|

시장보고서

상품코드

2061772

인도네시아의 히트펌프 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Indonesia Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

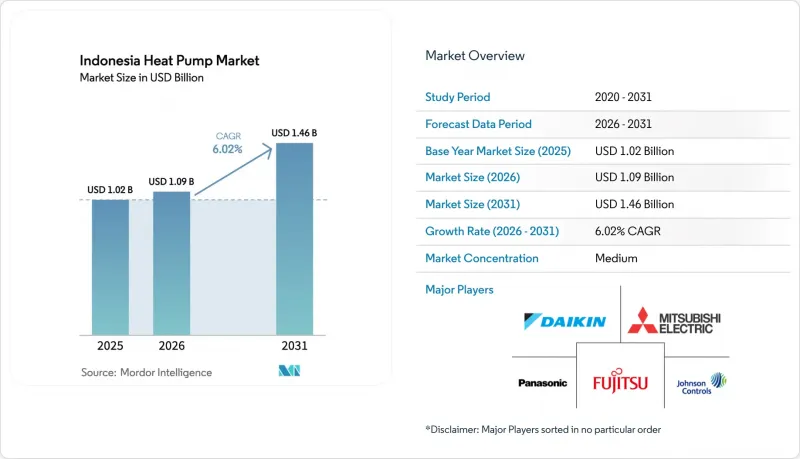

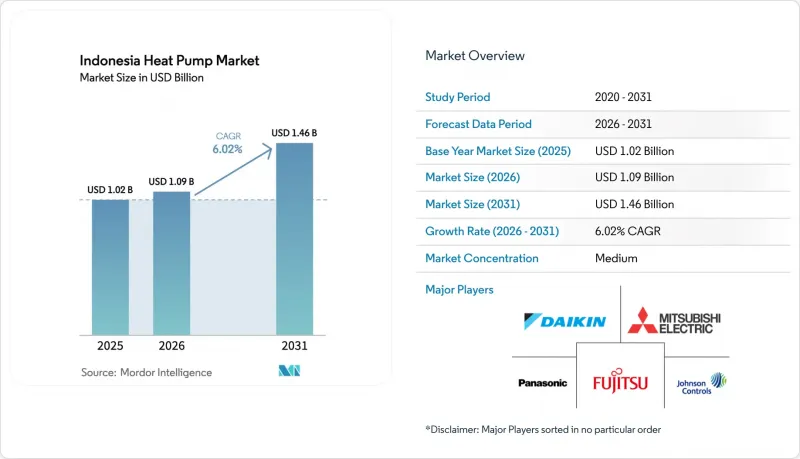

Mordor Intelligence에 의하면, 인도네시아의 히트펌프 시장 규모는 2025년에 10억 2,000만 달러로 평가되었습니다. 2026년에 10억 9,000만 달러에 달하고, 2031년까지 14억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.02%를 나타낼 것으로 전망됩니다.

본 보고서는 공급원(공기원, 수원 등), 기술(공기-공기, 공기-물 등), 용량(10kW 미만, 10-50kW 등), 용도(공간 난방, 공간 냉방 등), 최종 사용자(주거, 상업, 산업), 설치 형태(신규 설치, 개보수), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도네시아의 히트펌프 시장 동향과 인사이트

히트펌프 도입을 위한 정부의 인센티브 시행

개정된 에너지 절약 규정에 따라 의무화된 에너지 관리 기준치가 하향 조정됨에 따라, 공장, 쇼핑몰, 호텔 등 더 광범위한 시설이 감사 대상이 되었습니다. 현재 감사에서는 저항식 히터보다 히트펌프로의 개조를 더 중시하고 있습니다. 녹색기후기금(GCF)의 혼합금융을 통해 1억 500만 달러의 양허성 자본과 1억 4,270만 달러의 협동융자가 추가됨에 따라, 그동안 에너지 절약을 통한 현금흐름을 담보로 한 대출에 소극적이었던 은행들의 프로젝트 리스크가 완화되었습니다. 감사를 통해 투자 회수 기간이 5년 미만으로 단축된 온수, 세탁 및 공정 열 부하가 확인됨에 따라, 인도네시아의 히트펌프 시장은 직접적인 혜택을 보고 있습니다. 또한, 규제 위반에 대한 처벌도 집행 조치가 강화되기 전에 경영진이 투자를 하도록 독려하고 있습니다. 주요 과제는 인증 에너지 서비스 기업의 수가 제한적이라는 점이지만, 이 프레임워크는 다른 대출 기관들도 따라 할 만한, 대출이 가능한 활용 사례를 입증하고 있습니다.

급속한 도시화와 에너지 효율이 높은 건축물 증가

건물은 이미 인도네시아 최종 에너지 소비량의 23%를 차지하고 있으며, 에너지 절약 대책이 지연될 경우 2030년까지 40%에 달할 가능성이 있습니다. 2025년 4월에 개최된 자카르타 그린 성장 포럼에서는 부동산 소유주들로부터 배출량을 10% 감축하겠다는 165건의 자발적 약속을 확보했으며, 이는 인증을 받은 공조 설비 업그레이드에 대한 시장 수요가 증가하고 있음을 보여줍니다. 조명 및 공조와 관련된 최소 에너지 성능 기준은 연간 1조 9,000억 루피아(1억 2,100만 달러)에 달하는 절감 효과와 2030년까지 8,400만 톤의 CO2 배출 감축을 약속하고 있어, 개발업자들을 향한 자본 시장의 압박이 거세지고 있습니다. 2030년까지 100만 호의 친환경 주택을 신축하거나 개보수한다는 국가 프로그램에서는 고효율 온수 공급 솔루션의 도입이 의무화되어 있으며, 이에 따라 인도네시아의 히트펌프 시장은 주택 정책에 포함되었습니다. 시행 측면의 과제는 여전히 남아 있으며, 2025년 시점에서 에너지 관리 기준을 충족한 건물은 고작 1.45%에 그치고 있지만, 중기적인 방향성은 명확하여 장기적인 수요 증가를 뒷받침하고 있습니다.

높은 초기 도입 비용과 제한된 자금 조달 수단

히트펌프식 온수기는 여전히 전기식 저장 탱크보다 약 10배의 비용이 들며, 대부분의 상업용 대출은 최장 7년, 금리 7-12%로 제한되어 있어 자금 사정이 어려운 구매자들의 도입을 저해하고 있습니다. 2024년 전국에서 활동 중인 에너지 서비스 기업은 불과 약 25개사에 불과하며, 막대한 설비 투자를 상쇄할 수 있는 프로젝트의 집약이나 성과 기반 계약을 통한 솔루션은 제한적입니다. 은행이 에너지 절약을 통한 현금 흐름을 담보로 받아들이는 경우는 드물기 때문에 인도네시아의 히트펌프 시장은 실적을 보장하고 초기 자금을 지원하는 ‘에너지 절약 보험’이나 UOB의 ‘U-Energy’ 플랫폼과 같은 기부자 지원 프로그램에 의존하고 있습니다. 이러한 방안들은 유망하지만, 전국적인 수요에 비해 규모가 작기 때문에 단기적으로는 비용 측면의 장벽이 지속될 것으로 보입니다.

부문별 분석

2025년에는 공기원 히트펌프가 시장 가치의 46.78%를 차지했으며, 온화한 열대 기후의 온도 변동에 대응하면서도 비교적 간편하게 설치할 수 있는 이 기술이 인도네시아 히트펌프 시장에서 점유율 1위를 차지하고 있는 것으로 밝혀졌습니다. 가자 마다 대학교 및 PT Geoenergis가 주도한 시범 사업은 인도네시아의 추정 2만 3,766MW 규모의 표층 지열 자원을 활용하는 지열 히트 펌프 시장에 대해 연평균 7.31%의 성장 여지가 있음을 시사하고 있습니다. 2건의 수평 루프 방식 실증 실험에서는 성능 계수가 4에 가까운 수치를 기록했으며, 스플릿형 에어컨에 비해 21-45%의 전력 절감 효과를 달성했습니다.

공기식 장비는 유통업체이 전국에 예비 부품을 재고로 보유하고 있으며, 허가 절차도 최소한으로 이루어지기 때문에 대규모 도입 기반을 유지하고 있습니다. 그러나 정부의 에너지 감사 의무에서는 수명 주기 비용 지표가 중시되고 있어, 병원이나 대학의 향후 공공 조달에서는 지중 루프 방식이 우위를 점할 것으로 보입니다. 수원식 및 하이브리드 솔루션은 이용 가능한 연못의 유무나 제어의 복잡성 때문에 여전히 틈새 시장 수준에 머물러 있습니다. 규제 당국이 탄소 가격 도입을 검토하고 있는 만큼, 상당한 감축 효과가 초기 비용이라는 장벽을 상회할 가능성이 있어, 인도네시아의 히트펌프 시장에서 지중 루프 방식의 성장세는 구조적으로 지속될 것으로 보입니다.

2025년 매출의 42.59%를 공중-수중 시스템이 차지했으며, 이는 호텔, 병원, 아파트 운영자들이 기존 물 순환 배관과 원활하게 연동되는 패키지 솔루션을 중시하고 있음을 보여줍니다. 호텔에서 가변 냉매 유량(VRF) 시스템으로 교체함에 따라 냉방 에너지 효율 지수가 5.40까지 향상되었으며, 인버터 압축기의 우수성이 다시 한번 입증되었습니다. 지중-수 시스템은 지열 이용 시장 전반의 호조를 반영하여 7.03%라는 예측 연평균 성장률(CAGR)을 기록하며, 다른 방식을 앞지르는 추세를 보이고 있습니다.

공기-공기 히트펌프는 냉방 분야에서 깊이 뿌리내린 스플릿형 에어컨 문화와 경쟁하고 있습니다. 스플릿형 에어컨은 운영 비용이 높음에도 불구하고, 여전히 소비자 인지도 면에서 우위를 차지하고 있습니다. 물-물 시스템이나 태양열·바이오매스와 결합한 하이브리드 시스템은 전문 기술 인력을 보유한 산업단지 내에서만 제한적으로 운영되고 있습니다. 건축 기준이 엄격해지는 가운데, 건축가들은 미래를 내다본 건물 설계의 일환으로 온수 순환 루프를 지정하고 있으며, 이에 따라 인도네시아의 전체 히트펌프 시장에서 공기-물 시스템의 주도적 지위가 유지될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the indonesia heat pump market size is projected to be USD 1.02 billion in 2025, USD 1.09 billion in 2026, and reach USD 1.46 billion by 2031, growing at a CAGR of 6.02% from 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Heat Pump Market Trends and Insights

Implementation of Government Incentives for Heat Pump Adoption

Revised Energy Conservation rules lower mandatory energy-management thresholds, bringing a broader mix of factories, malls, and hotels under audit requirements that now emphasize heat-pump retrofits over resistance heaters. Blended-finance from the Green Climate Fund adds USD 105 million of concessional capital and USD 142.7 million of co-financing, trimming project risk for banks that previously hesitated to lend against energy-savings cash flows. The Indonesia heat pump market gains directly because audits identify hot-water, laundry, and process-heat loads where paybacks now fall under five years. Penalties for non-compliance also drive management teams to invest before enforcement actions escalate. The main drag is the limited pool of accredited energy-service companies, but the framework proves bankable use cases that other lenders will replicate.

Rapid Urbanization and Rising Construction of Energy Efficient Buildings

Buildings already absorb 23% of Indonesia's final energy use and could touch 40% by 2030 if efficiency lags. The Jakarta Green Growth forum in April 2025 secured 165 voluntary commitments from property owners to cut emissions 10%, signaling stronger market pull for certified HVAC upgrades. Minimum Energy Performance Standards for lighting and air conditioning promise savings equal to IDR 1.9 trillion (USD 121 million) per year and prevent 84 million tons of CO2 by 2030, so capital-markets pressure on developers is intensifying. National programs to build or retrofit one million green homes by 2030 mandate efficient hot-water solutions, inserting the Indonesia heat pump market into housing policy. Enforcement gaps persist, only 1.45% of buildings met energy-management standards in 2025, but the medium-term signal is clear and supports long-run demand growth.

High Initial Installation Cost and Limited Financing Options

Heat-pump water heaters still cost roughly ten times electric tanks, and most commercial loans top out at seven-year tenors with 7-12% interest rates, suppressing uptake among cash-constrained buyers. Only about 25 active energy-service companies existed nationwide in 2024, limiting project aggregation and performance-contracting solutions that could offset high capex. Banks rarely accept energy-savings cash flows as collateral, so the Indonesia heat pump market relies on donor-supported programs like Energy Savings Insurance and UOB's U-Energy platform that guarantee performance and front capital. These schemes are promising but remain small relative to nationwide demand, so cost barriers will persist in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Declining Upfront Costs and Higher Seasonal Performance of Inverter Based Units

- Increasing Electricity Access and Grid Reliability

- Shortage of Skilled Heat Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source heat pumps delivered 46.78% of market value in 2025, demonstrating the Indonesia heat pump market share lead of a technology that balances moderate tropical temperature swings with relatively simple installation. Institutional pilots at Universitas Gadjah Mada and PT Geoenergis point to a 7.31% annual growth runway for ground-source units that tap Indonesia's estimated 23,766 MW shallow geothermal resource. Two horizontal-loop demonstrations recorded coefficients of performance near four, saving 21-45% electricity over split ACs.

Air-source equipment keeps its large installed base because distributors stock spare parts nationwide and permits are minimal. Yet government energy-audit mandates favor lifecycle cost metrics, tilting future public procurements toward ground loops in hospitals and universities. Water-source and hybrid solutions stay niche, limited by available ponds or high control complexity. With regulators considering carbon pricing, deep reductions may outweigh first-cost hurdles, making ground-source momentum structurally durable inside the Indonesia heat pump market.

Air-to-water configurations earned 42.59% of 2025 revenue, illustrating how hotel, hospital, and apartment operators value a package that dovetails with existing hydronic lines. Variable refrigerant flow upgrades in hotels raised cooling energy efficiency ratios to 5.40, further validating inverter compressor advantages. Ground-to-water systems mirror overall ground-source tailwinds, clocking a 7.03% forecast CAGR that is poised to outstrip other formats.

Air-to-air heat pumps contend with the deeply entrenched split-AC culture for cooling, which still dominates consumer mindshare despite higher operating costs. Water-to-water and hybrid solar-thermal or biomass couplings remain confined to industrial estates with specialized engineering staff. As building codes tighten, architects specify hydronic loops that future-proof properties, sustaining air-to-water leadership inside the broader Indonesia heat pump market size narrative.

List of Companies Covered in this Report:

- Daikin Industries, Ltd.

- Mitsubishi Electric Corp.

- Panasonic Heating and Cooling Solutions

- Fujitsu General Ltd.

- Carrier Global Corp.

- Trane Technologies plc

- Johnson Controls-Hitachi Air Conditioning

- NIBE Industrier AB

- Stiebel Eltron GmbH and Co. KG

- Viessmann Climate Solutions SE

- Vaillant Group

- Glen Dimplex Group (Dimplex)

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp.

- Mayekawa Mfg. Co., Ltd.

- Aermec S.p.A

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of Government Incentives for Heat Pump Adoption

- 4.2.2 Rapid Urbanisation and Rising Construction of Energy-Efficient Buildings

- 4.2.3 Declining Upfront Costs and Higher Seasonal Performance of Inverter-Based Units

- 4.2.4 Increasing Electricity Access and Grid Reliability

- 4.2.5 Surge in Distributed Solar-Heat Pump Hybrid Installations in Remote Resorts

- 4.2.6 Push From Cold-Chain Fishery Exports Requiring High-Efficiency Process Cooling

- 4.3 Market Restraints

- 4.3.1 High Initial Installation Cost and Limited Financing Options

- 4.3.2 Shortage of Skilled Heat Pump Technicians

- 4.3.3 Fragmented After-Sales Service Network in Outer Islands

- 4.3.4 Customer Preference for Cheap Split AC and Water Heater Combos

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corp.

- 6.4.3 Panasonic Heating and Cooling Solutions

- 6.4.4 Fujitsu General Ltd.

- 6.4.5 Carrier Global Corp.

- 6.4.6 Trane Technologies plc

- 6.4.7 Johnson Controls-Hitachi Air Conditioning

- 6.4.8 NIBE Industrier AB

- 6.4.9 Stiebel Eltron GmbH and Co. KG

- 6.4.10 Viessmann Climate Solutions SE

- 6.4.11 Vaillant Group

- 6.4.12 Glen Dimplex Group (Dimplex)

- 6.4.13 PHNIX Eco-Energy Solution Ltd.

- 6.4.14 Thermia Heat Pumps AB

- 6.4.15 Sanden Holdings Corp.

- 6.4.16 Mayekawa Mfg. Co., Ltd.

- 6.4.17 Aermec S.p.A

- 6.4.18 Clivet SpA

- 6.4.19 Alpha Innotec GmbH

- 6.4.20 Ochsner Warmepumpen GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment