|

시장보고서

상품코드

2061730

스페인의 맘모그래피 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Mammography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

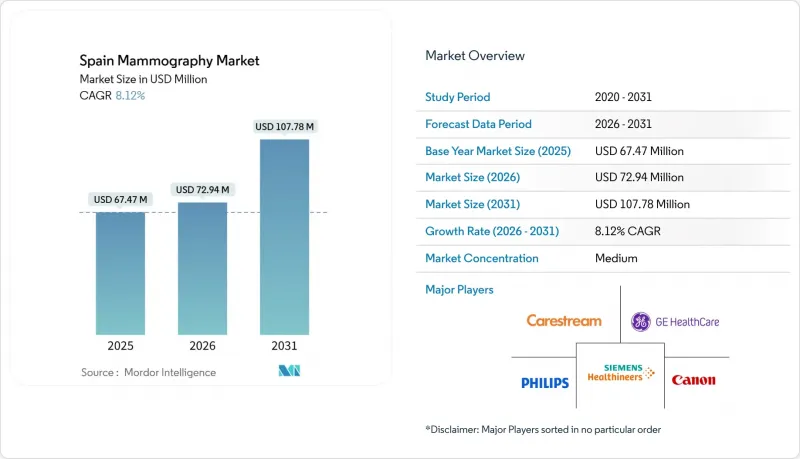

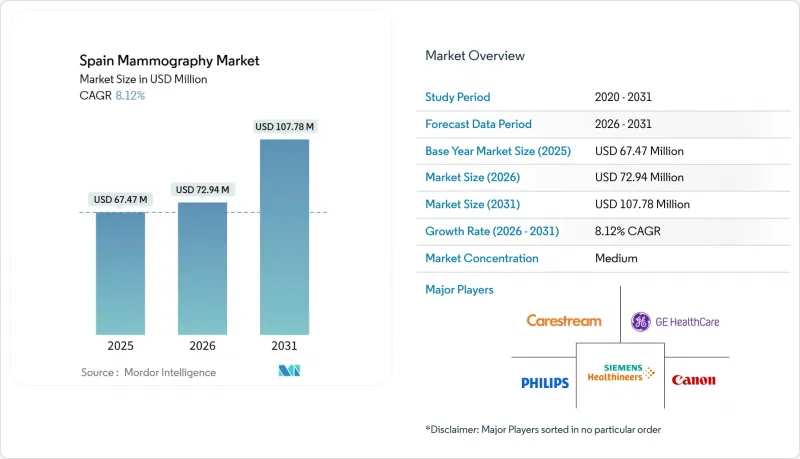

Mordor Intelligence에 의하면, 스페인의 맘모그래피 시장 규모는 2025년에 6,747만 달러로 평가되었습니다. 2026년에 7,294만 달러에 달하고, 2031년까지 1억 778만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.12%를 나타낼 것으로 전망됩니다.

본 보고서는 제품 유형(디지털 시스템, 유방 토모신테시스(3D) 등), 최종 사용자(병원, 진단센터, 전문 클리닉, 이동식 검진 유닛, 유방 영상 진단센터), 기술(2D 맘모그래피, 3D/DBT, AI 지원 CAD, 조영제 강화 디지털 맘모그래피), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

스페인의 맘모그래피 시장 동향 및 분석

40-69세 여성의 유방암 발병률 증가

2024년, 스페인에서는 3만 6,395건의 신규 유방암 진단 사례가 보고되어, 이 나라에서 발병률이 가장 높은 악성 종양이 되었습니다. 카탈루냐 주에서는 지난 10년 동안 환자 수가 16% 증가했습니다. 진단 사례의 대부분은 50-69세 여성에게서 발생하고 있으며, 이는 2년마다 정기 검진을 받는 연령대와 일치합니다. 참여율이 조금만 상승해도 시스템 이용률은 85%를 넘어설 가능성이 있습니다. 검진 대상 연령을 45-74세로 확대할 것을 요구하는 제안 활동이 진행 중이며, 이것이 실현되면 연간 150만 건의 추가 검진이 가능해집니다. 그러나 대기 기간을 30일 이내로 유지하기 위해서는 20-25개의 검사 유닛을 추가로 확보해야 합니다. 10월에 진행된 홍보 캠페인으로 인해 2024년 자발적 검진 건수가 12% 증가하면서, 기존의 아날로그형 플랫폼에 대한 부담이 더욱 커졌습니다. 이러한 요인들이 복합적으로 작용하여, 첨단 디지털 시스템에 대한 수요가 증가하고 있음이 분명해지고 있습니다.

2년마다 실시되는 전국 검진의 확대

스페인의 17개 자치주에서는 50-69세 여성을 대상으로 2년마다 검진을 실시하고 있지만, 참여율은 2017년 83%에서 2020년 74%로 떨어졌습니다. 이는 주로 코로나19와 관련된 혼란 때문인 것으로 보입니다. 5개 자치주에서는 45-49세 및 70-74세 여성에게도 검진 안내를 확대하고 있으며, 이는 향후 EU 지침 개정을 위한 귀중한 참고 자료가 되고 있습니다. 전국 암 감시 시스템을 통한 실시간 추적 조사 결과, 외국 출생 여성이나 농촌 지역 주민의 참여율이 낮은 격차가 드러났습니다. 이러한 격차를 해소하기 위해 이동식 검진차가 도입되었습니다. 예를 들어, 갈리시아 주의 이동식 검진 차량단은 인구 5,000명 미만의 마을에서 검진 대상자 비율을 1년 만에 68%에서 79%로 높였습니다. 마찬가지로, 안달루시아 주의 프로그램에서는 2024년에 4만 2,000명의 여성을 대상으로 검진을 실시하여 연간 15% 증가율을 보였습니다.

방사선과 전문의 부족으로 인해 AI의 검증과 도입이 지연되고 있습니다.

향후 AI 임상시험을 위해서는 방대한 양의 그라운드 트루스(실측 데이터) 라벨링이 필요하지만, 스페인의 방사선과 의사 밀도가 평균보다 낮은 점이 이 과정에 있어 큰 과제로 대두되고 있습니다. 카이론의 Mia 알고리즘은 카탈루냐 주의 3개 병원에서 검출률을 13% 향상시키고, 간격 암을 25% 감소시켰습니다. 그러나 보다 광범위한 도입은 현지 검증 데이터의 확보 여부에 달려 있습니다. 또한, eHealth Network는 현재 국경을 초월한 데이터 교환을 위해 BI-RADS 표준을 준수하는 메타데이터를 요구하고 있어, 대규모 AI 시범 프로젝트를 추진하기 전에 병원의 IT 시스템 업그레이드가 필요합니다.

부문별 분석

2025년, 스페인의 디지털 맘모그래피 시장 규모는 57억 3,400만 달러로 추산되며, 2031년까지 연평균 성장률(CAGR)은 11.50%를 나타낼 것으로 전망됩니다. AMAT-I 기금의 노력 덕분에 저선량 고효율 검출기의 도입이 촉진되고 있으며, 아날로그 시스템에서 디지털 시스템으로의 전환이 가속화되고 있습니다. GE 헬스케어가 최근 우에스카에서 체결한 계약과 같은 장기 서비스 계약은 전환 비용을 높여 기존 업체들의 입지를 공고히 하고 있습니다. 토모신테시스 플랫폼은 30-40%의 가격 프리미엄이 붙지만, 주요 병원들이 보고한 15%의 감도 향상 등을 고려할 때, 해당 장비의 도입 결정은 타당합니다. 그러나 조영제를 이용한 디지털 맘모그래피의 도입은 보험 급여 관련 문제로 인해 여전히 제한적이며, 그 이용은 본인 부담 환자를 대상으로 하는 민간 네트워크로 한정되어 있습니다.

연구 개발(R&D) 활동이 활발해지고 있으며, 평균 유방 피폭 선량을 최대 30%까지 줄일 수 있는 검출기 소재 개발에 주력하고 있는데, 이는 의료 분야의 지속가능성 목표와도 부합합니다. 또한, 각 벤더사는 AI 분류 소프트웨어를 통합하여 의심도가 높은 사례를 우선 처리함으로써 워크플로우를 효율화하고 있으며, 이를 통해 방사선과 전문의는 복잡한 분석에 집중할 수 있게 되었습니다. On-Premise 서버 없이 토모신테시스 데이터 세트를 관리하기 위해 벤더 중립 아카이브(NVA)가 필요한 지역 의료 IT 프로젝트의 추진에 힘입어, 시장에서는 클라우드 지원 플랫폼에 대한 지지가 높아지고 있습니다. 에너지 효율 및 사이버 보안 규정 준수에 연방 자금이 연계되어 있는 만큼, 디지털 시스템은 앞으로도 아날로그 장비를 대체하는 속도를 계속해서 앞지를 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the spain mammography market size is projected to be USD 67.47 million in 2025, USD 72.94 million in 2026, and reach USD 107.78 million by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

This report is Segmented by Product Type (Digital Systems, Breast Tomosynthesis (3-D), and More), End User (Hospitals, Diagnostic Centers, Specialty Clinics, Mobile Screening Units, Breast Imaging Centres), Technology (2-D Mammography, 3-D/DBT, AI-Assisted CAD, Contrast-Enhanced Digital Mammography), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Spain Mammography Market Trends and Insights

Growing Breast-Cancer Incidence in Women 40-69

In 2024, Spain reported 36,395 new breast cancer diagnoses, making it the country's most prevalent malignancy. Catalonia experienced a 16% increase in cases over the past decade. The majority of diagnoses occur among women aged 50-69, aligning with the demographic targeted for biennial screening. Even slight increases in participation can drive system utilization rates beyond 85%. Advocacy efforts are pushing to expand screening age eligibility to 45-74, which could result in an additional 1.5 million screenings annually and require 20-25 more units to maintain wait times under 30 days. Awareness campaigns in October led to a 12% rise in self-referrals in 2024, further straining traditional analog platforms. These factors collectively highlight the growing demand for advanced digital systems.

Expansion of Biennial National Screening

All 17 autonomous communities in Spain invite women aged 50-69 to biennial screenings, but participation rates dropped from 83% in 2017 to 74% in 2020, primarily due to COVID-19-related disruptions. Five regions have extended invitations to women aged 45-49 and 70-74, providing valuable insights for an upcoming EU guideline revision. Real-time tracking by the national Cancer Surveillance System reveals disparities, with foreign-born women and rural residents participating at lower rates. Mobile units are being deployed to address these gaps. For instance, Galicia's mobile fleet increased coverage in towns with fewer than 5,000 residents from 68% to 79% within a year. Similarly, Andalusia's program screened 42,000 women in 2024, reflecting a 15% annual growth.

Radiologist Shortage Delaying AI Validation & Deployment

Prospective AI trials require extensive ground-truth labeling, but Spain's below-average radiologist density poses a significant challenge to this process. Kheiron's Mia algorithm demonstrated a 13% improvement in detection rates and a 25% reduction in interval cancers across three Catalan hospitals. However, broader implementation is contingent on the availability of local validation data. Additionally, the eHealth Network now requires BI-RADS-compliant metadata for cross-border data exchange, necessitating IT system upgrades in hospitals before large-scale AI pilot projects can proceed.

Other drivers and restraints analyzed in the detailed report include:

- Regional Tenders Accelerating 3-D Tomosynthesis Roll-Out

- Shift to Personalized, Risk-Based Screening Models

- Reimbursement Gaps for Tomosynthesis Outside Public Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Spain's digital mammography market was valued at USD 57.34%, with a projected CAGR of 11.50% through 2031. The AMAT-I fund initiatives are driving the adoption of low-dose, energy-efficient detectors, accelerating the shift from analog systems. Long-term service agreements, such as GE HealthCare's recent contract in Huesca, are increasing switching costs and strengthening the position of established players. While tomosynthesis platforms command a 30-40% price premium, procurement decisions are justified by sensitivity improvements, such as a 15% gain reported by leading hospitals. However, contrast-enhanced digital mammography adoption remains limited due to reimbursement challenges, restricting its use to private networks catering to self-pay patients.

Rising R&D efforts are focusing on detector materials that reduce the average glandular dose by up to 30%, aligning with sustainability goals in healthcare. Vendors are also integrating AI-triage software to streamline workflows by prioritizing high-suspicion cases, enabling radiologists to focus on complex analyses. The market increasingly favors cloud-ready platforms, driven by regional health IT projects requiring Vendor-Neutral Archives to manage tomosynthesis datasets without on-premise servers. With federal funding tied to energy efficiency and cybersecurity compliance, digital systems are expected to continue outpacing analog replacements.

List of Companies Covered in this Report:

- Agfa-Gevaert

- Analogic

- Canon Inc. (Canon Medical Systems)

- Carestream Health

- CMR Naviscan Corp.

- ESAOTE SpA

- FUJIFILM

- GE Healthcare

- General Medical Merate

- Hologic

- iCAD Inc.

- IMS Giotto SpA

- Incepto Medical Iberia

- Koninklijke Philips

- Kubtec Medical Imaging

- Metaltronica

- Miwendo Solutions

- Palex Medical

- Planmed

- Samsung Medison Co. Ltd.

- Sectra

- Shimadzu

- Siemens Healthineers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Breast-Cancer Incidence in Women 40-69

- 4.2.2 Expansion of Biennial National Screening

- 4.2.3 Regional Tenders Accelerating 3-D Tomosynthesis Roll-Out

- 4.2.4 Shift to Personalised, Risk-Based Screening Models

- 4.2.5 GDPR-Compliant Cloud PACS Enabling Cross-Facility Teleradiology

- 4.2.6 Hospital Decarbonisation Goals Favouring Low-Dose, Energy-Efficient Detectors

- 4.3 Market Restraints

- 4.3.1 Cumulative-Dose Radiation Anxiety Among Younger Cohorts

- 4.3.2 Reimbursement Gaps for Tomosynthesis Outside Public Programmes

- 4.3.3 Radiologist Shortage Delaying AI Validation & Deployment

- 4.3.4 Litigation Over Interval Cancers Diverting Budgets to MRI

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Digital Systems

- 5.1.2 Breast Tomosynthesis (3-D)

- 5.1.3 Analog Systems

- 5.1.4 Contrast-Enhanced Digital Mammography

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Diagnostic Centers

- 5.2.3 Specialty Clinics

- 5.2.4 Mobile Screening Units

- 5.2.5 Breast Imaging Centres

- 5.3 By Technology

- 5.3.1 2-D Mammography

- 5.3.2 3-D / DBT

- 5.3.3 AI-Assisted CAD

- 5.3.4 Contrast-Enhanced Digital Mammography

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agfa-Gevaert Group

- 6.3.2 Analogic Corporation

- 6.3.3 Canon Inc. (Canon Medical Systems)

- 6.3.4 Carestream Health Inc.

- 6.3.5 CMR Naviscan Corp.

- 6.3.6 ESAOTE SpA

- 6.3.7 Fujifilm Holdings Corporation

- 6.3.8 GE HealthCare

- 6.3.9 General Medical Merate SpA

- 6.3.10 Hologic Inc.

- 6.3.11 iCAD Inc.

- 6.3.12 IMS Giotto SpA

- 6.3.13 Incepto Medical Iberia

- 6.3.14 Koninklijke Philips NV

- 6.3.15 Kubtec Medical Imaging

- 6.3.16 Metaltronica SpA

- 6.3.17 Miwendo Solutions

- 6.3.18 Palex Medical

- 6.3.19 Planmed Oy

- 6.3.20 Samsung Medison Co. Ltd.

- 6.3.21 Sectra AB

- 6.3.22 Shimadzu Corporation

- 6.3.23 Siemens Healthineers AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment