|

시장보고서

상품코드

2061900

동박적층판(CCL) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Copper Clad Laminate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

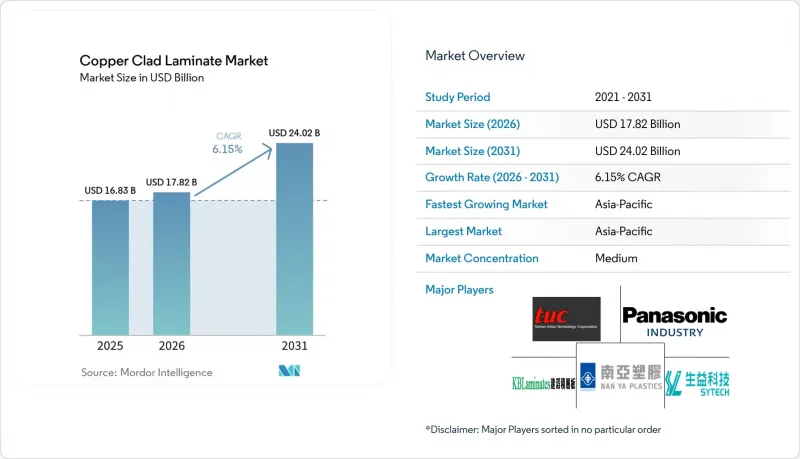

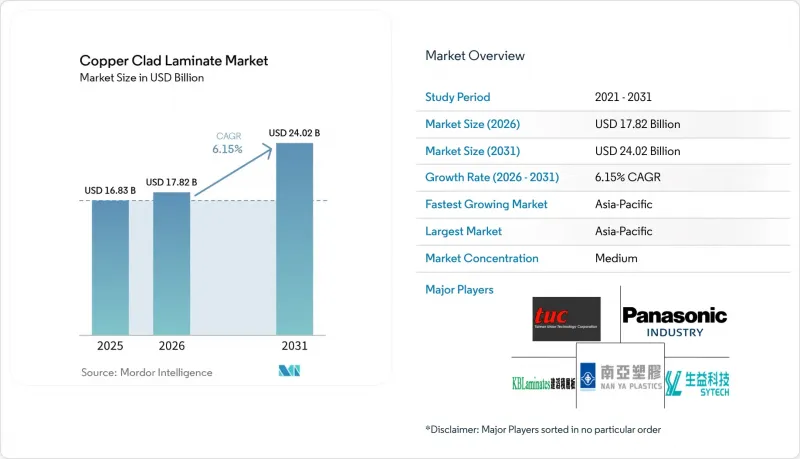

Mordor Intelligence에 의하면, 동박적층판(CCL) 시장 규모는 2025년에 168억 3,000만 달러로 평가되었습니다. 2026년 178억 2,000만 달러에서 2031년까지 240억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.15%를 나타낼 전망입니다.

본 보고서는 수지 유형(에폭시, 페놀, 폴리이미드 등), 형태(리지드 및 플렉서블), 보강재(유리 섬유 직물, 종이 계열 등), 용도(가정용 전자기기, 통신 시스템 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 동박적층판(CCL) 시장 동향 및 분석

전자제품 및 PCB에 대한 견조한 수요가 근본적인 성장을 견인

인도의 전자기기 생산액은 2015 회계연도(FY 2015)의 19조 루피(296억 달러)에서 2024 회계연도(FY 2024)에는 95.2조 루피(1,130억 달러)로 증가하여, 국내 PCB 수요를 높여, 동박적층판(CCL) 시장을 견인하고 있습니다. 2026년 1월 ‘전자 부품 제조 계획’에 따라 승인된 22개 프로젝트를 통해, 국내 라미네이트 및 PCB(인쇄 회로 기판) 공장에 4만 1,863 카롤 루피(44억 3,800만 달러) 규모의 투자가 이루어졌습니다. 저비용 FR-4가 가격 압박에 직면한 상황에서도, 다층 HDI(고밀도 배선) 기판으로의 통합을 추진하는 공급업체들은 더 높은 이익률을 확보하고 있습니다.

5G 네트워크 인프라 구축 가속화가 고주파 CCL 채택을 뒷받침

5G 기지국 건설에는 24-77GHz 대역에서 유전 손실이 0.005 미만인 적층 기판이 필요하며, 이 틈새 시장에는 RO3003 및 RO4830 Plus 시리즈가 대응하고 있습니다. 대만 유니온 테크놀로지의 무할로겐이자 탄소 중립적인 소재에 대한 연구 개발은 통신 사업자들이 성능과 지속가능성 모두를 추구하고 있음을 여실히 보여주고 있습니다. 초기 단계의 6G 연구 결과, 서브 THz 대역에서 작동하는 폴리이미드 필름 시제품이 이미 개발되었으나, 실용화 수준은 TRL 3-6에 그치고 있습니다.

구리 및 석유계 수지의 가격 변동이 이익률을 압박하고 있습니다.

런던 금속 거래소(LME)의 구리 가격은 2024년에 톤당 1만 3,842달러 가까이까지 치솟은 후 안정세를 보였습니다. 또한, 에폭시 수지의 원자재 비용은 유가 변동과 아시아태평양공급망 혼란을 배경으로 2025년까지 연평균 7-10% 상승했습니다. 레조낙 홀딩스는 2026년 3월부터 30%의 가격 인상을 단행했으며, 킹보드 라미네이츠와 난아 플라스틱도 2025년에 여러 차례 가격 조정을 실시했으나, 이러한 조치는 원자재 비용의 급등보다 3-6개월 늦게 이루어졌기 때문에 그동안 매출총이익률은 압박을 받고 있습니다. 동박이나 수지 생산에 대한 수직 통합을 실시하지 않는 중소 CCL 제조업체들은 심각한 취약성에 직면해 있습니다. 고정가격 계약을 협상할 만한 규모가 부족하여, 비용 상승분을 하류 단계에 전가하지 않고 자체적으로 흡수할 수 없기 때문에 가격 안정성을 제공할 수 있는 대형 경쟁사에게 시장 점유율을 빼앗길 위험이 있습니다.

부문별 분석

에폭시는 2025년 생산량의 65.66%를 차지하며, 가전제품용 범용 기판을 뒷받침했지만, 항공우주 분야나 플렉서블 전자기기에서는 250°C까지의 내구성이 요구되기 때문에 폴리이미드는 2031년까지 연평균 성장률(CAGR) 7.12%로 더욱 급속한 성장을 이루고 있습니다. 특수 불소 수지 등급은 규모는 작지만, mm파 및 레이더의 요구 사항을 충족함으로써 에폭시 수지보다 3-5배 높은 가격을 실현하고 있습니다. Shengyi 등 공급업체들은 임베디드 커패시터가 탑재된 서버의 수주를 확보하기 위해 PTFE 생산 능력을 통합하고 있으며, 이는 수지 선택이 이익률의 폭을 결정한다는 점을 여실히 보여주고 있습니다.

현재 고성능 블렌드에서는 열팽창 계수(CTE)의 차이를 줄이기 위해 에폭시와 PPO를 조합하여 다층 서버 기판에 대응하고 있습니다. 단면 용도가 줄어들면서 페놀 수지나 종이 기반 제품의 사용도 감소하는 추세입니다. Arlon사의 85N이나 파나소닉의 HIPER 시리즈와 같은 복합 수지의 출시로 항공우주 및 전기차 인버터 분야의 틈새 시장을 선점했으며, 이는 원자재 가격 변동 시 공급업체가 가격 결정력을 유지하는 데 도움이 되고 있습니다.

2025년 매출에서 리지드 제품이 차지하는 비중은 78.21%였으나, 폴더블 스마트폰 및 웨어러블 기기의 보급에 힘입어 플렉서블 라미네이트 시장은 2031년까지 연평균 성장률(CAGR) 7.34%로 확대되고 있습니다. 두산(Doosan)의 FCCL은 100만 회 이상의 굽힘을 견딜 수 있는 내구성을 보여주고 있으며, 한편 타이플렉스(Taiflex)의 3,500만 달러 규모 태국 공장은 자동차 내장재 및 디스플레이 모듈 수요를 뒷받침하게 될 것입니다.

리지드-플렉스 하이브리드 제품은 의료기기 및 로봇 공학 분야로 확대되고 있으며, 2-3배의 비용 프리미엄이 요구되고 있습니다. 초박형 구리박 가공 및 접착제가 필요 없는 라미네이팅 기술을 습득한 공급업체는 설계 채택 후에도 안정적인 공급을 보장하고 있습니다. 한편, 대형 리지드 기판 제조업체들은 자체 생산한 유리 섬유와 구리박을 통해 규모의 경제를 유지하고 있으며, 범용 FR-4 기판에 대한 적극적인 가격 책정을 통해 시장 점유율을 지키고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 35.38%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.78%를 나타낼 것으로 전망됩니다. 태국과 인도만 보더라도 인센티브를 바탕으로 한 투자 계획이 발표되어, 현지 라미네이트 수요를 견인하고 있습니다. 중국은 여전히 최대의 소비 기반을 유지하고 있지만, 지정학적 변화로 인해 대만과 중국 본토의 기업들이 동남아시아로 진출하고 있으며, 2026년에는 태국의 PCB 점유율이 전 세계 전체의 5%를 넘어설 것으로 예측됩니다.

북미와 유럽은 항공우주, 방위, 하이퍼스케일 데이터센터를 배경으로, 합쳐서 전 세계 매출의 약 절반을 차지했습니다. AGC Multi Material America는 미국공급 안정성을 강화하기 위해 Tritek을 통해 유통망을 확대했습니다. EU의 탄소 정책은 규정 준수 기준을 높여 놓았기 때문에 할로겐 무함유화 및 재생에너지로의 전환에 자금을 투입할 수 있는 대형 기존 기업들이 유리한 입장에 있습니다.

2025년 기준으로 남미와 중동 및 아프리카의 점유율이 가장 낮았습니다. 브라질 자동차 시장의 회복과 걸프 지역 국가들의 통신 프로젝트는 미개척 분야에서 성장 기회를 제공하고 있지만, 인프라 격차와 원자재 부족이 단기적인 시장 침투를 저해하고 있습니다. 지역 제조 생태계가 성숙해짐에 따라, 현지에서 기술 지원을 제공하는 선도 기업들은 고객의 충성도를 확보할 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the copper clad laminate market size was valued at USD 16.83 billion in 2025 and is estimated to grow from USD 17.82 billion in 2026 to reach USD 24.02 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Epoxy, Phenolic, Polyimide, and More), Form Type (Rigid and Flexible), Reinforcement Material (Fiberglass Fabric, Paper-Based, and More), Application (Consumer Electronics, Communication Systems, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Copper Clad Laminate Market Trends and Insights

Robust Demand for Electronics and PCB Drives Baseline Growth

India's electronics output climbed from INR 1.90 lakh crore (USD 29.6 billion) in FY 2015 to INR 9.52 lakh crore (USD 113 billion) in FY 2024, raising local PCB requirements and boosting the Copper Clad Laminate market. Twenty-two projects cleared under the Electronics Component Manufacturing Scheme in January 2026 unlocked INR 41,863 crore (USD 4.438 billion) of investment aimed at domestic laminate and PCB (Printed Circuit Board) plants. Suppliers integrating into high-layer HDI (High-Density Interconnect) boards capture stronger margins even as low-cost FR-4 faces price pressure.

Acceleration of 5G Network Infrastructure Rollout Fuels High-Frequency CCL Adoption

5G base-station builds require laminates with dielectric loss below 0.005 across 24-77 GHz, a niche addressed by RO3003 and RO4830 Plus families. Taiwan Union Technology's R&D for halogen-free, carbon-neutral materials underscores how carriers seek both performance and sustainability. Early 6G research is already prompting prototypes of polyimide films operating in the sub-THz band, though readiness sits at TRL 3-6.

Copper and Petroleum-Based Resin Price Volatility Compresses Margins

Copper prices on the London Metal Exchange peaked near USD 13,842 per tonne in 2024 before moderating, and epoxy resin feedstock costs rose 7-10% annually through 2025, driven by petroleum price swings and supply-chain disruptions in Asia-Pacific. Resonac Holdings implemented a 30% price increase effective March 2026, and Kingboard Laminates and Nan Ya Plastics executed multiple price adjustments in 2025, yet these actions lag raw-material cost spikes by 3-6 months, compressing gross margins during the interim. Smaller CCL manufacturers without vertical integration into copper foil or resin production face acute vulnerability: they lack the scale to negotiate fixed-price contracts and cannot absorb cost inflation without passing it downstream, which risks losing share to larger competitors who can offer price stability.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Electrification and ADAS Penetration Reshape Material Specifications

- AI-Server Boards Demand Ultra-Thin Embedded-Capacitance CCL

- Stricter Global EHS and Carbon-Footprint Regulations Elevate Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy held 65.66% of 2025 volume, anchoring commodity boards for consumer devices, yet polyimide captured faster growth with a 7.12% CAGR through 2031 as aerospace and flexible electronics seek durability to 250°C. Specialty fluoropolymer grades, though small, earn 3-5 times epoxy prices by meeting mmWave and radar requirements. Suppliers such as Shengyi integrate PTFE capability to secure embedded-capacitance server wins, highlighting how resin choice determines margin bands.

High-performance blends now pair epoxy with PPO to reduce CTE mismatch, supporting multi-layer server boards. Phenolic and paper-based products are declining as single-sided applications fade. Composite resin launches, including Arlon's 85N and Panasonic's HIPER series, capture aerospace and EV inverter niches and help suppliers defend pricing power during raw-material swings.

Rigid products contributed 78.21% of 2025 revenue, yet flexible laminates are pacing at a 7.34% CAGR to 2031, owing to foldable phones and wearables. Doosan's FCCL demonstrates durability over 1 million folds, while Taiflex's USD 35 million Thailand plant will support automotive interiors and display modules.

Rigid-flex hybrids are spreading into medical devices and robotics, commanding a 2-3 times cost premium. Suppliers that master ultra-thin copper handling and adhesive-less lamination secure design-win stickiness. Meanwhile, large rigid producers defend scale economies through in-house glass fabric and copper foil, allowing aggressive pricing in commodity FR-4 to protect share.

Geography Analysis

Asia-Pacific generated 35.38% of 2025 revenue and is projected to rise at a 7.78% CAGR through 2031. Thailand and India alone have announced incentive-led investments, catalyzing local laminate demand. China maintains the largest consumption base, yet geopolitical shifts are steering Taiwanese and mainland firms to Southeast Asia, with Thailand's PCB share expected to top 5% globally in 2026.

North America and Europe together accounted for about half of global revenue, owing to aerospace, defense, and hyperscale data centers. AGC Multi Material America expanded distribution through Tritek to fortify UnitedStates supply security. EU carbon policies elevate compliance hurdles, favoring large incumbents that can fund halogen-free and renewable power upgrades.

South America and the Middle East & Africa held the lowest share in 2025. Brazil's vehicle rebound and Gulf-state telecom projects offer white-space growth, but infrastructure gaps and limited upstream feedstocks temper near-term penetration. Early movers that provide local technical support may capture loyalty as regional manufacturing ecosystems mature.

- AGC Inc.

- Chang Chun Group

- Doosan Corporation Electro-Materials

- Elite Material Co., Ltd.

- Goldenmax International Technology Ltd.

- Grace Electron

- Guangdong Chaohua Technology Co., Ltd.

- Isola Group

- ITEQ CORPORATION

- Kingboard Laminates Holdings Ltd.

- NAN YA PLASTICS CORPORATION

- Panasonic Industry Co., Ltd.

- Resonac Holdings Corporation

- Rogers Corporation

- Shandong Jinbao Electronics Co., Ltd.

- SHENGYI TECHNOLOGY CO., LTD.

- Sumitomo Bakelite Co., Ltd.

- Sytech Technology Co., Ltd.

- TACONIC

- Taiwan Union Technology Corporation

- Ventec International Group

- ZHEJIANG WAZAM NEW MATERIALS CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust demand for electronics and PCB

- 4.2.2 Acceleration of 5G network infrastructure rollout

- 4.2.3 Automotive electrification and ADAS penetration

- 4.2.4 AI-server boards need ultra-thin embedded-capacitance CCL

- 4.2.5 Rise of GaN/SiC power modules needing high-thermal CCL

- 4.3 Market Restraints

- 4.3.1 Copper and petroleum-based resin price volatility

- 4.3.2 Stricter global EHS and carbon-footprint regulations

- 4.3.3 CAPEX inflation for next-gen press and plasma lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Phenolic

- 5.1.3 Polyimide

- 5.1.4 Polyester

- 5.1.5 Fluoropolymer / PTFE

- 5.1.6 Polyphenylene Ether (PPE)

- 5.1.7 Polyphenylene Oxide (PPO)

- 5.1.8 Others

- 5.2 By Form Type

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 By Reinforcement Material

- 5.3.1 Fiberglass Fabric

- 5.3.2 Paper-based

- 5.3.3 Composite / Aramid / LCP

- 5.3.4 Other Materials

- 5.4 By Application

- 5.4.1 Communication Systems

- 5.4.2 Consumer Electronics

- 5.4.3 Automotive Electronics and EV Powertrain

- 5.4.4 Industrial and Power Electronics

- 5.4.5 Data-centre and AI Servers

- 5.4.6 Aerospace and Defense

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Chang Chun Group

- 6.4.3 Doosan Corporation Electro-Materials

- 6.4.4 Elite Material Co., Ltd.

- 6.4.5 Goldenmax International Technology Ltd.

- 6.4.6 Grace Electron

- 6.4.7 Guangdong Chaohua Technology Co., Ltd.

- 6.4.8 Isola Group

- 6.4.9 ITEQ CORPORATION

- 6.4.10 Kingboard Laminates Holdings Ltd.

- 6.4.11 NAN YA PLASTICS CORPORATION

- 6.4.12 Panasonic Industry Co., Ltd.

- 6.4.13 Resonac Holdings Corporation

- 6.4.14 Rogers Corporation

- 6.4.15 Shandong Jinbao Electronics Co., Ltd.

- 6.4.16 SHENGYI TECHNOLOGY CO., LTD.

- 6.4.17 Sumitomo Bakelite Co., Ltd.

- 6.4.18 Sytech Technology Co., Ltd.

- 6.4.19 TACONIC

- 6.4.20 Taiwan Union Technology Corporation

- 6.4.21 Ventec International Group

- 6.4.22 ZHEJIANG WAZAM NEW MATERIALS CO., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 High-frequency (mmWave), 5G and Automotive Growth Nodes

- 7.3 Capacity Expansion in Emerging Manufacturing Hubs