|

시장보고서

상품코드

2061696

미국의 헤파린 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Heparin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

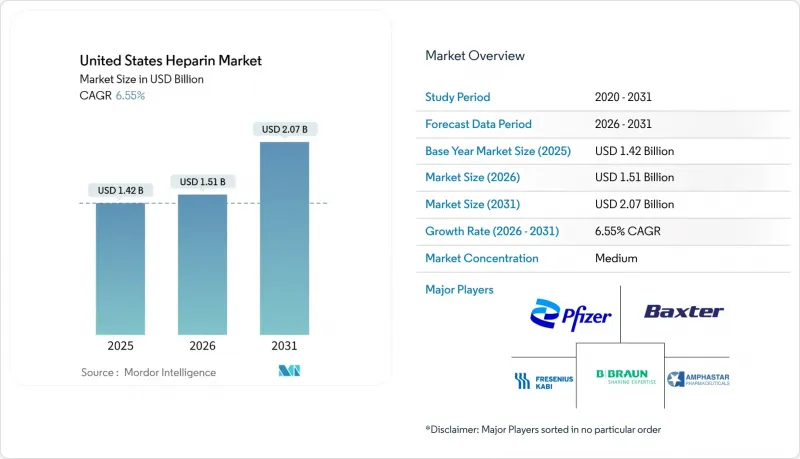

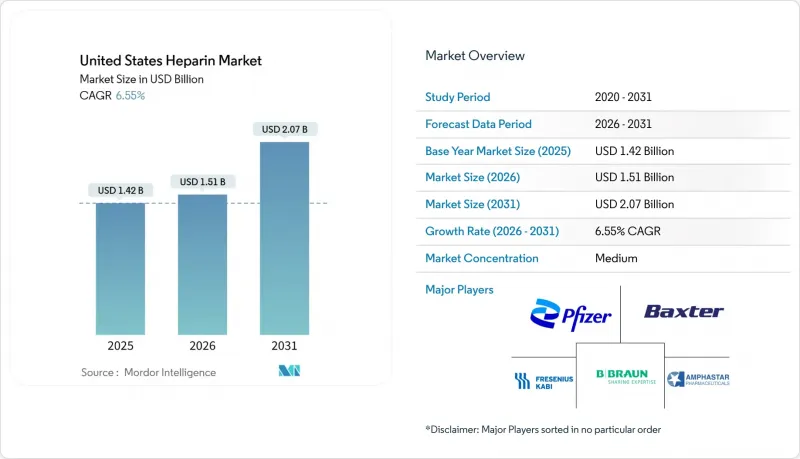

Mordor Intelligence에 의하면, 미국의 헤파린 시장 규모는 2025년에 14억 2,000만 달러로 평가되었습니다. 2026년에 15억 1,000만 달러에 달하고, 2031년까지 20억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 6.55%를 나타낼 전망입니다.

본 보고서는 제품별(비분획 헤파린, 저분자량 헤파린(LMWH) 등), 원료별(소 유래 및 돼지 유래), 투여 경로별(정맥 내 및 피하), 제형별(바이알 및 앰플 등), 용도(심부정맥 혈전증, 폐색전증 등), 그리고 최종 사용자(병원, 외래수술센터(ASC) 등)에 따라 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 헤파린 시장 동향 및 분석

심혈관 질환 및 혈전성 질환으로 인한 큰 부담

매년 미국에서 정맥혈전색전증(VTE)은 약 90만 명에게 영향을 미치며, 6만에서 10만 명의 사망을 초래하고, 100억 달러에 가까운 직접 의료비를 발생시키고 있습니다. 이러한 사례의 3분의 1 이상은 병원 내에서 발생하고 있으며, 그중 상당수는 적절한 시기에 약물 예방 치료를 통해 예방할 수 있습니다. 2024년, 미국의 심방세동(AF) 유병자 수는 성인 610만 명에 달했으며, 주로 고령화를 배경으로 2030년까지 그 수가 2배로 늘어날 것으로 예측됩니다. 암 환자는 특히 위험이 높으며, VTE 발병 위험이 4-7배 더 높고, 전체 혈전성 사건의 약 20%를 차지하고 있습니다. 또한, 이들 환자의 30% 가까이가 10년 이내에 혈전 재발을 경험하고 있어, 즉각적인 효과가 있으며 가역적인 치료제에 대한 지속적인 수요가 부각되고 있습니다. 이러한 시장 역학을 고려할 때, 미국의 헤파린 시장은 여전히 중요한 부문이며, 특히 경구용 약물의 편의성보다 신속한 효과나 프로타민을 통한 가역성이 우선시되는 상황에서는 그 중요성이 더욱 두드러집니다.

수술 및 투석 시술 건수 증가

수술 건수 증가가 예방적 헤파린 사용 증가를 이끌고 있습니다. 미국 질병통제예방센터(CDC)의 보고에 따르면, 연간 5,140만 건의 입원 수술과 2,860만 건의 외래 수술이 시행되고 있으며, 이 모든 수술에서 수술 전후 기간 동안 항응고 요법이 필요합니다. 투석 수요도 증가하고 있으며, 2024년에는 80만 9,103명의 환자가 있었으며, 이 중 69.8%가 시설 내 혈액투석을 받았습니다. FDA 승인을 받은 Defencath는 2024년 7월부터 TDAPA에 따른 보험 적용 대상이 되어, 투석 현장에서 도입이 확대되고 있습니다.

아프리카 돼지열병으로 인한 돼지고기 공급 변동

아프리카 돼지열병은 미국에서 사용되는 조헤파린의 약 80%를 공급하고 있는 중국의 양돈 업계에 계속해서 타격을 주고 있습니다. 2024년 8월, 박스터사가 엔도톡신 오염을 이유로 제품을 리콜한 사례는 공급망이 긴박해지면 품질 관리에 어떤 부담이 가해지는지를 보여줍니다. 과거 원자재 공급 차질로 인해 병원 내 헤파린 오용률이 152% 증가함에 따라, 절약 프로토콜 도입이 촉진되었습니다. 대부분의 시설에서는 비상시 처방집을 마련해 두고 있으며, 새로운 공급처가 H 스케일 도입에 대응할 수 있게 되면 공급업체 변경을 계획하고 있습니다. FDA의 소 유래 헤파린 심사는 제조업체가 필요한 안전 기준을 충족한다는 전제 하에, 공급원을 다각화하기 위한 단기적인 방안을 제시하고 있습니다.

부문별 분석

2025년, 저분자량 헤파린은 미국의 헤파린 시장 점유율의 62.22%를 차지했으며, 일반적으로 검사를 통한 모니터링이 필요 없는 1일 1회 예방 투여에 의해 뒷받침되고 있습니다. 에녹사파린은 정형외과 및 복부외과 치료 지침에서 여전히 주력으로 사용되고 있으며, 제네릭 의약품이기 때문에 공동구매 계약상 1회 투여당 비용은 10달러 미만으로 억제되고 있습니다. 비분획 헤파린은 심폐 우회술이나 ECMO 등 실시간 투여량 조정이 필수적인 중요한 시술 분야에서 수요를 유지하고 있어, 안정적인 기본 수요를 확보하고 있습니다. 초저분자량 헤파린은 항-Xa 활성을 저해하지 않으면서 출혈 위험을 줄이는 정제 분획 기술의 발전 덕분에, 2031년까지 연평균 성장률(CAGR) 6.90%를 나타낼 것으로 전망됩니다. FDA의 505(b)(2) 절차에 따른 크로마토그래피 기술에 대한 투자는 미국의 헤파린 시장에서 정밀 분자 기술로의 점진적인 전환을 시사하고 있습니다.

2025년에는 헤파린 원료의 89.30%가 돼지 장 점막에서 추출된 것이었으나, 브라질과 호주의 추출 능력을 바탕으로 소 유래 대체품이 연평균 성장률(CAGR) 7.40%로 확대되고 있습니다. FDA의 장려 조치와 프리온 검사 개선으로 인해 규제상의 마찰은 줄어들고 있지만, 효능 검증의 변경 및 라벨 갱신으로 인해 개발 기간은 길어지고 있습니다. 대학병원 처방위원회에서는 돼지 질병으로 인한 공급 충격에 대비하기 위해 2종 혼합 전략의 시범 도입이 진행되고 있으며, 미국의 헤파린 시장에서 회복탄력성을 중시하는 사고방식이 확산되고 있음이 부각되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the united states heparin market size is projected to be USD 1.42 billion in 2025, USD 1.51 billion in 2026, and reach USD 2.07 billion by 2031, growing at a CAGR of 6.55% from 2026 to 2031.

This report is Segmented Into by Product (Unfractionated Heparin, LMWH, and More), Source (Bovine and Porcine), Route of Administration (Intravenous and Sub-Cutaneous), Formulation (Vials and Ampoules and More), Application (Deep Vein Thrombosis and Pulmonary Embolism and More), and End-User (Hospitals, Ambulatory Surgical Centers and More). The Market and Forecasts are Provided in Terms of Value (USD).

United States Heparin Market Trends and Insights

High Burden of Cardiovascular & Thrombotic Diseases

Each year, venous thromboembolism (VTE) impacts nearly 900,000 individuals across the U.S., leading to 60,000 to 100,000 fatalities and incurring close to USD 10 billion in direct medical expenses. Over a third of these cases occur in hospital settings, many of which could be prevented with timely pharmacologic prophylaxis. In 2024, the prevalence of atrial fibrillation (AF) reached 6.1 million adults in the U.S., with projections indicating a doubling by 2030, driven primarily by an aging population. Oncology patients are particularly at risk, facing a 4- to 7-fold increased likelihood of VTE, which accounts for approximately 20% of all thrombotic events. Additionally, nearly 30% of these patients experience recurrent clots within a decade, highlighting a sustained demand for rapid-acting, reversible treatment agents. Given these market dynamics, the U.S. heparin market remains a critical segment, particularly in scenarios where a rapid onset and the ability to be reversed with protamine are prioritized over the convenience of oral medications.

High Surgical & Dialysis Procedure Volumes

Rising procedure volumes are driving increased prophylactic heparin use. The Centers for Disease Control and Prevention reports 51.4 million inpatient and 28.6 million outpatient surgeries annually, all of which require perioperative anticoagulation. Dialysis demand also climbs, with 809,103 patients in 2024 and 69.8% receiving in-center hemodialysis. FDA-approved Defencath is eligible for TDAPA reimbursement from July 2024, improving adoption in dialysis settings.

Porcine-Supply Volatility from African Swine Fever

African Swine Fever continues to disrupt Chinese pig herds that supply about 80% of the crude heparin used in the United States. The August 2024 Baxter recall for endotoxin contamination shows how tight supply chains can strain quality controls. Previous raw-material shocks raised hospital heparin error rates by 152% and prompted conservation protocols. Most facilities keep contingency formularies and plan supplier changes once new sources reacthe implementation of h scale. FDA review of bovine heparin offers a near-term path to diversify supply, provided manufacturers meet the required safety standards.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Heparin Formulations & Delivery Devices

- FDA-Led Diversification to Bovine-Sourced APIs

- Competition From Direct Oral Anticoagulants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low molecular weight heparin controlled 62.22% of the United States heparin market share in 2025, supported by once-daily prophylaxis that usually avoids lab monitoring. Enoxaparin remains the workhorse in orthopedic and abdominal surgery protocols, and its generic status keeps per-dose costs below USD 10 for group-purchasing contracts. Unfractionated heparin sustains a vital procedural niche where real-time dose adjustment is critical, such as cardiopulmonary bypass and ECMO, ensuring steady baseline demand. Ultra-low molecular weight heparin is forecast to post a 6.90% CAGR to 2031 as refined fractionation lowers bleeding risk without sacrificing anti-Xa potency. Investment in chromatographic technologies under the FDA 505(b)(2) pathway signals an incremental shift toward precision molecules within the United States heparin market.

Porcine intestinal mucosa supplied 89.30% of heparin APIs in 2025, yet bovine alternatives are expanding at a 7.40% CAGR on the back of Brazilian and Australian extraction capacity. FDA encouragement and improved prion testing reduce regulatory friction, though potency calibration changes and label updates extend timelines. Formulary committees at academic medical centers are piloting dual-species strategies to hedge against swine disease shocks, underscoring a growing resilience mindset in the United States heparin market.

List of Companies Covered in this Report:

- Accord Healthcare, Inc.

- Amphastar Pharmaceuticals

- B. Braun

- Baxter

- Bioiberica

- Changzhou Qianhong Bio-pharma

- CorMedix Inc.

- Dr. Reddy's Laboratories

- Fresenius Kabi USA LLC

- GLAND PHARMA

- Hikma Pharmaceuticals

- Laboratorios Ferrer/ROVI

- Meitheal Pharmaceuticals, Inc.

- Nanjing King-Friend Biochemical

- Pfizer

- Sagent Pharmaceuticals

- Sanofi

- Shenzhen Hepalink Pharmaceutical Co.

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden of Cardiovascular & Thrombotic Diseases

- 4.2.2 High Surgical & Dialysis Procedure Volumes

- 4.2.3 Advances In Heparin Formulations & Delivery Devices

- 4.2.4 FDA Led Diversification to Bovine-Sourced Apis

- 4.2.5 Bio-Engineered, Animal-Free Heparin Trial Roll-Outs

- 4.2.6 Bed-Side Anti-Xa POC Monitoring Drives Safe-Use Protocols

- 4.3 Market Restraints

- 4.3.1 Porcine-Supply Volatility from African Swine Fever

- 4.3.2 Competition From Direct Oral Anticoagulants

- 4.3.3 Stringent FDA Quality-Recall Environment

- 4.3.4 CMS Bundled-Payment Compression on Inpatient Anticoagulant Spend

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Unfractionated Heparin (UFH)

- 5.1.2 Low Molecular Weight Heparin (LMWH)

- 5.1.3 Ultra-Low Molecular Weight Heparin (ULMWH)

- 5.2 By Source

- 5.2.1 Porcine

- 5.2.2 Bovine

- 5.3 By Route of Administration

- 5.3.1 Intravenous

- 5.3.2 Subcutaneous

- 5.4 By Formulation

- 5.4.1 Vials & Ampoules

- 5.4.2 Prefilled Syringes & Cartridges

- 5.5 By Application

- 5.5.1 Atrial Fibrillation & Acute Myocardial Infarction

- 5.5.2 Stroke & Transient Ischemic Attack

- 5.5.3 Deep Vein Thrombosis & Pulmonary Embolism

- 5.5.4 Renal Dialysis & CRRT

- 5.5.5 Cardiopulmonary Bypass / ECMO

- 5.6 By End-User

- 5.6.1 Hospitals

- 5.6.2 Ambulatory Surgical Centers

- 5.6.3 Dialysis Centers

- 5.6.4 Home-care & Specialty Pharmacies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accord Healthcare, Inc.

- 6.3.2 Amphastar Pharmaceuticals, Inc.

- 6.3.3 B. Braun SE

- 6.3.4 Baxter International Inc.

- 6.3.5 Bioiberica S.A.U.

- 6.3.6 Changzhou Qianhong Bio-pharma

- 6.3.7 CorMedix Inc.

- 6.3.8 Dr. Reddy's Laboratories Ltd.

- 6.3.9 Fresenius Kabi USA LLC

- 6.3.10 Gland Pharma Ltd.

- 6.3.11 Hikma Pharmaceuticals PLC

- 6.3.12 Laboratorios Ferrer/ROVI

- 6.3.13 Meitheal Pharmaceuticals, Inc.

- 6.3.14 Nanjing King-Friend Biochemical

- 6.3.15 Pfizer Inc.

- 6.3.16 Sagent Pharmaceuticals

- 6.3.17 Sanofi

- 6.3.18 Shenzhen Hepalink Pharmaceutical Co.

- 6.3.19 Teva Pharmaceutical Industries Ltd.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment