|

시장보고서

상품코드

2061706

첨단 치료 의약품(ATMP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Advanced Therapy Medicinal Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

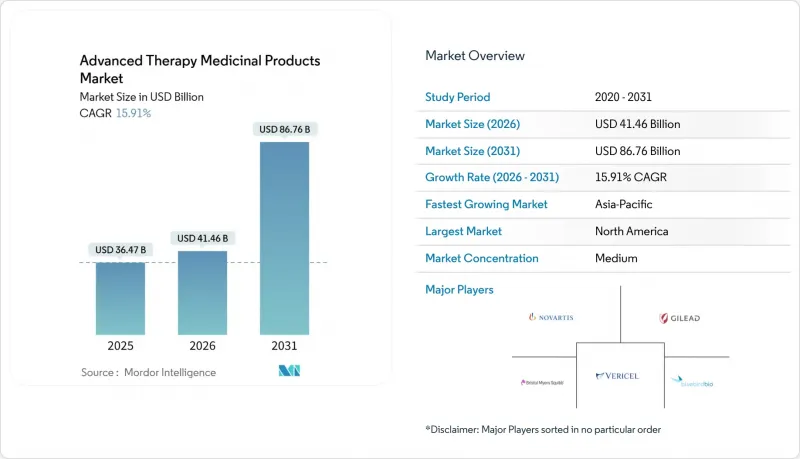

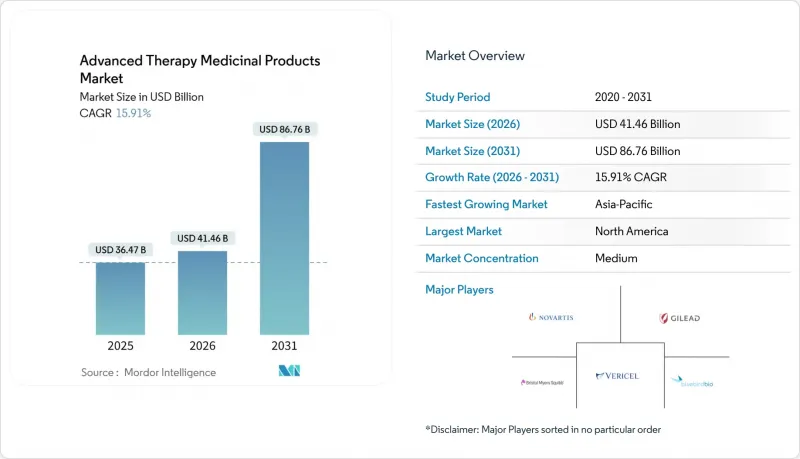

Mordor Intelligence에 의하면, 첨단 치료 의약품(ATMP) 시장 규모는 2025년에 364억 7,000만 달러로 평가되었습니다. 2026년에 414억 6,000만 달러에 달하고, 2031년까지 867억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 15.91%를 나타낼 것으로 전망됩니다.

본 보고서는 치료법의 유형(세포 치료, 유전자 치료 등), 세포 출처(자가 유래, 타가 유래), 벡터 유형(바이러스 벡터 등), 용도(종양학, 희귀 유전성 질환 등), 최종 사용자(병원·이식 센터 등), 제조 플랫폼(생체 내 변형 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 첨단 치료 의약품(ATMP) 시장 동향과 인사이트

2024년 이후, 규제 당국의 패스트트랙 지정 및 승인이 급증

규제 당국은 수요가 높은 치료법에 대한 심사 기간을 단축하고 있어, 선도 기업들이 희귀질환 시장을 신속하게 확보할 수 있게 되었습니다. EMA의 PRIME 프로그램은 2024년에 11건의 첨단 치료제 후보를 선정하여, 2023년 대비 38% 증가했습니다. 마찬가지로, 일본의 ‘선도’ 제도도 4건의 동종 이식 지정을 승인하여, 제2상 임상시험 데이터를 바탕으로 한 조건부 승인을 가능하게 했습니다. 이러한仕組み 덕분에 시장 출시까지의 기간은 약 6년으로 단축되지만, FDA의 새로운 지침에 따라 렌티바이러스 제제의 시판 후 조사 기간이 15년으로 연장되면서 중소 혁신 기업의 규정 준수 예산에 부담이 가중되고 있습니다.

ATMP 파이프라인 분야에서 벤처 캐피털 및 대형 제약사의 거래액이 급증

2024년에 발표된 거래액은 브리스톨-마이어스 스퀴브의 미라티 인수(48억 달러)와 길리어드의 레전드 바이오테크에 대한 8억 5,000만 달러 투자에 힘입어 123억 달러에 달했습니다. 2025년 빔 테라퓨틱스(Beam Therapeutics)가 5억 2,000만 달러 규모의 시리즈 D 투자 유치를 성사시킨 것은 차세대 유전자 편집 기술에 대한 벤처 기업들의 열의를 상징합니다. 미국과 유럽으로의 자본 집중은 다중 적응증 프로그램을 가속화하고 있지만, 아시아태평양의 많은 팀은 라이선싱에 의존할 수밖에 없는 상황에 처해 있습니다.

근치적 단일 투여 요법의 높은 비용과 보험 급여의 불확실성

환자 1인당 150만-300만 달러에 달하는 정가는 지불 주체의 예산을 압박하여, 부유한 지역 이외의 곳에서는 치료 접근성을 제한하고 있습니다. 블루버드 바이오의 ‘Lyfgenia’는 310만 달러에 시장에 데뷔했으며, exa-cel은 220만 달러에 상장되어 있습니다. 미국의 민간 보험사들은 유전자 치료를 보험 적용 대상에서 제외하는 경우가 많으며, 중소득국에는 보조금 제도가 마련되어 있지 않아 도입이 지연되고 있습니다.

부문별 분석

CAR-T 제제의 첨단 치료 의약품(ATMP) 시장 규모는 연평균 성장률(CAGR) 20.01%로 확대될 것으로 예상되며, 2025년에는 44.79%를 차지했던 유전자 치료와의 격차를 좁혔습니다. 2024년에 2차 치료제로서 미만성 대세포형 B세포 림프종에 대한 승인을 획득한 Breyanzi는 화학요법과 비교해 무악화 생존 기간을 34% 개선했습니다. Temcell 등의 세포 치료 제품은 일본 국내에서 1억 8,000만 달러의 매출을 기록했으나, 조직 공학 제품은 지불 기관들이 여전히 그 비용 대비 효과에 대해 논의하고 있어 틈새 시장에 머물러 있습니다. 유전자 편집과 저면역성 세포 공학을 융합한 복합형 ATMP는 인간을 대상으로 한 제1상 임상시험 단계에 접어들었습니다. 전반적으로, 급속히 확대되고 있는 CAR-T 파이프라인은 치료법의 구도를 재편하고 있으며, 첨단 치료 의약품(ATMP) 시장에서 점유율을 확대할 태세를 갖추고 있습니다.

유전자 치료는 단일 유전자 질환 치료에 있어 여전히 필수적이지만, 벡터 공급 제한과 면역원성 문제라는 과제에 직면해 있습니다. 유럽의 주요 시장에서는 병원 면제 제도를 활용하여 도입을 가속화하고 있지만, 미국의 지급 기관은 장기적인 유효성 데이터의 제시를 강력히 요구하고 있습니다. 펜실베이니아 대학교와 노바티스 같은 산학 협력 기관들은 생착률을 높이기 위해 CRISPR 편집 기술을 개선하고 있으며, 이는 첨단 치료 의약품(ATMP) 시장에서 지속적인 혁신이 이루어지고 있음을 시사합니다.

동종 이식 제제는 2031년까지 연평균 성장률(CAGR) 17.53%를 기록하며 자가 이식 워크플로우를 앞지를 것으로 예상되며, 현재 61.73%를 차지하는 자가 이식 시장 점유율에 도전하게 될 것입니다. 센추리 테라퓨틱스(Century Therapeutics)의 iPSC-CAR-NK 프로그램에서는 24명의 환자에서 이식편 대 숙주 질환(GVHD) 발생이 전혀 없었으며, 사나 바이오테크놀러지(Sana Biotechnology)의 SC291은 78%의 완전 반응률을 기록했습니다.

세계적인 보급은 재고 기반의 유통에 좌우됩니다. 이로 인해 환자의 대기 시간은 48시간으로 단축되고, 제조 비용은 60% 절감됩니다. 그러나 치료 기간이 짧다는 점 때문에 일부 임상의들은 여전히 자가 요법을 선택하고 있으며, 이것이 첨단 치료 의약품(ATMP) 시장 규모의 일부를 지탱하고 있습니다. 규제 당국은 현재 유전자 편집을 거친 동종 이식 제제에 대해 10년간의 모니터링을 의무화하고 있으며, 위험 관리 체계가 점차 명확해지고 있습니다.

지역별 분석

북미는 FDA의 신속 승인 프로그램과 학술적인 CAR-T 거점 간의 긴밀한 네트워크 덕분에 2025년 매출의 39.22%를 차지했습니다. exa-cel과 BEAM-101을 포함한 2024년 미국 내 10건의 ATMP 승인은 규제 측면에서의 긍정적인 추세를 뒷받침하고 있습니다. 캐나다의 조화로운 기준 덕분에 Lyfgenia의 동시 출시가 가능해졌습니다. 한편, 멕시코의 비용 대비 효과가 높은 임상시험 인프라는 Poseida의 제2상 동종 이식 임상시험을 유치하는 계기가 되었습니다. 미국 민간 보험사의 42%가 유전자 치료를 보험 적용 대상에서 제외하고 있어, 비용 부담 주체의 분산이 여전히 장벽으로 작용하며 단기적인 성장을 저해하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 18.46%를 기록하며 시장 성장을 주도할 것으로 전망됩니다. 중국 국가의약품감독관리국(NMPA)은 2024년에 9개의 국내 CAR-T 브랜드를 승인했으며, 이 중 Carvykti의 매출액 6억 8,000만 달러가 대부분을 차지했습니다. 인도는 2025년에 ATMP(첨단 치료 의약품) 개발에 1억 2,000만 달러를 배정하고, 헤모글로빈 질환을 우선순위로 삼았습니다. 한편, 한국의 인보사는 국민건강보험 적용으로 4,200만 달러의 매출을 확보했습니다. 그러나 아세안 각국의 규제 차이로 인해 해당 지역에서의 출시가 여전히 12-18개월 지연되고 있어, 첨단 치료 의약품(ATMP) 시장의 확대가 다소 늦어지고 있습니다.

유럽에서는 성과 연계형 상환 제도의 구축이 진행되고 있습니다. 독일의 공동 조달 이니셔티브에 따라 2025년에는 유전자 치료제 가격이 22% 인하될 것으로 결정되었으며, 프랑스에서는 현재 졸겐스마의 비용을 5년에 걸쳐 분할 납부하고 있습니다. EMA의 PRIME 프로그램 승인은 해당 지역의 임상적 깊이를 더욱 부각시키고 있습니다. 중동 및 아프리카 시장은 콜드체인의 부족과 높은 본인 부담 비용으로 인해 보급이 제한되고 있어, 여전히 초기 단계에 머물러 있습니다. 브라질에서 남미 최초로 2건의 CAR-T 치료제가 승인된 것은 시장의 점진적인 성장을 시사하고 있지만, 보험 급여 제도의 지연으로 인해 당분간 판매량이 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the advanced therapy medicinal products market size is projected to be USD 36.47 billion in 2025, USD 41.46 billion in 2026, and reach USD 86.76 billion by 2031, growing at a CAGR of 15.91% from 2026 to 2031.

This report is Segmented by Therapy Type (Cell Therapy, Gene Therapy, and More), Cell Source (Autologous, Allogeneic), Vector Type (Viral Vectors, and More), Application (Oncology, Rare Genetic Disorders, and More), End User (Hospitals & Transplant Centers, and More), Manufacturing Platform (In-Vivo Modified, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Advanced Therapy Medicinal Products Market Trends and Insights

Regulatory Fast-Track Designations and Approvals Surging Post-2024

Regulators are condensing review windows for high-need therapies, enabling first movers to secure orphan markets quickly. The EMA PRIME program accepted 11 advanced candidates in 2024, a 38% rise on 2023.Japan's Sakigake pathway similarly granted four allogeneic designations, allowing conditional approval on Phase II data. These mechanisms reduce the time-to-market to roughly six years, but new FDA guidance extends post-marketing surveillance for lentiviral products to 15 years, stretching the compliance budgets of smaller innovators.

Escalating VC and Big-Pharma Deal Values in ATMP Pipelines

Disclosed transaction value climbed to USD 12.3 billion in 2024, buoyed by Bristol-Myers Squibb's USD 4.8 billion Mirati buy-out and Gilead's USD 850 million Legend Biotech stake. Beam Therapeutics' USD 520 million Series D in 2025 exemplifies venture appetite for next-gen base-editing. Capital concentration in the United States and Europe accelerates multi-indication programs yet leaves many Asia-Pacific teams reliant on out-licensing.

High Cost and Reimbursement Uncertainty for Curative One-Off Therapies

List prices of USD 1.5 million-3 million per patient strain payer budgets, limiting access outside wealthy regions. Bluebird bio's Lyfgenia debuted at USD 3.1 million, and exa-cel lists at USD 2.2 million. U.S. private insurers often leave gene therapies off formularies, and middle-income economies lack subsidy frameworks, slowing adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rising Prevalence of Orphan and Oncology Indications Addressable by ATMPs

- Payer Shift Toward Outcome-Based Reimbursement Pilots for One-Time Cures

- Complex Cold-Chain Logistics and Short Shelf-Life Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The advanced therapy medicinal products market size for CAR-T constructs is forecast to advance at a 20.01% CAGR, narrowing the lead of gene therapy, which held 44.79% in 2025. Breyanzi's 2024 approval for second-line diffuse large B-cell lymphoma improved progression-free survival by 34% compared to chemotherapy. Cell therapy options, such as Temcell, posted USD 180 million in Japanese sales, while tissue-engineered products remain a niche market because payers still debate their cost-effectiveness. Combination ATMPs blending gene editing with hypoimmune cell engineering are entering first-in-human studies. Overall, rapidly expanding CAR-T pipelines recalibrate the therapeutic mix and are poised to capture a growing share of the advanced therapy medicinal products market.

Gene therapy remains critical for treating monogenic disorders, but it contends with vector supply limitations and immunogenicity hurdles. Demand centers in Europe leverage hospital-exemption options to accelerate adoption, whereas U.S. payers insist on long-term durability data. Academic-industry coalitions such as Penn-Novartis are refining CRISPR edits to improve engraftment, signaling iterative innovation inside the advanced therapy medicinal products market.

Allogeneic constructs are projected to outpace autologous workflows with a 17.53% CAGR through 2031, challenging the incumbent 61.73% autologous share. Century Therapeutics' iPSC-CAR-NK program showed zero graft-versus-host events across 24 patients, and Sana Biotechnology's SC291 posted 78% complete responses.

Global adoption hinges on inventory-based distribution, which reduces patient wait times to 48 hours and cuts manufacturing costs by 60%. Yet shorter persistence still drives some clinicians toward autologous regimens, sustaining segments of the advanced therapy medicinal products market size. Regulatory agencies now demand 10-year monitoring of gene-edited allogeneic constructs, adding clarity to risk management.

Geography Analysis

North America retained 39.22% of 2025 revenue thanks to FDA acceleration programs and a dense network of academic CAR-T hubs. Ten U.S. ATMP approvals in 2024, including exa-cel and BEAM-101, underline regulatory momentum. Canada's harmonized standards enabled simultaneous Lyfgenia launch, while Mexico's cost-effective trial infrastructure attracted Poseida's Phase II allogeneic study. Payer fragmentation remains a hurdle as 42% of U.S. private insurers exclude gene therapies, tempering near-term growth.

Asia-Pacific is projected to lead expansion with an 18.46% CAGR. China's NMPA cleared nine domestic CAR-T brands in 2024 and contributed most of Carvykti's USD 680 million sales. India earmarked USD 120 million for ATMP development in 2025, prioritizing hemoglobinopathies, while South Korea's Invossa secured USD 42 million sales under national insurance coverage. ASEAN regulatory divergence, however, still tacks 12-18 months onto regional launches, marginally delaying the advanced therapy medicinal products market ramp-up.

Europe continues to refine outcome-based reimbursement. Germany's pooled procurement initiative locked in a 22% gene-therapy discount in 2025, and France now spreads Zolgensma payments over five years. EMA's PRIME admissions accentuate the region's clinical depth. Middle East and Africa markets remain embryonic as cold-chain gaps and high out-of-pocket expenses limit diffusion. South America's first two CAR-T approvals in Brazil signal gradual emergence, yet reimbursement lags constrain immediate volume.

- Adaptimmune Therapeutics plc

- Beam Therapeutics Inc.

- Bluebird Bio

- Bristol-Myers Squibb

- Century Therapeutics

- CRISPR Therapeutics AG

- Roche

- Gilead Sciences

- JCR Pharmaceuticals

- Kolon TissueGene

- Legend Biotech Corp.

- MeiraGTx Holdings plc

- Novartis

- Orchard Therapeutics plc

- Pharmicell

- Poseida Therapeutics

- Sana Biotechnology Inc.

- Sarepta Therapeutics

- Spark Therapeutics

- uniQure N.V.

- Vericel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Fast-Track Designations & Approvals Surging Post-2024

- 4.2.2 Escalating VC & Big-Pharma Deal Values in ATMP Pipelines

- 4.2.3 Rising Prevalence of Orphan & Oncology Indications Addressable by ATMPs

- 4.2.4 Payer Shift Toward Outcome-Based Reimbursement Pilots for One-Time Cures

- 4.2.5 Decentralized GMP Micro-Facilities Enabling Point-Of-Care Cell Manufacturing

- 4.2.6 AI-Driven Vector Engineering Compressing Pre-Clinical Cycle Times

- 4.3 Market Restraints

- 4.3.1 High Cost & Reimbursement Uncertainty for Curative One-Off Therapies

- 4.3.2 Complex Cold-Chain Logistics & Short Shelf-Life Challenges

- 4.3.3 Long-Term Insertional-Oncogenesis Monitoring Liability Deterring Insurers

- 4.3.4 Shortage of GMP-Grade Plasmids & LNP Raw Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Cell Therapy

- 5.1.2 Gene Therapy

- 5.1.3 CAR-T Therapy

- 5.1.4 Tissue-Engineered Product

- 5.1.5 Combination ATMPs

- 5.2 By Cell Source

- 5.2.1 Autologous

- 5.2.2 Allogeneic

- 5.3 By Vector Type

- 5.3.1 Viral Vectors

- 5.3.2 Non-viral Vectors

- 5.3.3 Gene-editing

- 5.4 By Application

- 5.4.1 Oncology

- 5.4.2 Rare Genetic Disorders

- 5.4.3 Cardiovascular

- 5.4.4 Musculoskeletal & Orthopedic

- 5.4.5 Ophthalmology

- 5.4.6 Neurological Disorders

- 5.4.7 Others

- 5.5 By End User

- 5.5.1 Hospitals & Transplant Centers

- 5.5.2 Specialty Clinics

- 5.5.3 Academic & Research Institutes

- 5.5.4 Contract Manufacturing Organizations

- 5.6 By Manufacturing Platform

- 5.6.1 In-vivo Modified

- 5.6.2 Ex-vivo Modified

- 5.6.3 Point-of-Care Facilities

- 5.6.4 Centralised GMP Facilities

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 France

- 5.7.2.3 United Kingdom

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Adaptimmune Therapeutics plc

- 6.3.2 Beam Therapeutics Inc.

- 6.3.3 Bluebird Bio Inc.

- 6.3.4 Bristol-Myers Squibb Co.

- 6.3.5 Century Therapeutics

- 6.3.6 CRISPR Therapeutics AG

- 6.3.7 F. Hoffmann-La Roche Ltd

- 6.3.8 Gilead Sciences Inc.

- 6.3.9 JCR Pharmaceuticals Co. Ltd

- 6.3.10 Kolon TissueGene Inc.

- 6.3.11 Legend Biotech Corp.

- 6.3.12 MeiraGTx Holdings plc

- 6.3.13 Novartis AG

- 6.3.14 Orchard Therapeutics plc

- 6.3.15 Pharmicell Co. Ltd

- 6.3.16 Poseida Therapeutics

- 6.3.17 Sana Biotechnology Inc.

- 6.3.18 Sarepta Therapeutics

- 6.3.19 Spark Therapeutics

- 6.3.20 uniQure N.V.

- 6.3.21 Vericel Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment