|

시장보고서

상품코드

2061723

프리캐스트 콘크리트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Precast Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

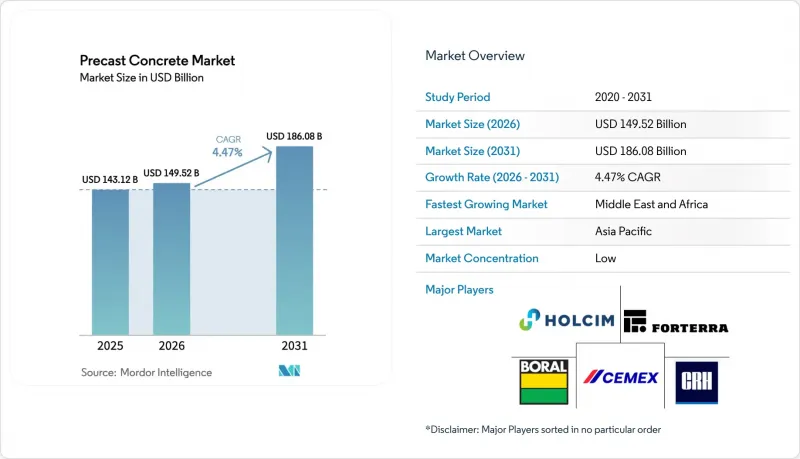

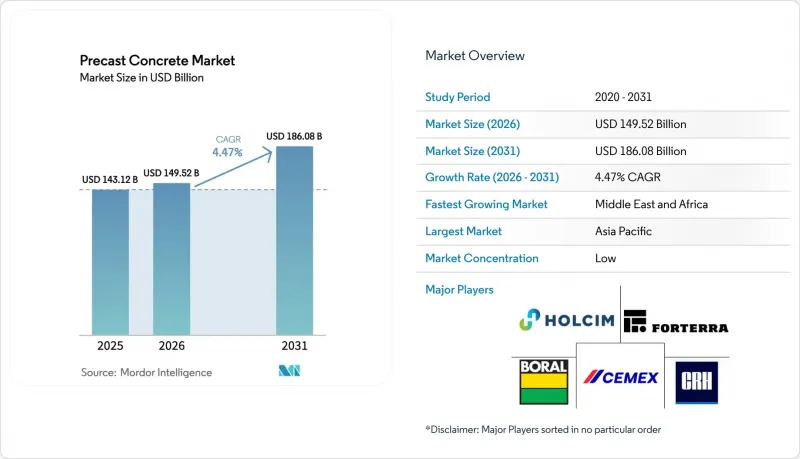

Mordor Intelligence에 의하면, 2026년 프리캐스트 콘크리트 시장 규모는 1,495억 2,000만 달러에 달할 것으로 추정됩니다. 2025년 1,431억 2,000만 달러에서 성장하여 2031년에는 1,860억 8,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 4.47%를 나타낼 것으로 전망됩니다.

본 보고서는 제품 유형(기둥·보, 벽·방호벽, 바닥·지붕, 파이프, 포장 슬래브, 기타), 최종 이용 산업(주택, 상업, 인프라, 산업·공공시설), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 프리캐스트 콘크리트 시장 동향 및 분석

정부 주도의 메가 프로젝트 계획

각국의 인프라 계획은 설계 표준화와 자재 조달 일정을 앞당김으로써 프리캐스트 콘크리트 시장에 예측 가능한 수요를 창출하고 있습니다. 1조 2,000억 달러 규모의 미국 ‘인프라 투자 및 고용법’, 유럽 그린딜의 저탄소 건축 목표, 그리고 중국의 ‘신규 도시 건축물의 30%에 조립식 공법을 채택한다’는 의무화 조치가 모두 맞물려, 수년에 걸친 수요 기반을 뒷받침하고 있습니다. 태즈메이니아주 브리지워터 교량 재건설 공사에서는 현장 타설 공법과 비교해 공사 기간이 40% 단축된 것으로 입증되었습니다. 대규모 조달을 통해 단가가 낮아지고, 프로젝트 간 품질의 일관성이 확보됩니다. 지역 거점 공장과 모듈식 거푸집 시스템을 보유한 공급업체들은 초기 단계의 패키지 계약을 수주하며 선구자로서의 우위를 공고히 하고 있습니다.

신흥국에서의 ‘모두를 위한 주택’ 정책

저렴한 가격의 주택 건설 계획은 프리캐스트 콘크리트 업계의 신속하고 표준화된 공급을 조건으로 보조금 지급을 연계함으로써, 프리캐스트의 채택을 촉진하고 있습니다. 인도의 ‘프라단 만트리 아와스 요자나’는 2,000만 가구를 목표로 하고 있으며, 프리캐스트 벽체, 슬래브, 계단 코어를 사용함으로써 건설 기간이 50% 단축되고 직접 비용이 15% 절감되었다고 보고되고 있습니다(2). 인도네시아는 군도 전역에 이동식 공장을 배치하여, 이동식 배치 플랜트가 지리적 단절을 극복할 수 있음을 입증하고 있습니다. 예측 가능한 생산량 덕분에 자동화된 캐러셀 라인에 투자할 수 있게 되어, 기존 현장에 비해 시간당 생산량이 3배로 증가합니다. 라틴아메리카의 사회주택 담당 부처들은 허리케인 하중 기준을 충족하기 위해 공장 제작 패널의 도입을 점점 더 요구하고 있으며, 이는 비용, 속도, 그리고 재해 대응 능력이라는 목표가 일치하고 있음을 보여줍니다.

초대형 자재의 높은 물류 비용

30미터를 초과하는 거더의 운반은 특히 공장에서 100km 이상 떨어진 장소에서는 납품 자재 비용을 15-25% 가중시킬 가능성이 있습니다(3). 교량의 통행 높이 제한이나 중량 제한으로 인해 우회 경로를 이용할 수밖에 없어, 연료비와 허가 수수료가 증가합니다. 도시 지역의 교통 정체는 크레인 설치 및 도로 통제 요건을 강화하여 허용되는 배송 시간대를 단축시키고, 시간외 수당을 증가시킵니다. 외딴 지역의 건설 현장에서는 선도 차량 비용이 많이 들기 때문에 프리캐스트 콘크리트 업계에서 공장의 생산성 향상으로 얻는 이점을 상쇄해 버리는 경우도 있습니다. 공급업체들은 위성 야드 설치 및 결합 가능한 부문 설계를 통해 위험을 완화하고 있지만, 이동식 거푸집 및 배치 설비에 대한 설비 투자가 단기적인 확장성을 제한하고 있습니다.

부문별 분석

기둥과 보(梁)는 프리캐스트 콘크리트 시장 규모를 지탱하는 핵심 요소로, 2025년에는 36.62%의 점유율을 차지했습니다. 이러한 견조한 수요는 하중 지지 정밀도가 공장 내 통제된 주조 공정을 필요로 하는 고층 빌딩, 교량 및 산업용 구조물에서 비롯된 것입니다. 정부가 주변 보안 기준을 강화하고 모듈식 주택 키트가 보급됨에 따라, 벽 및 방호벽 시장은 2031년까지 연평균 성장률(CAGR) 5.07%를 나타낼 것으로 전망됩니다. 바닥과 지붕은 오픈 플랜에 대한 선호를 배경으로, 현장에서의 가설 공사를 단축하는 장스팬 중공 슬래브의 활용으로 인해 이점을 얻고 있습니다. 배관 부문은 상수도 인프라의 자금 조달 주기와 연동되며, 포장 슬래브는 꾸준한 도로 경관 개선 사업에 기여하고 있습니다.

자동화는 모든 제품 라인을 혁신하고 있습니다. 프리캐스트 콘크리트 업계 전반에서 로봇화 된 철근 케이지를 통해 인력이 40-60% 절감되고, 레이저 투영을 통해 거푸집의 정밀도가 확보되며, 3D 프린팅된 거푸집을 통해 건축물의 질감을 쉽게 맞춤화할 수 있게 되었습니다. 단열재와 배관 공간이 일체화된 벽체 및 칸막이는 단순한 범용 패널에서 턴키 방식의 외피 시스템으로 진화하여, 프리미엄 가격 책정을 뒷받침하고 있습니다. 표준화된 연결 부속품은 현장 조립 속도를 높여, 이러한 속도상의 이점을 부품 설계에 직접 반영하고 있습니다. 지진이 빈번하게 발생하는 지역에서는 연성이 있는 접합부의 상세 설계가 요구되며, 지역별 제품 포트폴리오의 최적화가 더욱 중요해지고 있습니다.

지역별 분석

2025년, 아시아태평양은 프리캐스트 콘크리트 시장의 39.12%를 차지했으며, 중국에서는 신규 도시 프로젝트 전체에 대해 30%의 프리캐스트 적용 비율이 의무화되었고, 인도에서는 저소득층 주택 착공 시 보조금이 지급되었습니다. 지역 제조업체들은 규모의 경제와 현지 시멘트 공급망을 활용하여 베트남과 필리핀으로의 표준화된 거푸집 기술 수출을 추진하고 있습니다. 일본과 한국은 내진 등급의 프리캐스트 프레임 개발을 선도하고 있는 반면, 호주는 연안 인프라를 위해 내구성이 뛰어난 해양용 콘크리트 배합을 도입하고 있습니다.

중동 및 아프리카은 2031년까지 연평균 성장률(CAGR) 4.83%를 기록하며 가장 높은 성장률을 보이고 있습니다. 걸프 연안 국가들의 정부계 펀드는 사우디아라비아의 NEOM과 같은 스마트 시티 플랫폼에 자금을 투자하고 있으며, 해당 프로젝트에서는 단열 효율을 높이기 위해 공장에서 완성된 파사드를 사용하도록 규정하고 있습니다. 카타르 월드컵 건설 프로젝트는 현재 지하철 및 해수 담수화 프로젝트로 재배치된 제조 거점의 여력을 유산으로 남겼습니다. 나이로비나 라고스 등 아프리카의 주요 도시에서는 모듈식 학교와 병원이 시범 도입되고 있지만, 도로 운송 제한과 크레인 부족으로 인해 당분간 확장성은 제한되고 있습니다.

북미와 유럽의 프리캐스트 콘크리트 업계에서는 성숙기에 접어들었음에도 불구하고 혁신 주도형 수요 동향이 나타나고 있습니다. 미국 보험사들의 재해 저항성 할인 제도가 허리케인이 빈번히 발생하는 지역에서의 도입을 촉진하는 한편, 캐나다의 탄소세 도입 일정은 시멘트 사용량이 적은 프리캐스트 혼합물의 도입을 촉진하고 있습니다. 유럽의 입찰 사양서에서는 제조 단계까지의 CO2 배출량(크래들-투-게이트) 공개가 점점 더 중요시되고 있으며, 공급업체들은 클링커 저감 시멘트나 재생 에너지를 활용한 양생 가마의 도입을 요구받고 있습니다. 시장 진출은 진화하는 EN 및 ASTM 규격은 물론, 현지 상황에 맞추어 조정된 환경 제품 선언(EPD) 요건을 충족하는지에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, precast concrete market size in 2026 is estimated at USD 149.52 billion, growing from 2025 value of USD 143.12 billion with 2031 projections showing USD 186.08 billion, growing at 4.47% CAGR over 2026-2031.

This report is Segmented by Product Type (Columns and Beams, Walls and Barriers, Floors and Roofs, Pipes, Paving Slabs, Others), End-Use Industry (Residential, Commercial, Infrastructure, Industrial and Institutional), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Precast Concrete Market Trends and Insights

Government-led Megaproject Pipelines

National infrastructure programs funnel predictable volumes to the precast concrete market by standardizing designs and front-loading component procurement. The USD 1.2 trillion U.S. Infrastructure Investment and Jobs Act, the European Green Deal's low-carbon build targets, and China's mandate that 30% of new urban buildings employ prefabrication collectively underpin a multiyear demand base. Tasmania's Bridgewater Bridge replacement documented a 40% schedule reduction versus cast-in-place options. Scale procurement compresses unit costs and assures cross-project quality consistency. Suppliers with regional hub plants and modular formwork systems capture early-stage package awards, reinforcing first-mover advantages.

Housing-for-All Mandates in Emerging Economies

Affordable-housing blueprints elevate precast adoption by tying subsidy disbursements to rapid, standardized delivery within the precast concrete industry. India's Pradhan Mantri Awas Yojana targets 20 million units and reports 50% faster build cycles plus 15% direct cost savings with precast walls, slabs, and stair cores[2]. Indonesia relocates portable factories across its archipelago, proving that mobile batch plants overcome geographic fragmentation. Predictable volume unlocks investments in automated carousel lines that triple hourly output compared with conventional yards. Latin American social-housing ministries increasingly require factory-molded panels to meet hurricane-load codes, illustrating the alignment between cost, speed, and resilience objectives.

High Logistics Cost of Oversize Elements

Hauling girders longer than 30 meters can add 15-25% to delivered component cost , especially beyond 100 km from the plant[3]. Limited bridge clearances and weight caps force circuitous routes that inflate fuel usage and permit fees. Urban congestion magnifies crane staging and road-closure requirements, compressing allowable delivery windows and raising overtime premiums. Remote project sites endure elevated escort-vehicle expenses, occasionally offsetting factory productivity benefits in the precast concrete industry. Suppliers mitigate exposure by deploying satellite yards or designing splice-ready segments, yet capex for mobile forms and batch setups restrains near-term scalability.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Off-site Manufacturing Amid Skilled-Labor Scarcity

- Embodied-Carbon Credits Monetization

- Competition from Self-Healing In-situ Concretes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Columns and beams anchored the precast concrete market size, accounting for 36.62% share in 2025. Robust demand stems from high-rise, bridge, and industrial frameworks where load-bearing precision necessitates controlled factory casting. Walls and barriers are poised to expand at a 5.07% CAGR to 2031 as governments tighten perimeter-security codes and modular housing kits proliferate. Floors and roofs benefit from open-plan preferences, leveraging long-span hollow-core slabs that cut on-site shoring time. Pipe segments track water-infrastructure funding cycles, while paving slabs serve steady streetscape renewal programs.

Automation reshapes all product lines: robotized cages trim labor by 40-60% across the precast concrete industry; laser projection ensures formwork accuracy, and 3D-printed molds facilitate custom architectural textures. Integrated insulation and conduit chases elevate walls and barriers from commodity panels to turnkey envelope systems, supporting premium pricing. Standardized connection hardware accelerates job-site assembly, embedding speed advantages directly into component design. Earthquake zones demand ductile joint details, reinforcing the regional tailoring of product portfolios.

Geography Analysis

Asia-Pacific held a 39.12% share of the precast concrete market in 2025, with China enforcing 30% prefabrication quotas across new urban projects and India subsidizing low-income housing starts. Regional manufacturers capitalize on scale economies and local cement supplies, driving export of standardized formwork technology to Vietnam and the Philippines. Japan and South Korea pioneer seismic-grade precast frames, while Australia integrates high-durability marine mixes for coastal infrastructure.

The Middle East and Africa register the fastest 4.83% CAGR to 2031. Gulf sovereign wealth funds channel capital into smart-city platforms such as Saudi Arabia's NEOM, which specifies factory-finished facades for thermal efficiency. Qatar's World Cup build-out left a legacy of yard capacity now redeployed for metro and desalination projects. African metros like Nairobi and Lagos trial modular schools and hospitals, yet road-haul limits and crane shortages temper immediate scalability.

North America and Europe exhibit mature yet innovation-driven demand profiles within the precast concrete industry. U.S. insurers' resilience discounts spur uptake in hurricane corridors, while Canada's carbon-tax schedule incentivizes low-cement precast mixes. European tender specifications increasingly weight cradle-to-gate CO2 declarations, pushing suppliers to adopt clinker-reduced cements and renewable-energy curing kilns. Market access hinges on meeting evolving EN and ASTM standards alongside locally calibrated environmental product declarations.

- Balfour Beatty

- Boral Ltd.

- Bouygues Construction

- CEMEX S.A.B. de C.V.

- CRH

- ELO Beton

- Forterra Building Products Limited

- FP McCann

- Gulf Precast

- Holcim

- Larsen & Toubro Limited

- Molins

- Oldcastle Infrastructure Inc.

- Skanska

- The Wells Companies, Inc.

- Tindall Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-led megaproject pipelines

- 4.2.2 Housing-for-All mandates in emerging economies

- 4.2.3 Shift to off-site manufacturing amid skilled-labor scarcity

- 4.2.4 Embodied-carbon credits monetisation

- 4.2.5 Insurance-premium discounts for resilient precast structures

- 4.3 Market Restraints

- 4.3.1 High logistics cost of oversize elements

- 4.3.2 Competition from self-healing in-situ concretes

- 4.3.3 Regional code fragmentation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Columns and Beams

- 5.1.2 Walls and Barriers

- 5.1.3 Floors and Roofs

- 5.1.4 Pipes

- 5.1.5 Paving Slabs

- 5.1.6 Others

- 5.2 By End-use Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Turkey

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Balfour Beatty

- 6.4.2 Boral Ltd.

- 6.4.3 Bouygues Construction

- 6.4.4 CEMEX S.A.B. de C.V.

- 6.4.5 CRH

- 6.4.6 ELO Beton

- 6.4.7 Forterra Building Products Limited

- 6.4.8 FP McCann

- 6.4.9 Gulf Precast

- 6.4.10 Holcim

- 6.4.11 Larsen & Toubro Limited

- 6.4.12 Molins

- 6.4.13 Oldcastle Infrastructure Inc.

- 6.4.14 Skanska

- 6.4.15 The Wells Companies, Inc.

- 6.4.16 Tindall Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment