|

시장보고서

상품코드

2061741

모션 컨트롤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Motion Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

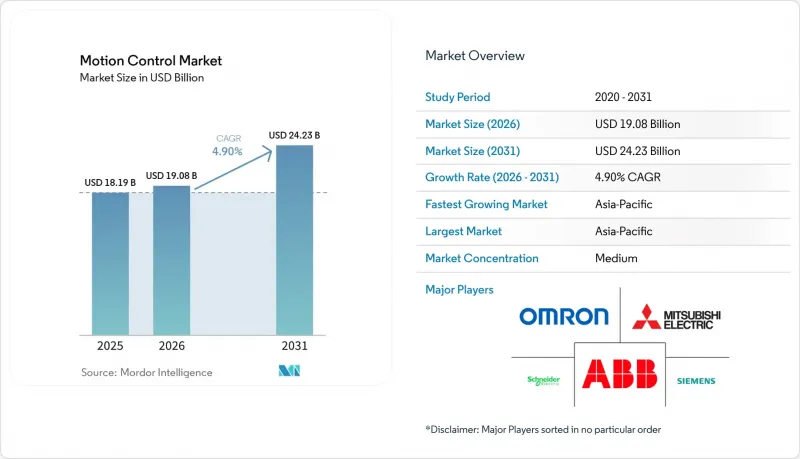

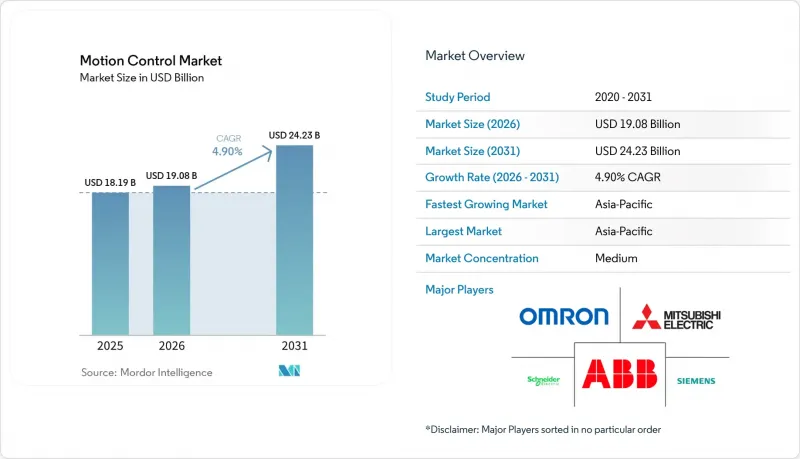

Mordor Intelligence에 의하면, 모션 컨트롤 시장 규모는 2025년 181억 9,000만 달러로 평가되었습니다. 2026년에는 190억 8,000만 달러로 확대되어 2031년까지 242억 3,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 4.90%를 나타낼 전망입니다.

본 보고서는 제품 유형(모터, 드라이브 등), 기술(전기 기계식, 유압식, 공압식), 시스템 유형(개방 루프, 폐쇄 루프), 축 유형(단축, 다축), 용도(자재관리, 포장 등), 최종 사용자 산업(일렉트로믹스 및 반도체, 석유 및 가스 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 모션 컨트롤 시장 동향과 인사이트

스마트 이송 및 기계 통합형 로봇 수요 급증

각 제조업체는 처리 능력 향상과 인력 부족 문제를 해결하기 위해 자율 주행 로봇과 AI 기반 컨베이어를 도입하고 있습니다. 전 세계 로봇 공학 관련 지출은 2025년 717억 8,000만 달러에서 2030년까지 1,508억 4,000만 달러로 증가할 것으로 예상되며, 다축 경로 계획 및 충돌 회피를 관리하는 컨트롤러에 대한 수요가 높아지고 있습니다. 제조업체의 83%가 공장 현장에 생성형 AI를 도입할 계획을 세우고 있는 만큼, 모션 컨트롤용 펌웨어에는 현재 유지보수 일정 설정, 부하 균형 조정, 서보 게인 자동 조정을 수행하는 예측 알고리즘이 탑재되어 있습니다. 이러한 기능 덕분에 스마트 로보틱스는 모션 컨트롤 시장의 주요 성장 동력으로서의 입지를 확고히 하고 있습니다.

분산형 서보 드라이브로의 급속한 전환

제어반에서 모터 측으로 인텔리전스를 이전함으로써 배선량을 최대 86%까지 줄이고, 모션 컨트롤 시장의 전자기 호환성을 향상시킬 수 있습니다. 최첨단 드라이브에는 현재 안전 PLC, 데이터 로깅, 엣지 컴퓨팅이 통합되어 있어 패널 공간을 줄이고 라인의 유연성을 높이고 있습니다. SEW-EURODRIVE사의 MOVIMOT 시리즈(정격 0.37-7.5 kW)는 디지털 모터 인터페이스와 내장형 안전 토크 오프 기능을 갖추고 있어 이러한 변화를 잘 보여주고 있습니다.

희토류 자석 공급 변동으로 인한 가격 급등

네오디뮴 및 디스프로슘의 가격 변동으로 인해 서보 모터의 원가가 최대 25% 상승하여, 고토크 모션 플랫폼의 이익률이 압박받고 있습니다. 공급업체 다각화 프로그램과 페라이트계 모터 연구 개발이 진행 중이지만, 상용화는 예상 시기보다 늦어질 전망입니다.

부문별 분석

2025년 기준으로 모터는 모션 컨트롤 시장의 20.78%를 차지하며, 범용 액추에이터로서의 입지를 확고히 했습니다. 성장의 원동력은 로봇용 소형 서보 모터, 반도체 스테퍼용 고토크 모터, 그리고 의료기기용 프레임리스 모터입니다. 동력 및 위치 제어 사이에 위치한 인텔리전스 계층인 드라이브는 연평균 성장률(CAGR) 6.65%로 가장 빠르게 성장하고 있으며, 진동, 온도, 부하를 실시간으로 분석하는 엣지 컴퓨터로 진화하고 있습니다. 이러한 하드웨어와 소프트웨어의 융합을 통해, 벤더들이 예측 알고리즘을 구독형으로 판매함으로써 서비스 수익이 확대되고 있습니다.

MRI 내부 공간을 이동하는 의료용 로봇의 경우 소형화가 필수적인 반면, 미쓰비시 전기에서 제조한 1,500A HVIGBT와 같은 고출력 모듈은 제철소나 풍력 터빈의 인버터 효율을 향상시킵니다. OEM 업체들이 더 높은 서보 대역폭과 안전 규격에 대응하는 드라이브를 도입하기 위해 기존 생산 라인을 개조함에 따라, 컨트롤러 및 기계 시스템에 대한 수요는 꾸준히 증가하고 있습니다.

2025년에는 전기 기계식 플랫폼이 모션 컨트롤 시장의 60.55%를 차지하며, 깨끗한 작동, 확장 가능한 정밀도, 디지털 트윈과의 손쉬운 통합이 높이 평가되어 시장을 주도했습니다. 탄소 중립 공정으로의 전환과 에너지 비용 절감에 힘입어, 유압식 프레스를 대체하는 서보 전동 프레스의 도입이 가속화되고 있습니다. 압력 센서 및 IO-Link 밸브를 탑재한 공압 솔루션은 정밀도보다 속도가 더 중요한 저하중 픽 앤 플레이스 작업의 요구를 충족시킴으로써 연평균 성장률(CAGR) 6.85%로 성장하고 있습니다.

하이브리드화의 동향은 전동 액추에이터와 비례 유압을 결합하여, 높은 출력을 유지하면서도 에너지 효율이 뛰어난 작동을 실현하고 있습니다. 전기 리니어 액추에이터의 매출액은 자동차 프레스 가공 및 식품 포장 분야에서 지속가능성에 대한 요구를 반영하여, 2022년 205억 달러에서 2032년까지 343억 달러로 증가할 것으로 전망됩니다.

지역별 분석

아시아태평양은 2025년 전 세계 매출의 37.65%를 차지했으며, 이는 중국의 저비용 조립에서 고도화된 자동화 생산으로의 전환과 한국의 사상 최대 규모의 반도체 투자가 주도한 결과입니다. 인도의 생산 연계형 인센티브(PLI) 프로그램은 SMT 라인에 서보 전동식 픽 앤 플레이스 장비를 의무적으로 도입하는 전자 산업 단지의 설립을 촉진하고 있습니다. 지역별 정책 지원, 저렴한 엔지니어 인력, 그리고 임금 상승이 맞물리면서, 많은 공장에서 자동화 투자 비용을 2년 이내에 회수할 수 있게 되었습니다.

북미에서는 리쇼어링(국내 복귀)에 대한 우대 조치와 세액 공제를 활용하여 기존 공장(브라운필드)을 에너지 효율이 높은 구동 장치로 업그레이드하고 있습니다. 미국의 각 OEM 기업들은 OT 네트워크를 겨냥한 랜섬웨어 공격에 대한 관심이 높아짐에 따라, 사이버 보안을 고려한 아키텍처를 중시하고 있습니다. ABB가 1억 달러를 투자한 위스콘신주 캠퍼스는 공급망 단축과 신속한 맞춤형 대응을 목표로 한 투자의 좋은 사례입니다.

유럽에서는 친환경 제조가 우선시되고 있으며, 독일의 자동차 제조업체들은 스코프 1 목표를 달성하기 위해 서보 프레스에 에너지 회생 모듈을 사후 장착하고 있습니다. NIS2 지침에 따라 모션 네트워크에 대한 엄격한 암호화 조치가 도입되면서 일부 프로젝트는 지연되고 있지만, 결국에는 견고한 아키텍처 구축으로 이어지고 있습니다. 특히 이탈리아와 스페인에서는 인구 고령화로 인해 숙련된 노동력이 부족해지고 있어, 협동 로봇의 도입이 활발히 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the motion control market size is expected to increase from USD 18.19 billion in 2025 to USD 19.08 billion in 2026 and reach USD 24.23 billion by 2031, growing at a CAGR of 4.90% over 2026-2031.

This report is Segmented by Product Type (Motors, Drives, and More), Technology (Electromechanical, Hydraulic, Pneumatic), System Type (Open Loop, Closed Loop), Axis Type (Single Axis, Multi-Axis), Application (Material Handling, Packaging, and More), End-User Industry (Electronics and Semiconductor, Oil and Gas, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Motion Control Market Trends and Insights

Surge in Demand for Smart Conveyance and Machine-Integrated Robotics

Manufacturers are deploying autonomous mobile robots and AI-driven conveyors to raise throughput and offset labor shortages. Global robotics spending is projected to climb from USD 71.78 billion in 2025 to USD 150.84 billion by 2030, intensifying the need for controllers that manage multi-axis path planning and collision avoidance. With 83% of producers planning to embed generative AI on the plant floor, motion-control firmware now incorporates predictive algorithms that schedule maintenance, balance loads, and self-tune servo gains. These capabilities position smart robotics as a primary catalyst for the motion control market.

Rapid Transition to Decentralised Servo Drives

Moving intelligence from the cabinet to the motor slashes cabling by up to 86% and improves electromagnetic compatibility in the motion control market. Advanced drives now integrate safety PLC, data logging, and edge computing, cutting panel space and boosting line flexibility. SEW-EURODRIVE's MOVIMOT range, rated 0.37-7.5 kW, illustrates this shift with digital motor interfaces and built-in safe torque off functions.

Price Spikes from Rare-Earth Magnet Supply Volatility

Neodymium and dysprosium price swings have inflated servo motor costs by up to 25%, squeezing margins for high-torque motion platforms. Supplier diversification programs and ferrite-based motor R&D are under way, but commercial roll-out will trail the forecast window.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor Fab Expansions in South Korea and Taiwan

- Electrification of Mobile Hydraulics Upgrading Motion Controllers

- OT-Network Cyber-Security Certification Delays in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Motors held 20.78% of the motion control market in 2025, underscoring their status as universal actuators. Growth stems from compact servomotors for robotics, large torque motors for semiconductor steppers, and frameless motors for medical devices. Drives, the intelligence layer between power and position, are the fastest risers at 6.65% CAGR, evolving into edge computers that analyze vibration, temperature, and load in real time. This hardware-software fusion enlarges service revenues as vendors sell predictive algorithms on subscription.

Miniaturization is critical in medical robots that navigate inside MRI bores, while high-power modules like Mitsubishi Electric's 1,500 A HVIGBT raise inverter efficiency for steel mills and wind turbines. Controllers and mechanical systems enjoy steady demand as OEMs retrofit legacy lines to accommodate higher servo bandwidths and safety-rated drives.

Electromechanical platforms dominated the motion control market with a 60.55% share in 2025, favored for clean operation, scalable precision, and straightforward integration with digital twins. The shift toward net-zero processes and lower utility bills accelerates adoption of servo-electric presses, replacing hydraulic counterparts. Pneumatic solutions, now equipped with pressure sensors and IO-Link valves, are expanding at 6.85% CAGR by satisfying low-force pick-and-place tasks where speed trumps accuracy.

The hybridization trend marries electric actuators with proportional hydraulics, allowing force-dense yet energy-efficient motion. Electric linear actuator revenues are projected to climb from USD 20.5 billion in 2022 to USD 34.3 billion by 2032, mirroring sustainability mandates in automotive stamping and food packaging.

Geography Analysis

Asia Pacific held 37.65% of global revenue in 2025, propelled by China's shift from low-cost assembly to high-automation production and South Korea's record semiconductor outlays. India's Production Linked Incentive program is catalyzing electronics parks that specify servo-electric pick-and-place units in SMT lines. Regional policy support, low-cost engineering talent, and rising wages converge to make automation pay back in under two years for many factories.

North America leverages reshoring incentives and tax credits to upgrade brownfield plants with energy-efficient drives. U.S. OEMs emphasize cyber-secure architectures, a response to high-profile ransomware attacks on OT networks. ABB's USD 100 million Wisconsin campus exemplifies investment aimed at shortening supply chains and supporting quick-turn customization.

Europe prioritizes green manufacturing; German automakers retrofit servo presses with energy-recuperation modules to meet Scope 1 targets. The NIS2 directive introduces strict encryption for motion networks, slowing some projects but ultimately fostering resilient architectures. Collaborative robot adoption is high as demographic aging creates skilled-labor gaps, particularly in Italy and Spain.

- ABB Ltd.

- Siemens AG

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Yaskawa Electric Corporation

- Schneider Electric SE

- Omron Corporation

- Parker Hannifin Corp

- Fanuc Corporation

- Bosch Rexroth AG

- Delta Electronics, Inc.

- Emerson Electric Co.

- Kollmorgen Corporation

- Inovance Technology

- Nidec Corporation

- Novanta Inc.

- Danfoss A/S

- Altra Industrial Motion

- Moog Inc.

- Beckhoff Automation GmbH & Co. KG

- Lenze SE

- Aerotech Inc.

- Allied Motion Technologies Inc.

- NSK Ltd.

- Hiwin Technologies Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for smart conveyance and machine-integrated robotics

- 4.2.2 Rapid transition to decentralised servo drives

- 4.2.3 Semiconductor fab expansions in South Korea and Taiwan

- 4.2.4 Electrification of mobile hydraulics upgrading motion controllers

- 4.2.5 Post-FDA Annex 1 modernisation of pharma fill-finish lines

- 4.2.6 India's PLI-backed electronics clusters accelerating servo demand

- 4.3 Market Restraints

- 4.3.1 Price spikes from rare-earth magnet supply volatility

- 4.3.2 OT-network cyber-security certification delays in Europe

- 4.3.3 IGBT and MCU shortages constraining drive shipments

- 4.3.4 Lack of unified programming standards in South America

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Advancements

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Motors

- 5.1.2 Drives

- 5.1.3 Controllers

- 5.1.4 Actuators and Mechanical Systems

- 5.1.5 Sensors and Feedback Devices

- 5.1.6 Software and Services

- 5.2 By Technology

- 5.2.1 Electromechanical

- 5.2.2 Hydraulic

- 5.2.3 Pneumatic

- 5.3 By System Type

- 5.3.1 Open Loop

- 5.3.2 Closed Loop

- 5.4 By Axis Type

- 5.4.1 Single Axis

- 5.4.2 Multi-Axis

- 5.5 By Application

- 5.5.1 Material Handling

- 5.5.2 Packaging

- 5.5.3 Assembly and Disassembly

- 5.5.4 Inspection and Testing

- 5.5.5 Robotics

- 5.5.6 3D Printing / Additive Manufacturing

- 5.6 By End-user Industry

- 5.6.1 Electronics and Semiconductor

- 5.6.2 Pharmaceutical / Life Sciences / Medical Devices

- 5.6.3 Oil and Gas

- 5.6.4 Metal and Mining

- 5.6.5 Food and Beverage

- 5.6.6 Automotive

- 5.6.7 Aerospace and Defense

- 5.6.8 Logistics and Warehousing

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 Middle East

- 5.7.4.1.1 Israel

- 5.7.4.1.2 Saudi Arabia

- 5.7.4.1.3 United Arab Emirates

- 5.7.4.1.4 Turkey

- 5.7.4.1.5 Rest of Middle East

- 5.7.4.2 Africa

- 5.7.4.2.1 South Africa

- 5.7.4.2.2 Egypt

- 5.7.4.2.3 Rest of Africa

- 5.7.4.1 Middle East

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Mitsubishi Electric Corporation

- 6.4.4 Rockwell Automation, Inc.

- 6.4.5 Yaskawa Electric Corporation

- 6.4.6 Schneider Electric SE

- 6.4.7 Omron Corporation

- 6.4.8 Parker Hannifin Corp

- 6.4.9 Fanuc Corporation

- 6.4.10 Bosch Rexroth AG

- 6.4.11 Delta Electronics, Inc.

- 6.4.12 Emerson Electric Co.

- 6.4.13 Kollmorgen Corporation

- 6.4.14 Inovance Technology

- 6.4.15 Nidec Corporation

- 6.4.16 Novanta Inc.

- 6.4.17 Danfoss A/S

- 6.4.18 Altra Industrial Motion

- 6.4.19 Moog Inc.

- 6.4.20 Beckhoff Automation GmbH & Co. KG

- 6.4.21 Lenze SE

- 6.4.22 Aerotech Inc.

- 6.4.23 Allied Motion Technologies Inc.

- 6.4.24 NSK Ltd.

- 6.4.25 Hiwin Technologies Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment