes.

Two-stage-to-orbit (TSTO) systems held an 88.90% share in 2025 and are growing at the highest CAGR of 8.17% through 2031, reflecting a balance between aerodynamic margins and propulsion flexibility. First-stage return consumes modest payload mass while upper stages remain expendable or are queued for future recovery trials. Companies experimenting with advanced aerospike engines and lightweight composites illustrate the appeal-simple ground operations and a small vehicle count-yet must demonstrate that re-entry loads and propellant reserves do not erode commercial economics.

Expansion of engine thrust-to-weight ratios and the adoption of high-efficiency closed-cycle designs could narrow the performance gap by the end of the decade. If SSTO prototypes validate durable heat-shield tiles and rapid refuel-and-go procedures, the reusable launch vehicles market could witness a second wave of architectural disruption.

Geography Analysis

North America controlled 83.61% of 2025 revenue, anchored by mature launch pads, vertically integrated engine lines, and multi-billion-USD government launch contracts. Operators headquartered in the region accounted for over half of global orbital flights, securing market leadership through demonstrable reflight statistics and rapid pad turnaround capabilities. Export control rules channel allied military missions back to US providers, reinforcing a domestic backlog that sustains factory utilization.

Asia-Pacific will be the fastest-growing geography at a 17.77% CAGR. Chinese commercial firms flight-tested booster landings in 2025, pairing domestic mega-constellation plans with coastal spaceport build-outs. India's Next Generation Launch Vehicle program adopts recover-and-reuse plans, while private startups leverage cost-effective supply chains to build methane engines domestically. Japan, South Korea, and Australia are investing in equatorial launch pads and propellant depots, anticipating regional customer demand for low-inclination orbits.

Europe's uptake of reusability is slower. Sparse institutional launch volumes and reliance on a single heavy-lift program constrain economies of scale needed to justify dedicated refurbishment facilities. New entrants pursuing mini-launchers with fold-out heat shields illustrate technical innovation, yet limited domestic payload pipelines hinder the economics of reuse. Policy efforts, including ESA's reusability campaigns and public-private co-funding of test stands, aim to narrow the gap, but meaningful share gains may slip beyond 2030.

- Space Exploration Technologies Corp.

- ArianeGroup SAS

- United Launch Alliance, LLC

- Indian Space Research Organisation

- Rocket Lab USA, Inc.

- Mitsubishi Heavy Industries, Ltd.

- Blue Origin Enterprises, L.P.

- Hyundai Rotem Company

- Shanghai Academy of Spaceflight Technology

- Korea Aerospace Research Institute

- ispace, inc.

- LandSpace Technology Co., Ltd.

- Stoke Space Technologies, Inc.

- China Aerospace Science and Technology Corporation

- Innovative Rocket Technologies Inc. (iRocket)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-per-kg drop to less than USD 2,500 driven by booster reuse

- 4.2.2 Constellation boom demanding high-cadence launches

- 4.2.3 Government and DoD multi-year service contracts

- 4.2.4 Emergence of heavy-lift fully reusable systems (Less than 100 tons)

- 4.2.5 Venture-capital shift to "launch-on-demand" business models

- 4.2.6 Certification of reused boosters for national-security payloads

- 4.3 Market Restraints

- 4.3.1 Up-front capex and refurbishment infrastructure

- 4.3.2 Safety-driven regulatory delays

- 4.3.3 Sparse domestic demand in Europe limits reuse economics

- 4.3.4 Spaceport environmental/community opposition

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Partially Reusable

- 5.1.2 Fully Reusable

- 5.2 By Configuration

- 5.2.1 Single-Stage-to-Orbit (SSTO)

- 5.2.2 Two-Stage-to-Orbit (TSTO)

- 5.2.3 Multi-Stage (Booster-only reuse)

- 5.3 By Payload Class

- 5.3.1 Small (Less than 2,000 kg)

- 5.3.2 Medium (2,000 kg to 20,000 kg)

- 5.3.3 Heavy (More than 20,000 kg)

- 5.4 By End User

- 5.4.1 Commercial

- 5.4.2 Defense and Governments

- 5.5 By Mission

- 5.5.1 Satellite Deployment

- 5.5.2 Cargo Resupply and In-Space Logistics

- 5.5.3 Human Spaceflight

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 Middle East

- 5.6.4.2 Africa

- 5.6.4.3 South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Space Exploration Technologies Corp.

- 6.4.2 ArianeGroup SAS

- 6.4.3 United Launch Alliance, LLC

- 6.4.4 Indian Space Research Organisation

- 6.4.5 Rocket Lab USA, Inc.

- 6.4.6 Mitsubishi Heavy Industries, Ltd.

- 6.4.7 Blue Origin Enterprises, L.P.

- 6.4.8 Hyundai Rotem Company

- 6.4.9 Shanghai Academy of Spaceflight Technology

- 6.4.10 Korea Aerospace Research Institute

- 6.4.11 ispace, inc.

- 6.4.12 LandSpace Technology Co., Ltd.

- 6.4.13 Stoke Space Technologies, Inc.

- 6.4.14 China Aerospace Science and Technology Corporation

- 6.4.15 Innovative Rocket Technologies Inc. (iRocket)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment