|

시장보고서

상품코드

2061904

제본기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Binding Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

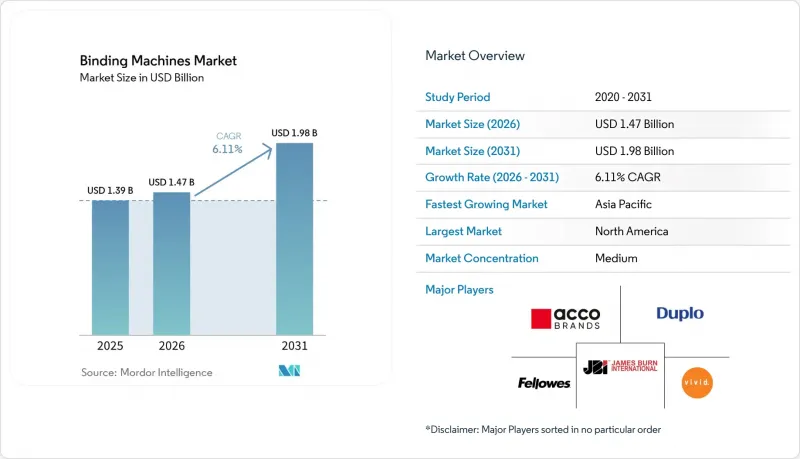

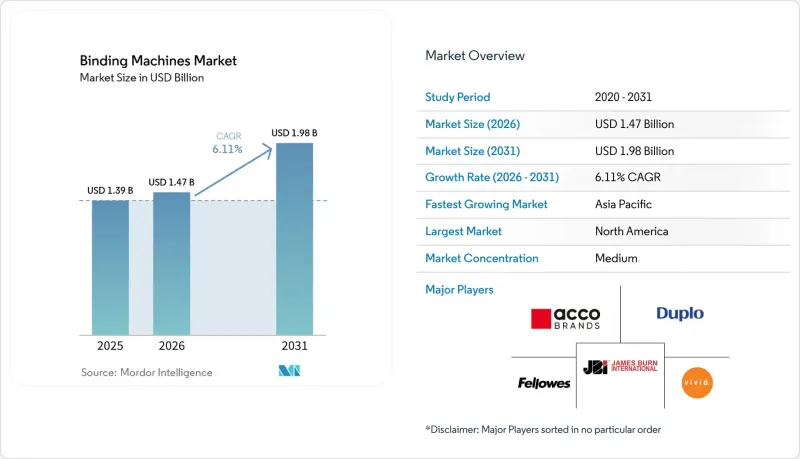

Mordor Intelligence에 의하면, 제본기 시장 규모는 2025년 13억 9,000만 달러로 평가되었습니다. 2026년 14억 7,000만 달러로 확대되어 2031년까지 19억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 6.11%를 나타낼 전망입니다.

본 보고서는 제본 방식(콤 제본, 와이어 제본 등), 작동 모드(수동, 반자동 등), 최종 사용자 산업(기업 사무실·정부 기관, 상업 인쇄·출판사 등), 유통 채널(직접 판매·OEM, 전문 판매점·재판매업자 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 제본기 시장 동향과 인사이트

자동화 및 전동 제본 솔루션으로의 전환

상업 인쇄 회사나 퀵 복사 센터에서는 인건비 절감과 납기 단축을 목적으로 마감 공정의 자동화가 진행되고 있습니다. 디지털 인쇄기와 직접 연결되는 전자동 PUR 제본기는 현재 시간당 500사이클 이상을 처리하며, 책 한 권당 인건비를 최대 3분의 1까지 절감하고 있습니다. Fastbind의 2025 ONE 시리즈는 터치스크린 조작과 자동 두께 감지 기능을 도입하여, 중규모 사용자가 수동식 열제본기에서 전환할 수 있도록 지원하고 있습니다. 또한, 자동화는 작업장의 안전 측면에서도 기여하고 있습니다. 전동 펀칭을 사용하면 반복성 스트레스 장애의 발생이 줄어들기 때문입니다. 이는 유럽과 북미 전역에서 중요하게 여겨지는 산업위생상의 과제입니다. 시급이 20달러를 넘는 시장에서는 주당 처리량이 500권을 넘으면 2년 이내에 투자 비용을 회수할 수 있습니다. 임금 상승으로 인해 기존에 인건비 경쟁력이 높았던 중국과 인도에서도 이러한 추세는 더욱 가속화되고 있습니다.

주문형 및 자비 출판 서비스의 성장

자비 출판사나 디지털 스토어프론트에서는 내구성을 해치지 않으면서 1부부터 소량 생산이나 페이지 수 변동에 대응할 수 있는 매우 유연한 제본 방식이 요구되고 있습니다. Kindle Direct Publishing(KDP) 및 기타 플랫폼에서는 하루에 수천 건의 소량 주문이 자동 퍼펙트 바인더로 전송되며, 24시간 이내에 발송되어야 합니다. 포토북 키오스크에서는 광택지에 균열이 잘 생기지 않기 때문에 PUR 제본이 선호됩니다. 이는 결혼식 앨범이나 여행기에서 소비자가 기대하는 품질입니다. 퀵 프린트 샵은 맞춤형 표지나 특수 라미네이팅 가공을 패키지로 묶어 수익을 늘리고, 몇 분 만에 콤 제본, 와이어 제본, 열 제본 설정을 전환할 수 있는 멀티 모드 장비에 대한 투자를 촉진하고 있습니다. 아시아태평양에서는 가처분 소득이 증가하고 선물용 인쇄 제품의 인기가 높아짐에 따라 이러한 추세가 급속히 확산되고 있습니다.

디지털 문서화와 전자 서명의 보급 가속화

북미에서는 기업 계약 워크플로우의 95%가 이미 전자 서명을 통해 처리되고 있어, 물리적 문서를 인쇄, 정리, 제본할 필요가 줄어들고 있습니다. 미국의 ESIGN이나 유럽의 eIDAS와 같은 규제 체계에서는 디지털 기록이 종이 사본과 법적으로 동등한 것으로 인정되고 있어, 과거 사무실에서 제본된 원본을 보관하던 주된 이유가 사라졌습니다. 협업용 클라우드 플랫폼은 검색 가능한 PDF와 공유 디지털 작업 공간을 통해 종이 매뉴얼을 더욱 대체하고 있습니다. 정부 기관이나 대학에서는 여전히 물리적 아카이브에 의존하는 경우도 있지만, 전환 속도는 가속화되고 있으며, 이러한 제약 요인은 예측 기간의 전반부에 집중적으로 나타날 것으로 보입니다.

부문별 분석

EVA 및 PUR 접착제를 활용한 열제본 기술은 2026년부터 2031년까지 6.58%라는 가장 높은 성장률을 보일 것으로 예측됩니다. 이는 포토북 키오스크, 주문형 출판사, 그리고 책등이 평평하게 펼쳐지고 강력한 접착력이 필요한 기업 프레젠테이션에 의해 주도되고 있습니다. PUR 배합은 냉각이 아닌 습기에 의해 경화되기 때문에 EVA에 비해 최대 60% 더 높은 인장 강도를 발휘하여 고광택 인화지의 내구성을 보장합니다. Duplo DPB-500과 같은 기계는 짧은 납기 워크플로우에 대응하기 위해 시간당 500권 이상을 처리하는 반면, 약 4,500유로(5,040달러)의 데스크톱 모델은 소규모 스튜디오를 대상으로 제공되고 있습니다. 2025년에도 콤 제본은 28.28%의 시장 점유율을 유지했습니다. 이는 플라스틱 빗을 개당 불과 0.10달러에 구입할 수 있고, 페이지를 쉽게 교체할 수 있기 때문입니다. 이러한 장점은 교육 매뉴얼이나 사내 보고서에서 높이 평가받고 있습니다.

디지털 인쇄기로의 전환이 진행되는 가운데, HP Indigo 및 Xerox iGen 장비에서 생산되는 코팅지에 적용 가능한 PUR에 대한 관심이 높아지고 있습니다. PUR의 소모품 비용은 EVA의 약 3배이지만, 책 한 권당 접착제 사용량을 3분의 1로 줄일 수 있기 때문에 비용 차이는 줄어들고 있습니다. 와이어 제본은 위변조 방지 기능이 필요한 법적 제출 서류나 규제 당국에 대한 신고 시 여전히 필수적이지만, 스파이럴 제본이나 코일 제본은 360도 회전이 가능하기 때문에 달력이나 노트 시장에서 주류를 이루고 있습니다. 상업 인쇄에서는 무선 제본이나 중철 제본이 소프트커버 책이나 카탈로그에 주로 사용되며, 고급 하드커버 제작에는 여전히 실제본이 주류를 이루고 있습니다.

2025년에는 500달러 미만의 가격과 간편한 조작 방식 덕분에 수동식 기계가 시장의 45.51%를 차지했으나, 그 처리 능력은 시간당 약 20권으로 제한되어 있습니다. 18만 루피에서 35만 루피(2,160-4,200 달러) 범위의 반자동 기계는 대학 인쇄실 등 중규모 사용자를 대상으로 펀칭 및 클리핑 작업 속도를 높여줍니다. 퀵 프린트 샵과 상업 인쇄 업체들이 인건비 절감과 안정적인 품질을 중시하고 있기 때문에 완전 자동화 시스템 시장은 2031년까지 연평균 7.05%의 성장률을 보일 것으로 전망됩니다.

디지털 인쇄기와 인라인으로 연결된 C.P. Bourg BB3202 PUR 제본기는 무인 운전이 가능하여, 대당 인건비를 최대 35% 절감할 수 있습니다. 인건비 계산이 자동화 확대를 촉진하고 있으며, 시급이 20달러인 경우 주간 처리량이 500부를 넘으면 5만 달러짜리 시스템은 18개월 이내에 투자 비용을 회수할 수 있습니다. 반면, 사용 빈도가 낮은 교육 기관에서는 여전히 저렴한 수동식 기계에 의존하고 있습니다. 중국과 인도에서는 임금 상승으로 인해 투자 회수 기간이 단축됨에 따라 자동화 도입이 가속화될 전망입니다.

지역별 분석

2025년, 북미는 제본기 시장의 33.13%를 차지했습니다. 이는 성숙한 기업 부문과 퀵 프린트 센터의 촘촘한 네트워크에 힘입은 결과입니다. 1990년대에 도입된 많은 구형 수동 기계들은 현재 점차 노후화되고 있어, 꾸준한 교체 수요를 창출하고 있습니다. 전자 서명의 보급률이 95%에 달하면서 사무실에서의 제본량은 감소했으나, 포토북 제작 업체와 자비 출판자들 수요가 그 감소분을 부분적으로 상쇄하고 있습니다. 미국은 대규모 상업 인쇄 산업과 다각적인 기업 지출에 힘입어, 계속해서 이 지역의 핵심 시장으로서의 위상을 유지하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 7.12%로 확대될 것으로 예상되며, 이는 모든 지역 중 가장 높은 성장률입니다. 인도에서는 국가 교육 정책에 따른 교육 인프라 구축의 일환으로, 100만 개 이상의 학교에 있는 도서관 및 관리 거점을 위한 시설 자금이 확보되어 있습니다. 중국의 인쇄업체들은 코팅지용 PUR 제본이 요구되는 수출 사업을 수주하기 위해 수동식 기계에서 자동식 기계로의 전환을 추진하고 있습니다. 일본과 한국은 꾸준한 재구매 수요를 창출하고 있는 반면, 인도네시아, 베트남, 태국에서는 신흥 중산층의 맞춤형 인쇄물 소비에 발맞추어 신규 시장이 급속히 확대되고 있습니다.

유럽은 독일, 프랑스, 영국의 상업 인쇄 거점들에 힘입어 안정적인 시장 점유율을 유지하고 있습니다. 유럽연합(EU)의 순환 경제 의제는 바이오 접착제에 대한 수요를 촉진하고 있으며, 공급업체들이 재활용 가능한 소모품을 개발하도록 장려하고 있습니다. 2025년 6월 Plockmatic Group이 Renz를 인수함에 따라 업계 재편이 진행되고 있으며, 와이어 제본 제품을 위한 더욱 견고한 플랫폼이 구축되고 있습니다. 중동 및 아프리카에서는 걸프협력회의(GCC) 회원국과 사하라 이남 아프리카 일부 지역의 학교 건설을 주도하는 역할을 통해 성장의 조짐이 보이고 있습니다. 남미에서는 거시경제의 변동에도 불구하고 브라질과 아르헨티나에서 기초 수요가 유지되고 있으며, 지출은 교육 및 정부 부문에 집중되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the binding machines market size is expected to increase from USD 1.39 billion in 2025 to USD 1.47 billion in 2026 and reach USD 1.98 billion by 2031, growing at a CAGR of 6.11% over 2026-2031.

This report is Segmented by Binding Method (Comb Binding, Wire Binding, and More), Operation Mode (Manual, Semi-Automatic, and More), End-User Industry (Corporate Offices and Government, Commercial Print and Publishing Houses, and More), Distribution Channel (Direct Sales and OEM, Specialty Dealers and Resellers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Binding Machines Market Trends and Insights

Shift Toward Automated and Electric Binding Solutions

Commercial print shops and quick-copy centers are automating finishing lines to shrink labor costs and cut turnaround times. Fully automatic PUR binders that connect directly to digital presses now process more than 500 cycles each hour, driving per-book labor down by up to one-third. Fastbind's 2025 ONE Series introduced touchscreen controls and automatic thickness sensing, helping mid-volume users move away from manual thermal units. Automation also supports workplace safety because electric punching lowers repetitive-strain incidents, an occupational-health focus across Europe and North America. In markets where hourly wages surpass USD 20, the investment pays back in less than two years when weekly volumes exceed 500 books. The trend is gaining traction in China and India as rising wages narrow the historical labor-cost advantage.

Growth of On-Demand and Self-Publishing Services

Self-publishers and digital storefronts require highly flexible binding that handles single-copy runs and variable page counts without sacrificing durability. Kindle Direct Publishing and other platforms route thousands of micro-orders a day to automated perfect binders that must ship within 24 hours. Photobook kiosks prefer PUR because it resists cracking on glossy paper, a quality consumers expect for wedding albums and travel books. Quick-print shops increase revenue by bundling personalized covers and specialty laminates, and by encouraging investment in multi-mode machines that switch between comb, wire, and thermal setups in minutes. Asia-Pacific is witnessing strong uptake as disposable incomes rise and gift-oriented print products gain popularity.

Accelerating Digital Documentation and E-Signature Uptake

Electronic signatures already cover 95% of corporate contract workflows in North America, eroding the need to print, collate, and bind physical documents. Regulatory frameworks such as ESIGN in the United States and eIDAS in Europe accept digital records as legally equivalent to paper copies, removing a key reason offices once retained bound originals. Collaborative cloud platforms further replace paper manuals with searchable PDFs and shared digital workspaces. Government bodies and universities still rely on physical archiving in some cases, but their migration pace is accelerating, keeping this restraint front-loaded in the forecast horizon.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Educational Infrastructure Worldwide

- Rising Adoption of Office Automation Hardware

- High Capital Cost of Fully Automatic Systems for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal binding techniques using EVA and PUR adhesives are projected to post the fastest growth at 6.58% from 2026-2031, fueled by photobook kiosks, on-demand publishers, and corporate presentations that require lay-flat spines and strong adhesion. PUR formulas cure through moisture rather than cooling, delivering up to 60% higher pull strength than EVA, which guarantees longevity for high-gloss photo papers. Machines such as the Duplo DPB-500 process more than 500 books an hour to meet quick-turn workflows, while desktop models priced around EUR 4,500 (USD 5,040) serve small studios. Comb binding retained a 28.28% share in 2025 because plastic combs cost as little as USD 0.10 each and allow easy page replacement, an advantage valued in training manuals and internal reports.

The ongoing shift toward digital presses has heightened interest in PUR, as it handles coated stocks produced by HP Indigo or Xerox iGen devices. Although PUR consumables cost about three times as much as EVA, operators use one-third as much adhesive per book, narrowing the cost gap. Wire binding remains essential for legal submissions and regulatory filings that require tamper-evident security, while spiral and coil binding dominate calendars and notebooks thanks to 360-degree rotation. Perfect binding and saddle-stitch cover softcover books and catalogs in commercial runs, and book-sewing persists in high-end hardcover production.

Manual machines accounted for 45.51% of the market in 2025, driven by sub-USD 500 pricing and simplicity, but their throughput is limited to roughly 20 books per hour. Semi-automatic units ranging from INR 180,000 to INR 350,000 (USD 2,160-4,200) speed punching or crimping for mid-volume users such as university print rooms. Fully automatic systems are forecast to grow at 7.05% through 2031 because quick-print shops and commercial printers value labor savings and consistent quality.

A C.P. Bourg BB3202 PUR binder linked inline to a digital press can run lights-out shifts, trimming per-unit labor by up to 35%. Labor-cost math drives the automation uptick, at an hourly wage of USD 20, a USD 50,000 system pays for itself within 18 months when weekly volumes exceed 500 units. Meanwhile, educational institutions with intermittent usage continue to rely on affordable manual machines. Automation adoption in China and India is poised to accelerate as wage inflation shortens payback periods.

Geography Analysis

North America accounted for 33.13% of the binding machines market in 2025, driven by its mature corporate sector and a dense network of quick-print centers. Many legacy manual units installed in the 1990s are now approaching obsolescence, creating a steady replacement pipeline. Electronic signature penetration at 95% has trimmed office binding volumes, yet demand from photobook producers and self-publishers partially offsets the decline. The United States remains the region's anchor market, supported by a large commercial-print industry and diversified corporate spending.

Asia-Pacific is forecast to expand at a 7.12% CAGR through 2031, the fastest among all regions. India's education infrastructure drive under the National Education Policy finances equipment for libraries and administrative hubs in more than one million schools. Chinese printers are migrating from manual to automated machines to win export business that requires PUR binding for coated paper. Japan and South Korea contribute steady replacement volumes, while Indonesia, Vietnam, and Thailand show rapid greenfield growth tied to emerging middle-class consumption of personalized print goods.

Europe maintains a stable share propelled by commercial-print hubs in Germany, France, and the United Kingdom. The European Union's circular-economy agenda boosts demand for bio-based adhesives, encouraging vendors to develop recyclable consumables. Consolidation is reshaping the regional landscape following Plockmatic Group's June 2025 acquisition of Renz, creating a stronger platform for wire-binding products. The Middle East and Africa show nascent growth led by school construction in Gulf Cooperation Council states and parts of sub-Saharan Africa. In South America, Brazil and Argentina sustain baseline demand despite macro-economic volatility, with spending concentrated in education and government segments.

- ACCO Brands (GBC)

- Duplo Corporation

- Fellowes Brands

- James Burn International (JBI)

- Vivid Laminating Technologies Ltd.

- General Binding Corporation

- Akiles Products Inc.

- Bindomatic AB

- Plastikoil of Pennsylvania Inc.

- Tamerica Products Inc.

- MBM Corporation

- Graphic Whizard Inc.

- Challenge Machinery Company

- Intimus International Group GmbH

- Morgana Systems Ltd.

- Standard Finishing Systems

- Plockmatic International AB

- Powis Parker Inc.

- IML Machinery Inc.

- Zhejiang Yunguang Machinery Co. Ltd.

- Shanghai Loretta Machinery Manufacture Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Office Automation Hardware

- 4.2.2 Expansion of Educational Infrastructure Worldwide

- 4.2.3 Growth of On-Demand and Self-Publishing Services

- 4.2.4 Shift Toward Automated and Electric Binding Solutions

- 4.2.5 Niche Demand for Tamper-Evident Binding in Legal Sector

- 4.2.6 Adoption of Sustainable and Recyclable Binding Consumables

- 4.3 Market Restraints

- 4.3.1 Accelerating Digital Documentation and E-Signature Uptake

- 4.3.2 High Capital Cost of Fully Automatic Systems for SMEs

- 4.3.3 Supply-Chain Volatility for Steel and Plastic Components

- 4.3.4 Growing Refurbished Equipment Market Depressing New Sales

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Binding Method

- 5.1.1 Comb Binding

- 5.1.2 Wire Binding

- 5.1.3 Spiral/Coil Binding

- 5.1.4 Thermal Binding

- 5.1.5 Perfect Binding

- 5.1.6 Saddle Stitch and Book Sewing

- 5.1.7 Tape and Velo Binding

- 5.2 By Operation Mode

- 5.2.1 Manual

- 5.2.2 Semi-Automatic

- 5.2.3 Fully Automatic

- 5.3 By End-User Industry

- 5.3.1 Corporate Offices and Government

- 5.3.2 Commercial Print and Publishing Houses

- 5.3.3 Quick Print and Copy Shops

- 5.3.4 Educational Institutions

- 5.3.5 Other End-user Industries

- 5.4 By Distribution Channel

- 5.4.1 Direct Sales and OEM

- 5.4.2 Specialty Dealers and Resellers

- 5.4.3 Office Supply Superstores

- 5.4.4 Online Retail/E-commerce

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ACCO Brands (GBC)

- 6.4.2 Duplo Corporation

- 6.4.3 Fellowes Brands

- 6.4.4 James Burn International (JBI)

- 6.4.5 Vivid Laminating Technologies Ltd.

- 6.4.6 General Binding Corporation

- 6.4.7 Akiles Products Inc.

- 6.4.8 Bindomatic AB

- 6.4.9 Plastikoil of Pennsylvania Inc.

- 6.4.10 Tamerica Products Inc.

- 6.4.11 MBM Corporation

- 6.4.12 Graphic Whizard Inc.

- 6.4.13 Challenge Machinery Company

- 6.4.14 Intimus International Group GmbH

- 6.4.15 Morgana Systems Ltd.

- 6.4.16 Standard Finishing Systems

- 6.4.17 Plockmatic International AB

- 6.4.18 Powis Parker Inc.

- 6.4.19 IML Machinery Inc.

- 6.4.20 Zhejiang Yunguang Machinery Co. Ltd.

- 6.4.21 Shanghai Loretta Machinery Manufacture Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment