|

시장보고서

상품코드

2061720

지게차용 배터리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Forklift Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

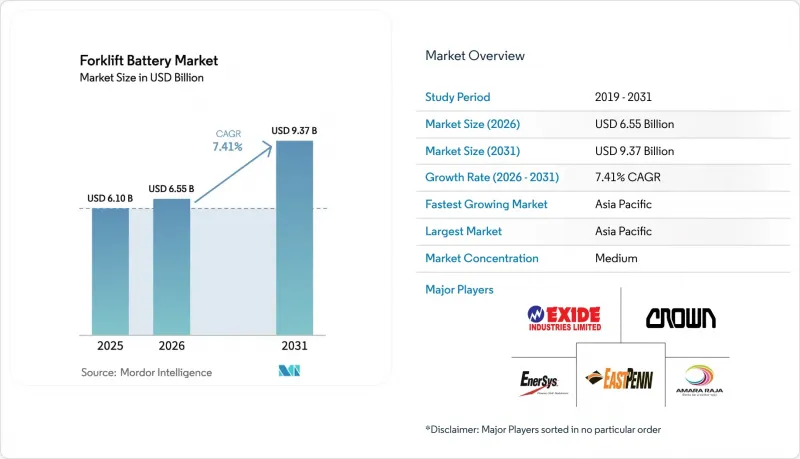

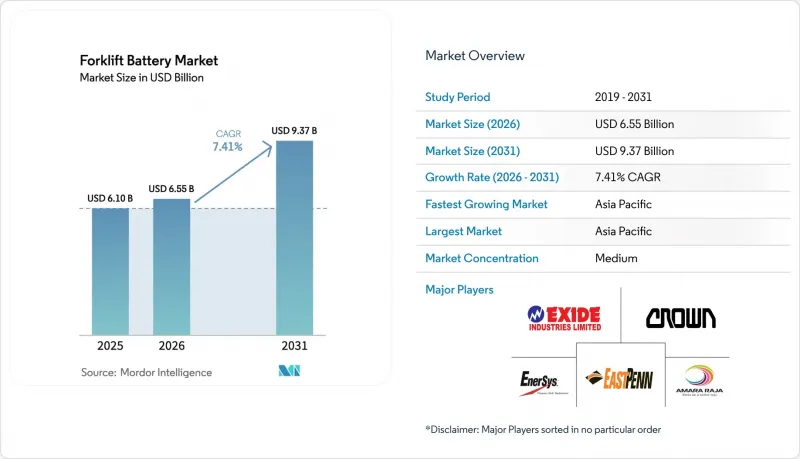

Mordor Intelligence에 의하면, 지게차용 배터리 시장 규모는 2025년 61억 달러로 평가되었고, 2026년에는 65억 5,000만 달러로 추정되고, 2031년까지 93억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년)에서 CAGR 7.41%로 성장할 전망입니다.

본 보고서는 배터리 유형별(납축전지, 리튬이온전지 등), 전압 용량별(24V 미만, 24V-36V 등), 용도별(창고 및 물류, 제조 등), 판매 채널별(OEM(원청 브랜드 제조), 애프터마켓) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 지게차 배터리 시장 동향과 분석

리튬 이온 배터리의 비용 절감과 총소유비용(TCO)의 경쟁력

리튬 이온 배터리 팩의 평균 가격은 최근 몇 년간 크게 하락했으며, 양극재의 양산 규모 확대와 셀-투-팩 통합의 진전에 따라 추가적인 가격 하락이 예상됩니다. 니켈·망간·코발트계 배터리에 비해 훨씬 저렴한 인산철리튬(LFP) 배터리 팩은 현재 전 세계 전기차(EV) 배터리 시장의 상당 부분을 차지하고 있으며, 지게차 구매자들에게 상당한 규모의 경제 효과를 가져다주고 있습니다. 급수 작업, 환기 설비, 전용 배터리실이 필요 없어짐에 따라, 운영자는 기존의 납축전지 시스템에 비해 총 운영 비용을 대폭 절감할 수 있습니다. 또한, 리튬 시스템의 회생 제동은 납산 시스템보다 더 높은 비율로 에너지를 회수하기 때문에 특히 처리량이 많은 환경에서 전력 비용 절감으로 이어집니다. 비용 면에서의 이점은 배터리 팩 자체에만 국한되지 않습니다. 예를 들어, 밀폐된 작업 환경에서 전동 장비로 전환함으로써, 주로 환기 요건이 완화되어 연간 상당한 비용 절감 효과가 입증되었습니다.

전자상거래와 창고 자동화의 급속한 성장

온라인 소매의 급속한 성장에 따라 물류 환경은 급변하고 있습니다. 전자상거래가 확산될수록 창고 공간에 대한 추가 수요가 크게 증가하고 있습니다. 여러 교대 근무제를 도입한 지게차 운영이 주류를 이루는 현대의 창고에서는 리튬 이온 배터리로의 전환이 진행되고 있습니다. 이 배터리들은 전압 강하 위험 없이 수시로 충전할 수 있습니다. 이러한 추세를 상징하듯, Geekplus가 JJCL을 위해 도입한 콜드체인 자동화 시스템은 보관 밀도를 대폭 높이고 피킹 효율을 향상시켰습니다. 이러한 로봇 기술의 발전은 리튬 배터리 교체 투자에 대한 회수 기간을 단축하는 데 있어 매우 중요한 역할을 하고 있습니다. 기존 소매 매장에서 전문 물류 허브로의 전환으로 인해, 매출 1달러당 필요한 물류 공간이 크게 증가했습니다. 이러한 변화로 인해 밀폐형이며 유지보수가 필요 없는 배터리 화학 조성에 대한 수요가 증가하고 있습니다. 많은 화주들이 더욱 신속한 배송을 기대하게 되면서, 다중 교대 근무 체제에 대한 의존도가 급격히 증가하고 있습니다. 그러나 납축전지는 이러한 수요 증가에 충분히 대응하지 못하고 있습니다.

제한된 리튬 이온 배터리 재활용 인프라와 책임 위험

유럽의 배터리 규제에서는 코발트, 리튬, 니켈에 대해 재활용 함유율 기준치가 의무화되어 있을 뿐만 아니라, 야심찬 회수 목표도 설정되어 있습니다. 그러나 중국의 세계 배터리 재활용 시장 지배력으로 인해, 유럽과 북미에서는 현지 시설이 부족하다는 문제에 직면해 있습니다. 폐쇄형 순환 시스템의 부재로 인해 사업자들은 사용 후 배터리 팩을 수출하거나 매립 처분할 수밖에 없으며, 공급업체들은 확대 생산자 책임(EPR)에 따른 법적 책임과 증가하는 재활용 비용에 직면해 있습니다. 재활용 시설에서 발생하는 열폭주 사고 증가 역시 보험료 인상을 초래하고 있으며, 고가의 소화 설비를 업그레이드하지 않는 한 중규모 차량 보유자들이 리튬 배터리 도입을 주저하게 만드는 요인이 되고 있습니다. 의무화될 디지털 배터리 패스포트에는 원자재의 추적 가능성이 요구되므로, 첨단 IT 시스템을 갖추지 못한 중소 공급업체에는 추가 비용이 발생하게 됩니다. 파산 전 낮은 가동률로 어려움을 겪었던 노스볼트의 에트 공장은 리튬 가격 하락과 높은 인건비가 유럽의 국내 재활용 사업에 미치는 영향을 여실히 보여주고 있습니다.

부문별 분석

2025년 기준으로 납축전지는 지게차용 배터리 시장 점유율의 70.21%를 차지했으며, 이는 주로 확립된 서비스 생태계와 구형 충전기와의 호환성 때문인 것으로 분석됩니다. 그럼에도 불구하고, 특히 교대 근무제나 냉장 창고와 같은 현장에서 총 소유 비용이 납축전지보다 약 40% 저렴하기 때문에 리튬 이온 배터리는 2031년까지 연평균 성장률(CAGR) 8.11%로 성장할 것으로 전망됩니다. 고체 배터리 시스템은 아직 실험 단계에 있는 반면, 니켈-수소 배터리 기술은 여전히 틈새 시장 수준에 머물러 있으며, 팩 가격은 400달러/kWh를 초과하고 있습니다.

리튬 기술의 부상은 사용자 친화적인 개조 키트의 도입에 힘입고 있습니다. 예를 들어, BSLBATT는 도요타, 하이스터, 린데, 윤하이리히 등의 브랜드 트럭과 호환되는 UL 인증 모듈을 특징으로 하는 드롭인 시리즈를 출시했습니다. 반면, GS 유아사의 YBX9625와 같은 AGM형이나 개량형 액체식 납축전지는 사이클 수명이 길다는 장점이 있지만, 리튬 전지의 뛰어난 에너지 밀도나 급속 충전 능력에는 미치지 못하는 것이 현실입니다.

2025년 기준 지게차용 배터리 시장 점유율의 38.22%를 차지하는 24-36V 등급은 1교대 근무 방식의 팔레트 트럭이나 오더 피커에 적합합니다. 그러나 36-48V 솔루션 시장은 2031년까지 연평균 성장률(CAGR) 8.28%로 성장할 전망입니다. 현재 대형 창고에서는 훨씬 더 높은 토크와 더 빠른 리프트 동작을 구현하는 장비가 우선적으로 도입되고 있습니다. 또한, 고전압 운전은 저항 손실을 줄여주며, 상당한 에너지 회수를 가능하게 합니다.

대당 전환 비용은 높지만, 콜드체인 및 외식 산업의 차량 운영사들은 신뢰할 수 있는 저온 성능과 위생적으로 밀폐된 차체의 필요성을 중시하여 도입을 주저하지 않고 있습니다. 시장이 점차 고전압으로 전환되고 있다는 사실은 리튬 배터리 팩과 차량 내 충전 기능을 탑재한 EP 북미 모델 등, 각 OEM 업체들의 신제품 발표를 통해서도 분명히 드러납니다.

지역별 분석

아시아태평양은 2025년에 지게차용 배터리 시장 점유율의 46.34%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.89%를 기록할 전망입니다. 이는 중국이 전 세계 리튬 이온 배터리 셀 생산 능력의 대부분을 차지하는 반면, 인도가 기가팩토리에 대규모 투자를 진행하고 있기 때문입니다. 주요 기업인 CATL은 전 세계 전기차 및 전력망용 배터리 시장의 상당 부분을 공급하고 있습니다. 이러한 경쟁 우위 덕분에 지역 통합 공급업체는 유럽 및 미국의 동종 업체보다 훨씬 저렴한 가격으로 지게차용 배터리 팩을 공급할 수 있게 되었습니다. 일본의 탄소 중립이라는 야심 찬 목표에 발맞추어, BSLBATT는 주요 거점에 전략적으로 거점을 확장하고 있습니다.

유럽 시장에서는 탄소 발자국 공개를 의무화하고 재활용 소재 사용 기준을 설정하는 규제가 적용되고 있습니다. 에너지 비용과 인건비가 높기 때문에 유럽의 셀 제조업체들은 중국 제조업체들에 비해 가격이 상당히 비쌉니다. 최근 유럽의 한 대형 제조업체가 파산한 것은 해당 지역의 재무적 위험을 여실히 드러내고 있습니다. 독일에서는 대형 트럭용 충전 인프라에 대한 투자가 활발히 진행되고 있지만, 지게차용 시설은 여전히 제한적입니다. 이러한 부족으로 인해 창고 운영사들은 주도권을 쥐고 자비로 충전기를 도입하고 있습니다.

캘리포니아주의 청정 차량 정책은 북미에서 매우 중요한 원동력이 되고 있습니다. 냉장 창고에서는 저온 환경에서 뛰어난 용량 유지 성능을 장점으로 삼아 LFP 팩의 도입이 확대되고 있습니다. 이러한 전환으로 인해 예비 배터리 세트의 필요성이 줄어들고 있습니다. 관세의 영향으로 중국산 전기 기기의 수입 비용이 크게 상승했습니다. 그 결과, 많은 조립 제조업체들이 공급처를 변경하여 현재는 한국이나 일본의 셀을 선택하고 있습니다. 자본 비용이 높음에도 불구하고, 남미에는 미래가 밝을 것으로 기대되고 있습니다. 브라질의 전자상거래와 아르헨티나의 광업 부문이 리튬 수요의 급증을 주도하고 있습니다. 중동에서는 사우디아라비아의 기존 설비 개보수 프로젝트를 계기로, 극심한 더위와 가혹한 환경 하에서 리튬 배터리의 성능이 주목을 받았습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the forklift battery market size is expected to increase from USD 6.10 billion in 2025 to USD 6.55 billion in 2026 and is forecast to reach USD 9.37 billion by 2031, growing at a CAGR of 7.41% during the forecast period (2026-2031).

This report is Segmented by Battery Type (Lead-Acid, Lithium-Ion, and More), Voltage Capacity (Below 24V, 24V-36V, and More), Application (Warehousing and Distribution, Manufacturing, and More), Sales Channel (Original Equipment Manufacturer (OEM) and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Forklift Battery Market Trends and Insights

Falling Li-ion Costs and TCO Advantage

Average prices for lithium-ion battery packs have significantly declined in recent years, with further reductions expected as advancements in cathode scaling and cell-to-pack integration continue. Lithium-iron-phosphate (LFP) packs, which are considerably cheaper than their nickel-manganese-cobalt counterparts, now dominate a substantial portion of global electric vehicle (EV) battery installations, offering forklift buyers notable economies of scale. By removing the need for watering labor, ventilation equipment, and dedicated battery rooms, operators can achieve significant reductions in total operating costs compared to traditional lead-acid systems. Additionally, regenerative braking in lithium systems recovers a higher percentage of energy than in lead-acid systems, resulting in lower electricity costs, particularly in high-throughput environments. The cost benefits extend beyond the battery packs themselves; for example, transitioning to electric equipment in enclosed operations has demonstrated substantial annual savings, primarily due to reduced ventilation requirements.

E-commerce and Warehouse-Automation Boom

As online retail surges, it's reshaping the distribution landscape. Every increase in e-commerce penetration drives significant demand for additional warehouse space. Modern warehouses, dominated by multi-shift forklift operations, are increasingly turning to lithium-ion batteries. These batteries allow for opportunity charging without the risk of voltage sag. Highlighting the trend, Geekplus' cold-chain automation for JJCL significantly increased storage density and boosted picking efficiency. Such robotic advancements are proving instrumental in hastening the payback period for lithium battery retrofits. The transition from traditional retail stores to specialized fulfillment hubs has greatly increased the distribution space required per sales dollar. This shift has intensified the demand for sealed, maintenance-free battery chemistries. With many shippers now anticipating faster delivery times, the reliance on multi-shift duty cycles has surged. However, lead-acid batteries are struggling to keep pace with this increased demand.

Limited Li-ion Recycling Infrastructure and Liability Risks

Europe's Battery Regulation mandates recycled-content thresholds for cobalt, lithium, and nickel, alongside ambitious collection targets. However, with China dominating global battery recycling, Europe and North America face challenges due to limited local facilities. The lack of closed-loop networks forces operators to export end-of-life packs or landfill them, exposing suppliers to extended producer responsibility liabilities and increased recycling costs. Rising thermal runaway incidents at recycling yards have also driven up insurance premiums, discouraging mid-size fleets from adopting lithium without costly fire-suppression upgrades. Mandatory digital battery passports will require material tracing, adding costs for smaller suppliers without advanced IT systems. Northvolt's Ett plant, which struggled with low utilization before insolvency, highlights the impact of declining lithium prices and high labor costs on Europe's domestic recycling efforts.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Zero-Emission Regulations

- Cold-Chain and 3PL Multi-Shift Demand

- Sparse Fast-Charging Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-acid batteries accounted for 70.21% of the forklift battery market share in 2025, mainly due to entrenched service ecosystems and compatibility with legacy chargers. Still, lithium-ion units are projected to grow at an 8.11% CAGR through 2031, as total ownership costs drop by about 40% below those of lead-acid, especially in multi-shift and cold-storage sites. While solid-state systems are still in the experimental phase, nickel-metal-hydride technology remains a niche player, with pack prices exceeding USD 400/kWh.

The rise of lithium technology is supported by the introduction of user-friendly retrofit kits. For example, BSLBATT launched a drop-in series featuring UL-certified modules compatible with trucks from brands such as Toyota, Hyster, Linde, and Jungheinrich. In contrast, AGM and enhanced-flooded lead-acid variants, like GS Yuasa's YBX9625, offer extended cycle life but cannot match lithium's superior energy density and rapid charging capabilities.

The 24-36V class owned 38.22% of the forklift battery market share in 2025, suitable for single-shift pallet trucks and order pickers. Yet 36-48V solutions will expand at an 8.28% CAGR through 2031. Heavy-duty warehouses are now prioritizing equipment that offers significantly higher torque and faster lifts. Additionally, operating at a higher voltage reduces resistive losses, enabling notable energy recuperation.

Despite substantial conversion costs per truck, cold-chain and food-service fleets remain undeterred, emphasizing the need for reliable low-temperature performance and hygienically sealed housings. The market's gradual shift towards higher voltage is evident in OEM launches, such as EP North America's model featuring a lithium pack and onboard charging.

Geography Analysis

Asia-Pacific captured 46.34% of the forklift battery market share in 2025 and is on course for a 7.89% CAGR through 2031, as China dominates the global lithium-ion cell capacity with a significant share, while India has made substantial commitments to gigafactories . CATL, a major player, supplies a large portion of the world's EV and grid-storage batteries. This dominance allows regional integrators to price forklift packs significantly lower than their Western counterparts. In line with Japan's ambitious goal of carbon neutrality, BSLBATT has strategically opened hubs in key locations .

Europe's market is under the purview of regulations mandating carbon-footprint disclosures and setting recycled-content benchmarks. Due to higher energy and labor costs, European cell manufacturers are considerably pricier than their Chinese counterparts. The recent bankruptcy of a major European manufacturer underscores the financial risks in the region. While Germany invests in charging infrastructure for heavy trucks, facilities for forklifts remain limited. This scarcity has led warehouse operators to take the initiative, self-financing their own chargers.

California's clean fleet policies are pivotal drivers in North America. Cold-storage facilities are increasingly adopting LFP packs, reaping benefits from their superior low-temperature capacity retention. This transition diminishes the need for redundant battery sets. Tariffs led to a notable surge in the landed cost of Chinese electrical gear. Consequently, many assemblers shifted their sourcing, now opting for cells from Korea or Japan. Despite high capital costs, South America shows promise: Brazil's e-commerce and Argentina's mining sectors are driving a burgeoning demand for lithium. In the Middle East, Saudi Arabia's retrofitting initiatives highlighted lithium's capabilities in extreme heat and challenging conditions.

- EnerSys

- East Penn Manufacturing Company

- Exide Industries Ltd.

- GS Yuasa International Ltd.

- Hoppecke

- Crown Equipment Corporation

- Trojan Battery Company, LLC.

- Flux Power

- Amara Raja Batteries Ltd.

- Zhejiang Narada Power Source Co., Ltd

- Saft Groupe SAS

- Storage Battery Systems

- BSL NEW ENERGY TECHNOLOGY CO., LTD

- MIDAC S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce and Warehouse-Automation Boom

- 4.2.2 Falling Li-Ion Costs and TCO Advantage

- 4.2.3 Stricter Zero-Emission Regulations

- 4.2.4 Cold-Chain and 3PL Multi-Shift Demand

- 4.2.5 AI-Enabled BMS For Energy Optimization

- 4.2.6 Battery-as-a-Service Models Lowering Capex

- 4.3 Market Restraints

- 4.3.1 Limited Li-ion Recycling Infrastructure and Liability Risks

- 4.3.2 Sparse Fast-Charging Infrastructure

- 4.3.3 OEM-Warranty Complexity on Retrofits

- 4.3.4 LFP-Cathode Precursor Supply Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Battery Type

- 5.1.1 Lead-Acid Batteries

- 5.1.2 Lithium-Ion Batteries

- 5.1.3 Nickel-Metal Hydride (NiMH)

- 5.1.4 Others (incl. Solid-State)

- 5.2 By Voltage Capacity

- 5.2.1 Below 24V

- 5.2.2 24V - 36V

- 5.2.3 36V - 48V

- 5.2.4 Above 48V

- 5.3 By Application

- 5.3.1 Warehousing and Distribution

- 5.3.2 Manufacturing

- 5.3.3 Construction

- 5.3.4 Mining

- 5.3.5 Retail and Wholesale

- 5.3.6 Others

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 EnerSys

- 6.4.2 East Penn Manufacturing Company

- 6.4.3 Exide Industries Ltd.

- 6.4.4 GS Yuasa International Ltd.

- 6.4.5 Hoppecke

- 6.4.6 Crown Equipment Corporation

- 6.4.7 Trojan Battery Company, LLC.

- 6.4.8 Flux Power

- 6.4.9 Amara Raja Batteries Ltd.

- 6.4.10 Zhejiang Narada Power Source Co., Ltd

- 6.4.11 Saft Groupe SAS

- 6.4.12 Storage Battery Systems

- 6.4.13 BSL NEW ENERGY TECHNOLOGY CO., LTD

- 6.4.14 MIDAC S.p.A.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment