|

시장보고서

상품코드

2061748

항공우주용 베어링 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aerospace Bearings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

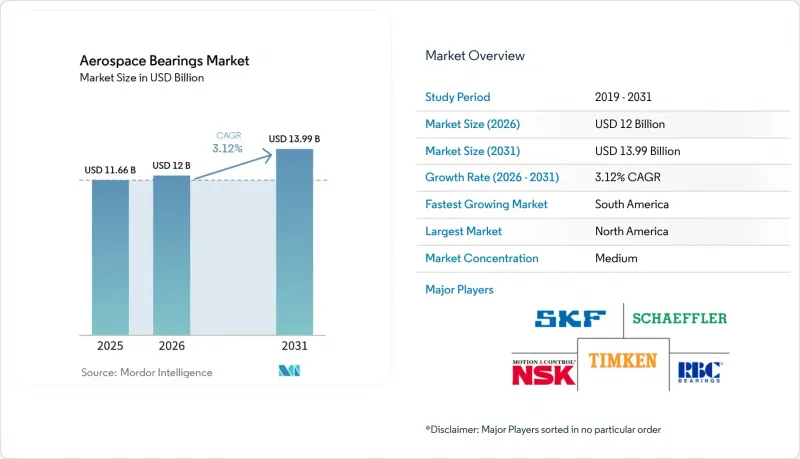

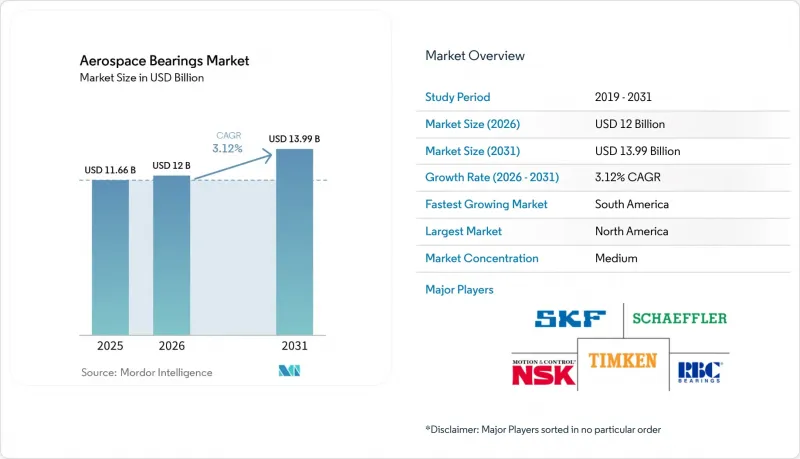

Mordor Intelligence에 의하면, 항공우주용 베어링 시장은 2025년 116억 6,000만 달러로 평가되었습니다. 2026년에는 120억 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 3.12%를 나타내, 2031년까지 139억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형(고정익기, 회전익기 및 무인항공기), 제품 유형(미끄럼 베어링, 롤러 베어링, 볼 베어링, 롤러 나사 및 볼 나사), 용도(엔진, 항공기 구조 부품 등), 재질(금속, 세라믹 등), 판매 채널(OEM 및 애프터마켓), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공우주용 베어링 시장 동향과 인사이트

급증하는 전 세계 민간 항공기 대수

보잉사는 향후 인도될 항공기의 76%가 단일 통로 제트기로 구성될 것으로 전망하고 있으며, 이에 따라 규모의 경제를 뒷받침할 대규모의 표준화된 베어링 수요가 발생할 것입니다. 미결 주문량이 1만 7,000대를 넘어선 가운데, 아시아태평양에 현지 공장을 보유한 OEM 제조업체들은 생산 일정 면에서 유리한 입장에 있습니다. SKF는 이 기회를 활용하기 위해 중국에 4억 스웨덴 크로나(4,222만 달러)를 투자하여 볼 베어링 생산 능력을 확대되고 있습니다. OEM 업체들은 생산 지연의 위험을 감수할 수 없기 때문에 신속한 인증 지원을 제공하는 공급업체가 우선적으로 선정됩니다. 또한, 생산 능력 확대는 조달 결정에 영향을 미치는 국내 조달률에 관한 정부의 규제도 준수해야 합니다.

차세대 프로그램에서의 경량화 요구

실리콘 질화물 제동체는 강철 제동체에 비해 무게가 40% 가벼우며, 더 긴 피로 수명을 실현합니다. 이는 열적 한계에 가까운 상태에서 작동하는 고바이패스비 엔진에게 있어 매우 중요한 장점입니다. NASA는 부식이 발생하기 쉬운 부위를 대상으로, 무게를 줄이면서도 ABEC 등급 10의 공차를 충족하는 니켈·티타늄·하프늄 베어링의 실증 테스트를 수행했습니다. GE 에어로스페이스는 2025년 미국 내 파일럿 라인에 1억 달러 이상을 투자한 후, 세라믹 매트릭스 복합재료의 생산 규모를 확대되고 있습니다. 복합재료로 제작된 케이지는 고온에 견디지만, 수년에 걸친 인증 절차가 필요하기 때문에 시장 출시까지의 기간이 길어지고 있습니다. 인증 절차가 장기화되고 있음에도 불구하고, 항공사들은 연료 소비량 감축을 최우선으로 삼고 있으며, 이것이 수요를 견인하고 있습니다.

특수 합금 및 희토류 가격 변동

지정학적 요인으로 인해 러시아공급 경로가 혼란을 겪으면서 티타늄 가격이 급격히 변동하고 있어, 단조 링과 레이스의 이익률을 압박하고 있습니다. 레늄은 1kg당 1,200-1,800달러 전후로 거래되고 있으며, 와이드바디 항공기 엔진을 구동하는 고온 초합금 제조에 여전히 필수적인 소재입니다. 미국 국방부는 현재 적대국에 대한 의존도를 낮추기 위해 중요 광물의 이중 조달을 의무화하고 있으며, 공급업체들은 조달처의 다각화를 요구받고 있습니다. 각 베어링 제조업체들은 2025년까지 레늄 수요의 30%를 충당할 수 있는 재활용 시스템 구축을 모색하고 있습니다.

부문별 분석

2025년, 항공우주용 베어링 시장 매출의 66.10%를 고정익기가 차지했습니다. 이는 엔진, 착륙 장치 및 제어면을 위한 베어링 부품 번호를 표준화하는 대량 생산형 단일 통로 항공기 프로그램에 기반을 두고 있습니다. 다중 조달 계약은 회복탄력성을 높여주지만, 각 공급업체는 생산 라인에 임베디드되기 전에 엄격한 PPAP 및 AS9100 감사를 통과해야 합니다. 항공우주용 베어링 시장은 북미와 아시아의 최종 조립 라인 간 생산 일정이 조율되고 있는 혜택을 누리고 있으며, 이로 인해 물류 리스크가 감소하고 있습니다.

무인 항공기(UAV) 시장은 군 및 민간 기업들이 ISR(정보·감시·정찰) 및 화물 수송 임무를 위해 장거리 비행이 가능한 드론을 도입함에 따라, 2031년까지 연평균 성장률(CAGR) 9.62%라는 가장 높은 성장세를 보일 것으로 전망됩니다. 이러한 플랫폼에는 고출력 전자기기 주변의 전자기 간섭을 견딜 수 있는 베어링이 필요합니다. UAV 구동 시스템용 항공우주 베어링 시장 규모는 기체 도입이 시제품 단계에서 양산 단계로 넘어감에 따라 꾸준히 확대될 것으로 전망됩니다.

볼 베어링은 2025년에 41.17%의 시장 점유율을 차지했으며, 대부분의 회전 기계에서 레이디얼 하중 및 액시얼 하중에 대한 기본적인 솔루션으로 자리매김하고 있습니다. OEM은 설계 라인을 한 번만 승인하면 되므로, 장기간에 걸친 생산이 가능해져 생산량을 확보할 수 있습니다. 롤러 베어링 시장은 전동화된 비행 제어 액추에이터에 대한 정밀한 직선 운동 수요에 힘입어 연평균 성장률(CAGR) 3.38%를 나타낼 것으로 전망됩니다. 하이브리드 세라믹-스틸 설계는 강성을 유지하면서 경량화를 실현함으로써, 항공우주용 베어링 시장에서 롤러 나사의 전망을 더욱 밝게 하고 있습니다.

미끄럼 베어링은 터보 기계의 고온 영역에서 계속 사용되고 있으며, 한편 테이퍼 롤러 베어링 세트는 착륙 장치의 극심한 충격에 대응하고 있습니다. 적층 가공 기술을 통해 윤활 경로를 최적화한 복잡한 일체형 홀더의 형상이 구현될 것입니다. 항공우주용 베어링 시장에서는 범용 볼 베어링과 용도 특화형 롤러 나사 어셈블리 간의 차별화가 진행되고 있습니다.

지역별 분석

북미는 2025년 매출의 33.15%를 차지했으며, 항공기 생산 증가, 엔진 제조 및 기체 운용 기간 연장에 힘입은 애프터마켓의 성장이 이를 주도했습니다. 이 지역에는 인증을 받은 베어링 공장이 가장 많이 모여 있습니다. GE 에어로스페이스는 2025년에 미국 내 시설에 약 10억 달러를 투자할 계획이며, 세라믹 매트릭스 복합재의 생산량을 확대할 예정입니다.

남미는 가장 빠르게 성장하는 지역이 될 것으로 보이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 3.40%를 기록할 전망입니다. 브라질은 견실한 국내 OEM과 확대되는 공급망에 힘입어 라틴아메리카에서 가장 발전된 항공우주 제조 거점으로 자리매김하고 있습니다. 이 업계는 지역 제트기 분야의 세계적 주요 제조업체이자 비즈니스 항공 분야에서도 중요한 역할을 담당하는 엠브라에르가 주도하고 있습니다. 다른 많은 신흥 시장과 달리, 브라질은 설계, 조립, 통합을 아우르는 종합적인 항공기 제조 역량을 갖추고 있습니다.

항공 수요의 급증과 국내 제조 정책이 아시아태평양의 확장을 뒷받침하고 있습니다. 중국에서는 중국상용항공기(COMAC)가 베어링의 현지 조달을 주도하고 있는 반면, 인도에서는 민간 부문이 전 세계 자산 인수를 통해 역량을 강화하고 있습니다. 일본 기업은 지역 제트기 프로그램에 사용되는 초정밀 레이스를 공급하고 있습니다. 한국과 호주는 지역 내 대대적인 정비 업무를 유치하기 위해 정비 거점을 확대되고 있습니다. 유럽에서는 하이브리드 전기 추진 시스템을 통합한 지속 가능한 항공 프로그램이 추진되고 있으며, 베어링 공급업체들에게 고속 세라믹 설계의 개선이 요구되고 있습니다.

중동에서는 정부계 펀드가 방위 조달 및 산업 상쇄 조치에 자금을 배분하고 있어 완만한 성장이 예상됩니다. 타와준 프리시전 인더스트리즈는 보잉과 제휴하여 아부다비에 베어링 마감 공정을 담당하는 표면 처리 공장을 운영하고 있습니다. 또한 사우디아라비아의 ‘비전 2030’에서는 항공우주 산업을 경제 다각화의 핵심 축 중 하나로 삼고 있어, 지역 내 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the aerospace bearings market is expected to grow from USD 11.66 billion in 2025 to USD 12.00 billion in 2026 and to reach USD 13.99 billion by 2031, at a 3.12% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Fixed-Wing, Rotary-Wing, and UAVs), Product Type (Plain Bearings, Roller Bearings, Ball Bearings, Roller Screws, and Ball Screws), Application (Engine, Aerostructures, and More), Material (Metal, Ceramic, and More), Sales Channel (OEM and Aftermarket), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aerospace Bearings Market Trends and Insights

Surging Global Commercial Aircraft Fleet

Boeing projects that single-aisle jets will form 76% of future deliveries, creating large-volume, standardized bearing requirements that support economies of scale. Order backlogs exceed 17,000 units, giving OEMs with local plants in Asia-Pacific a scheduling advantage. SKF is investing SEK 400 million (USD 42.22 million) in China to boost ball-bearing output to capitalize on this opportunity. Suppliers that offer rapid certification support gain preferred status because OEMs cannot risk production delays. Capacity expansions must also align with government mandates on domestic content, which shape sourcing decisions.

Light-weighting Imperatives in Next-gen Programs

Silicon-nitride rolling elements weigh 40% less than steel and deliver longer fatigue life, a critical benefit for high-bypass engines operating near thermal limits. NASA demonstrated nickel-titanium-hafnium bearings that meet grade 10 ABEC tolerances while cutting weight, targeting corrosion-prone locations. GE Aerospace is scaling ceramic-matrix composites after injecting more than USD 100 million into US pilot lines in 2025. Composite cages resist high temperatures yet require multi-year qualification programs, slowing time-to-market. Despite longer certification cycles, airlines prioritize fuel burn savings, reinforcing demand.

Volatile Specialty Alloy and Rare-earth Prices

Titanium prices swing sharply as geopolitics disrupt Russian supply routes, squeezing margins for forged rings and races. Rhenium trades near USD 1,200-1,800 per kg and remains critical for high-temperature superalloys that power widebody engines. The Pentagon now mandates dual sourcing of critical minerals to cut reliance on adversarial nations, compelling suppliers to diversify procurement. Bearing firms explore recycling loops that could meet 30% of rhenium demand by 2025.

Other drivers and restraints analyzed in the detailed report include:

- Defense Rotorcraft Life-extension Budgets Rising

- Boom in Small-sat and Launch Vehicles

- Lengthy FAA/EASA Certification Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing aircraft contributed 66.10% of the aerospace bearings market revenue in 2025, anchored by high-volume single-aisle programs that standardize bearing part numbers for engines, landing gear, and control surfaces. Multi-sourcing agreements improve resilience, but each supplier must pass stringent PPAP and AS9100 audits before line fitment. The aerospace bearings market benefits from synchronized production schedules across North American and Asian final-assembly lines, which lowers logistics risk.

Unmanned aerial vehicles (UAVs) are projected to post the strongest 9.62% CAGR to 2031 as militaries and commercial operators adopt long-endurance drones for ISR and cargo roles. These platforms need bearings that resist electromagnetic interference around high-power electronics. The aerospace bearings market size for UAV actuation systems is projected to expand steadily as fleets migrate from prototype to mass production.

Ball bearings held a 41.17% share in 2025, remaining the baseline solution for radial and axial loads across most rotating groups. OEMs approve design families once, enabling long production runs that protect volume. Roller bearings are forecast to grow at a 3.38% CAGR, driven by the demand for precise linear motion from electrified flight-control actuators. Hybrid ceramic-steel designs cut weight while maintaining stiffness, strengthening the outlook for roller screws in the aerospace bearings market.

Plain bearings persist in high-temperature zones of turbomachinery, whereas tapered roller sets handle extreme landing-gear shocks. Additive manufacturing will lift complex one-piece bearing-cage geometries that optimize lubrication paths. The aerospace bearings market is seeing greater differentiation between commodity ball bearings and application-specific roller screw assemblies.

Geography Analysis

North America accounted for 33.15% of revenue in 2025, driven by increased aircraft production, engine manufacturing, and a growing aftermarket fueled by extended fleet usage. It is home to the largest pool of certified bearing plants. GE Aerospace plans to invest nearly USD 1 billion in US facilities in 2025, boosting ceramic-matrix composite throughput.

South America will be the fastest-growing region, with a CAGR of 3.40% during 2026-2031. Brazil is the most developed aerospace manufacturing hub in Latin America, supported by a robust domestic OEM and an expanding supplier network. The industry is dominated by Embraer, a leading global producer of regional jets and a significant player in business aviation. Unlike many other emerging markets, Brazil possesses comprehensive aircraft manufacturing capabilities, including design, assembly, and integration.

Rapid growth in air traffic and domestic manufacturing policies are fueling the Asia-Pacific's expansion. In China, local procurement of bearings is spearheaded by COMAC, whereas in India, the private sector is bolstering its capabilities through global asset acquisitions. Japanese firms supply ultra-precision races used in regional jet programs. South Korea and Australia expand maintenance hubs that attract regional overhaul work. Europe advances sustainable aviation programs that integrate hybrid-electric propulsion, pushing bearing suppliers to refine high-speed ceramic designs.

The Middle East is expected to record moderate growth as sovereign funds allocate capital to defense procurement and industrial offsets. Tawazun Precision Industries partners with Boeing to operate a surface-treatment plant that anchors bearing-finishing activities in Abu Dhabi. Moreover, Saudi Arabia's Vision 2030 earmarks aerospace as a pillar of economic diversification, boosting regional demand.

- AST Bearings LLC (Genuine Parts Company)

- The Timken Company

- JTEKT Corporation

- Kaman Corporation

- National Precision Bearing (Mechatronics, Inc.)

- New Hampshire Ball Bearings, Inc.

- UMBRAGROUP S.p.A.

- Thomson Industries, Inc.

- AB SKF

- Schaeffler AG

- NTN Corporation

- RBC Bearings Incorporated

- NSK Ltd.

- Barden Corporation (HQW Aerospace (UK) Ltd.)

- Schatz Bearing Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global commercial aircraft fleet

- 4.2.2 Light-weighting imperatives in next-gen programs

- 4.2.3 Defense rotorcraft life-extension budgets

- 4.2.4 Boom in small-sat and launch vehicles

- 4.2.5 Electrified flight-control actuation demand

- 4.2.6 Advanced air-mobility (eVTOL) proliferation

- 4.3 Market Restraints

- 4.3.1 Volatile specialty alloy and rare-earth prices

- 4.3.2 Lengthy FAA/EASA certification cycles

- 4.3.3 Emergence of magnetic and air-foil bearing tech

- 4.3.4 Aerospace-grade powder supply-chain bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Fixed-wing

- 5.1.2 Rotary-wing

- 5.1.3 Unmanned Aerial Vehicles (UAVs)

- 5.2 By Product Type

- 5.2.1 Plain Bearings

- 5.2.2 Roller Bearings

- 5.2.3 Ball Bearings

- 5.2.4 Roller Screws

- 5.2.5 Ball Screws

- 5.3 By Application

- 5.3.1 Engine

- 5.3.2 Aerostructures

- 5.3.3 Landing Gear

- 5.3.4 Flight Control and Actuation

- 5.3.5 Others

- 5.4 By Material

- 5.4.1 Metal

- 5.4.2 Ceramic

- 5.4.3 Metal-Polymer and Engineered Plastics

- 5.4.4 Fiber-Reinforced Composites

- 5.5 By Sales Channel

- 5.5.1 Original Equipment Manufacturer (OEM)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 Egypt

- 5.6.5.2.2 South Africa

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AST Bearings LLC (Genuine Parts Company)

- 6.4.2 The Timken Company

- 6.4.3 JTEKT Corporation

- 6.4.4 Kaman Corporation

- 6.4.5 National Precision Bearing (Mechatronics, Inc.)

- 6.4.6 New Hampshire Ball Bearings, Inc.

- 6.4.7 UMBRAGROUP S.p.A.

- 6.4.8 Thomson Industries, Inc.

- 6.4.9 AB SKF

- 6.4.10 Schaeffler AG

- 6.4.11 NTN Corporation

- 6.4.12 RBC Bearings Incorporated

- 6.4.13 NSK Ltd.

- 6.4.14 Barden Corporation (HQW Aerospace (UK) Ltd.)

- 6.4.15 Schatz Bearing Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment