|

시장보고서

상품코드

2061769

산업용 NOR 플래시 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

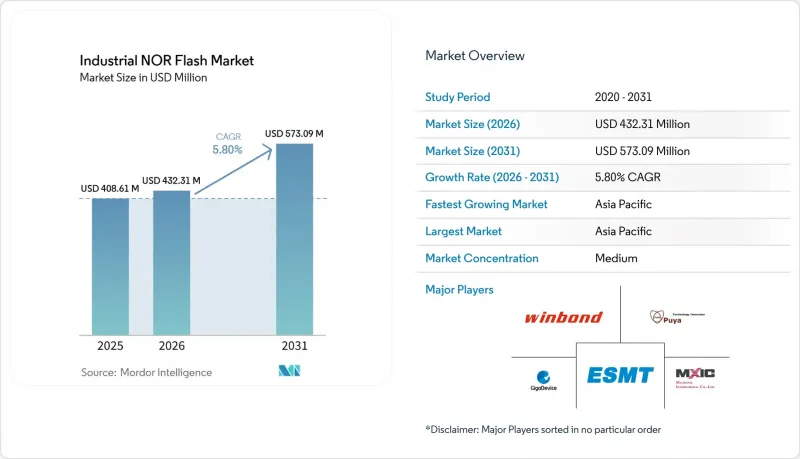

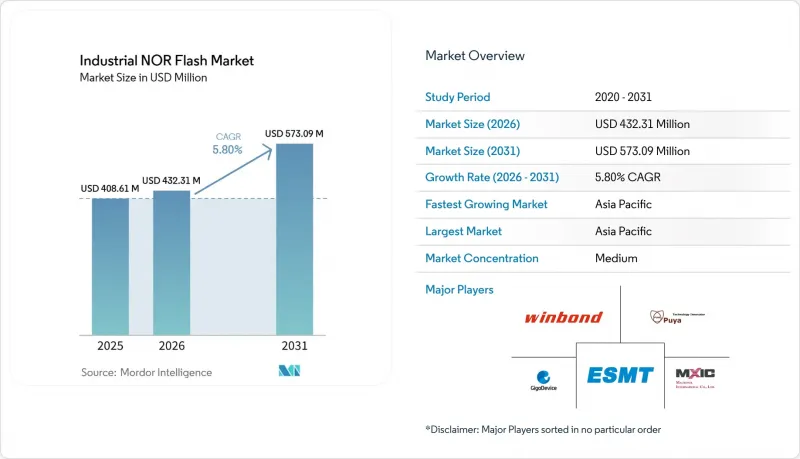

Mordor Intelligence에 의하면, 산업용 NOR 플래시 시장 규모는 2025년 4억 861만 달러로 평가되었습니다. 2026년에는 4억 3,231만 달러로 확대되어 2031년까지 5억 7,309만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 5.80%를 나타낼 전망입니다.

본 보고서는 NOR 플래시의 유형(직렬, 병렬), 인터페이스(SPI 싱글/듀얼 등), 용량(2메가비트 이하 등), 전압(3V급, 1.8V급 등), 공정 기술 노드(65nm, 45nm 등), 패키지 유형(WLCSP/CSP 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(개) 단위로 제공됩니다.

세계의 산업용 NOR 플래시 시장 동향 및 분석

쿼드 및 옥탈 SPI를 채택하여 IoT 에지에서의 처리량 향상을 실현

쿼드 SPI는 이미 코드 스토리지 소켓의 광범위한 도입 기반을 지원하고 있으며, 옥탈 SPI 및 xSPI로의 전환을 통해 더 빠른 부팅 및 실행 성능이 필요한 엣지 플랫폼에서 지속적 읽기 대역폭이 400 MB/s로 향상되었습니다. GigaDevice는 2025년 11월, 1.8V 코어 및 1.2V I/O 설계를 채택한 GD25NX 시리즈를 출시했습니다. 이 회사에 따르면, 이 제품은 200MHz 더블 전송 속도 모드에서 기존의 1.8V 옥탈 플래시와 비교해 프로그래밍 속도가 30% 빨라지고, 삭제 시간이 10% 단축되었다고 합니다. 산업용 NOR 플래시 시장에서 이러한 변화는 중요한 의미를 지닙니다. 많은 AI 에지 노드에서 펌웨어 이미지의 용량이 커짐에 따라, 저장 용량보다 대역폭이 설계상의 병목 현상으로 부각되고 있기 때문입니다. xSPI 지원과 인플레이스 실행 기능을 결합한 벤더들은 그동안 응답 시간을 낮게 유지하기 위해 외부 SRAM에 의존하던 용도으로 NOR 플래시의 적용 범위를 확대되고 있습니다. 이로 인해 플랫폼 인증 기간이 단축되어, 산업용 NOR 플래시 시장에서 이미 고속 제품군에 대한 인증을 획득한 공급업체들에게 경쟁 우위가 생기고 있습니다.

중국의 55nm 및 40nm 국산 공정, 공급 균형 재조정

중국은 대만 및 미국과 관련된 공급원에 대한 의존도를 낮추는 것을 목표로, 55nm 및 40nm 공정의 현지 생산을 확대함으로써 산업용 NOR 플래시 시장공급 구조를 재편하고 있습니다. 우한 XMC는 2024년 9월 상하이 STAR 시장에 상장 신청을 접수했으며, 이 회사는 40nm 이상의 NOR 플래시용 파운드리 서비스를 제공합니다. 기가디바이스(GigaDevice)와 푸야(Puya) 역시 국내 공급처를 확대하고 있으며, 이에 따라 표준 및 중밀도 제품에 대한 현지 조달 전략의 중요성이 커지고 있습니다. 이러한 생산 체제의 확충은 단순히 수입품의 대체 수단이 될 뿐만 아니라, 프리미엄 부문보다 일반 상품 부문에서 더욱 치열한 가격 경쟁 환경을 조성하고 있습니다. 따라서 산업용 NOR 플래시 시장은 가격 중심의 국내 공급과, 안전 및 보안 및 오랜 설계 실적이 가격 그 자체보다 여전히 더 중요하게 여겨지는 인증 중심의 프리미엄 공급 사이에서 더욱 명확하게 양분되고 있습니다.

NAND에 대한 비용 프리미엄이 고밀도 영역에서의 채택을 제약하고 있습니다.

산업용 NOR 플래시 시장은 밀도 요구 사항이 256Mb를 초과할 경우, 여전히 NAND에 비해 비트당 비용 측면에서 구조적으로 불리한 입장에 있어, 고속 랜덤 읽기 액세스보다 스토리지의 경제성이 중시되는 설계에서의 채택을 제한하고 있습니다. 또한, 2D NOR의 로드맵은 45nm 이후에도 여전히 난항을 겪고 있으며, 의미 있는 밀도 향상을 위해서는 아직 양산 단계와는 거리가 먼, 더욱 정교한 구조가 필요합니다. 마크로닉스는 2026년, 공급 제약이 있는 중밀도 NOR 및 eMMC 제품에 자원을 집중하기 위해 3D NOR 개발 프로그램을 약 2년 연기했습니다. 이 결정은 장기적인 확장 투자와 이미 공급 제약이 있는 부문에서의 단기적인 수익 기회 사이의 상충 관계를 여실히 보여주고 있습니다. 그 결과, 산업용 NOR 플래시 시장은 양극화되어 있으며, 인프라, 산업, 자동차 분야에서는 128-512Mb 제품이 지속적으로 성장하고 있는 반면, NAND가 더 저렴한 대체재이기 때문에 저용량 소비자용 제품의 판매량을 늘리는 것은 어려워지고 있습니다.

부문별 분석

시리얼 NOR 플래시는 2025년 산업용 NOR 플래시 시장 규모의 66.1%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.7%를 나타낼 것으로 전망됩니다. 이러한 장점은 현재의 IoT 및 자동차용 SoC가 전용 메모리 버스가 필요 없고 ‘execute-in-place’를 지원하는 핀 수가 적은 직렬 인터페이스를 선호하는 경향을 반영하고 있습니다. 산업용 NOR 플래시 시장은 신제품의 더욱 까다로운 기판 레이아웃 및 저전력 요구 사항에 부합하기 때문에 꾸준히 시리얼 설계로 전환되고 있습니다. GigaDevice에 따르면, 자사의 GD25NX xSPI NOR 시리즈는 400 MB/s의 처리량을 달성했으며, 기존의 1.8V 옥탈 제품에 비해 읽기 시 전력 소비를 최대 50% 줄였습니다.

병렬 NOR 플래시 시장 점유율은 감소 추세에 있지만, 구형 프로그래머블 로직 컨트롤러(PLC), 특정 방위용 전자 장비 및 일부 자동차용 안전 모듈 분야에서는 여전히 확고한 입지를 유지하고 있습니다. 이러한 용도에서는 동기식 병렬 액세스나 넓은 버스 폭이 필요한 경우가 많으며, 초기 인증 후 오랜 기간 동안 계속 사용되는 경향이 있습니다. 따라서 산업용 NOR 플래시 업계에서 신규 설계의 상당수가 시리얼 아키텍처로 전환되고 있는 상황에서도, 병렬 제품에는 안정적인 수익 기반이 확보되어 있습니다. 전반적인 추세로 볼 때, 신규 수요에서는 시리얼 방식이 주류를 이루고 있는 반면, 재설계보다는 지속성이나 검증된 호환성을 중시하는 용도에서는 병렬 방식이 여전히 중요한 역할을 하고 있습니다.

2025년 기준으로, Quad SPI는 산업용 NOR 플래시 시장 점유율의 52.3%를 차지했습니다. 이는 대역폭, 기판 설계의 간소화, 그리고 컨트롤러와의 호환성 측면에서 최적의 균형을 제공했기 때문입니다. Quad SPI는 광범위한 산업용 에지 디바이스 및 마이크로컨트롤러 플랫폼의 도입 기반에서 여전히 기본 선택지로 자리 잡고 있습니다. JEDEC의 표준화는 기기 제조업체에 시리얼 플래시의 상호 운용성에 관한 명확한 기준을 제공함으로써 이러한 위상을 뒷받침해 왔습니다. SPI 싱글 및 듀얼 카테고리는 레거시 설계의 업데이트가 빠르게 진행되지 않는 저밀도 및 비용 중심의 소켓을 위해 여전히 제공되고 있습니다.

옥탈 및 xSPI는 가장 빠르게 성장하는 인터페이스 분야로, 2031년까지 연평균 성장률(CAGR)이 6.9%를 나타낼 것으로 전망됩니다. 이러한 성장은 인스턴트 온(Instant-on) 작동과 더 높은 지속 읽기 속도가 필요한 AI 추론 노드 및 자동차용 도메인 컨트롤러 수요를 반영한 것입니다. 산업용 NOR 플래시 시장에서 옥탈 제품에 ECC 및 CRC 기능을 통합하는 공급업체들은 외부 지원 로직이 비용과 설계 복잡성을 증가시키는 자동차 안전 프로그램 분야에서 시장 진입 기회를 확대되고 있습니다. 또한, JEDEC xSPI 프로토콜 준수는 프리미엄 플랫폼 인증을 위한 실질적인 관문이 되고 있습니다. 신뢰할 수 있는 xSPI 로드맵을 갖추지 못한 벤더는 산업용 NOR 플래시 시장에서 수익성이 가장 높은 분야가 아닌, 표준 소켓 분야에 머무를 가능성이 높습니다.

지역별 분석

아시아태평양은 2025년 산업용 NOR 플래시 시장 점유율의 55.2%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.2%를 나타낼 것으로 전망되어, 생산 규모와 수요의 깊이 양면에서 확고한 선두 자리를 유지하고 있습니다. 중국은 여전히 이 지역 최대의 내수 시장이며, 현지 기업들이 자급자족을 위해 55nm 및 40nm 공정 생산을 확대하고 있어 공급 측면에서도 가장 활발한 주체로 부상하고 있습니다. 대만은 산업용 NOR 플래시 시장에서 IDM(수직 통합형 반도체 제조업체)의 거점으로서 계속해서 중요한 역할을 수행하고 있으며, 윈본드는 전 세계 NOR 플래시 매출의 23%를 차지하고 있는 것으로 보고되고 있으며, 2026년까지 NOR 플래시 출하량을 30%-40% 늘리는 것을 목표로 하고 있습니다. 또한, 맥로닉스는 2026년까지 12인치 공장의 생산 능력을 50% 확대하기 위한 220억 대만 달러(6억 9,910만 달러) 규모의 투자 계획을 재개했습니다. 일본과 한국은 자동차 및 산업용 전자기기를 통해 안정적인 수요를 창출하고 있는 반면, 인도와 동남아시아는 ‘차이나 플러스 원(China Plus One)’ 조달 전략에 따라 전자기기 조립이 확대됨에 따라 그중요성이 커지고 있습니다.

북미와 유럽은 합쳐서 2위 수요 블록을 형성하고 있으며, 산업용 NOR 플래시 시장의 이 부분은 제조 규모보다는 용도의 가치에 의해 특징지어집니다. 수요는 자동차용 ADAS, 방위, 항공우주, 산업용 자동화 분야에 집중되어 있으며, 이로 인해 일반 소비자용 메모리 부문보다 높은 평균 판매 가격이 유지되고 있습니다. 인피니온은 ASIL-D 규격을 준수하는 SEMPER NOR 제품과 우주 프로그램용으로 QML 인증을 획득한 512Mbit 내방사선성 NOR 플래시를 통해 이러한 입지를 공고히 하고 있습니다. 또한, 유럽은 연결된 산업용 기기의 기반이 잘 갖춰져 있다는 장점도 있어, ‘사이버 복원력법’에 따라 해당 지역의 산업용 디바이스 생태계 전반에서 보안 NOR 플래시 조달이 증가하고 있습니다.

세계 기타 지역들은 여전히 규모는 작지만, 통신 인프라 및 산업용 IoT 도입과 관련해 새로운 수요를 창출하고 있습니다. 4G 및 5G 기지국이 구축될 때마다, 네트워크 장비 내의 부트 펌웨어와 시스템 구성을 저장하기 위한 NOR 플래시에 대한 수요가 점차 증가하고 있습니다. 중동 또한 석유 및 가스 자동화 및 스마트 시티 프로그램과 관련된 견고한 산업용 전자 기기의 중요한 2차 시장으로 부상하고 있습니다. 남미는 전자기기 조립 및 가전제품 제조와 밀접한 관련이 있기 때문에 그 성장세는 산업용 NOR 플래시 시장에서 독자적인 추세를 보이기보다는 보다 광범위한 세계적 수요 변화에 따라가는 경향이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the industrial nOR flash market size is expected to increase from USD 408.61 million in 2025 to USD 432.31 million in 2026 and reach USD 573.09 million by 2031, growing at a CAGR of 5.80% over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V Class, and More), Process Technology Node (65 Nm, 45 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Industrial NOR Flash Market Trends and Insights

Quad And Octal SPI Adoption Unlocking Higher Throughput at the IoT Edge

Quad SPI already supports a large installed base of code-storage sockets, and the move toward Octal SPI and xSPI is raising sustained read bandwidth to 400 MB/s for edge platforms that need faster boot and execution behavior. GigaDevice launched its GD25NX series in November 2025 with a 1.8 V core and 1.2 V I/O design, and the company said the product delivered 30% faster programming speed and 10% shorter erase time than conventional 1.8 V octal flash in 200 MHz double transfer rate mode. In the industrial NOR flash market, this shift matters because larger firmware images are making bandwidth a more visible design bottleneck than raw capacity in many AI edge nodes. Vendors that combine xSPI support with execute-in-place behavior are extending the role of NOR flash into applications that previously leaned on external SRAM to keep response times low. That is tightening platform qualification windows and giving an advantage to suppliers that already have certified high-speed portfolios in the industrial NOR flash market.

China 55 Nm And 40 Nm Indigenous Process Reshaping The Supply Equilibrium

China is reshaping the supply side of the industrial NOR flash market by expanding local production at 55 nm and 40 nm, with the goal of reducing dependence on Taiwan-based and U.S.-linked sources. Wuhan XMC had its IPO application accepted by the Shanghai STAR Market in September 2024, and the company offers foundry services for NOR flash at 40 nm and above. GigaDevice and Puya are also broadening domestic supply options, which is increasing the strategic weight of local sourcing in standard and mid-density products. This build-out is not only replacing imports, but it is also creating a parallel pricing environment that is more aggressive in commodity tiers than in premium categories. The industrial NOR flash market is therefore becoming more clearly split between price-led domestic supply and qualification-led premium supply, where safety, security, and long design history still matter more than price alone.

Cost Premium Over NAND Constraining Adoption At The Density Ceiling

The industrial NOR flash market still faces a structural cost-per-bit disadvantage against NAND once density requirements exceed 256 Mb, which limits adoption in designs where storage economics matter more than fast random read access. The 2D NOR roadmap also remains difficult beyond 45 nm, and meaningful density scaling would require more advanced structures that are still far from broad-volume deployment. Macronix delayed its 3D NOR development program by about 2 years in 2026 to redirect resources toward supply-constrained mid-density NOR and eMMC products. That decision highlights the trade-off between long-term scaling investments and near-term revenue opportunities in segments that are already supply-constrained. The result is a dual-track industrial NOR flash market where 128-512 Mb products continue to grow in infrastructure, industrial, and automotive applications, but low-density consumer volumes are harder to expand when NAND alternatives are cheaper.

Other drivers and restraints analyzed in the detailed report include:

- Secure-Boot And OTA-Update Mandates Creating Compliance-Driven Demand Pull

- Constellation-Scale LEO Satellites Creating A Durable Premium-ASP Pocket

- Scaling Ceilings Opening Architectural Entry Points For MRAM And ReRAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR flash held 66.1% of the industrial NOR flash market size in 2025 and is projected to grow at a 6.7% CAGR through 2031. Its lead reflects the preference of current IoT and automotive SoCs for low-pin-count serial interfaces that support execute-in-place without a dedicated memory bus. The industrial NOR flash market has moved steadily toward serial designs, as they better fit tighter board layouts and lower power budgets in new products. GigaDevice said its GD25NX xSPI NOR series achieved 400 MB/s throughput and reduced read power by up to 50% compared with conventional 1.8 V octal alternatives.

Parallel NOR flash is losing share, but it still retains a durable position in legacy programmable logic controllers, selected defense electronics, and some automotive safety modules. Those sockets often need synchronous parallel access and a wide bus width, and they also tend to stay in service for many years after initial qualification. That gives parallel products a stable revenue floor even as most new designs in the industrial NOR flash industry move to serial architectures. The overall pattern shows a market where serial dominates new demand, while parallel remains relevant in applications that value continuity and proven fit over redesign.

Quad SPI accounted for 52.3% of the industrial NOR flash market share in 2025 because it offered the best balance between bandwidth, board simplicity, and controller compatibility. It remains the default choice across a wide installed base of industrial edge devices and microcontroller platforms. JEDEC standardization has supported this position by giving equipment makers a clear framework for serial flash interoperability. The SPI Single and Dual category still serves low-density and cost-sensitive sockets where legacy designs are not being refreshed quickly.

Octal and xSPI are the fastest-growing interface segments, with a 6.9% CAGR projected through 2031. That growth reflects demand from AI inference nodes and automotive domain controllers that need instant-on behavior and higher sustained read speed. In the industrial NOR flash market, vendors that embed ECC and CRC features into octal products are improving their chances in automotive safety programs where external support logic adds cost and design complexity. JEDEC xSPI protocol alignment is also becoming a practical gatekeeper for premium platform qualification. Vendors without a credible xSPI roadmap are likely to stay concentrated in standard sockets rather than the highest-margin part of the industrial NOR flash market.

Geography Analysis

Asia-Pacific held 55.2% of the industrial NOR flash market share in 2025 and is projected to grow at a 7.2% CAGR through 2031, which keeps it firmly in the lead by both production scale and demand depth. China remains the largest domestic demand center in the region and is also the most active supply-side challenger, as local players expand 55 nm and 40 nm production for domestic self-sufficiency. Taiwan continues to anchor the IDM base in the industrial NOR flash market, and Winbond was reported to hold 23% of global NOR flash revenue while targeting a 30%-40% rise in NOR flash shipments in 2026. Macronix also restarted a TWD 22 billion (USD 699.1 million) investment plan to expand 12-inch factory output by 50% in 2026. Japan and South Korea add stable demand through automotive and industrial electronics, while India and Southeast Asia are becoming more important as electronics assembly expands under China-plus-one procurement strategies.

North America and Europe together form the second-largest demand block, and this part of the industrial NOR flash market is defined more by application value than by manufacturing scale. Demand is concentrated in automotive ADAS, defense, aerospace, and industrial automation, which supports higher average selling prices than standard consumer-driven memory segments. Infineon has reinforced this position with ASIL-D-aligned SEMPER NOR products and its 512 Mbit QML-qualified radiation-hardened NOR flash for space programs. Europe also benefits from a dense base of connected industrial equipment, and the Cyber Resilience Act is increasing procurement of secure NOR flash across the region's industrial device ecosystem.

The Rest of the World remains smaller, but it is still adding new demand in telecommunications infrastructure and industrial IoT deployments. Each 4G and 5G base station rollout creates an incremental need for NOR flash to store boot firmware and system configuration in network equipment. The Middle East is also becoming a meaningful secondary outlet for ruggedized industrial electronics tied to oil and gas automation and smart city programs. South America is more closely linked to electronics assembly and appliance manufacturing, so its growth tends to follow broader global demand shifts rather than define them within the industrial NOR flash market.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC Co. Ltd.

- Zbit Semiconductor Inc.

- Eon Silicon Solution Inc.

- Integrated Silicon Solution Inc.

- Alliance Memory Inc.

- AMIC Technology Corp.

- XTX Technology (Shenzhen) Ltd.

- Fudan Microelectronics Group Co. Ltd.

- Giantec Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Quad/Octal SPI Adoption for Fast-Boot IoT Edge Devices across Global Manufacturing Hubs

- 4.2.2 Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- 4.2.3 China 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency

- 4.2.4 Secure-Boot and OTA-Update Mandates in Industry 4.0 Factories

- 4.2.5 Low-Power 1.8 V Serial NOR for Wearable and Point-of-Care Healthcare Electronics

- 4.2.6 Real-Time Sensor Fusion in Autonomous Mobile Robots Driving Demand for 128-512 Mb NOR

- 4.3 Market Restraints

- 4.3.1 Cost Premium over NAND above 256 Mb Limiting High-Density Consumer Adoption

- 4.3.2 Scaling Ceilings beyond 45 nm Steering OEM Roadmaps toward MRAM / ReRAM Substitutes

- 4.3.3 Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk

- 4.3.4 ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Reliability and Qualification Standards Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65-3.6 V)

- 5.4.4 <=1.2 V and Other Specialty Voltages

- 5.5 By Process Technology Node (Value)

- 5.5.1 90 nm and More

- 5.5.2 65 nm

- 5.5.3 55 nm (incl. 58 nm)

- 5.5.4 45 nm

- 5.5.5 28 nm and Below

- 5.6 By Packaging Type (Value)

- 5.6.1 WLCSP / CSP

- 5.6.2 QFN / SOIC

- 5.6.3 BGA / FBGA

- 5.6.4 Other Industrial Grade Packages

- 5.7 By Geography (Value, Volume)

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 France

- 5.7.2.3 United Kingdom

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 Taiwan

- 5.7.3.5 India

- 5.7.3.6 South East Asia

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 Rest of the World

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.5 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.6 Wuhan XMC Co. Ltd.

- 6.4.7 Zbit Semiconductor Inc.

- 6.4.8 Eon Silicon Solution Inc.

- 6.4.9 Integrated Silicon Solution Inc.

- 6.4.10 Alliance Memory Inc.

- 6.4.11 AMIC Technology Corp.

- 6.4.12 XTX Technology (Shenzhen) Ltd.

- 6.4.13 Fudan Microelectronics Group Co. Ltd.

- 6.4.14 Giantec Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis