|

시장보고서

상품코드

2061773

베트남의 히트펌프 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vietnam Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

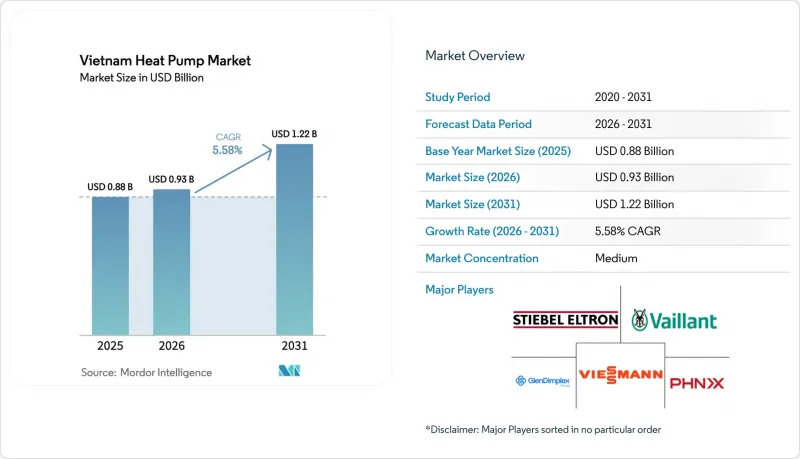

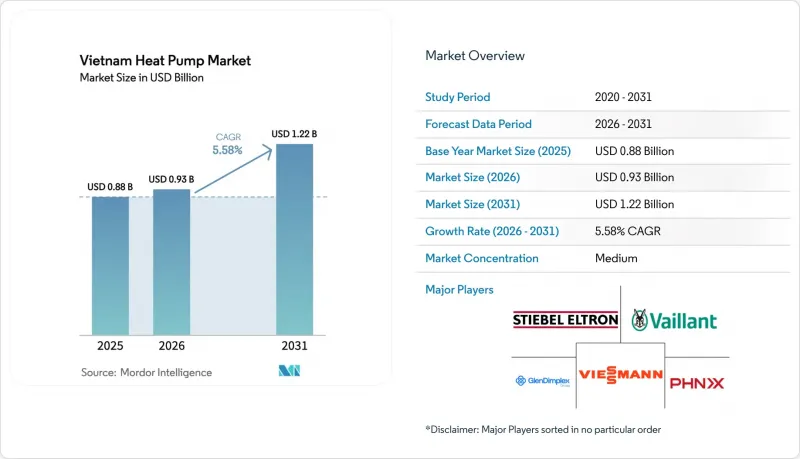

Mordor Intelligence에 의하면, 베트남의 히트펌프 시장 규모는 2025년에 8억 8,000만 달러로 평가되었습니다. 2026년 9억 3,000만 달러에서 2031년까지 12억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.58%를 나타낼 전망입니다.

본 보고서는 열원 유형(공기원, 수원 등), 기술(공기-공기, 공기-물 등), 용량(10kW 미만, 10-50kW 등), 용도(공간 난방, 공간 냉방 등), 최종 사용자(주거, 상업, 산업), 설치 형태(신규 설치, 개보수), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

베트남의 히트펌프 시장 동향과 인사이트

정부 보조금 및 무이자 그린론 도입 가속화

자금 조달 비용의 감소로 인해 구매 행동에 변화가 나타나기 시작하고 있습니다. 특히, 그동안 고효율화를 위한 설비 교체를 미뤄왔던 소규모 호텔 체인이나 아파트 관리조합에서 이러한 현상이 두드러집니다. 상업 금융기관이 그린론 상품에 2%의 이자 보조금을 포함시킴으로써, 중층 빌딩용 온수 설비의 월별 상환액은 전력 사용량 감축으로 인한 절감액을 밑돌게 되어, 차주에게 즉각적인 긍정적 현금 흐름이 발생하고 있습니다. 설치 업체에 따르면, 호치민시의 R32 냉온수 히트펌프 미처리 수주는 2026년 1월부터 3월 사이에 2배로 증가했습니다. 이러한 변화는 할당 한도에 도달하기 전에 우대 조건을 확보하려는 구매자들이 몰려들었기 때문인 것으로 분석됩니다. 이에 대해 제조업체는 장비, 모니터링 소프트웨어, 미리 작성된 신청 서류를 한 세트로 묶은 ‘대출 지원’ 패키지를 제공함으로써 대응하고 있으며, 그린 파이낸스 관련 서류 절차에 익숙하지 않은 최종 사용자의 거래 장벽을 낮추고 있습니다. 향후 2년 동안, 이러한 정책 주도형 자금 공급에 힘입어 많은 상업시설에서 히트펌프와 가스 온수기의 투자 회수 기간 차이가 3년 미만으로 줄어들 것으로 예상되며, 단기적인 수요가 확고해질 것으로 전망됩니다.

도시 지역의 비효율적인 전기 온수기에 대한 단계적 폐지 의무화

QCVN 25 : 2025에 규정된 준수 기한에 따라, 부동산 관리자는 보유 중인 기기의 점검을 실시해야 하며, 이에 따라 수년에 걸친 교체 일정을 수립하고 있습니다. 현재 시 검사관이 정기 안전 점검 시 에너지 증명서 기록을 확인하고 있기 때문에 구형 저항식 온수기 소유자는 전기요금 증가에 더해 과태료 부과 대상이 될 위험에 처해 있으며, 이로 인해 기술 전환을 결정하는 속도가 빨라지고 있습니다. 하노이의 소매 체인점들은 이미 효율이 낮은 축열식 온수기를 매장에서 철수하고, 2025년 최소 성능 기준을 충족하는 인버터 구동식 히트펌프 모델로 교체하고 있습니다. 보험사 역시 기준을 충족하지 못하는 기기에 대해서는 화재 위험에 대한 보상이 무효화될 가능성이 있다고 시사하고 있어, 규제에 따른 ‘당근’에 더해 경제적 ‘채찍’도 가해지게 됩니다. 규제의 적용이 1급 도시에서 2급 도시로 확산됨에 따라, 수요의 파장이 유통 채널 전반으로 퍼져 나가며, 2029년까지 두 자릿수의 출하 성장세가 지속될 것으로 예측됩니다.

저탄소형 수산 양식용 난방 시스템에 대한 수요 증가

수출 중심의 새우 및 팡가시우스 양식장은 탄소 조정 요금 도입이 임박한 유럽 및 북미의 구매처와 계약을 유지하기 위해, 스코프 1 배출량 감축 실적을 입증하라는 압력을 받고 있습니다. 초기 실증 실험 결과, 수원형 히트펌프가 디젤 연료 사용량을 줄이면서 치어의 생존율을 6-8포인트 향상시키는 것으로 나타났으며, 이러한 운영상의 장점은 양식장 관리자들로부터 높은 평가를 받고 있습니다. 기후 변화 관련 보험 계약에서는 현재 전기로 운영되는 부화장에 대해 보험료 할인이 제공되고 있어, 이러한 가치 제안을 더욱 매력적으로 만들고 있습니다. 100억 달러 규모의 수산물 수출 산업을 지키고자 하는 주 당국은 소규모 사업자들에게 비용 절감 효과를 입증하기 위해 실증 플랜트에 공동 출자하고 있습니다. 2028년 시장 개시를 앞두고 탄소 크레딧의 현물 가격이 상승하는 가운데, 히트펌프 프로젝트를 통해 검증된 감축량을 축적한 양식장은 프로젝트의 경제성을 높일 수 있는 거래 가능한 수익원을 확보하게 될 것입니다.

부문별 분석

2025년 기준, 베트남의 히트펌프 시장 점유율의 68.78%를 공기원 시스템이 차지했습니다. 이는 적절한 외부 기온, 광범위한 판매점 네트워크, 그리고 설치의 용이성이 배경에 있습니다. 히트 펌프와 가스 또는 바이오매스 보일러를 결합한 하이브리드 설계는 상업 및 산업용 사용자들이 피크 시간대의 전력 가격 및 송전망의 불안정성에 대비하기 위해 도입함에 따라 연평균 성장률(CAGR) 7.13%를 나타낼 전망입니다. 베트남의 수원형 히트펌프 시장 규모는 여전히 작지만, 해안 리조트 지역과 양식업 분야에서 진행되고 있는 실증 실험은 장기적으로 틈새 시장이 확대될 가능성을 시사하고 있습니다. 지열 이용의 보급은 도시 지역의 토지 부족과 시추 비용 문제로 인해 제약을 받고 있으며, 도입은 처음부터 수직 시추공을 계획할 수 있는 데이터센터 캠퍼스나 신규 산업단지로 한정되어 있습니다.

하노이와 호치민시의 개발업체들은 2029년 냉매 규제를 준수하는 R32 충전형 공기원열 유닛을 사전에 설치하는 사례가 늘어나고 있으며, 이를 통해 주민들이 개조 공사를 할 때 겪는 번거로움을 줄이고 있습니다. 한편, 각 제조업체는 습도가 높고 기온이 35-40℃에 달하는 여름철 기상 조건에 맞추어 실외기 코일과 인버터 구동 장치를 미세 조정하여, 부분 부하 시에도 계절 성능 계수(SEER)를 4.5 이상으로 유지하고 있습니다. 이러한 발전으로 인해 공기열원 히트펌프의 우위는 더욱 공고해지고 있지만, 산업의 전기화가 진행되고 냉매의 단계적 폐지가 추진되는 가운데, 특수 용도 분야에서 지중열원 및 수열원 히트펌프 도입을 위한 발판이 마련되고 있습니다.

2025년, 호텔, 병원, 아파트에서 온수 공급 및 바닥 난방 루프를 우선시한 결과, 공기-물식 기기가 베트남의 히트펌프 시장 규모의 60.31%를 차지했습니다. 데이터센터가 폐열 회수를 추진하고, 메콩 델타의 부화장이 이상 기후 시 수온을 안정화하기 위해 지열 루프를 도입함에 따라, 베트남 내 지중-수식 유닛 시장 점유율은 상승할 전망입니다. 공대공 분할형 유닛은 남부 여러 현에서 냉방 용도로 주로 사용되고 있지만, 난방 모드로 가동되는 경우는 드물며, 시장 확대에 기여하는 정도는 제한적입니다. 물-물형 장비는 도시 재개발 구역의 지역 냉방 시스템에 활용되고 있으며, 이곳에서는 중앙 냉수 플랜트가 열회수 칠러를 통합함으로써 추가 전력 투입 없이 공정용 또는 위생용 온수를 공급하고 있습니다.

빈즈엉성의 데이터센터 캠퍼스 개발업체들은 지중-수열 펌프가 30℃의 서버 폐열을 회수하여, 보조 부스터 없이 60℃의 공정용수로 가열하는 이중 온도 수열 루프의 시범 운영을 진행하고 있습니다. 한편, 양식업자들은 내식성과 몬순 기간 동안 안정적인 COP(성능 계수)를 이유로, 모듈식 물-물 유닛에 연결된 밀폐 루프식 연못용 코일을 선호하여 채택하고 있습니다. 이에 반해, 장비 제조업체들은 공장에서 사전 조립된 스키드 모듈을 제공함으로써 설계 기간을 수개월에서 수주일로 단축하고 있습니다. 이는 수출 인증 감사를 제때 마칠 수 있도록 서둘러 진행되는 프로젝트에 있어 큰 장점이 됩니다. 감시 플랫폼이 현장 데이터를 통합함으로써, 자금 제공업체는 장기적인 성능에 대한 확신을 얻을 수 있고, 더 저렴한 비용으로 자금을 조달할 수 있게 되어, 주류인 공기-물 시스템과의 비용 격차를 줄일 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the vietnam heat pump market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 0.93 billion in 2026 to reach USD 1.22 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Space Cooling, and More), End User (Residential, Commercial, and Industrial), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Heat Pump Market Trends and Insights

Accelerated Roll-out of Government Subsidies and Zero-Interest Green Loans

Cheaper capital is beginning to reshape buying behavior, especially among small hotel chains and condominium associations that historically delayed high-efficiency upgrades. As commercial lenders embed the 2% interest subsidy in their green-loan products, monthly installments for a mid-rise hot-water plant fall below the cash savings from lower electricity use, creating immediate positive cash flow for borrowers. Installation contractors report that order backlogs for R32 air-to-water units in Ho Chi Minh City doubled between January and March 2026, a shift they attribute to buyers racing to lock in concessional terms before any quota caps are reached. Manufacturers are responding by offering "loan-ready" packages that bundle equipment, monitoring software, and pre-filled application documents, reducing transaction friction for end users who lack experience with green-finance paperwork. Over the next two years, this policy-driven liquidity is expected to narrow the payback gap between heat pumps and gas heaters to less than three years for many commercial sites, firmly anchoring demand in the short term.

Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas

Compliance deadlines embedded in QCVN 25:2025 are forcing property managers to audit appliance fleets and draft multi-year replacement schedules. Because municipal inspectors now review energy-certificate logs during routine safety checks, owners of older resistance heaters are exposed to fines as well as higher electricity bills, accelerating their decision to switch technologies. Retail chains in Hanoi have already removed low-efficiency storage heaters from shelves, replacing them with inverter-driven heat-pump models that meet the 2025 minimum-performance threshold. Insurance firms are also signaling that non-compliant equipment could void fire-risk coverage, adding a financial stick to the regulatory carrot. As enforcement radiates from tier-1 to tier-2 cities, a rolling wave of demand is expected to cascade through the distribution channel, sustaining double-digit shipment growth through 2029.

Rising Demand for Low-Carbon Aquaculture Heating Systems

Export-oriented shrimp and pangasius farms are under pressure to document Scope 1 reductions to retain buyer contracts in Europe and North America, where carbon-adjustment fees loom. Early pilots show that water-source heat pumps can lift larval survival rates by 6-8 percentage points while trimming diesel usage, an operational win that resonates with farm managers. Climate-linked insurance policies now offer premium discounts for electrified hatcheries, further sweetening the value proposition. Provincial authorities, keen to safeguard a USD 10 billion seafood export sector, are co-financing demonstration plants to showcase cost savings to smaller operators. As carbon-credit spot prices rise ahead of the 2028 market launch, farms that bank verified reductions via heat-pump projects will gain a tradable revenue stream that enhances project economics.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Residential High-Rise Construction Boom in Tier-1 Cities

- High Upfront Equipment and Installation Cost

- Shortage of Certified Heat-Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source systems accounted for 68.78% of the Vietnam heat pump market share in 2025, underpinned by favorable ambient temperatures, widespread dealer networks, and lower installation complexity. Hybrid designs pairing heat pumps with gas or biomass boilers are set for a 7.13% CAGR as commercial and industrial users hedge against peak-hour electricity prices and grid instability. The Vietnam heat pump market size for water-source solutions remains modest, yet pilots in coastal resorts and aquaculture hint at long-term niche expansion. Ground-source uptake is inhibited by urban land scarcity and drilling costs, restricting deployments to data-center campuses and greenfield industrial parks where vertical boreholes can be planned from the outset.

Developers in Hanoi and Ho Chi Minh City increasingly pre-install R32-charged air-source units that meet 2029 refrigerant rules, cutting retrofit headaches for residents. Meanwhile, manufacturers fine-tune outdoor coils and inverter drives for humid, 35-40 °C summer conditions, sustaining seasonal performance factors above 4.5 even at partial load. These advances reinforce air-source hegemony, yet rising industrial electrification and refrigerant phase-outs are opening beachheads for ground- and water-source configurations in specialized applications.

Air-to-water equipment captured 60.31% of the Vietnam heat pump market size in 2025 as hotels, hospitals, and condominiums prioritized domestic hot water and radiant floor loops. The Vietnam heat pump market share for ground-to-water units will rise as data centers pursue waste-heat recovery and Mekong Delta hatcheries deploy geothermal loops to stabilize water temperatures during extreme weather events. Air-to-air split units dominate southern provinces for cooling but seldom run in heating mode, curbing their incremental contribution. Water-to-water machines serve district cooling schemes in urban redevelopment zones, where central chilled-water plants integrate heat-recovery chillers to deliver process or sanitary hot water without extra electrical input.

Developers of data-center campuses in Binh Duong are piloting dual-temperature hydronic loops that let ground-to-water heat pumps scavenge 30 °C server exhaust and elevate it to 60 °C process water without auxiliary boosters. Aquaculture operators, meanwhile, favor sealed-loop pond coils linked to modular water-to-water units, citing corrosion resistance and stable COPs during monsoon season. Equipment makers are responding with factory-prefabricated skid modules that compress design timelines from months to weeks, an advantage for fast-track projects racing to meet export certification audits. As monitoring platforms aggregate field data, financiers gain confidence in long-term performance, unlocking cheaper debt that narrows the cost differential with mainstream air-to-water systems.

List of Companies Covered in this Report:

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- Mitsubishi Electric Corp.

- Midea Group Co. Ltd.

- Gree Electric Appliances Inc. of Zhuhai

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- Glen Dimplex Group

- WaterFurnace International Inc.

- PHNIX Eco-Energy Solution Ltd.

- Thermia Heat Pumps AB

- Sanden Holdings Corp. (Heat Pump Div.)

- Enertech Global LLC

- Ecoforest Geotermia S.L.

- MasterTherm CZ s.r.o.

- Mayekawa Mfg. Co. Ltd. (Heat Pump Div.)

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

- Aermec S.p.A

- Alpha Innotec GmbH

- Heliotherm Warmepumpentechnik GmbH

- Ochsner Warmepumpen GmbH

- Clivet SpA

- Hitachi Air Conditioning

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Accelerated Roll-out of Government Subsidies and Zero-Interest Green Loans

- 4.3.2 Mandatory Phase-Out of Inefficient Electric Water Heaters in Urban Areas

- 4.3.3 Rapid Residential High-Rise Construction Boom in Tier-1 Cities

- 4.3.4 Rising Demand for Low-Carbon Aquaculture Heating Systems

- 4.3.5 Heat-Pump Integration in Hyperscale Data-Center Waste-Heat Recovery

- 4.3.6 Impending Ban on R22 Refrigerant Driving Retrofit Demand

- 4.4 Market Restraints

- 4.4.1 High Upfront Equipment and Installation Cost

- 4.4.2 Shortage of Certified Heat-Pump Technicians

- 4.4.3 Limited Available Land for Ground-Source Loop Fields

- 4.4.4 Industrial Natural-Gas Tariff Advantage Over Electricity Prices

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Daikin Industries Ltd.

- 6.4.2 Panasonic Holdings Corp.

- 6.4.3 Mitsubishi Electric Corp.

- 6.4.4 Midea Group Co. Ltd.

- 6.4.5 Gree Electric Appliances Inc. of Zhuhai

- 6.4.6 Stiebel Eltron GmbH & Co. KG

- 6.4.7 Vaillant Group

- 6.4.8 Viessmann Climate Solutions SE

- 6.4.9 Glen Dimplex Group

- 6.4.10 WaterFurnace International Inc.

- 6.4.11 PHNIX Eco-Energy Solution Ltd.

- 6.4.12 Thermia Heat Pumps AB

- 6.4.13 Sanden Holdings Corp. (Heat Pump Div.)

- 6.4.14 Enertech Global LLC

- 6.4.15 Ecoforest Geotermia S.L.

- 6.4.16 MasterTherm CZ s.r.o.

- 6.4.17 Mayekawa Mfg. Co. Ltd. (Heat Pump Div.)

- 6.4.18 Clade Engineering Systems Ltd.

- 6.4.19 Calorex Heat Pumps Ltd.

- 6.4.20 Aermec S.p.A

- 6.4.21 Alpha Innotec GmbH

- 6.4.22 Heliotherm Warmepumpentechnik GmbH

- 6.4.23 Ochsner Warmepumpen GmbH

- 6.4.24 Clivet SpA

- 6.4.25 Hitachi Air Conditioning

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment