|

시장보고서

상품코드

2061708

독일의 윤활유 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

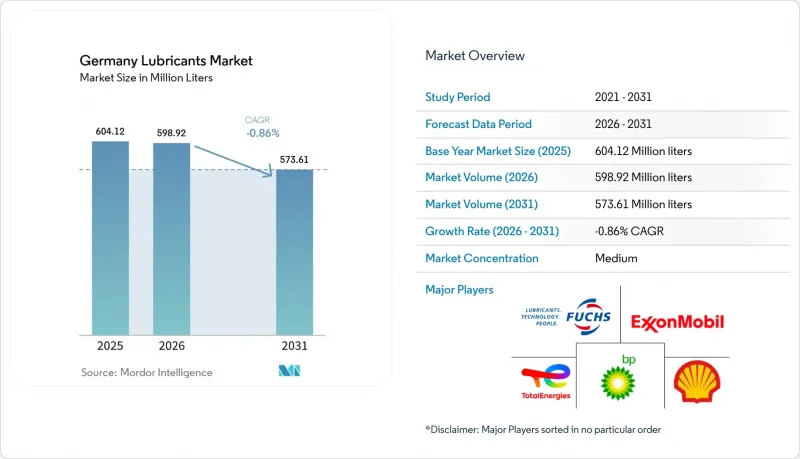

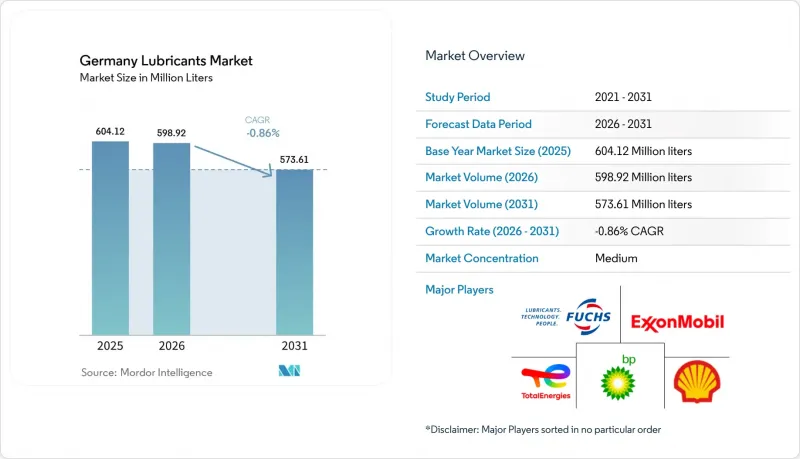

Mordor Intelligence에 의하면, 독일의 윤활유 시장 규모는 2025년 6억 412만 리터에서 2026년에는 5억 9,892만 리터로 축소되고, 2026년부터 2031년에 걸쳐 CAGR은 -0.86%를 나타내, 2031년에는 5억 7,361만 리터에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(자동차 엔진 오일, 산업용 엔진 오일, 변속기 오일, 기어 오일, 브레이크 오일, 유압 오일, 그리스, 공정 오일 등), 최종 사용자 산업(자동차, 선박, 항공우주, 중장비, 산업용), 기유 유형(광유계, 합성유, 반합성유, 바이오베이스)별로 분류되어 있습니다. 시장 전망은 수량(리터) 단위로 제시되어 있습니다.

독일의 윤활유 시장 동향과 인사이트

제조업 PMI의 회복이 금속 가공용 유압유 가격을 끌어올리고 있습니다.

2025년 12월, 독일의 기계 및 자동차 공장에서는 생산량이 크게 감소한 후 안정세를 보였습니다. 그 후, PMI가 상승할 때마다 금속 절삭 가공에 대한 수요가 증가했습니다. IoT 센서와 통합된 예측 유지보수용 에멀전은 샌프의 수명을 연장하는 데 성공하여 폐기물 발생량을 줄이는 데 기여하고 있습니다. 바덴뷔르템베르크주의 한 공급업체는 이미 CNC 가동률에 따라 냉각수를 보충하는 방안을 도입하여 가동 중지 시간을 현저히 줄이는 성과를 거두고 있습니다. 한편, 포름알데히드 방출제에서 에스테르계 반합성유로 전환함으로써 ISO 6743-7 규격 준수가 용이해졌으며, 표면 마감 품질이 저하되지 않습니다. 생산이 안정됨에 따라 이러한 공정 개선들이 시너지 효과를 발휘하여, 축소 추세를 보이고 있는 독일의 윤활유 시장에서도 완만한 판매량 증가가 예상됩니다.

전기차 전용 E-플루이드 및 열관리 오일

독일자동차산업협회(VDA)는 2024년의 부진한 실적과 비교해 2026년까지 배터리 전기차(BEV)의 등록 대수가 크게 증가할 것으로 전망하고 있습니다. 각 BEV에는 열전도율이 0.15 W/m·K를 초과하는 유전성 냉각수 외에도, 전기 절연성과 마찰 저감을 위해 특별히 배합된 E-액슬 오일이 필요합니다. 공장 충전용 공급 계약은 구동계 효율 향상에 기여합니다. 전기차용 배터리를 위해 설계된 합성 에스테르계 냉각수는 광범위한 온도 범위에서 점도 안정성을 보장합니다. 자동차 차종 구성이 전기화로 전환되는 가운데, 이러한 특수 유체는 독일의 윤활유 시장에서 가장 빠르게 성장하는 부문으로 부상하고 있습니다.

유럽의 정유시설 폐쇄로 인해 원유 공급이 부족해지고 있습니다.

BP는 게르젠키르헨에 있는 원유 처리 시설을 폐쇄할 계획을 발표했습니다. 한편, 쉘은 베셀링의 시설을 그룹 III 기유를 생산할 수 있는 거점으로 전환했습니다. 최근 독일에서는 기초유의 판매가 크게 감소하고 있어, 이에 따라 각 블렌더 업체들은 ARA 허브에서 고품질 기초유를 조달할 수밖에 없는 상황입니다. 게다가 장기 공급 계약을 맺지 않은 중소 사료 제조업체들은 이익률 압박으로 어려움을 겪고 있으며, 이러한 상황은 업계 재편을 가속화할 가능성이 있습니다.

부문별 분석

2025년에는 자동차용 엔진 오일이 29.72%를 차지하며 시장을 주도했습니다. 그러나 0W-16이나 0W-20과 같은 초저점도 오일의 등장은 시장에 혁명을 일으켜, 주입량 감축과 교환 주기 대폭 연장을 가능하게 했습니다. 금속 가공유 시장만이 유일하게 긍정적인 추세를 보이고 있으며, PMI 회복에 힘입어 2031년까지 연평균 성장률(CAGR) 0.06%로 완만하게 성장하고 있습니다. 합성 터빈유 및 변압기유는 해상 풍력 발전 프로젝트와 송전망 현대화에 따른 수요 증가의 흐름을 타고 성장했습니다. 한편, 회생 제동으로 인한 극심한 열에 적절히 대응할 수 있도록 브레이크 오일을 DOT 5.1로 업그레이드하는 작업이 진행되었습니다. 그 결과, 독일의 엔진 오일 시장은 전체 시장의 축소 속도를 웃도는 속도로 위축되었습니다.

2025년에는 산업용 오일, 변속기 오일, 기어 오일이 상용차 차량군에서 선호하는 긴 교환 주기의 영향으로 시장 규모에서 상당한 비중을 차지했습니다. 시장에서 상당한 점유율을 차지하고 있는 작동유와 그리스는 전기유압식 액추에이터의 대체품과의 경쟁에 직면했습니다. 기본적인 광물유 제품이 쇠퇴하는 시장에서 IoT를 활용한 상태 모니터링 기술을 적용한 특수 블렌드 제품이 독일의 윤활유 시장에서 틈새 시장을 공략하며 입지를 굳혔습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 CEO을 위한 중요 전략적 과제

KTH 26.06.19According to Mordor Intelligence, the germany lubricants market size is expected to decline from 604.12 million liters in 2025 to 598.92 million liters in 2026 and is forecast to reach 573.61 million liters by 2031 at -0.86% CAGR over 2026-2031.

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Transmission Fluids, Gear Oil, Brake Fluids, Hydraulic Fluids, Greases, Process Oil, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based). Market Forecasts are Provided in Volume (Liters).

Germany Lubricants Market Trends and Insights

Manufacturing-PMI Rebound Lifting Metalworking Fluids

In December 2025, Germany's machinery and motor-vehicle plants experienced a significant dip in output before stabilizing. Every uptick in the PMI subsequently bolstered the demand for metal-cutting. Predictive-maintenance emulsions, now integrated with IoT sensors, have successfully extended sump life, leading to a reduction in disposal volumes. Suppliers in Baden-Wurttemberg have already begun synchronizing coolant replenishment with CNC utilization, achieving a notable reduction in downtime. Meanwhile, a shift from formaldehyde releasers to ester-based semi-synthetics has allowed for easy compliance with ISO 6743-7, ensuring surface finish quality isn't compromised. As production stabilizes, these process enhancements are expected to compound, driving modest volume growth even in a contracting German lubricants market.

EV-Specific E-Fluids and Thermal-Management Oils

By 2026, the Verband der Automobilindustrie forecasts significant growth in battery electric vehicle (BEV) registrations compared to the subdued figures of 2024. Each BEV necessitates dielectric coolants with thermal conductivity greater than 0.15 W/m*K, alongside e-axle oils specifically formulated for electrical insulation and reduced friction. Contracts for factory-fill supplies enhance drivetrain efficiency. Synthetic-ester coolants designed for electric vehicle batteries ensure viscosity stability across a wide temperature range. As automotive fleets transition to electric, these specialized fluids are emerging as the most rapidly expanding segment in Germany's lubricants market.

European Refinery Closures Tightening Base-Oil Supply

BP has announced plans to close down its crude capacity at Gelsenkirchen. Meanwhile, Shell repurposed its Wesseling facility into a site capable of producing Group III base oil. In recent years, Germany experienced a significant decline in base-oil sales, which compelled blenders to source premium stocks from the ARA hub. Additionally, smaller formulators, lacking long-term offtake contracts, have been grappling with margin compression, a situation that could hasten industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind and Green-Hydrogen Turbine-Fluid Demand

- EU Batteries Regulation Fostering Electrolyte Know-How

- Upcoming PFAS Ban Threatening High-Temp Greases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive engine oil dominated at 29.72% in 2025. However, ultra-low-viscosity formulations such as 0W-16 and 0W-20 revolutionized the market, allowing for fill volume reductions and extending service intervals significantly. Metalworking fluids show the only positive trend, inching forward at 0.06% CAGR through 2031 as PMI rebounds. Synthetic turbine and transformer oils rode the wave of demand from offshore wind projects and grid upgrades. Meanwhile, brake fluids evolved, with upgrades to DOT 5.1 to better handle the intense heat from regenerative braking. Consequently, the market for engine oils in Germany contracted at a pace outstripping the broader market decline.

In 2025, industrial oil, transmission fluid, and gear oil collectively commanded a significant portion of the market volume, bolstered by long drain intervals favored by commercial fleets. Hydraulic fluids and greases, accounting for a notable share, faced competition from electro-hydraulic actuation substitutes. In a market where basic mineral products waned, specialty blends that leveraged IoT condition monitoring carved out a niche in the German lubricants landscape.

List of Companies Covered in this Report:

- ADDINOL

- BP p.l.c.

- Carl Bechem GmbH

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication

- LIQUI MOLY GmbH

- Quaker Chemical Corporation

- ROWE Mineralolwerk GmbH

- SCT Lubricants

- Shell plc

- TotalEnergies

- Valvoline

- Zeller+Gmelin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Manufacturing-PMI rebound lifting metal-working fluids

- 4.2.2 EV-specific e-fluids and thermal-management oils

- 4.2.3 Offshore-wind and green-hydrogen turbine-fluid demand

- 4.2.4 EU Batteries Regulation fostering electrolyte know-how

- 4.2.5 CSRD-driven uptake of re-refined base oils

- 4.3 Market Restraints

- 4.3.1 European refinery closures tightening base-oil supply

- 4.3.2 Upcoming PFAS ban threatening high-temp greases

- 4.3.3 EV-subsidy withdrawal distorting specialty-fluid mix

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 ADDINOL

- 6.4.2 BP p.l.c.

- 6.4.3 Carl Bechem GmbH

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Kluber Lubrication

- 6.4.7 LIQUI MOLY GmbH

- 6.4.8 Quaker Chemical Corporation

- 6.4.9 ROWE Mineralolwerk GmbH

- 6.4.10 SCT Lubricants

- 6.4.11 Shell plc

- 6.4.12 TotalEnergies

- 6.4.13 Valvoline

- 6.4.14 Zeller+Gmelin

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment