|

시장보고서

상품코드

2061709

유럽의 윤활유 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

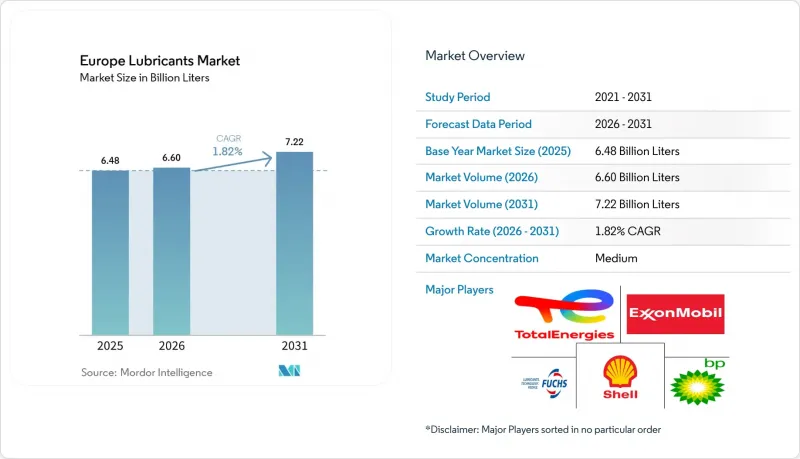

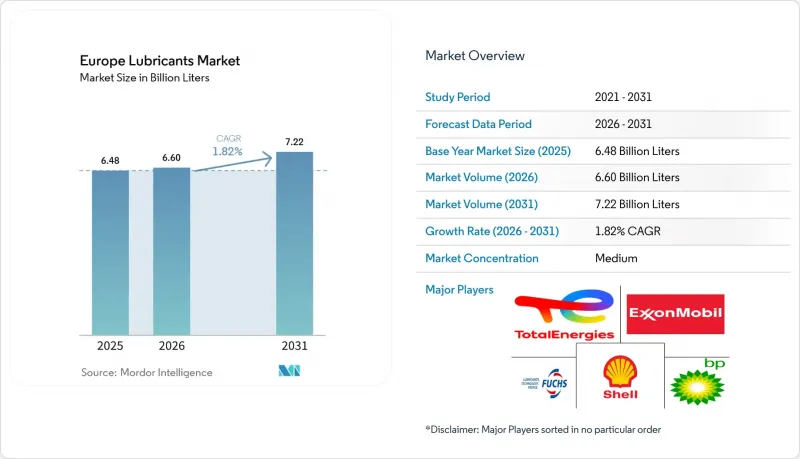

Mordor Intelligence에 의하면, 유럽의 윤활유 시장 규모는 2025년 64억 8,000만 리터에서 2026년에는 66억 리터로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 1.82%를 나타내, 2031년까지 72억 2,000만 리터에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(자동차 엔진 오일, 산업용 엔진 오일, 기어 오일 등), 베이스 오일 유형(광유계, 합성계, 반합성계, 바이오계), 최종 사용자 산업(자동차, 선박, 항공우주 등) 및 지역(프랑스, 독일, 이탈리아, 러시아, 스페인, 영국 및 기타 유럽)별로 분류되어 있습니다. 시장 전망은 수량(리터) 기준으로 제시되어 있습니다.

유럽의 윤활유 시장 동향과 인사이트

중동부 유럽의 산업 회복과 자동화의 급증

2025년, 중동부 유럽(CEE)의 제조업 생산액은 견조한 성장세를 보였으며, 특히 폴란드의 산업생산지수가 4.2% 상승하고, 독일의 OEM 제조업체에 부품을 공급하는 체코의 부품 부문이 8% 성장한 점이 주목을 받았습니다. 이러한 성장에 힘입어 배터리 하우징 및 모터용 적층판의 정밀 가공에 사용되는 금속 가공유 수요가 증가했습니다. 헝가리는 2024년부터 2025년에 걸쳐 배터리 공장 투자로 18억 유로(19억 5,000만 달러)를 확보했습니다. 각 기가팩토리에서는 자동화된 생산 라인을 위해 열전도유 및 작동유가 필요합니다. 루마니아의 제철소와 폴란드의 파운드리에서 인더스트리 4.0으로의 업그레이드가 진행됨에 따라, 센서 기반 유지보수를 지원하는 터빈 및 압축기용 윤활유 수요가 증가하고 있습니다. 구매자들은 유압 시스템에 대한 ISO 12925-1 청정도 기준을 점점 더 엄격하게 요구하고 있으며, 윤활유의 품질은 조달 결정의 중요한 요소가 되고 있습니다. 이러한 동향은 산업용 유체 시장에서 판매량과 이익률 모두를 끌어올리는 요인이 되고 있습니다.

팬데믹 이후 자동차 보유 대수의 회복

2025년, 유럽의 자동차 보유 대수는 2억 5,200만 대에 달했으며, 평균 차령 12.5년으로 세계에서 가장 높은 차령을 유지하고 있습니다. 구형 엔진은 여전히 많은 오일을 소모하기 때문에 신규 등록이 하이브리드 차량이나 배터리식 전기차로 전환되고 있음에도 불구하고 애프터마켓 판매를 지탱하고 있습니다. 디젤 차량은 여전히 전체 차량의 40%를 차지하고 있으며, 유로 6d 디젤 차량용으로 고SAPS 및 저SAPS 배합유가 공존해야 합니다. 2025년 시점에서 배터리식 전기차는 전체 차량 수의 불과 1.8%에 불과하여, 엔진 오일 수요에 미치는 즉각적인 영향은 제한적이었습니다. 하이브리드 차량은 연비 효율을 높이기 위해 0W-16이나 0W-20과 같은 저점도 등급에 대한 의존도를 높이고 있습니다. 상용차 차량군에서는 합성유를 사용함으로써 오일 교환 주기를 10만 킬로미터로 연장하고 있으며, 이로 인해 판매량과 이익률 간의 상충 관계가 발생하여 고급 윤활유 공급업체에 이익을 가져다주고 있습니다.

원유 가격과 첨가제 가격의 변동이 이익률을 압박하고 있습니다.

브렌트유 가격은 2025년에 배럴당 평균 82달러를 기록했으며, 2026년 초에도 84달러 전후로 움직였습니다. 기유 가격은 원유 가격의 동향과 밀접하게 연동되어, 소매 가격이 원가 상승을 따라가지 못하는 상황에서 블렌더의 이익률을 압박했습니다. 2024년부터 2025년에 걸쳐, 소수공급업체에 의해 생산되는 이황화 몰리브덴 및 ZDDP 농축물공급 제약으로 인해 첨가제 패키지 비용이 12% 상승했습니다. 이탈리아와 스페인의 중소규모 블렌더들은 2025년 4분기에 특정 SKU에서 매출 총이익률이 마이너스를 기록했다고 보고했습니다. 게다가 달러 강세로 인해 유로화 표시 수입 비용이 증가하면서, 북아프리카와 중동을 주요 시장으로 삼는 수출업체들의 이익률에 추가적인 압박이 가해졌습니다.

부문별 분석

2025년 기준으로 자동차 엔진 오일은 판매량 점유율의 39.12%를 차지했으나, 그리스는 2031년까지 연평균 성장률(CAGR) 2.07%라는 가장 높은 성장률을 기록하며 확대될 것으로 예측됩니다. 리튬 복합 그리스가 이 부문을 주도하고 있으며, 전체 시장의 약 60%를 차지하고 있어 전기차 휠 베어링이나 풍력 터빈의 블레이드 피치 장치에 널리 사용되고 있습니다. 칼슘설폰산계 그리스는 뛰어난 방청 성능 덕분에 선박 및 비도로용 분야에서 인기가 높아지고 있습니다. 금속 가공유와 관련하여, 공구 수명을 연장하기 위해 저발포성 에멀전이 필요한 배터리 부품의 기계 가공을 배경으로 폴란드, 체코, 헝가리에서 수요가 증가하고 있습니다. 한편, 변속기 오일 수요는 둔화되는 추세입니다. 이는 기존의 자동 변속기에 비해 하이브리드 차량의 듀얼 클러치 시스템에서는 필요한 오일량이 적기 때문입니다. 한편, 브레이크 오일 소비량은 차량의 노후화에 힘입어 안정적인 수준을 유지하고 있습니다.

또한, 그리스는 해상 풍력 터빈이나 고속 전기차용 베어링에서 극한의 온도를 견딜 수 있는 능력을 갖추고 있어 높은 수익률을 창출하고 있습니다. 중동부 유럽(CEE)의 건설 및 광업 분야에서는 유압작동유 사용이 확대되고 있으며, 임업 및 해상 설비에는 HEES 라벨이 부착된 에스테르 블렌드의 사용이 의무화되어 있습니다. 터빈 오일은 그룹 III 및 그룹 IV 합성유로 전환되고 있으며, 이를 통해 5년 주기의 교환 주기가 가능해져 피크 발전소 및 풍력 발전소의 가동 중단 시간이 줄어들고 있습니다. 변압기유의 등급 향상은 독일과 프랑스의 송전망 현대화를 뒷받침하고 있으며, 이 지역에서는 에스테르계 오일이 도시 변전소의 화재 안전성을 높이고 있습니다. 타이어 제조 및 제약 업계의 공정 오일 수요는 PAH 함량에 관한 REACH 규정의 기준치를 준수하는 처리된 증류 분획의 방향족 추출물로 점차 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 CEO을 위한 중요 전략적 과제

KTH 26.06.19According to Mordor Intelligence, the europe lubricants market size is expected to grow from 6.48 Billion Liters in 2025 to 6.60 Billion Liters in 2026 and is forecast to reach 7.22 Billion Liters by 2031 at 1.82% CAGR over 2026-2031.

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Gear Oil, and More), Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based), End-User Industry (Automotive, Marine, Aerospace, and More), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Liters).

Europe Lubricants Market Trends and Insights

Industrial Rebound And Automation Surge In CEE

Manufacturing output in Central and Eastern Europe saw robust growth in 2025, highlighted by a 4.2% rise in Poland's industrial production index and an 8% expansion in the Czech component sector supplying German OEMs. This growth has driven demand for metalworking fluids used in precision machining of battery housings and motor laminations. Hungary secured EUR 1.8 billion (USD 1.95 billion) in battery-plant investments during 2024-2025, with each gigafactory requiring heat-transfer and hydraulic oils for automated production lines. Industry 4.0 upgrades in Romanian mills and Polish foundries have increased the need for turbine and compressor lubricants, which support sensor-driven maintenance. Buyers are increasingly demanding ISO 12925-1 cleanliness standards for hydraulic systems, embedding lubricant quality into procurement decisions. These developments collectively boost both volume and margins in the industrial fluids market.

Post-Pandemic Vehicle-Parc Recovery

Europe's car fleet reached 252 million units in 2025, maintaining its status as the oldest globally, with an average age of 12.5 years. Older engines continue to consume more oil, supporting aftermarket sales despite a shift in new registrations toward hybrids and battery-electric vehicles. Diesel vehicles still make up 40% of the fleet, necessitating the coexistence of high-SAPS and low-SAPS formulations for Euro 6d diesels. Battery-electric vehicles accounted for only 1.8% of the fleet in 2025, limiting their immediate impact on engine oil demand. Hybrid vehicles increasingly rely on low-viscosity grades like 0W-16 and 0W-20, which enhance fuel efficiency. Commercial fleets are extending oil drain intervals to 100,000 kilometers by using synthetic formulations, creating a volume-for-margin trade-off that benefits premium lubricant suppliers.

Volatile Crude-Oil And Additive Prices Squeeze Margins

Brent crude oil averaged USD 82 per barrel in 2025 and remained near USD 84 in early 2026. Base-oil prices closely tracked crude trends, compressing blender margins when retail prices lagged behind cost increases. Additive package costs rose by 12% during 2024-2025 due to supply constraints for molybdenum disulfide and ZDDP concentrates, which are produced by a limited number of suppliers. Smaller blenders in Italy and Spain reported negative gross margins on certain SKUs in Q4 2025. Additionally, the strength of the US dollar inflated euro-denominated import costs, further pressuring margins for exporters targeting North Africa and the Middle-East.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Build-Out Needs Gear And Hydraulic Lubes

- Circular-Economy Mandates For Re-Refined Base Oils

- EU PFAS And Phosphate-Ester Restrictions In Fire-Resistant Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive engine oil accounted for a 39.12% volume share in 2025, while greases are expected to grow at the fastest 2.07% CAGR through 2031. Lithium-complex greases dominate the segment, representing approximately 60% of the category, and are widely used in electric vehicle wheel bearings and wind turbine blade-pitch mechanisms. Calcium-sulfonate greases are gaining popularity in marine and off-highway applications due to their enhanced rust protection. Metalworking fluids are witnessing increased demand in Poland, the Czech Republic, and Hungary, driven by battery-component machining that requires low-foaming emulsions to extend tool life. Meanwhile, transmission fluid demand is moderating as hybrid dual-clutch systems require smaller oil volumes compared to traditional automatics, while brake fluid consumption remains stable, supported by an ageing vehicle fleet.

Greases also offer high margins due to their ability to withstand extreme temperatures in offshore turbines and high-speed EV bearings. Hydraulic fluid usage is expanding in Central and Eastern Europe (CEE) construction and mining sectors, with HEES-labeled ester blends mandated for forestry and offshore equipment. Turbine oils are transitioning to Group III and Group IV synthetics, enabling five-year drain intervals and reducing downtime in peaker plants and wind farms. Transformer oil upgrades are supporting grid modernization in Germany and France, where ester-based fluids enhance fire safety for urban substations. Process oil demand in tire manufacturing and pharmaceuticals is shifting toward treated distillate aromatic extracts that comply with REACH thresholds for PAH content.

List of Companies Covered in this Report:

- BP p.l.c.

- Chevron Corporation

- Eni SpA

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft

- Idemitsu Kosan Co. Ltd

- Kluber Lubrication

- Liqui Moly GmbH

- Lukoil

- MOL Hungary

- Repsol

- Rosneft

- Shell plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industrial rebound and automation surge in CEE

- 4.2.2 Post-pandemic vehicle-parc recovery

- 4.2.3 Offshore-wind build-out needs gear and hydraulic lubes

- 4.2.4 Circular-economy mandates for re-refined base oils

- 4.2.5 AI-enabled predictive-maintenance boosting service fluids

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil and additive prices squeeze margins

- 4.3.2 EU PFAS and phosphate-ester restrictions in fire-resistant fluids

- 4.3.3 Lifetime-fill lubricants in wind-turbine gearboxes curb aftermarket

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-user Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By Base Stock Type

- 5.2.1 Mineral Oil-Based Lubricants

- 5.2.2 Synthetic Lubricants

- 5.2.3 Semi-Synthetic Lubricants

- 5.2.4 Bio-Based Lubricants

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.1.1 Passenger Vehicles

- 5.3.1.2 Commercial Vehicles

- 5.3.1.3 Two-Wheelers

- 5.3.2 Marine

- 5.3.3 Aerospace

- 5.3.4 Heavy Equipment

- 5.3.4.1 Construction

- 5.3.4.2 Mining

- 5.3.4.3 Agriculture

- 5.3.5 Industrial

- 5.3.5.1 Power Generation

- 5.3.5.2 Metallurgy and Metalworking

- 5.3.5.3 Textiles

- 5.3.5.4 Oil and Gas

- 5.3.6 Other End-user Industries

- 5.3.1 Automotive

- 5.4 By Geography

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Russia

- 5.4.5 Spain

- 5.4.6 United Kingdom

- 5.4.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BP p.l.c.

- 6.4.2 Chevron Corporation

- 6.4.3 Eni SpA

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gazpromneft

- 6.4.7 Idemitsu Kosan Co. Ltd

- 6.4.8 Kluber Lubrication

- 6.4.9 Liqui Moly GmbH

- 6.4.10 Lukoil

- 6.4.11 MOL Hungary

- 6.4.12 Repsol

- 6.4.13 Rosneft

- 6.4.14 Shell plc

- 6.4.15 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment