|

시장보고서

상품코드

2061905

인쇄 필름 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Printed Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

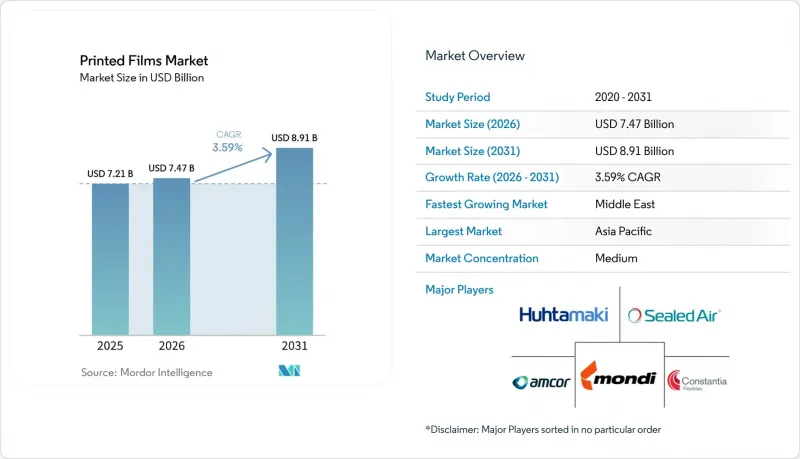

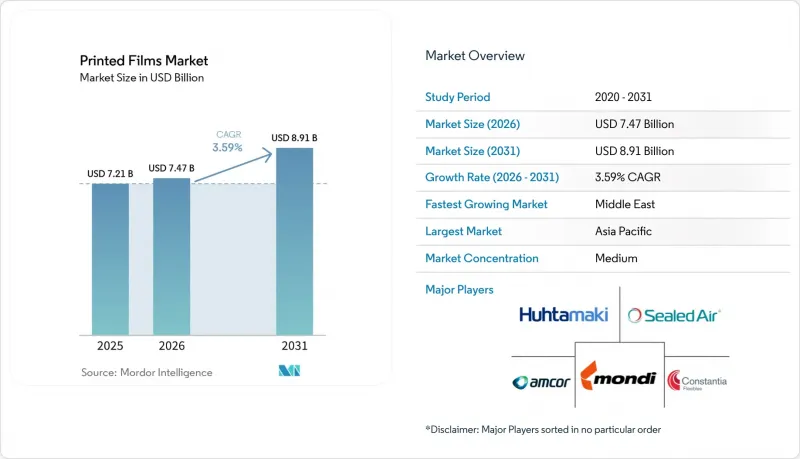

Mordor Intelligence에 의하면, 인쇄 필름 시장 규모는 2025년 72억 1,000만 달러로 평가되었습니다. 2026년 74억 7,000만 달러에서 2031년까지 89억 1,000만 달러로 확대되어 예측 기간(2026-2031년) CAGR 3.59%를 나타낼 전망입니다.

본 보고서는 필름 소재(폴리에틸렌 필름, 폴리프로필렌 필름 등), 인쇄 기술(플렉소 인쇄 등), 인쇄 잉크의 유형(용제형 잉크, 수성 잉크 등), 최종 사용자 산업(식품 및 음료, 퍼스널케어 및 화장품 등), 필름 두께(25mm 이하 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인쇄 필름 시장 동향과 인사이트

지속 가능한 포장 솔루션에 대한 수요 증가

현재 브랜드의 조달 계약에는 순환 경제와 관련된 조항이 포함되어 있으며, 컨버터는 바이오 원료의 함유율과 재활용 가능성을 입증할 의무가 있습니다. CARBIOS사는 2025년, 효소 분해를 통해 재활용된 폴리젖산 필름에 대해 미국에서 식품 접촉 적합 인증을 획득함으로써, 다운사이클링을 수반하지 않는 폐쇄형 회수 체계를 실현했습니다. Metalvuoto사의 PLA 기판용 바이오 배리어 코팅은 산소 투과율을 5 cc/m²/일 미만으로 억제하여 농산물의 저장 기간을 40% 연장합니다. 2026년에 시행될 EU의 포장 및 포장 폐기물 규정에 따라, 규정을 준수하지 않는 연포장에 대해 금전적 제재가 도입됨에 따라, 기재의 재조성이 급속히 진행되고 있으며, 지속 가능한 인쇄 필름의 채택이 촉진되고 있습니다.

전자상거래의 성장이 보호용 인쇄 필름 수요를 끌어올리고 있습니다.

2025년 전 세계 소포 처리량은 1,500억 개에 달했으며, 일반적으로 각 소포는 1.8겹의 필름으로 포장되어 있습니다. 각 변환기 제조업체들은 400 gf를 초과하는 내천자 시험을 견디면서도 수성 플렉소 잉크에도 대응할 수 있는 고충격성 폴리에틸렌 재질의 메일러를 통해 이에 대응했습니다. 자동 주문 처리 센터에서는 마찰 계수 0.18의 공압출 슬립층이 선호됩니다. 이를 통해 분류 벨트 위에서 시간당 8,000개의 소포를 처리할 수 있게 됩니다. 10분 이내에 그래픽을 교체할 수 있는 디지털 인쇄기는 소량 판촉용 물량에 대응하고, 당일 배송 수요를 충족시키는 동시에 물류 포장용 인쇄 필름 시장의 확산을 지속시키고 있습니다.

인쇄용 잉크 및 필름 원자재 가격 변동

2025년, 중동공급 중단과 중국의 크래커 가동 중단으로 인해 폴리에틸렌 가격은 톤당 950달러에서 1,320달러로 급등하여, 가공업체의 이익률을 크게 압박했습니다. 2026년 초 이산화티타늄 가격이 전년 대비 18% 상승해 톤당 3,200달러에 달하면서, 화이트 잉크의 원가를 끌어올렸습니다. Uflex와 같이 자체적으로 수지 및 안료 생산 시설을 보유한 컨버터는 200-250 베이시스 포인트의 이익 마진을 누리고 있지만, 많은 독립 기업들은 분기마다 가격을 조정할 수밖에 없어 인쇄 필름 시장에 대한 예측 가능한 투자가 제한되고 있습니다.

부문별 분석

2025년 매출액에서 폴리에틸렌이 차지하는 비중은 37.22%였으나, 산소 투과율이 3cc/m²/일 미만이어야 하는 의약품 및 고차단성 식품 용도 수요에 힘입어 폴리에스터는 연평균 성장률(CAGR) 3.61%를 기록하며 인쇄 필름 시장보다 빠른 속도로 성장할 전망입니다. 도레이의 산화알루미늄 코팅 PET는 12µm에서 0.8 cc/m2/day를 달성하면서도 투명성을 유지하고 있으며, 이는 다층 구조의 복잡성이 수반되지 않는 한 저밀도 폴리에틸렌으로는 달성할 수 없는 사양입니다. 2.5 N/15 mm를 초과하는 열밀봉 강도가 요구되는 경우에는 폴리프로필렌이 여전히 필수적이지만, 프탈산 에스테르류의 사용 금지 조치로 인해 식품 접촉 용도에서 PVC 시장 점유율은 계속해서 감소하고 있습니다. 신흥 바이오폴리머는 현재 그 가치가 한 자릿수 중반 수준에 머물러 있지만, 순환형 경제 시범 사업의 시험대 역할을 수행하며, 지속가능성을 둘러싼 인쇄 필름 시장에서의 논의를 활발하게 유지하고 있습니다.

비용 효율이 뛰어난 박판화 전략이 폴리에스터 채택을 촉진하고 있습니다. Innovia사의 나노 다공성 BOPP는 레이저 천공 처리 없이도 상추나 베리류의 통기성을 확보해 주며, Cosmo First사의 안개 방지 PET는 냉장 파우치를 3주간의 보관 기간 동안에도 투명한 상태로 유지해 줍니다. EU에서는 규제 당국이 총 이온 함량을 10 mg/dm²로 제한하고 있어, 완벽한 추적성을 갖춘 식품용 수지에 대한 수요가 증가하고 있으며, 이에 따라 특수 PET 등급은 인쇄 필름 업계에서 기존의 폴리올레핀에 대항하는 유력한 경쟁자로서의 입지를 다져가고 있습니다.

2025년 매출에서 플렉소 인쇄가 차지하는 비중은 41.82%였으나, 잉크젯 인쇄의 연평균 성장률(CAGR) 3.75%는 전환점을 시사하고 있습니다. 디지털 인쇄기는 판 설치로 인한 가동 중단 시간을 없애고, 500미터 분량의 작업에서도 수익성을 확보할 수 있어 지역 한정 프로모션이나 SKU 증대에 최적입니다. Windmoller & Hersch의 하이브리드 유닛은 정적 브랜딩용 플렉소 스테이션과 일련번호가 부여된 QR 코드용 잉크젯 헤드를 통합하여, 다양한 제품 포트폴리오 전반에 걸쳐 1,000장당 비용을 절감합니다. 그라비아 인쇄는 100만 미터를 넘는 스낵 및 담배용 필름 분야에서 여전히 중요한 역할을 하고 있으며, 실린더 비용이 효율적으로 상각되어야 하고 색차도 ±1ΔE 이내로 유지되어야 합니다.

지속적인 혁신을 통해 플렉소 인쇄의 경쟁력은 유지되고 있습니다. Bobst사의 M6 라인은 플레이트를 자동으로 정렬하여 세팅 시 발생하는 불량률을 40% 줄이고, 디지털 인쇄와의 폐기물 차이를 좁히고 있습니다. 한편, 스크린 인쇄나 패드 인쇄 기술을 활용한 인쇄 필름 시장은 여전히 틈새 시장에 머물러 있으며, 전도성 트랙이나 특수한 위조 방지 씰에 중점을 두고 있습니다. 모든 인쇄 플랫폼에서 각 변환 업체들은 설비 투자액과 생산 로트 수의 유연성을 저울질하고 있으며, 이러한 상충 관계가 인쇄 필름 업계 전체의 향후 설비 구매를 좌우하게 될 것입니다.

지역별 분석

아시아태평양은 인쇄 필름 시장의 34.17%를 차지하고 있으며, 코스모 퍼스트(Cosmo First)사의 인도 내 연간 8만 1,200톤 규모의 생산 라인과 진달 폴리 필름스(Jindal Poly Films)사의 700카롤 루피(8,400만 달러) 규모의 확장 사업이 이를 주도하고 있습니다. 이로 인해 BOPP 및 BOPET 공급 분야에서 해당 지역의 주도적 입지가 강화되고 있습니다. 중국에서는 수지 부족에도 불구하고, 전자상거래용 봉투의 국내 수요가 한 자릿수 중반대의 성장률을 기록하며 확대되었습니다. 한편, 일본의 각 변환기 제조업체들은 엄격한 전환 관리가 요구되는 수출 지향적인 의약품 용도에 주력했습니다. 동남아시아 각국에서는 특수 라미네이트 분야에 대한 추가 투자가 이루어져, 해당 지역 전체의 인쇄 필름 시장이 더욱 심화되었습니다.

북미와 유럽은 저이동성 및 재활용 가능 필름의 판매 가격 상승에 힘입어, 합쳐서 세계 시장 가치의 거의 절반을 차지했습니다. 베리와 월드와의 합병 이후 암콜의 매출액 240억 달러는 업계 재편을 뚜렷이 보여주고 있으며, 몬디의 12억 유로(13억 4,000만 달러) 규모의 설비 투자 계획은 단일 소재 스탠드업 파우치의 생산량을 늘리고 있습니다. 2026년에 발효될 EU 포장 규제는 재활용이 가능한 구조로의 재설계를 촉진하고 있으며, 이러한 요구 사항이 성숙한 경제권 내 인쇄 필름 시장 규모를 유지하는 요인이 되고 있습니다.

중동은 2031년까지 연평균 성장률(CAGR) 3.96%를 기록하며 가장 높은 성장률을 보일 것으로 예측됩니다. 이는 GulfPack사의 연간 13만 5,000톤 규모의 BOPP 생산 라인 덕분에 사우디아라비아가 아프리카 및 남아시아로의 재수출 거점으로서의 위상을 확립하고 있기 때문입니다. 남미는 높은 잠재력을 지니고 있지만, 자본 지출을 억제하는 환율 변동에 직면해 있습니다. 한편, 아프리카는 여전히 수입 의존도가 높은 편이며, 남아프리카공화국과 이집트가 지역 허브 역할을 수행하며 기본적인 연포장재 수요를 충족시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the printed films market size is projected to expand from USD 7.21 billion in 2025 and USD 7.47 billion in 2026 to USD 8.91 billion by 2031, registering a CAGR of 3.59% during the forecast period (2026 to 2031).

This report is Segmented by Film Material (Polyethylene Films, Polypropylene Films, and More), Printing Technology (Flexographic Printing, and More), Printing Ink Type (Solvent-Based Inks, Water-Based Inks, and More), End-User Industry (Food and Beverage, Personal Care and Cosmetics, and More), Film Thickness (Up To 25 Mm, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Printed Films Market Trends and Insights

Rising Demand for Sustainable Packaging Solutions

Brand procurement contracts now embed circularity clauses that oblige converters to certify bio-based content and recyclability. CARBIOS secured US food-contact clearance in 2025 for enzymatically recycled polylactic-acid films, enabling closed-loop recovery without downcycling. Metalvuoto's bio-based barrier coating on PLA substrates delivers oxygen transmission below 5 cc/m2/day and extends produce shelf life by 40%. The EU Packaging and Packaging Waste Regulation, effective in 2026, introduces monetary penalties for non-compliant flexibles, prompting rapid substrate reformulation and boosting the adoption of sustainable printed films.

Growth of E-Commerce Boosting Protective Printed Films

Global parcel volumes reached 150 billion in 2025, each typically wrapped in 1.8 layers of film. Converters answered with high-impact polyethylene mailers that withstand >400 g-force puncture tests yet accept water-based flexo inks. Automated fulfillment centers favor coextruded slip layers with a 0.18 coefficient of friction to enable sortation belts to move 8,000 parcels per hour. Digital presses that swap graphics within 10 minutes support small promotional batches, aligning with same-day-delivery demands and sustaining market penetration of printed films in logistics packaging.

Volatility in Raw Material Prices for Printing Inks and Films

Polyethylene swung from USD 950/t to USD 1,320/t in 2025 on Middle East outages and China cracker shutdowns, slashing converter margins. Titanium dioxide climbed 18% YoY to USD 3,200/t in early 2026, inflating white-ink costs. Converters with captive resin or pigment facilities, such as Uflex, enjoy a 200-250 bp margin cushion, yet many independents are forced into quarterly repricing, limiting predictable investment in the printed films market.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in High-Resolution Digital Printing Technologies

- Increasing Adoption of Smart and Interactive Packaging

- Environmental Concerns Regarding Plastic Waste Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene accounted for 37.22% of 2025 revenue, yet polyester is on track to outpace the printed films market at a 3.61% CAGR, buoyed by pharmaceutical and high-barrier food formats that demand oxygen levels below 3 cc/m2/day. Toray's aluminum-oxide-coated PET delivers 0.8 cc/m2/day at 12 µm yet remains transparent, a specification low-density polyethylene cannot match without multilayer complexity. Polypropylene remains essential wherever heat-seal strength above 2.5 N/15 mm is required, while PVC's share continues to erode in food-contact applications due to phthalate bans. Emerging biopolymers currently have only mid-single-digit value but serve as a testbed for circularity pilots and keep the printed films market narrative around sustainability alive.

Cost-effective downgauging strategies are reinforcing polyester uptake. Innovia's nano-porous BOPP allows lettuce and berries to breathe without laser perforation, and Cosmo First's anti-fog PET keeps refrigerated pouches clear for a three-week shelf life. With regulators capping overall migration at 10 mg/dm2 in the EU, demand for food-grade resins with full traceability is increasing, positioning specialty PET grades as credible challengers to incumbent polyolefins within the printed films industry.

Flexo accounted for 41.82% share of 2025 revenue, but inkjet's 3.75% CAGR signals an inflection. Digital presses eliminate plate-mount downtime and run 500-meter jobs profitably, making them perfect for regional promotions and SKU proliferation. Windmoeller and Hoelscher's hybrid unit integrates flexo stations for static branding and inkjet heads for serialized QR codes, reducing cost per thousand impressions across mixed portfolios. Rotogravure remains relevant for snack and tobacco films exceeding 1 million meters, where cylinder costs amortize efficiently, and color variation must remain within +-1 ΔE.

Ongoing innovation keeps flexo competitive. Bobst's M6 line automatically registers plates and curtails setup scrap by 40%, narrowing waste differentials versus digital. Meanwhile, the printed films market for screen and pad technologies remains niche, focusing on conductive tracks and specialized tamper seals. Across print platforms, converters are weighing capital outlay against run-length flexibility, a trade-off that shapes future equipment purchases throughout the printed films industry.

Geography Analysis

Asia-Pacific accounted for 34.17% of the printed films market, anchored by India's 81,200 tpa line from Cosmo First and Jindal Poly Films' INR 700 crore (USD 84 million) expansion, which together reinforce regional leadership in BOPP and BOPET supply. China's domestic demand for e-commerce mailers grew at mid-single-digit rates despite resin shortages, while Japan's converters focused on export-oriented pharmaceutical applications that require stringent migration controls. Southeast Asian nations captured follow-on investment in specialty laminates, adding to the depth of the printed films market across the region.

North America and Europe jointly captured nearly one-half of global value, driven by higher selling prices for low-migration and recyclability-compliant films. Amcor's USD 24 billion revenue base after merging with Berry Global accentuates consolidation, and Mondi's EUR 1.2 billion (USD 1.34 billion) capex program increases mono-material stand-up pouch output. The EU Packaging Regulation, taking effect in 2026, spurs redesigns toward recyclable structures, an imperative that sustains the printed films market size in mature economies.

The Middle East is expected to post the fastest CAGR of 3.96% through 2031, as GulfPack's 135,000 tpa BOPP line positions Saudi Arabia as a re-export platform to Africa and South Asia. South America holds high potential but faces currency volatility that tempers capital spending, while Africa remains largely import-dependent, with South Africa and Egypt hosting regional hubs that serve basic flexible packaging needs.

- Sealed Air Corporation

- Amcor plc

- Huhtamaki Oyj

- Mondi plc

- Constantia Flexibles Group GmbH

- CCL Industries Inc.

- Sonoco Products Company

- Avery Dennison Corporation

- Uflex Limited

- Cosmo First Limited

- Klockner Pentaplast GmbH & Co. KG

- Toppan Inc.

- Dai Nippon Printing Co., Ltd.

- Taghleef Industries LLC

- POLIFILM GmbH

- FlexFilms Limited

- Jindal Poly Films Limited

- Innovia Films Limited

- Toray Industries, Inc.

- Bemis Company, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Sustainable Packaging Solutions

- 4.2.2 Growth of E-Commerce Boosting Protective Printed Films

- 4.2.3 Advancements in High-Resolution Digital Printing Technologies

- 4.2.4 Increasing Adoption of Smart and Interactive Packaging

- 4.2.5 Rapid Expansion of Printed Electronics on Flexible Substrates

- 4.2.6 Stringent Regulations Driving Biodegradable Printed Film Usage

- 4.3 Market Restraints

- 4.3.1 Volatility in Raw Material Prices for Printing Inks and Films

- 4.3.2 Environmental Concerns Regarding Plastic Waste Management

- 4.3.3 High Initial Capital Investment in Advanced Printing Presses

- 4.3.4 Supply Chain Disruptions Affecting Specialty Substrates

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Film Material

- 5.1.1 Polyethylene (PE) Films

- 5.1.2 Polypropylene (PP) Films

- 5.1.3 Polyester (PET) Films

- 5.1.4 Polyvinyl Chloride (PVC) Films

- 5.1.5 Other Film Materials

- 5.2 By Printing Technology

- 5.2.1 Flexographic Printing

- 5.2.2 Rotogravure Printing

- 5.2.3 Digital Inkjet Printing

- 5.2.4 Other Printing Technologies

- 5.3 By Printing Ink Type

- 5.3.1 Solvent-based Inks

- 5.3.2 Water-based Inks

- 5.3.3 UV/EB-curable Inks

- 5.3.4 Other Printing Ink Types

- 5.4 By End-user Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Pharmaceuticals

- 5.4.4 Homecare and Cleaning

- 5.4.5 Other End-user Industries

- 5.5 By Film Thickness

- 5.5.1 Up to 25 µm

- 5.5.2 25 - 50 µm

- 5.5.3 50 -100 µm

- 5.5.4 Above 100 µm

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Israel

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sealed Air Corporation

- 6.4.2 Amcor plc

- 6.4.3 Huhtamaki Oyj

- 6.4.4 Mondi plc

- 6.4.5 Constantia Flexibles Group GmbH

- 6.4.6 CCL Industries Inc.

- 6.4.7 Sonoco Products Company

- 6.4.8 Avery Dennison Corporation

- 6.4.9 Uflex Limited

- 6.4.10 Cosmo First Limited

- 6.4.11 Klockner Pentaplast GmbH & Co. KG

- 6.4.12 Toppan Inc.

- 6.4.13 Dai Nippon Printing Co., Ltd.

- 6.4.14 Taghleef Industries LLC

- 6.4.15 POLIFILM GmbH

- 6.4.16 FlexFilms Limited

- 6.4.17 Jindal Poly Films Limited

- 6.4.18 Innovia Films Limited

- 6.4.19 Toray Industries, Inc.

- 6.4.20 Bemis Company, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment