|

시장보고서

상품코드

2061843

그라비어 인쇄기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gravure Printing Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

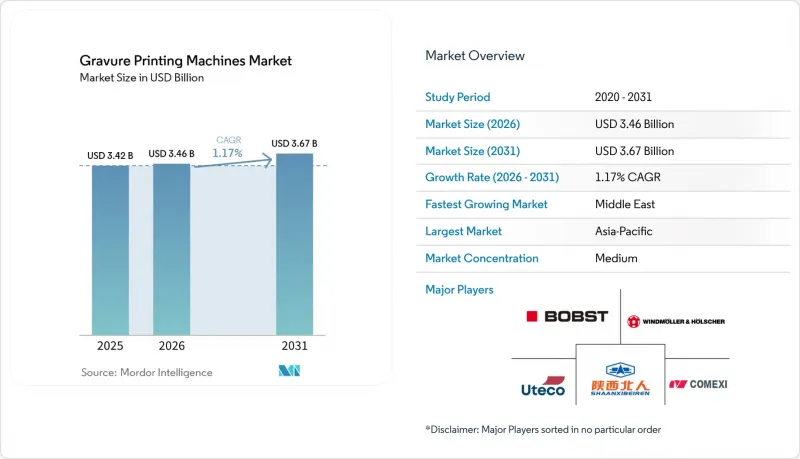

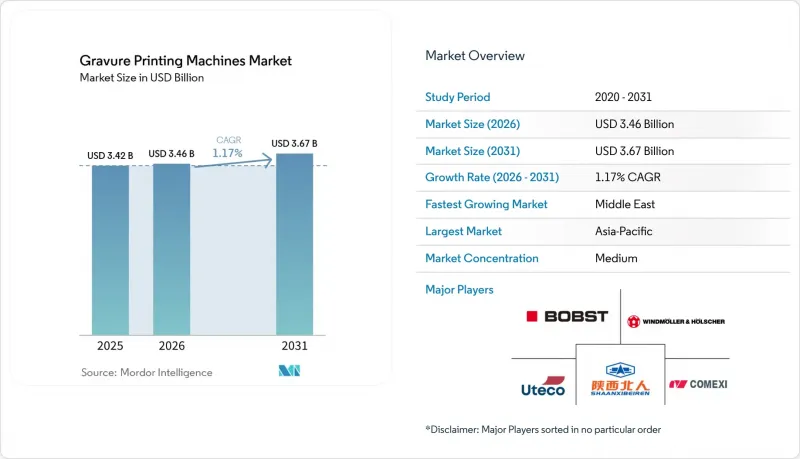

Mordor Intelligence에 의하면, 그라비어 인쇄기 시장 규모는 2025년 34억 2,000만 달러로 평가되었고, 2026년에는 34억 6,000만 달러로 추정되고, 2031년까지 36억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 1.17%로 성장할 전망입니다.

본 보고서는 용도별(연포장, 라벨 제조, 출판 및 상업 인쇄, 장식 인쇄, 산업 및 보안 인쇄), 기재 유형별(플라스틱 필름, 종이 및 판지, 금속 호일 등), 인쇄 속도 등급별(200m/분 이하, 201-350m/분, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 그라비아 인쇄기 시장 동향 및 분석

전자상거래 분야에서 고품질 연포장재에 대한 수요 증가

온라인 소매 업계는 포장 사양을 지속적으로 변경하고 있으며, 이에 따라 각 변환 업체들은 자동 주문 처리 센터에서 사용하기에 충분한 내구성을 갖춘 얇은 필름 위에 불투명도가 높은 그래픽을 인쇄할 수 있는 그라비아 인쇄기로 전환해야 하는 상황에 직면해 있습니다. 카트 장착형 실린더 트롤리를 갖춘 1,050mm에서 1,250mm 폭의 중폭 라인에서는 현재 10분 이내에 작업 전환이 가능해졌으며, 공장에서 색 농도를 저하시키지 않고 1만-2만 미터 단위의 소량 생산 로트에 대응할 수 있게 되었습니다. 2026년에 도입된 차세대 샤프트리스 인쇄기는 EU의 사용 후 재활용 소재 함유율 규정을 충족하기 위한 핵심 요건인 초박형 단일 소재 웹에 대한 장력을 유지하면서, 처리량을 분당 500m까지 더욱 향상시킵니다. 아시아태평양 및 북미의 브랜드 소유주들은 이러한 라인을 선호하여 채택하고 있습니다. 이는 뛰어난 진열 효과와 식품 접촉용 필름의 이물질 제한 기준을 모두 충족하여, 다중 유통 채널 전반에 걸쳐 제품의 품질을 보장하기 때문입니다.

고속 및 자동화 그라비아 인쇄기의 기술적 진보

각 제조업체는 서보 드라이브, 인라인 분광광도계, 클라우드 기반 레시피 라이브러리를 통합함으로써, 기존 그라비아 인쇄를 장폭 생산으로만 제한했던 숙련된 작업자 부족이라는 병목 현상을 해소했습니다. 특정 주력 시스템은 1초에 9,500회의 광학 밀도 측정을 수행하고, 잉크 점도를 4℃ 범위 내로 유지하며, 8분 이내에 설정을 완료함으로써 잉크 낭비를 절반으로 줄입니다. 중국에서는 새로 도입된 라인에 HD 비디오 검사 기능과 독립적인 데크 모터를 통합하여, 분당 500m의 속도로 ±10μm의 레지스터 정밀도를 실현하고 있습니다. 이는 과거 유럽의 플래그십 모델만이 달성했던 사양입니다. 이러한 자동화의 발전으로 인해 그라비아 인쇄가 플렉소 인쇄를 경제적으로 능가하는 전환점이 약 5,000m²까지 낮아졌으며, 중량 생산에서 수익성이 높은 영역이 열리면서 그라비아 인쇄기 시장이 기존에 플렉소그래피가 담당해 온 부문으로 진출할 수 있게 되었습니다.

높은 초기 투자 비용 및 긴 회수 기간

용제 회수 장치와 색상 자동 제어 기능을 갖춘 8-10색 그라비아 라인의 비용은 300만-500만 달러에 달하며, 중규모 SKU 포트폴리오의 경우 실린더 재고 비용으로 50만 달러가 추가로 발생할 수 있습니다. 신흥 시장의 변환업체들은 특히 수주량이 불안정하거나 가치가 낮은 현지 통화로 결제되는 경우, 이러한 자금 조달에 어려움을 겪는 경우가 많습니다. 자동화로 인해 비용의 손익분기점이 5,000제곱미터까지 낮아지더라도, 가동률이 70-80%를 유지하지 못한다면 투자 회수 기간은 7년을 초과할 가능성이 있습니다. 재활용 인쇄기나 저가형 중국산 모델은 설비 투자 비용을 일부 상쇄해 주지만, 에너지 비용 증가와 준비 시간 연장을 초래하기 때문에 고급 플렉서블 패키지 시장 진출을 목표로 하는 소규모 공장들의 딜레마를 더욱 심화시키고 있습니다.

부문별 분석

2025년, 연포장 시장은 그라비아 인쇄기 시장의 55.05%를 차지했으며, 얇은 필름에 불투명도가 높은 그래픽을 인쇄하는 그라비아 인쇄는 경쟁이 치열한 전자상거래 시장의 진열대에서 브랜드 차별화를 꾀하는 데 여전히 필수적입니다. 1,050mm에서 1,250mm 라인을 가동하는 컨버터는 한정판 생산을 높은 수익성으로 수행할 수 있음을 입증했으며, 세팅 시간을 45분에서 10분 미만으로 단축했습니다. 연포장용 그라비아 인쇄기 시장은 단일 소재 필름의 채택을 촉진하는 지속가능성 규제의 혜택을 지속적으로 누리고 있습니다. 이는 그라비아 인쇄의 정밀한 잉크 도포가 차단 성능을 저해하지 않기 때문입니다.

산업용 및 보안 인쇄 시장은 2031년까지 연평균 성장률(CAGR) 1.65%를 나타낼 것으로 예측되며, 이는 다른 모든 용도를 앞지르는 속도입니다. 의약품 시리얼화 관련 법률 및 고가품 위조 방지 요건에 따라, 10마이크로미터 미만의 선폭을 구현할 수 있는 마이크로 조각 실린더가 요구되고 있으나, 이는 플렉소 인쇄나 디지털 인쇄 기법으로는 불가능한 기술입니다. 이 분야에 서비스를 제공하는 각 변환기 업체들은 인라인 검사 카메라와 폐쇄 루프 레지스터 제어에 투자하고 있으며, 코드의 가독성을 저해하지 않으면서 분당 300미터의 생산 속도를 확보하고 있습니다. 반면, 출판 그라비아 인쇄는 잡지가 웹 오프셋으로 전환됨에 따라 2025년 생산량이 8% 미만으로 떨어질 것으로 예상되며, 장기적인 구조적 감소 추세가 확인되고 있습니다.

지역별 분석

2025년, 아시아태평양이 그라비아 인쇄기 시장 매출의 42.16%를 차지했습니다. 중국 제조업체들은 국내 시장을 장악하고 있으며, 경쟁력 있는 가격 책정, 현지화된 부품 네트워크, 그리고 더 빠른 설치 주기를 통해 해외 수주를 점점 더 많이 확보하고 있습니다. 인도의 주요 포장 제조업체들은 기술 이전 라이선스에 따라 국내 인쇄기 생산을 확대하고 있으며, 이를 통해 리드 타임을 14주로 단축하고 관세 부담을 줄이고 있습니다. 동남아시아 국가들, 즉 베트남, 태국, 인도네시아는 다국적 기업의 '중국 플러스 원' 전략의 혜택을 누리고 있으며, 무균 파우치 및 레토르트 용도로 조정된 분당 200-350m 속도의 생산 라인 신규 도입을 주도하고 있습니다.

중동은 가장 빠르게 성장하는 지역이며, 걸프협력회의(GCC) 회원국들이 고부가가치 포장 분야로 다각화를 추진함에 따라 2031년까지 연평균 성장률(CAGR)이 1.97%를 나타낼 것으로 전망됩니다. 그러나 많은 공장에서는 지역 슈퍼마켓용 상품의 납기 단축을 위해, 중형 로트의 그라비아 인쇄에서 중앙 압착형 플렉소 인쇄로 전환하는 추세입니다. 유럽은 시장 규모의 약 28%를 차지하고 있지만, 노후화된 설비가 VOC 배출 규제 및 크롬 프리화 의무에 대응해야 할 필요성에 직면함에 따라, 용제 회수 시스템 및 3가 크롬 도금 공정으로의 개조 수요가 발생하고 있습니다. 북미도 여전히 상당한 시장 점유율을 유지하고 있으며, 연포장 변환업체 간의 통합이 진행되는 가운데, 시리얼화 규정을 준수하는 그라비아-디지털 하이브리드 방식에 대한 관심이 높아지고 있습니다.

남미는 매출에서 상당한 비중을 차지하고 있으며, 환율 변동으로 인해 유럽으로부터의 수입이 위축되는 가운데, 중국의 미드스피드 라인으로의 업그레이드를 추진하는 브라질의 컨버터 업체들이 시장을 주도하고 있습니다. 아르헨티나에서는 신규 구매가 아닌 개보수를 통해 설비의 수명을 연장하고 있기 때문에 판매량 증가세가 둔화되고 있습니다. 아프리카는 약 5%의 점유율에 그치고 있어, 여전히 시장이 세분화되어 있습니다. 남아프리카와 이집트가 도입의 대부분을 차지하고 있지만, 대륙의 다른 지역에서는 브랜드화된 인쇄 포장재의 도입을 정당화할 수 있는 소매 인프라 구축과 물류 체계의 개선이 시급합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the gravure printing machines market size is expected to increase from USD 3.42 billion in 2025 to USD 3.46 billion in 2026 and reach USD 3.67 billion by 2031, growing at a CAGR of 1.17% over 2026-2031.

This report is Segmented by Application (Flexible Packaging, Label Manufacturing, Publication and Commercial Printing, Decorative Printing, and Industrial and Security Printing), Substrate Type (Plastic Films, Paper and Paperboard, Metallic Foils, and More), Printing Speed Class (Up To 200 M/Min, 201-350 M/Min, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Gravure Printing Machines Market Trends and Insights

Rising Demand for High-Quality Flexible Packaging in E-Commerce

Online retail continues to reshape packaging specifications, pushing converters toward gravure presses that deliver high-opacity graphics on downgauged films durable enough for automated fulfillment centers. Mid-width lines between 1,050 mm and 1,250 mm equipped with cart-mounted cylinder trolleys now change jobs in under 10 minutes, letting plants handle limited-edition batches of 10,000-20,000 linear meters without sacrificing color density. A new class of shaftless presses introduced in 2026 further elevates throughput to 500 m/min while maintaining tension on ultra-thin mono-material webs, a key requirement for meeting EU post-consumer-recycled content mandates. Brand owners in Asia-Pacific and North America prefer these lines because they combine premium shelf appeal with compliance to migration limits on food-contact films, ensuring product integrity throughout multi-modal distribution networks.

Technological Advancements in High-Speed and Automated Gravure Presses

Manufacturers have embedded servo drives, inline spectrophotometry, and cloud-based recipe libraries to eliminate the skilled-operator bottleneck that historically limited gravure to long runs. One flagship system measures optical density 9,500 times per second, holds ink viscosity within a 4 °C window, and completes makeready in under eight minutes, reducing ink waste by half. In China, newly launched lines integrate HD video inspection and independent deck motors to hit 500 m/min with +-10 µm register accuracy, a specification once reserved for European flagships. These automation gains push the economic crossover where gravure beats flexo down to roughly 5,000 m2, opening profitable space in medium runs and allowing the gravure printing machines market to penetrate segments traditionally served by flexography.

High Initial Capital Investment and Long Payback Period

Eight- to ten-color gravure lines with solvent recovery and color automation cost USD 3-5 million, while cylinder inventories can add another USD 500,000 for a mid-size SKU portfolio. Converters in emerging markets often struggle to secure that financing, especially when order volumes are volatile or denominated in weak local currencies. Even with automation that lowers the cost crossover to 5,000 m2, payback can exceed seven years without sustained 70-80% uptime. Refurbished presses and lower-cost Chinese models partially offset capex, but they also entail higher utility bills and longer makereadies, reinforcing the dilemma for small plants seeking to enter the premium flexible packaging.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Eco-Friendly Inks and Solvent Recovery Systems Driven by Regulations

- Expansion of Packaging Capacity in Emerging Asian Economies

- Intensifying Competition from Digital and Flexographic Printing for Short Runs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible packaging accounted for 55.05% of the gravure printing machines market in 2025, and gravure's high-opacity graphics on downgauged films remain indispensable for brand differentiation on crowded e-commerce shelves. Converters running lines between 1,050 mm and 1,250 mm have proven they can execute limited-edition drops profitably, trimming makeready from 45 minutes to under 10. The gravure printing machines market for flexible packaging continues to benefit from sustainability mandates that drive mono-material film adoption, as gravure's controlled ink lay-down maintains intact barrier properties.

Industrial and security printing is projected to expand at a 1.65% CAGR through 2031, outpacing all other uses. Pharmaceutical serialization laws and luxury goods' anti-counterfeiting requirements demand micro-engraved cylinders capable of sub-10 µm line widths, a feat beyond the capabilities of flexographic or digital methods. Converters serving these sectors invest in inline inspection cameras and closed-loop register control, ensuring production at 300 m/min without compromising code legibility. Publication gravure, by contrast, slipped below 8% of 2025 volume as magazines migrate to web offset, confirming a long-term secular decline.

Geography Analysis

Asia-Pacific accounted for 42.16% of the gravure printing machines market revenue in 2025. Chinese manufacturers dominate domestic demand and increasingly win orders abroad through competitive pricing, localized parts networks, and faster commissioning cycles. India's packaging majors are ramping up domestic press build under technology-transfer licenses, shrinking lead times to 14 weeks, and cutting duty exposure. Southeast Asian nations, Vietnam, Thailand, and Indonesia, benefit from multinationals' China-plus-one strategies, driving greenfield installations of 200-350 m/min lines tuned for aseptic pouches and retort applications.

The Middle East is the fastest-growing region, with a 1.97% CAGR through 2031, as Gulf Cooperation Council states diversify into value-added packaging. However, many plants are swapping mid-run gravure work for central-impression flexo, seeking faster turnarounds for goods bound to regional supermarkets. Europe commands about 28% of value, but aging assets must now meet VOC caps and chrome-free mandates, creating retrofit demand for solvent capture and trivalent plating. North America holds a notable share, where consolidation among flexible-packaging converters fuels interest in hybrid gravure-digital architectures compliant with serialization laws.

South America contributes a notable share of revenue, led by Brazilian converters upgrading to Chinese mid-speed lines as currency volatility discourages European imports. Argentina prolongs equipment life through retrofits rather than new buys, dampening volume growth. Africa, at about 5%, remains fragmented; South Africa and Egypt anchor most installs, while the rest of the continent awaits retail formalization and logistics upgrades that justify branded printed packs.

- Bobst Group SA

- Windmoller & Holscher KG

- Uteco Converting S.p.A.

- Shaanxi Beiren Printing Machinery Co., Ltd.

- Comexi Group Industries SAU

- Fuji Kikai Kogyo Co., Ltd.

- Officine Meccaniche Giovanni Cerutti S.p.A.

- Koenig & Bauer AG

- Rotatek S.A.

- Hsing Wei Machine Industry Co., Ltd.

- Shibaura Machine Co., Ltd.

- Weifang Donghang Graphic Technology Inc.

- Wenzhou Kingsun Machinery Industrial Co., Ltd.

- Pelican Rotoflex Pvt. Ltd.

- DCM Group

- Jiangyin Lida Printing & Packaging Machinery Co., Ltd.

- Weijin Machinery Industry Co., Ltd.

- Queen's Machinery Co., Ltd.

- HYPLAS Machinery Co., Ltd.

- J M Heaford Ltd.

- Qingdao Solna Printing Equipment Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High-Quality Flexible Packaging in E-Commerce

- 4.2.2 Technological Advancements in High-Speed and Automated Gravure Presses

- 4.2.3 Adoption of Eco-Friendly Inks and Solvent Recovery Systems Driven by Regulations

- 4.2.4 Expansion of Packaging Capacity in Emerging Asian Economies

- 4.2.5 Integration of Digital Gravure Modules for Short-Run Personalization

- 4.2.6 Growth in Anti-Counterfeiting Security Features Requiring Gravure Micro-Engraving

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investment and Long Payback Period

- 4.3.2 Intensifying Competition from Digital and Flexographic Printing for Short Runs

- 4.3.3 Volatility in Copper and Chromium Prices Affecting Cylinder Costs

- 4.3.4 Skilled Operator Shortage Leading to Production Bottlenecks

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Flexible Packaging

- 5.1.2 Label Manufacturing

- 5.1.3 Publication and Commercial Printing

- 5.1.4 Decorative Printing

- 5.1.5 Industrial and Security Printing

- 5.2 By Substrate Type

- 5.2.1 Plastic Films

- 5.2.2 Paper and Paperboard

- 5.2.3 Metallic Foils

- 5.2.4 Others (Textiles, Laminates)

- 5.3 By Printing Speed Class

- 5.3.1 Up to 200 m/min

- 5.3.2 201-350 m/min

- 5.3.3 More than 350 m/min

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Turkey

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bobst Group SA

- 6.4.2 Windmoller & Holscher KG

- 6.4.3 Uteco Converting S.p.A.

- 6.4.4 Shaanxi Beiren Printing Machinery Co., Ltd.

- 6.4.5 Comexi Group Industries SAU

- 6.4.6 Fuji Kikai Kogyo Co., Ltd.

- 6.4.7 Officine Meccaniche Giovanni Cerutti S.p.A.

- 6.4.8 Koenig & Bauer AG

- 6.4.9 Rotatek S.A.

- 6.4.10 Hsing Wei Machine Industry Co., Ltd.

- 6.4.11 Shibaura Machine Co., Ltd.

- 6.4.12 Weifang Donghang Graphic Technology Inc.

- 6.4.13 Wenzhou Kingsun Machinery Industrial Co., Ltd.

- 6.4.14 Pelican Rotoflex Pvt. Ltd.

- 6.4.15 DCM Group

- 6.4.16 Jiangyin Lida Printing & Packaging Machinery Co., Ltd.

- 6.4.17 Weijin Machinery Industry Co., Ltd.

- 6.4.18 Queen's Machinery Co., Ltd.

- 6.4.19 HYPLAS Machinery Co., Ltd.

- 6.4.20 J M Heaford Ltd.

- 6.4.21 Qingdao Solna Printing Equipment Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment