|

시장보고서

상품코드

2061887

직접 열전사 라벨 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Direct Thermal Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

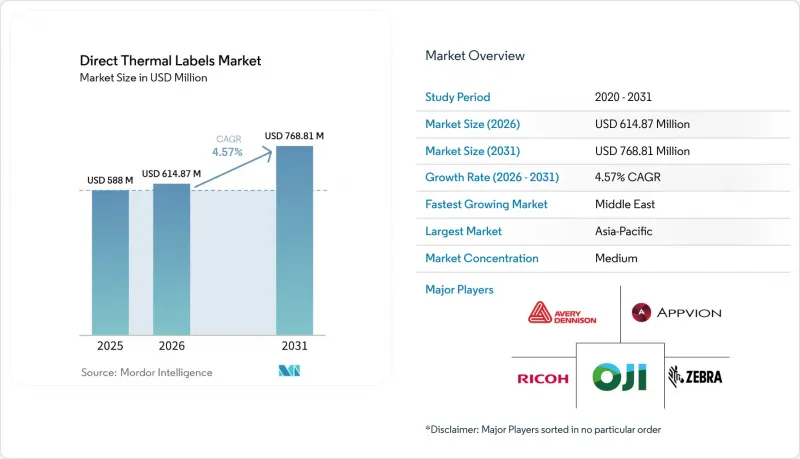

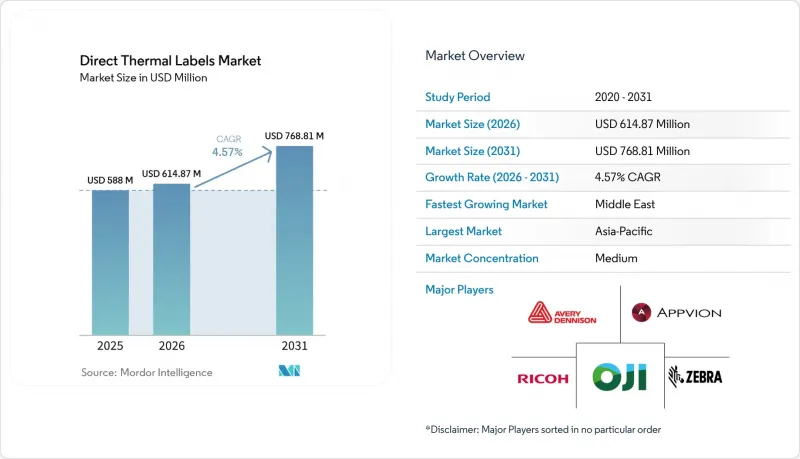

Mordor Intelligence에 의하면, 직접 열전사 라벨 시장은 2025년에 5억 8,800만 달러로 평가되었습니다. 2026년 6억 1,487만 달러에서 2031년까지 7억 6,881만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) 동안 CAGR 4.57%를 나타낼 전망입니다.

본 보고서는 소재 유형(종이 소재 및 합성 소재), 형태(롤, 팬폴드, 라이너리스), 최종 사용자 산업(물류 및 운송, 소매 및 전자상거래, 식품 및 음료, 의료 및 제약, 제조·산업, 기타 최종 사용자 산업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 직접 열전사 라벨 시장 동향 및 분석

전자상거래 물류 처리 확대로 온디맨드 라벨 인쇄가 가속화되고 있습니다.

아시아태평양의 소포 처리량은 2026년 512억 4,000만 달러에서 2035년에는 1,960억 9,000만 달러로 증가할 것으로 예상되며, 연평균 성장률(CAGR)은 16.08%를 나타낼 것으로 전망됩니다. 이로 인해 풀필먼트 센터는 일괄 배치 인쇄에서 실시간 인쇄로 전환할 수밖에 없게 되었습니다. 직접 열전사 방식은 리본 교체가 필요 없어 가동 중지 시간을 줄여줍니다. 이는 당일 배송 약속으로 인해 프린터 가동을 중단할 수 없는 상황에서 매우 중요합니다. 월마트가 하이브리드형 직접 서멀 및 RFID 라벨을 도입한 시범 프로그램에서는 재고 정확도 99%를 달성했으며, 바코드와 태그의 통합을 통한 생산성 향상 효과가 입증되었습니다. 현재, 배송업체용 라벨 API에는 결제 시 바코드 생성 기능이 탑재되어 있어, 판매자는 단 몇 밀리초 만에 정확한 배송 라벨을 인쇄할 수 있게 되었습니다. 이러한 소프트웨어 중심의 워크플로는 열전사 리본으로는 구현하기 어렵기 때문에 소포 물량 증가는 직접적으로 새로운 직접 열전사 프린터의 도입으로 이어지고 있으며, 가장 바쁜 지점에서는 교체 주기가 18개월에서 12개월 미만으로 단축되었습니다.

엄격한 의약품 추적성 규제

2025년에 발행된 사우디아라비아 식품의약청(SFDA)의 템플릿에서는 GS1 GTIN, 아랍어와 영어로 된 이중 언어 텍스트, 그리고 DataMatrix 코드의 표기를 의무화하고 있으며, 수탁 제조업체에 대해 분당 300개 이상의 속도로 가변 데이터를 인쇄할 수 있는 시스템을 도입할 것을 요구하고 있습니다. 아랍에미리트(UAE) 보건부는 글자 높이를 최소 1.6mm로 규정하고 12가지 필수 데이터 요소를 명시하고 있으며, 요르단 역시 이와 유사한 이중 언어 표기 규정을 시행하고 있습니다. 감열 프린터는 리본을 미리 감을 필요 없이 즉시 인쇄를 시작할 수 있으므로, 로트 전환 시마다 15-20초의 시간을 절약할 수 있습니다. 미국 FDA의 단계적인 전미 의약품 코드(NDC) 전환은 2033년까지 계속될 예정이므로, 변환기는 전환 기간 동안 10자리와 12자리 코드 모두를 지원해야 합니다. 리본 사용이 처리 능력을 제한하기 때문에 제약 업계에서는 단위별 일련번호 부여를 위해 직접 열전사 방식의 설비 도입이 진행되고 있으며, 이러한 추세는 2020년대 말까지 장비 및 소모품 판매량을 뒷받침할 것으로 보입니다.

감열지 원지 가격 변동

케일러, 돔터, 한솔은 2026년 3월, 전 세계 감열지 가격을 10% 인상했습니다. 그 이유로 운송 차질, 석유화학제품 가격 급등, 그리고 OBD-2 루코 염료 현상제의 구조적 부족을 꼽고 있습니다. OBD-2의 세계 수요는 6,000-7,000톤 수준인 반면, 생산 능력은 3,000톤 미만에 그치고 있어 현물 가격은 톤당 100만 위안(14만 달러)을 상회하고 있습니다. 2025년 말에는 펄프 비용이 18% 상승했고, 유럽의 제지 공장에서는 에너지 요금이 25-30% 급등함에 따라 제지 가공업체의 이익률이 압박받았습니다. 일부 중견 공급업체들은 소매업체와의 고정 가격 계약 재협상에 실패하여 시장에서 철수했습니다. 아시아의 새로운 코팅지 생산 라인은 2027년 하반기까지 가동되지 않을 예정이므로, 제지 업체들은 적어도 앞으로 2년 동안은 불안정한 원자재 비용 문제에 대처해야 합니다.

부문별 분석

2025년, 직접 열전사 라벨 시장에서 종이 재질 페이스 스톡의 점유율은 61.23%를 차지했습니다. 이는 저렴한 가격과 기존 프린터와의 호환성 덕분입니다. 합성 페이스 스톡은 가격이 비싸지만, 콜드체인 물류 및 시리얼화 도입으로 내구성에 대한 요구가 높아짐에 따라 2031년까지 연평균 4.69%의 성장률이 예상됩니다. 소매업체들은 라벨의 수명이 불과 30일에 불과한 단거리 배송 소포에는 여전히 종이를 사용하고 있지만, 유럽의 냉동식품 유통업체들은 합성 라벨로 전환한 후 교체 비용이 40% 절감되었다고 보고하고 있습니다. 폴리올레핀 필름의 가격 격차가 좁혀지고 있어, 합성 소재와 관련된 직접 열전사 라벨 시장 규모가 확대되고 있습니다. 그러나 합성 소재는 탄성 계수가 높기 때문에 정확한 플레이트 압력이 필요하며, 장력을 조절할 수 없는 프린터의 경우 여전히 종이 롤이 사용되고 있습니다.

의약품, 생명공학 및 야외 물류 분야에서는 현재 가격보다 내구성이 소재 선택을 좌우하고 있습니다. 이 합성 소재는 -40℃에서 +80℃에 이르는 온도 변화를 견디며, 습기에도 강해 저온실이나 습기가 많은 창고에서 종이 라벨에 흔히 발생하는 뒤틀림이나 박리 문제를 해결합니다. 에이버리 데니슨의 RFID 지원 인몰드 합성 라벨은 재사용 가능한 토트백이 라벨이 떨어지지 않은 채로 여러 번의 세척 과정을 견딜 수 있음을 입증했습니다. 그럼에도 불구하고, 컨버터가 두꺼운 소재를 처리하는 데 필요한 새로운 슬리팅 라인 및 검사 라인에 대한 투자 비용을 회수하기 전까지는 합성 미디어는 틈새 시장 제품으로 남아 있을 것입니다.

지역별 분석

아시아태평양은 2025년 전 세계 매출의 33.15%를 차지했습니다. 이는 2026년 512억 4,000만 달러에서 2035년에는 1,960억 9,000만 달러로 급증할 것으로 예상되는 전자상거래 포장 시장의 성장에 힘입은 것입니다. 중국은 여전히 최대 구매국이며, 인도는 가장 빠르게 성장하는 시장입니다. 또한, 동남아시아의 식료품 플랫폼에서는 열대 기후의 더위를 견디기 위해 합성 소재로의 전환이 진행되고 있습니다. GS1 Sunrise 2027 및 소매업체의 RFID 시범 프로젝트를 통해, 인쇄와 인코딩을 동시에 처리해야 하는 풀필먼트 허브에서 직접 열전사 인쇄 및 인코딩에 대한 수요가 증가하고 있습니다.

중동은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.11%를 기록하며 가장 빠르게 성장하는 하위 지역이 될 것으로 전망됩니다. 사우디아라비아의 이중 언어 지원 GS1 바코드 규정, UAE의 1.6mm 글자 크기 요건, 요르단의 일련번호 부여 프로그램으로 인해 의약품 라벨 수요가 확대되고 있습니다. ‘비전 2030’의 의료 분야 투자 및 신설 의약품 제조 거점에서는 분당 300장 이상의 라인 속도로 일련번호 인쇄가 가능한 프린터가 요구되고 있습니다. 홍해에서의 운송 차질과 원자재 가격 급등이 겹치면서, 켈러사를 비롯한 각사가 2026년 3월에 종이 가격을 인상한 배경이 되었으나, 제지 가공업체들은 2027년 하반기에 아시아의 새로운 코팅 라인이 가동되기 시작해야 비로소 상황이 완화될 것으로 전망하고 있습니다.

유럽과 북미에서는 상반된 추세가 나타나고 있습니다. 월마트는 2026년 말까지 미국 내 매장에서 종이 가격표를 디지털 가격표로 교체해 매장 내 종이 사용량을 줄이는 한편, 물류 센터에서는 하이브리드형 직접 열전사 라벨에 의존하는 RFID 의무화 범위를 확대되고 있습니다. 2026년 8월에 시행될 EU 규정은 라이너리스 방식의 채택을 권장하고 있으며, 2026년 5월에 출시된 UPM의 ‘ProCycle’ 워시오프 접착제는 이러한 요건을 충족하는 것을 목표로 하고 있습니다. 남미와 아프리카에서는 규제가 통일되어 있지 않고 가격에 대한 민감도가 높아, 장거리 운송에는 여전히 열전사 방식이 매력적인 선택지이기 때문에 도입이 더딘 상황입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the direct thermal labels market was valued at USD 588 million in 2025 and is estimated to grow from USD 614.87 million in 2026 to reach USD 768.81 million by 2031, growing at a CAGR of 4.57% during the forecast period (2026-2031).

This report is Segmented by Material Type (Paper Facestock, and Synthetic Facestock), Form Factor (Rolls, Fan-Fold, and Linerless), End-User Industry (Logistics and Transportation, Retail and E-Commerce, Food and Beverage, Healthcare and Pharmaceuticals, Manufacturing and Industrial, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Direct Thermal Labels Market Trends and Insights

E-Commerce Fulfilment Growth Accelerates On-Demand Label Printing

Parcel volume in Asia-Pacific is projected to climb from USD 51.24 billion in 2026 to USD 196.09 billion by 2035, a 16.08% compound annual growth rate that forces fulfillment centers to switch from bulk batches to real-time printing. Direct thermal eliminates ribbon changes and reduces downtime, which is critical when same-day delivery commitments leave no tolerance for printer stoppages. Walmart's use of hybrid direct thermal and RFID labels achieved 99% inventory accuracy in a pilot program, validating the productivity upside of integrated barcoding and tagging. Carrier-label APIs now embed barcode generation at checkout, letting merchants print the correct service label in milliseconds. These software-driven workflows are unlikely with thermal-transfer ribbons, so parcel growth is directly translating into new direct thermal printer installations, trimming replacement cycles from 18 months to under 12 months in the busiest nodes.

Stringent Pharmaceutical Traceability Mandates

The Saudi Food and Drug Authority template, issued in 2025, requires GS1 GTINs, bilingual Arabic-English text, and DataMatrix codes, pushing contract manufacturers to adopt variable-data printing at rates above 300 units per minute. The UAE Ministry of Health requires a minimum text height of 1.6 mm and 12 mandatory data elements, while Jordan enforces similar bilingual rules. Direct thermal printers start instantly without ribbon pre-feed, saving 15-20 seconds on every batch changeover. The United States FDA's phased National Drug Code migration extends through 2033, so converters must handle both 10-digit and 12-digit codes during transition. Because ribbon handling limits throughput, pharmaceutical lines are retooling around direct thermal for unit-level serialization, a trend likely to support equipment sales and consumables volume through the end of the decade.

Volatility in Thermal-Paper Base Prices

Koehler, Domtar, and Hansol raised global thermal paper prices by 10% in March 2026, blaming shipping disruptions, petrochemical inflation, and a structural shortage of OBD-2 leuco-dye developer. Global demand for OBD-2 stands near 6,000-7,000 tons while capacity remains below 3,000 tons, sending spot prices above RMB 1,000,000 (USD 0.14 million) per ton. Pulp costs climbed 18% in late 2025, and European mills faced 25-30% higher energy bills, squeezing converter margins. Some mid-tier suppliers exited the market after failing to renegotiate fixed-price contracts with retailers. New Asian coating lines will not arrive until late 2027, so converters must cope with unstable input costs for at least two more years.

Other drivers and restraints analyzed in the detailed report include:

- Integration of QR and RFID Features for Smart Logistics

- Cost-Efficient No-Ribbon Printing Lowers Total Ownership

- Fading and Image-Stability Limitations in Harsh Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper facestock accounted for 61.23% of the direct thermal label market share in 2025, driven by its low price and compatibility with legacy printers. Synthetic facestock, although more expensive, is forecast to grow at 4.69% through 2031 as cold-chain logistics and serialization raise durability requirements. Retailers continue to use paper for short-haul parcels, where labels last only 30 days, but frozen-food distributors in Europe reported a 40% reduction in replacement costs after shifting to synthetic labels. The direct thermal labels market size tied to synthetics is enlarging as polyolefin films narrow the price gap. However, synthetic's higher modulus demands precise platen pressure, so printers unable to adjust tension still default to paper rolls.

Durability rather than price now dictates substrate choice in pharmaceuticals, biotech, and outdoor logistics. Synthetic stock resists -40 °C to +80 °C swings and defies moisture, solving the curl and peel seen with paper in cold rooms or humid depots. Avery Dennison's RFID-enabled in-mold synthetic labels demonstrate that reusable totes can withstand multiple wash cycles without delamination. Even so, synthetic media remains niche until converters amortize the new slitting and inspection lines required to handle thicker calipers.

Geography Analysis

Asia-Pacific accounted for 33.15% of 2025 global revenue, supported by e-commerce packaging, which is projected to jump from USD 51.24 billion in 2026 to USD 196.09 billion by 2035. China remains the largest buyer, India the fastest grower, and Southeast Asian grocery platforms are shifting to synthetic stock to withstand tropical heat. GS1 Sunrise 2027 and retailers' RFID pilots are driving demand for direct thermal printing and encoding in fulfillment hubs that require simultaneous printing and encoding capability.

The Middle East is forecast to be the fastest-growing sub-region, with a 5.11% CAGR over 2026-2031. Saudi Arabia's bilingual GS1 barcode rule, the UAE's 1.6 mm text requirement, and Jordan's serialization program are expanding pharmaceutical label volume. Vision 2030 healthcare investment and new drug-manufacturing sites require serialization-ready printers at line speeds exceeding 300 units per minute. Shipping disruptions in the Red Sea, combined with raw-material inflation, explain why Koehler and peers raised paper prices in March 2026, but converters expect relief only after new Asian coating lines start in late 2027.

Europe and North America face mixed trends. Walmart will replace paper shelf tags with digital price labels across all US stores by end-2026, trimming in-store paper volume, yet the same retailer is expanding RFID mandates that rely on hybrid direct thermal labels at distribution centers. The EU regulation, effective in August 2026, favors the adoption of linerless, and UPM's ProCycle wash-off adhesive, launched in May 2026, targets that requirement. South America and Africa trail in uptake because fragmented rules and price sensitivity keep thermal transfer attractive for longer-life shipments.

- Avery Dennison Corporation

- Appvion Operations Inc.

- Zebra Technologies Corporation

- Oji Holdings Corporation

- Ricoh Company Ltd.

- CCL Industries Inc.

- Honeywell International Inc.

- 3M Company

- SATO Holdings Corporation

- UPM-Kymmene Oyj (UPM Raflatac)

- Brady Corporation

- Brother Industries, Ltd.

- Seiko Epson Corporation

- Fuji Seal International, Inc.

- Multi-Color Corporation

- WS Packaging Group, Inc.

- Resource Label Group, LLC

- LINTEC Corporation

- DNP Imagingcomm Co., Ltd.

- TSC Auto ID Technology Co., Ltd.

- BIXOLON Co., Ltd.

- Label Technology, Inc.

- R. R. Donnelley & Sons Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfillment Growth Accelerates On-Demand Label Printing

- 4.2.2 Stringent Pharmaceutical Traceability Mandates

- 4.2.3 Cost-Efficient No-Ribbon Printing Lowers Total Ownership

- 4.2.4 Rise of Linerless Sustainability Standards in Retail

- 4.2.5 Integration of QR and RFID Features for Smart Logistics

- 4.2.6 Expansion of Cold-Chain Food Delivery Services

- 4.3 Market Restraints

- 4.3.1 Volatility in Thermal Paper Base Prices

- 4.3.2 Fading and Image Stability Limitations in Harsh Environments

- 4.3.3 Growing Adoption of Digital Labeling and RFID Tags

- 4.3.4 Capital Expense for Linerless Conversion Equipment

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Paper Facestock

- 5.1.2 Synthetic Facestock

- 5.2 By Form Factor

- 5.2.1 Rolls

- 5.2.2 Fan-fold

- 5.2.3 Linerless

- 5.3 By End-user Industry

- 5.3.1 Logistics and Transportation

- 5.3.2 Retail and E-commerce

- 5.3.3 Food and Beverage

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Manufacturing and Industrial

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Turkey

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Avery Dennison Corporation

- 6.4.2 Appvion Operations Inc.

- 6.4.3 Zebra Technologies Corporation

- 6.4.4 Oji Holdings Corporation

- 6.4.5 Ricoh Company Ltd.

- 6.4.6 CCL Industries Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 3M Company

- 6.4.9 SATO Holdings Corporation

- 6.4.10 UPM-Kymmene Oyj (UPM Raflatac)

- 6.4.11 Brady Corporation

- 6.4.12 Brother Industries, Ltd.

- 6.4.13 Seiko Epson Corporation

- 6.4.14 Fuji Seal International, Inc.

- 6.4.15 Multi-Color Corporation

- 6.4.16 WS Packaging Group, Inc.

- 6.4.17 Resource Label Group, LLC

- 6.4.18 LINTEC Corporation

- 6.4.19 DNP Imagingcomm Co., Ltd.

- 6.4.20 TSC Auto ID Technology Co., Ltd.

- 6.4.21 BIXOLON Co., Ltd.

- 6.4.22 Label Technology, Inc.

- 6.4.23 R. R. Donnelley & Sons Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment