|

시장보고서

상품코드

2061902

텍스타일 프린터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Textile Printers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

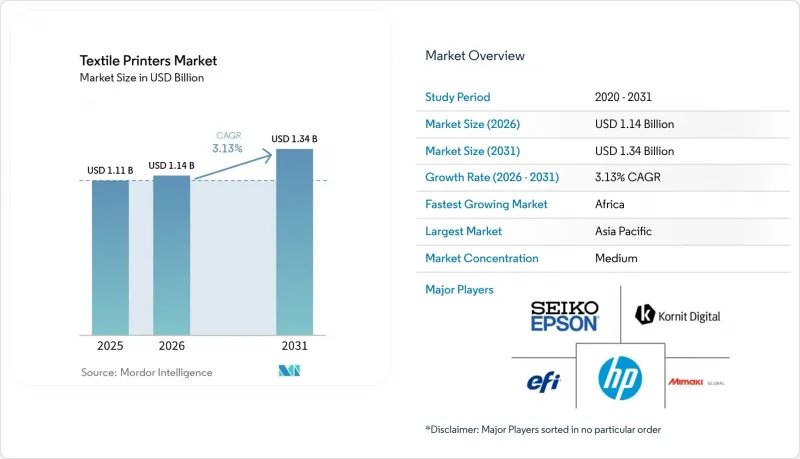

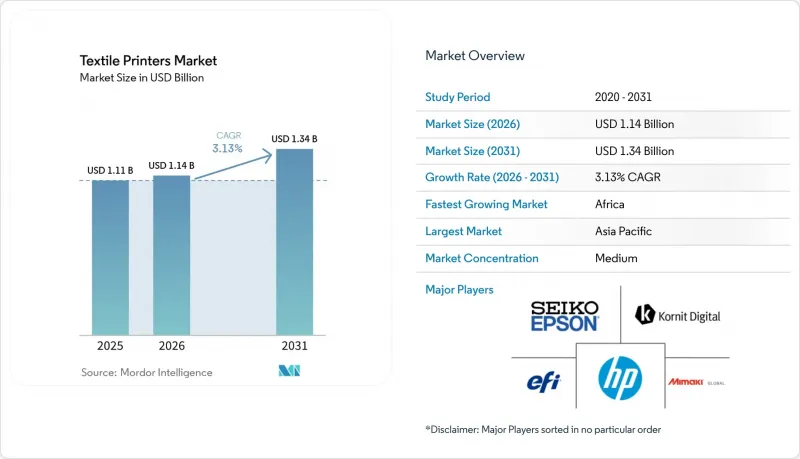

Mordor Intelligence에 의하면, 텍스타일 프린터 시장 규모는 2025년에 11억 1,000만 달러로 평가되었습니다. 2026년 11억 4,000만 달러에서 2031년까지 13억 4,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 3.13%를 나타낼 전망입니다.

본 보고서는 인쇄 기술(디지털 잉크젯 인쇄, 스크린 인쇄 등), 잉크 유형(반응성 염료 잉크, 산성 염료 잉크, 안료 잉크, 분산 염료 잉크 및 승화 잉크 등), 용도(의류, 홈 텍스타일, 간판·디스플레이 그래픽 등), 원단(면, 폴리에스터, 실크 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 텍스타일 프린터 시장 동향 및 인사이트

패스트 패션 및 맞춤형 의류에 대한 수요 증가

계절별 컬렉션 대신 주 단위로 소량 출시하는 방식이 주류를 이루면서, 아날로그 스크린으로는 대응할 수 없는 소량 주문에 대한 수요가 증가하고 있습니다. 디지털 기기의 도입으로 판 조각 공정이 불필요해지고, 몇 분 만에 패턴을 변경할 수 있게 됨에 따라 유럽 브랜드들은 신속한 재고 보충을 위해 생산을 니어쇼어화할 수 있게 되었습니다. 2025년에 싱글 패스 안료 프린터를 도입한 업체에 따르면, 온디맨드 인쇄 모델로 전환한 후 재고 평가 손실이 두 자릿수 감소했다고 보고되었습니다. 또한, 판매 거점과 가까운 곳에서 원단을 인쇄함으로써 물류 비용 절감 효과도 높아지고 있으며, 이는 향후 도입될 유럽의 추적성 규정에도 부합하는 요인이 되고 있습니다.

섬유 산업에서 아날로그 인쇄에서 디지털 인쇄로의 전환

디지털화의 확산은 생산량이 1,000미터 미만으로 떨어지면 가속화됩니다. 이는 로터리 스크린 인쇄와의 경제적 손익분기점입니다. Epson의 SureColor F10070H와 같은 플랫폼은 인라인 전처리 및 고정 기능을 통합하여 여러 습식 공정을 단일 건식 공정으로 통합합니다. 폴리에스터 소재 스포츠웨어의 보급이 가장 빠르게 진행된 이유는 승화형 인쇄를 통해 인쇄 후 세탁 공정이 필요 없어졌기 때문이지만, 인라인 경화 기술을 통해 동등한 내광성을 확보하게 되면서 면이나 비스코스 소재도 빠르게 그 뒤를 따라잡고 있습니다. 이러한 추세에 따라 2025년 중국에서 원단에 직접 잉크젯 인쇄 시스템의 판매 대수가 처음으로 로터리 스크린 인쇄를 넘어섰습니다.

산업용 규모의 기계에 필요한 막대한 초기 투자 비용

50만 달러에서 200만 달러 가격대의 싱글패스 프린터는 많은 중소기업에게는 감당하기 어려운 가격대입니다. 리스를 이용할 수 있는 경우에도, 필요한 신용 보증이 도입의 불균형을 초래하여 남미와 아프리카에서는 여전히 로터리 스크린에 의존하고 있습니다. 2025년에는 ‘Equipment-as-a-Service(EaaS)’ 모델이 보급되기 시작했지만, 투자 회수를 위해서는 여전히 연간 50만 제곱미터 이상의 생산량이 필요하며, 이 기준에 도달할 수 있는 신흥 시장의 가공업체는 거의 없습니다.

부문별 분석

디지털 잉크젯 솔루션은 2025년 매출의 62.51%를 차지하며, 이 부문은 텍스타일 프린터 시장의 성장을 이끄는 주요 동력이 되었습니다. 2026년부터 2031년에 걸쳐, 싱글 패스 기기가 아날로그 기기와 동등한 속도를 구현하면서도 무제한의 패턴 유연성을 제공함에 따라, 이 부문은 연평균 성장률(CAGR) 3.45%를 나타낼 것으로 전망됩니다. 현재 텍스타일 프린터 시장에서는 순수한 기계적 특성보다 소프트웨어 중심의 가동 시간이 더욱 중요시되면서, 공급업체들은 예측 유지보수 분석과 하드웨어 리스를 결합하는 추세입니다.

스크린 인쇄는 로터리 유닛의 속도가 100m/분을 초과하기 때문에 대량 생산되는 범용 제품 분야에서는 여전히 주류를 이루고 있지만, 브랜드들이 현지 생산이나 소량 주문을 요구할 때마다 그 중요성은 줄어들고 있습니다. 잉크젯 드롭으로는 구현할 수 없는 질감 효과를 얻기 위해 여전히 평판 스크린이 사용되고 있지만, 다층 디지털 바니시의 발전에 따라 이러한 우위도 점차 줄어들고 있습니다. 스크린 인쇄 스테이션을 베이스에 배치하고 그 뒤에 잉크젯 헤드를 배치하는 하이브리드 플랫폼은 기존 자산을 하룻밤 사이에 폐기하기를 원치 않는 변환업체들 사이에서 시장 점유율을 높이고 있습니다.

연평균 성장률(CAGR) 4.22%로 성장하고 있는 안료 화학 기술 덕분에, 텍스타일 프린터 시장은 물을 대량으로 소비하는 스팀 처리에 의존하지 않고도 세탁 견뢰도 4-5등급을 달성할 수 있게 되었습니다. 이러한 진전은 시장이 유해 화학물질 제로 배출(ZDHC) 기준 및 향후 시행될 EU의 정보 공개 규정을 준수하는 데 필수적입니다. NeoPigment 잉크는 인라인 전처리 모듈과 결합함으로써, 기존에는 반응성 염료로만 달성할 수 있었던 면 소재에서의 인쇄 수율을 실현했습니다. 그 결과, 아시아 각지의 여러 섬유 공장에서 스팀기 폐기를 시작했으며, 이러한 추세는 2025년에 더욱 가속화되었습니다. 이는 지속가능성과 규제 준수에 힘입어 이루어진 생산 관행의 큰 변화를 반영하고 있습니다.

2025년 매출의 41.08%를 차지한 분산형 및 승화형 잉크는 합성섬유와의 친화성과 선명한 발색 덕분에 폴리에스터 스포츠웨어 분야에서 여전히 주류를 이루고 있습니다. 그러나 각 브랜드가 폴리에스터 단독 사용에 대한 의존도를 줄이기 위해 여러 가지 혼방 소재를 도입하는 등 원단 선택의 폭을 다양화하고 있어, 이 분야의 성장률은 둔화되고 있습니다. 한편, UV 경화형 잉크 세트는 특히 실외 내구성과 환경적 요인에 대한 내성이 필수적인 용도에서 간판 업계의 주목을 받고 있습니다. 또한, 바이오 바인더는 현재 시장 점유율이 낮은 편이지만, 브랜드들이 지속가능성 목표와 규제 요건에 따라 구매 결정에 생애주기 평가(LCA)를 반영함에 따라 점차 채택이 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년 시장 규모의 39.34%를 차지했으며, 2030년까지 중국의 디지털 보급률이 35%를 넘어설 전망이고, 인도의 인센티브 제도를 통해 설비 투자액의 최대 25%를 환급받을 수 있게 됨에 따라 2031년까지 상당한 성장이 예상됩니다. 수라트와 광둥성의 투자 클러스터가 싱글패스 승화형 염색 라인 도입을 주도하고 있으며, 일본과 한국에서는 소프트웨어 업그레이드가 수요 증가를 뒷받침하고 있습니다. 동남아시아의 수출국, 특히 베트남과 방글라데시는 유럽의 니어쇼어링 추세 속에서 경쟁력을 유지하기 위해 하이브리드 플랫폼을 도입하고 있습니다.

아프리카는 3.91%라는 지역 내 가장 높은 성장률을 기록하고 있으며, 그 원동력은 WTO 면화 이니셔티브입니다. 이 이니셔티브는 에티오피아, 이집트, 모로코, 케냐에 통합형 섬유 단지를 개발하는 데 50억 달러를 투자하고 있습니다. 에티오피아에서는 하와사 산업단지 내의 한 공장이, 공급망 내 추적성을 요구하는 유럽 소매업체들 수요 증가에 대응하기 위해 2025년에 안료 잉크젯 생산 라인을 도입했습니다. 한편, 모로코는 스페인 및 프랑스와 지리적으로 인접한 이점을 살려, 해당 시장에 72시간 이내에 인쇄 원단을 납품할 수 있는 체제를 구축함으로써, 이 지역 내 주요 공급업체로서의 입지를 공고히 하고 있습니다.

북미와 유럽의 성장률은 각각 2.8%와 2.9%로 완만하지만, 여전히 기술의 인큐베이터로서의 역할을 수행하고 있습니다. AI를 활용한 색상 조합 및 디지털 제품 패스포트가 이러한 성숙 시장에서 디지털화를 가속화하고 있습니다. 남미와 중동은 수입 관세와 기술 지원 부족으로 인해 뒤처지고 있지만, 아랍에미리트(UAE)에서는 고급 호텔 리모델링 시 내부 지속가능성 방침을 충족하기 위해 물을 사용하지 않는 안료 잉크젯 라인이 지정되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the textile printers market size was valued at USD 1.11 billion in 2025 and was estimated to grow from USD 1.14 billion in 2026 to reach USD 1.34 billion by 2031, at a CAGR of 3.13% during the forecast period (2026-2031).

This report is Segmented by Printing Technology (Digital Inkjet Printing, Screen Printing, and More), Ink Type (Reactive Dye Inks, Acid Dye Inks, Pigment Inks, Disperse and Sublimation Inks, and More), Application (Garments and Apparel, Home Textiles, Signage and Display Graphics, More), Fabric (Cotton, Polyester, Silk, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Textile Printers Market Trends and Insights

Growing Demand for Fast Fashion and Customized Apparel

Weekly micro-drops now replace seasonal collections, pushing converters toward low-minimum orders that analog screens cannot satisfy. Digital devices eliminate screen engraving and allow pattern changes in minutes, enabling European brands to nearshore production for rapid replenishment. Operators that adopted single-pass pigment printers in 2025 reported double-digit reductions in inventory write-offs after shifting to print-on-demand models. Logistics savings also mount as fabric is printed closer to the point of sale, a factor that aligns with upcoming Europe traceability mandates.

Shift From Analog to Digital Printing in Textiles

Digital penetration is accelerating once job lengths fall below 1 000 meters, the economic break-even against rotary screens. Platforms such as the Epson SureColor F10070H integrate inline pretreatment and fixation, combining multiple wet processes into a single dry pass. Polyester sportswear has moved fastest because dye sublimation avoids post-print washing, but cotton and viscose are catching up now that inline curing achieves comparable fastness. These dynamics explain why direct-to-fabric inkjet systems outsold rotary screens for the first time in China during 2025.

High Initial Capital Investment for Industrial-Scale Machines

Single-pass printers priced between USD 500 000 and USD 2 million are out of reach for many small and medium enterprises. Even where leasing is available, required credit guarantees keep adoption uneven, prolonging reliance on rotary screens in South America and Africa. Equipment-as-a-service models gained traction in 2025, yet payback still depends on volumes above 500 000 m2 per year, a threshold few emerging-market converters can reach.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in High-Speed Inkjet Heads and Sublimation Inks

- Expanding E-Commerce and Web-to-Print Platforms

- Volatility in Textile Ink Raw Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital inkjet solutions accounted for 62.51% of 2025 revenue, making the segment a key driver of the textile printers market's growth. Between 2026 and 2031, the segment is projected to grow at a 3.45% CAGR, as single-pass machines match analog speed while offering unlimited pattern flexibility. The textile printers market now rewards software-driven uptime more than purely mechanical attributes, prompting suppliers to couple predictive-maintenance analytics with hardware leases.

Screen printing still dominates high-volume commodity runs because rotary units exceed 100 m min-1, but their relevance erodes each time brands push for localized production or smaller order lots. Flatbed screens persist for textured effects unattainable with inkjet drops, though even this moat is narrowing as multi-layer digital varnish evolves. Hybrid platforms that hold a base screen station followed by inkjet heads are gaining share among converters unwilling to scrap legacy assets overnight.

Pigment chemistries, expanding at a 4.22% CAGR, are enabling the textile printers market to achieve grade 4-5 wash-fastness without relying on water-intensive steaming processes. This advancement is crucial to helping the market comply with Zero Discharge of Hazardous Chemicals (ZDHC) limits and with upcoming EU disclosure regulations. NeoPigment inks, combined with inline pretreatment modules, have now achieved cotton yields previously achieved only with reactive dyes. As a result, several textile mills across Asia have begun decommissioning their steamers, a trend that gained momentum in 2025, reflecting a significant shift in production practices driven by sustainability and regulatory compliance.

Disperse and sublimation inks, which accounted for 41.08% of 2025 revenue, continue to dominate the polyester sportswear segment due to their compatibility with synthetic fabrics and vibrant color output. However, the growth rate in this segment is slowing as brands diversify their fabric choices to include multiple blends, reducing dependency on polyester alone. Meanwhile, UV-curable ink sets are gaining traction in the signage industry, particularly in applications where outdoor durability and resistance to environmental factors are critical. Additionally, bio-based binders, though currently a small share of the market, are gradually gaining adoption as brands incorporate life-cycle assessments into their purchasing decisions, aligning with sustainability goals and regulatory requirements.

Geography Analysis

Asia-Pacific accounted for 39.34% of the 2025 value and is projected to grow significantly through 2031, as China's digital penetration surpasses 35% by 2030 and India's incentive scheme refunds up to 25% of capital outlays. Investment clusters in Surat and Guangdong lead installations of single-pass dye-sublimation lines, with software upgrades driving incremental demand in Japan and South Korea. Southeast Asian exporters, notably Vietnam and Bangladesh, are installing hybrid platforms to remain competitive amid near-shoring in Europe.

Africa is experiencing the fastest regional growth, at 3.91%, driven by the WTO Cotton Initiative, which is channeling USD 5 billion into the development of integrated textile parks in Ethiopia, Egypt, Morocco, and Kenya. In Ethiopia, mills within the Hawassa Industrial Park installed pigment-inkjet corridors in 2025 to meet the growing demand of European retailers for traceability in their supply chains. Meanwhile, Morocco is capitalizing on its geographical proximity to Spain and France, enabling it to deliver printed fabric to these markets within 72 hours, thereby strengthening its position as a key supplier in the region.

North America and Europe expand more slowly, at 2.8% and 2.9% respectively, yet remain technology incubators. AI-based color-matching and digital product passports accelerate digital retrofits in these mature markets. South America and the Middle East lag due to import tariffs and limited technical support, although premium hospitality refurbishments in the United Arab Emirates now specify waterless pigment lines to meet internal sustainability charters.

- Seiko Epson Corporation

- Kornit Digital Ltd.

- Electronics For Imaging (EFI Reggiani)

- HP Inc.

- Mimaki Engineering Co., Ltd.

- Brother Industries, Ltd.

- Roland DG Corporation

- Durst Group AG

- Ricoh Company, Ltd.

- Mutoh Holdings Co., Ltd.

- MS Printing Solutions S.r.l.

- Aeoon Technologies GmbH

- ColorJet India Ltd.

- SPGPrints B.V.

- DGI Co., Ltd.

- Sawgrass Technologies, Inc.

- JHF Technology Group Co., Ltd.

- Shenzhen Homer Textile Digital Printing Co., Ltd.

- Fujifilm Holdings Corporation

- Zhejiang Atexco Digital Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Fast Fashion and Customized Apparel

- 4.2.2 Shift From Analog to Digital Printing in Textiles

- 4.2.3 Advancements in High-Speed Inkjet Heads and Sublimation Inks

- 4.2.4 Expanding E-Commerce and Web-to-Print Platforms

- 4.2.5 Adoption of Waterless Pigment Ink Printers to Meet ZDHC Guidelines

- 4.2.6 Integration of AI-Based Print Workflow Automation in Textile Mills

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investment for Industrial-Scale Machines

- 4.3.2 Volatility in Textile Ink Raw Material Prices

- 4.3.3 Limited Color Gamut and Fastness for Certain Digital Inks

- 4.3.4 Regulatory Scrutiny on Wastewater Nanoparticles From Polyester Sublimation

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Technology

- 5.1.1 Digital Inkjet Printing

- 5.1.1.1 Direct-to-Fabric (DTF)

- 5.1.1.2 Direct-to-Garment (DTG)

- 5.1.1.3 Dye-Sublimation

- 5.1.1.4 Single-Pass and Others

- 5.1.2 Screen Printing

- 5.1.2.1 Rotary Screen

- 5.1.2.2 Flatbed Screen

- 5.1.3 Other Printing Technologies

- 5.1.1 Digital Inkjet Printing

- 5.2 By Ink Type

- 5.2.1 Reactive Dye Inks

- 5.2.2 Acid Dye Inks

- 5.2.3 Pigment Inks

- 5.2.4 Disperse and Sublimation Inks

- 5.2.5 UV-Curable and Hybrid Inks

- 5.2.6 Other Ink Types

- 5.3 By Application

- 5.3.1 Garments and Apparel

- 5.3.2 Home Textiles

- 5.3.3 Signage and Display Graphics

- 5.3.4 Technical Textiles

- 5.3.5 Other Applications

- 5.4 By Fabric

- 5.4.1 Cotton

- 5.4.2 Polyester

- 5.4.3 Silk

- 5.4.4 Blends

- 5.4.5 Other Fabrics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Seiko Epson Corporation

- 6.4.2 Kornit Digital Ltd.

- 6.4.3 Electronics For Imaging (EFI Reggiani)

- 6.4.4 HP Inc.

- 6.4.5 Mimaki Engineering Co., Ltd.

- 6.4.6 Brother Industries, Ltd.

- 6.4.7 Roland DG Corporation

- 6.4.8 Durst Group AG

- 6.4.9 Ricoh Company, Ltd.

- 6.4.10 Mutoh Holdings Co., Ltd.

- 6.4.11 MS Printing Solutions S.r.l.

- 6.4.12 Aeoon Technologies GmbH

- 6.4.13 ColorJet India Ltd.

- 6.4.14 SPGPrints B.V.

- 6.4.15 DGI Co., Ltd.

- 6.4.16 Sawgrass Technologies, Inc.

- 6.4.17 JHF Technology Group Co., Ltd.

- 6.4.18 Shenzhen Homer Textile Digital Printing Co., Ltd.

- 6.4.19 Fujifilm Holdings Corporation

- 6.4.20 Zhejiang Atexco Digital Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment