|

시장보고서

상품코드

2061763

중국의 히트펌프 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

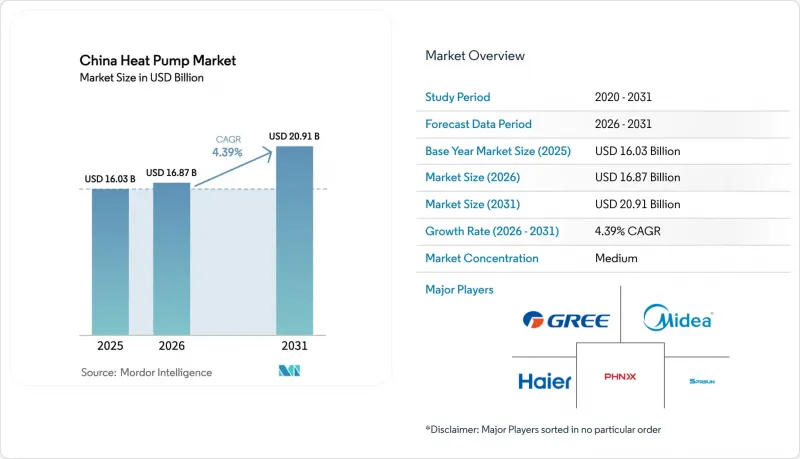

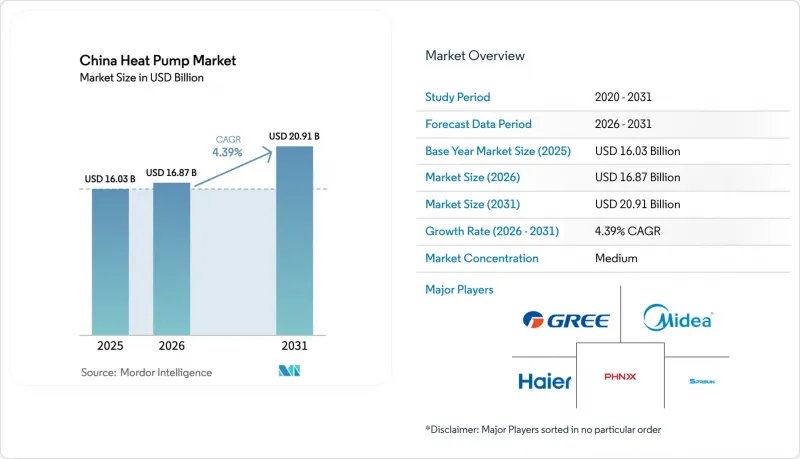

Mordor Intelligence에 의하면, 중국의 히트펌프 시장 규모는 2025년에 160억 3,000만 달러로 평가되었습니다. 2026년에 168억 7,000만 달러에 달하고, 2031년까지 209억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 4.39%를 나타낼 전망입니다.

본 보고서는 공급원 유형(공기원, 수원 등), 기술(공기-공기, 공기-물 등), 용량(10kW 미만, 10-50kW 등), 용도(공간 난방, 산업·공정 가열 등), 최종 사용자(주택, 상업시설 등), 설치 형태(신규 설치, 개조), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 히트펌프 시장 동향과 인사이트

기존의 냉난방 용도를 넘어선 히트펌프의 활용 확대

200°C 미만의 산업 공정 열은 중국 히트펌프 시장에서 규모는 크지만 아직 충분히 활용되지 않은 기회이며, 섬유, 식품, 석유화학 분야의 선구자들은 많은 증기 공정에서 3을 초과하는 성능 계수(COP)를 입증하고 있습니다. 석탄 화력 발전소 및 공항의 폐열 회수 설비는 기존 보일러에 비해 연료 사용량을 3분의 2로 줄이는 메가와트급 시스템을 자랑합니다. 청두의 데이터센터 열 활용 프로젝트에서는 서버에서 발생하는 폐열과 인근 상업시설의 부하를 실시간으로 조정하여, 연간 약 8킬로톤의 표준 석탄 소비량을 절감하고 있습니다. 이러한 시범 사업의 성공으로 인해, 그동안 전력 가격과 가스 가격의 변동에 회의적이었던 산업 분야 최종 소비자들에게 투자 실현 가능성이 높아지고 있습니다. 고온용 압축기가 시장 출시 준비 단계에 접어든 가운데, 165℃ 용도를 위한 기술적 여지는 향후 10년 동안 수십억 달러 규모의 추가적인 시장 기회를 창출할 것으로 보입니다.

에너지 효율이 높은 냉난방 시스템의 보급을 촉진하기 위한 정부 정책 및 인센티브 시행

2025년 5월의 가정용 가전 행동 계획은 초기 비용의 최대 30%를 지원하는 보조금 제도를 핵심으로 하고 있으며, 베이징, 허베이, 허난에서는 투자 회수 기간을 5년 미만으로 단축하고 있습니다. 트레이드인 프로그램은 소비자들의 관심을 전기 저항 히터에서 돌리게 하는 한편, 건축기준법 GB 55015는 대규모 신축 건축물에 대해 재생에너지를 통한 열 공급 비율을 10% 이상으로 할 것을 의무화하고 있습니다. 에너지 서비스 기업들은 이러한 인센티브를 활용하여 ‘열 공급 서비스(Heat-as-a-Service)’ 계약을 확대하고, 건물 소유주의 설비 투자 부담을 줄이고 있습니다. 또한 각 부처는 계절별 성능 계수의 기준치에 따라 리베이트 수준을 차등 적용하고 있으며, 제조업체들이 기준 효율을 초과하도록 독려하고 있습니다. 이러한 ‘당근과 채찍’ 방식의 정책들이 맞물려 지속적인 수요를 창출하며, 중국의 히트펌프 시장의 예상되는 성장을 뒷받침하고 있습니다.

높은 초기 설치 비용과 건물 개조의 복잡성

주거용 공기-물 열교환 시스템의 초기 비용은 가스 보일러의 3배에서 6배에 달하며, 여기에 외벽이나 전기 설비 개보수 비용이 20-40% 추가될 수 있습니다. 리모델링 프로젝트에서는 낮은 공급 온도에 대응하기 위해 라디에이터 교체가 필요한 경우가 많아, 공사 기간이 길어지면서 거주자들에게 불편을 끼치게 됩니다. 정부 보조금 이외의 자금 조달은 여전히 어려운 실정이며, 많은 지방 주택의 경우 투자 회수 기간이 8년 이상에 달하고 있습니다. 오래된 오피스 빌딩의 경우, 새로운 히트펌프 루프를 구식 냉수 인프라에 통합하기 위해 맞춤형 설계가 필요해지면서 리스크 프리미엄이 급등하고 있습니다. 이러한 경제적·기술적 마찰이, 본래라면 호조를 보이며 성장 궤도에 올라 있었을 중국의 히트펌프 시장의 발목을 잡고 있습니다.

부문별 분석

2025년, 중국의 히트펌프 시장 점유율의 68.78%를 공기원 히트펌프가 차지했습니다. 이는 개발업자가 초기 비용이 저렴하고, 옥상 설치에 적합하며, 인허가 절차의 장벽이 낮다는 점을 높이 평가했기 때문입니다. 수자원 유닛은 여전히 소수이지만, 지역 난방 사업자나 산업단지가 사계절 내내 안정적인 수온을 제공하는 하천, 대수층 또는 배수로를 활용할 수 있기 때문에 2031년까지 연평균 성장률(CAGR) 5.26%를 나타낼 것으로 전망됩니다. 공기 루프와 지하 루프를 결합한 하이브리드 시스템은 극한의 추위로 인해 공기 열원의 효율이 떨어지고 전력망에 가해지는 부하가 커질 우려가 있는 북부 주에서 지지를 얻고 있습니다. 이는 외기 온도 -19℃ 조건에서 COP 3.64를 달성한 93만 제곱미터 규모의 싱타이 렌제 프로젝트가 증명하고 있습니다. 정책 입안자들은 이러한 하이브리드 구조를 모범 사례로 주목하기 시작했으며, 이는 단일 열원 설계에서 벗어나는 과정을 가속화하는 규제 측면의 호재가 될 가능성이 있습니다.

지역 열공급 사업자 역시 공간 난방과 온수 공급을 동시에 수행할 수 있게 해주는 심정수 루프의 시범 운영을 진행하고 있으며, 이를 통해 최대 부하 운전 시간을 늘려 계절에 따른 수익 변동을 완화하고 있습니다. 톈진과 허베이에서 중국석유화학(Sinopec)의 지열 사업 포트폴리오는 이미 1억 2,000만 m² 이상을 차지하고 있으며, 수원 히트펌프를 통합한 후의 계절 성능 계수는 4.0을 초과합니다. 지방 당국은 보조금 연장을 정당화하기 위해 이러한 지표를 강조하고 있으며, 그로 인해 수자원 기술의 상업적 매력이 높아지고 있습니다. 지하수 취수 허가 취득은 여전히 어려운 상황이지만, 우물 인프라의 긴 가동 수명은 사업자의 투자 기간과 일치하여 중국 히트펌프 시장의 꾸준한 보급을 뒷받침하고 있습니다.

2025년, 중국의 히트펌프 시장에서 공기-물형 플랫폼이 46.59%의 점유율을 차지했습니다. 이는 4세대 지역 열공급 네트워크가 해당 설비의 최적 운전 범위인 35-45℃공급 온도에서 가동되는 사례가 증가하고 있기 때문입니다. 허베이성 자오현에서 진행된 430만 m² 규모의 프로젝트에서 집약형 공기-물형 어레이가 도시 쾌적성 기준을 충족하면서 석탄 보일러를 대체할 수 있음이 입증되었습니다. 수-수식 히트펌프는 안정적인 지열 및 산업 폐열원을 활용하여 COP 5 이상을 실현합니다. 특히 섬유 및 식품 산업단지에서는 냉난방을 동시에 사용함으로써 공정의 경제성이 향상됩니다. 지중-수식 유닛은 굴착 비용과 지하수 규제로 인해 프로젝트의 복잡성이 증가하기 때문에 여전히 틈새 시장으로 남아 있지만, 열교환기의 수명이 50년에 달하고 외기 온도 변동의 영향을 받지 않는다는 점 때문에 대학이나 병원에서 도입이 확대되고 있습니다.

남부 지방에서는 물 순환 배관이 갖춰지지 않은 냉방 위주의 기후 조건에서 여전히 공기 대 공기 히트펌프가 선호되고 있습니다. 그러나 정책적 인센티브에 따라, 향후 개보수 시 바닥 난방이 추가될 경우 공기-물 시스템으로 업그레이드할 수 있도록 개발업체에 듀얼 코일 채택을 권장하고 있습니다. 수-수식 히트펌프의 보급은 냉수와 온수를 동시에 생산하도록 장려하는 정부의 보조금에 힘입어 확대되고 있으며, 이로 인해 자산의 연간 이용률이 향상되고 있습니다. 중국의 히트펌프 시장이 확대됨에 따라, 각 제조업체들은 요금 시간대나 실외 조건에 따라 건물이 공기, 물, 지중 열원 사이를 동적으로 전환할 수 있는 스마트 제어 기능을 추가하고 있습니다. 이러한 제어 기술의 고도화는 계절 성능 계수를 향상시키고, 멀티 소스 기술 스택의 가치 제안을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the china heat pump market size is projected to be USD 16.03 billion in 2025, USD 16.87 billion in 2026, and reach USD 20.91 billion by 2031, growing at a CAGR of 4.39% from 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China Heat Pump Market Trends and Insights

Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

Industrial process heat below 200 °C represents a sizeable but under-served opportunity for the China heat pump market, and first movers in textiles, food, and petrochemicals now validate coefficients of performance that exceed 3 for many steam processes. Waste-heat-recovery installations at coal-fired units and airports showcase megawatt-scale systems that trim fuel use by two-thirds versus legacy boilers. Data-center coupling projects in Chengdu demonstrate real-time balancing of server waste heat with nearby commercial loads, cutting standard-coal consumption by almost 8 kilotonnes annually. Successful pilots accelerate bankability for industrial end users that were historically skeptical of electricity-to-gas price volatility. As high-temperature compressors reach market readiness, technical headroom for 165 °C applications offers an incremental addressable market worth billions over the next decade.

Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems

The May 2025 household-appliance action plan anchors subsidy streams that reimburse up to 30% of upfront costs, slashing payback periods below five years in Beijing, Hebei, and Henan. Trade-in programs direct consumer attention away from electric resistance heaters, while GB 55015 building codes mandate renewable thermal inputs above 10% for large new construction. Energy service companies harness these incentives to roll out heat-as-a-service contracts, freeing building owners from capital budgeting. Provinces also differentiate rebate levels by seasonal performance factor thresholds, nudging manufacturers to surpass baseline efficiency. Together, these carrots and sticks channel sustained demand that underpins the projected expansion of the China heat pump market.

High Upfront Installation Cost and Building Retrofit Complexity

Residential air-to-water systems cost three to six times more than gas boilers on a first-cost basis, and extra envelope or electrical upgrades can add another 20-40%. Retrofit projects must often replace radiators to accommodate lower supply temperatures, stretching construction timetables and disrupting occupants. Financing remains scarce outside provincial subsidies, pushing payback periods above eight years for many rural homes. Older office towers face bespoke engineering to merge new heat-pump loops with vintage chilled-water infrastructure, inflating risk premiums. These economic and technical frictions drag on the otherwise favorable growth trajectory of the China heat pump market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Construction of New Buildings

- Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors

- Limited Public Awareness and Certified Installer Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air source heat pumps controlled 68.78% of the China heat pump market share in 2025 as developers favored their lower upfront cost, rooftop compatibility, and limited permitting hurdles. Water source units, though still a minority, are projected to grow at a 5.26% CAGR through 2031 because district-heating companies and industrial parks can tap rivers, aquifers, or wastewater streams that deliver seasonally stable temperatures. Hybrid systems that couple air and ground loops are gaining favor in northern provinces where extreme cold can curb air source efficiency and raise grid stress, as evidenced by the 930,000 m2 Xingtai Renze scheme that achieved a 3.64 COP under -19 °C ambient conditions. Policymakers have begun spotlighting these hybrid architectures as model cases, signaling regulatory tailwinds that could accelerate diversification away from single-source designs.

District heating utilities are also trialing deep-well water source loops that allow simultaneous space heating and hot-water production, boosting full-load hours and flattening seasonal revenue volatility. In Tianjin and Hebei, Sinopec's geothermal portfolio already covers more than 120 million m2, with seasonal performance factors above 4.0 after water source heat pump integration. Local officials tout these metrics to justify subsidy extensions, thereby enhancing the commercial appeal of water source technology. Although permitting for groundwater extraction remains stringent, the long operational life of well infrastructure aligns with utility investment horizons and supports steady uptake within the China heat pump market.

Air-to-water platforms held 46.59% of the China heat pump market share in 2025 because fourth-generation district networks increasingly run at 35-45 °C supply temperatures that match these units' optimal operating range. Hebei Zhaoxian's 4.3 million m2 project validated that clustered air-to-water arrays can displace coal boilers while meeting municipal comfort standards. Water-to-water machines leverage stable geothermal or industrial waste-heat sources to deliver COPs above 5, especially in textile and food parks where simultaneous chilling and heating improve process economics. Ground-to-water units remain niche because drilling costs and groundwater regulations elevate project complexity, but universities and hospitals adopt them for their 50-year exchanger lifespan and immunity to outdoor temperature swings.

Southern provinces still prefer air-to-air heat pumps for cooling-led climates that lack hydronic distribution, yet policy incentives are nudging developers to specify dual coils so systems can upgrade to air-to-water when future retrofits add radiant flooring. Water-to-water penetration is aided by national subsidies that reward simultaneous production of chilled and hot water, improving annualized asset utilization. As the China heat pump market size grows, manufacturers are adding smart controls that let buildings switch dynamically among air, water, and ground sources based on tariff windows and outdoor conditions. This control sophistication boosts seasonal performance factors and reinforces the value proposition of multi-source technology stacks.

List of Companies Covered in this Report:

- Ariston Holding N.V.

- Carrier Global Corporation

- Daikin Industries, Ltd.

- Fujitsu General Limited

- Glen Dimplex Group

- Haier Group Corporation

- Johnson Controls-Hitachi Air Conditioning

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- NIBE Industrier AB

- Panasonic Corporation

- PHNIX Eco-Energy Solution Ltd.

- Robert Bosch GmbH (Bosch Thermotechnology)

- Sanden Corporation

- Stiebel Eltron GmbH and Co. KG

- Thermia Heat Pumps

- Trane Technologies plc

- Vaillant Group

- Viessmann Group

- WaterFurnace International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Use of Heat Pumps Beyond Traditional Heating and Cooling Applications

- 4.2.2 Implementation of Government Policies and Incentives to Promote Energy-Efficient Heating and Cooling Systems

- 4.2.3 Rapid Urbanization and Construction of New Buildings

- 4.2.4 Surge in Cold-Climate Air-Source Heat Pump Deployments Enabled by -35 °C Rated Compressors

- 4.2.5 Expansion of Rural Subsidies Replacing Coal Stoves with Heat Pumps

- 4.2.6 Integration of Heat Pumps with Rooftop PV and Time-of-Use Tariffs Driving Self-Consumption

- 4.3 Market Restraints

- 4.3.1 High Upfront Installation Cost and Building Retrofit Complexity

- 4.3.2 Limited Public Awareness and Certified Installer Shortage

- 4.3.3 Winter Peak-Load Constraints on Rural Distribution Grids

- 4.3.4 Uncertainty in Long-Term Electricity-to-Gas Price Ratios Affecting Industrial Adoption

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ariston Holding N.V.

- 6.4.2 Carrier Global Corporation

- 6.4.3 Daikin Industries, Ltd.

- 6.4.4 Fujitsu General Limited

- 6.4.5 Glen Dimplex Group

- 6.4.6 Haier Group Corporation

- 6.4.7 Johnson Controls-Hitachi Air Conditioning

- 6.4.8 LG Electronics Inc.

- 6.4.9 Mitsubishi Electric Corporation

- 6.4.10 NIBE Industrier AB

- 6.4.11 Panasonic Corporation

- 6.4.12 PHNIX Eco-Energy Solution Ltd.

- 6.4.13 Robert Bosch GmbH (Bosch Thermotechnology)

- 6.4.14 Sanden Corporation

- 6.4.15 Stiebel Eltron GmbH and Co. KG

- 6.4.16 Thermia Heat Pumps

- 6.4.17 Trane Technologies plc

- 6.4.18 Vaillant Group

- 6.4.19 Viessmann Group

- 6.4.20 WaterFurnace International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment