|

시장보고서

상품코드

2061915

플라즈마 절단기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Plasma Cutting Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

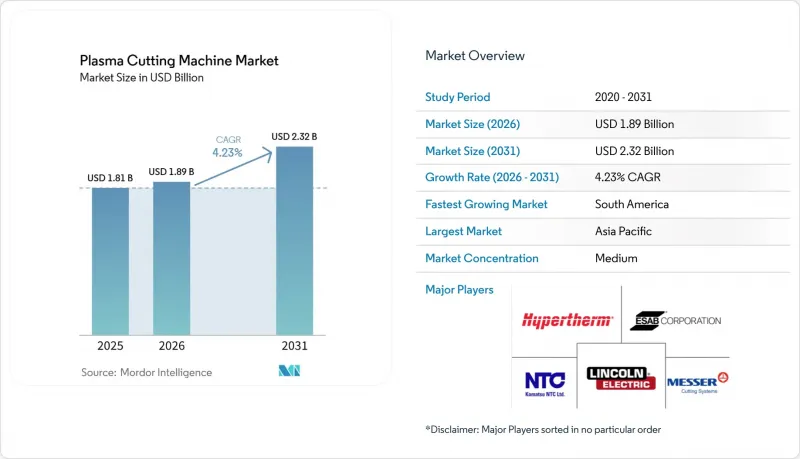

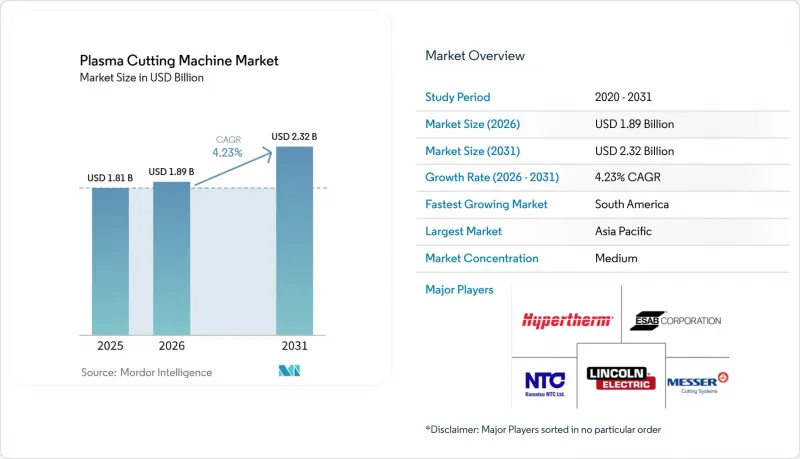

플라즈마 절단기 시장 규모는 2025년에 18억 1,000만 달러로 평가되었습니다. 2026년에 18억 9,000만 달러에 달하고, 2031년까지 23억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 4.23%를 나타낼 전망입니다.

본 보고서는 기술 유형별(기존, 첨단 HD), 자동화 수준별(수동/핸드헬드, 자동화·CNC, 하이브리드), 출력 용량별(120암페어 이하, 121-300암페어, 300암페어 초과), 최종 사용자 산업별(자동차 및 운송, 건설, 기타), 지역별(북미, 남미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(10억 달러) 기준으로 제시되어 있습니다.

세계의 플라즈마 절단기 시장 동향 및 인사이트

자동화 및 인더스트리 4.0 통합의 확산

국가 프로그램과 민관 파트너십을 통해 제조 분야의 디지털화 장벽이 낮아지고 있으며, 이에 따라 생산 현장에서 CNC 및 센서가 풍부하게 탑재된 플라즈마 시스템으로의 전환이 가속화되고 있습니다. Manufacturing USA는 15만 700명 이상의 학습자 및 근로자와의 협력을 보고했으며, 920건의 응용 연구개발 프로젝트를 지원하고 있으며, 시범 단계에서 상용화까지의 과정을 단축하는 디지털 기술 및 실증 시스템의 파이프라인을 강화하고 있습니다. NIST(미국 국립표준기술연구소)의 ‘스마트 제조 시스템 설계 및 분석’ 이니셔티브는 사이버-물리 시스템을 위한 참조 아키텍처와 보증 기법을 구축하고 있으며, 이를 통해 시스템 통합사업자는 컨트롤러, 로봇, 절단 플랫폼 간의 상호 운용성을 향상시킬 수 있습니다. 벤더들은 ERP 및 MES와의 연동과 관련하여 제조업체의 요구 사항을 충족하기 위해 개방형 인터페이스 및 표준화된 데이터 모델에 대한 대응을 추진하고 있으며, 이러한 동향은 공급업체의 정보 공개 및 기술 전시에도 반영되고 있습니다. NSF의 2026년도 예산 요청안에는 절단 작업 중 실시간 공정 제어 및 품질 문서화를 지원할 수 있는 AI 기반 디지털 트윈을 포함한 첨단 제조 기술에 대한 전용 자금이 배정되어 있습니다. 이러한 노력과 병행하여, 미국의 제조업체들은 2025년에 업무에 AI 도입이 급속히 진행되었다고 보고하고 있으며, 2027년까지 통합이 더욱 진전될 것으로 예상하고 있습니다. 이는 분석 기능과 폐쇄 루프 모니터링 기능을 탑재한 CNC 플라즈마 시스템에 대한 수요가 증가하고 있음을 시사합니다.

고화질(HD) 플라즈마 기술에 대한 수요 증가

HD 플라즈마에 대한 수요는 두꺼운 판재에서 엄격한 각도 정밀도와 용접 가능한 모서리가 요구되는 용도에 의해 뒷받침되고 있습니다. 이러한 용도에서는 레이저에 속도, 에지 품질 또는 듀티 사이클 측면에서 제약이 있습니다. HD 플랫폼은 코팅된 소재나 산화된 소재에서도 생산성 면에서 우위를 유지합니다. 이는 플라즈마가 레이저의 경우 시간이 오래 걸리는 전처리 공정이 필요한 표면 상태에도 견딜 수 있기 때문입니다. 두꺼운 판재 가공에서 HD 플라즈마가 처리량을 유지하고 열영향부를 제어할 수 있는 능력은 중장비, 조선, 구조용 강재 분야의 후속 공정 워크플로우 효율을 뒷받침하고 있습니다. 또한 제조업체들은 CNC 컨트롤러나 공장의 IT 시스템과 원활하게 통합될 수 있는 시스템을 선호하고 있습니다. 이는 이더넷 기반 인터페이스 및 표준 규격에 따른 데이터 교환을 통해 네트워크화된 공장으로의 통합이 간소화되기 때문입니다. 구매자가 두꺼운 판재의 생산성, 피복재에 대한 대응 능력, 인증 워크플로우를 비교 검토하는 과정에서 HD 플라즈마는 다품종·중간 두께부터 두꺼운 판재에 이르는 금속 가공을 수행하는 많은 현장에서 여전히 실용적인 선택지로 자리 잡고 있습니다.

파이버 레이저 절단 기술을 둘러싼 치열한 경쟁

파이버 레이저는 그 속도와 효율성 덕분에 박판에서 중판 분야에 걸쳐 급속히 보급되고 있으며, 시트 및 박판에 중점을 두는 제조업체들의 구매 결정을 재고하게 만들고 있습니다. 업계 비교에 따르면, 파이버 레이저는 벽면 콘센트 효율이 높고 박판 절단 속도가 훨씬 빠른 것으로 나타났으며, 2016년 이후 절단 작업 전반에 걸쳐 도입이 확대되고 있습니다. 각 공급업체들은 고도의 빔 품질을 갖춘 20kW를 초과하는 광섬유 출력 수준을 실현하고 있으며, 이를 통해 자동화 시스템에서 더 두꺼운 소재도 깔끔하게 절단하고 고속 가공할 수 있게 되었습니다. 기술적 검토에 따르면, 플라즈마는 일정 두께 이상의 연강이나 코팅된 소재, 녹슨 소재에서는 여전히 우위를 유지하고 있지만, 출력이 매우 높은 레이저의 경우 생산 공정에서 듀티 사이클이나 열 변형에 대한 우려가 발생할 수 있습니다. 다각적인 사업 전개를 펼치고 있는 각 기계 제조업체들은 전기차 배터리 접합 용도를 포함해 용접 및 절단용 파이버 제품군에 대한 투자를 지속하고 있으며, 이로 인해 과거에는 플라즈마가 표준으로 여겨졌던 인접한 작업 흐름에서도 레이저의 도입이 더욱 정당화되고 있습니다.

부문별 분석

기존 플라즈마 절단기는 2025년에 56.71%의 시장 점유율을 차지했습니다. 이는 일반 제조, 건설 서비스 센터 및 유지보수 업무 분야에서 확고한 도입 실적을 바탕으로 하고 있으며, 제한된 설비 투자 예산이 선택의 기준이 되고 있습니다. 사용자들이 더욱 엄격한 공차와 두꺼운 부위의 일관된 모따기 품질을 요구함에 따라, 첨단 고해상도(HD) 플랫폼의 인기가 높아지고 있으며, 2031년까지 연평균 성장률(CAGR)이 6.41%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 부문이 되고 있습니다. OEM 품질 기준이 강화됨에 따라, 많은 가공 업체들은 안정적인 모서리 품질, 2차 마감 작업의 감소, 그리고 두꺼운 판재 가공 시 안정적인 처리량을 요구하는 중요한 구조 부품 및 전기차 배터리 케이스를 위해 HD 플라즈마로 전환하고 있습니다. 기존 플랫폼은 계속해서 대량으로 출하될 것이지만, 구매자들이 HD 시스템의 생산성 향상, 소모품 수명, 용접 적합성 등의 장점을 중시함에 따라 시장 점유율이 감소할 것으로 예측됩니다. 이러한 경향은 조선 및 항공우주 분야의 절단 요건이 더욱 엄격해지고 있는 시장에서 더욱 두드러집니다. 이러한 이용 사례에서는 두꺼운 판재나 피복재에 대해 신뢰할 수 있는 결과가 요구되며, 플라즈마 가공이 공정상 우위를 유지하고 있는 분야이기 때문입니다.

산업 분야 전반의 활용 사례에서 현대화 전략의 경우 기계의 전면적인 교체보다는 테이블이나 제어 장치의 업그레이드가 선호되는 경향이 있으며, 이로 인해 개조 키트 및 고성능 소모품에 대한 수요가 유지되고 있습니다. Grosschadl Stahl사의 2026년 현대화 프로젝트는 기존 설치 면적을 유지하면서 개선된 토치, 모션 시스템 및 소프트웨어를 활용하여 제조업체가 기존 설비를 혁신하는 방법을 보여주고 있습니다. 해군 및 민간 조선소에서는 해상 역량 확대와 현대화를 위한 정책 지원에 힘입어, 산업 수준의 처리 능력으로 두꺼운 해군용 강재와 내식성 합금을 절단할 수 있는 고전류 플라즈마 기술에 투자가 집중되고 있습니다. 이러한 수요를 고려할 때, 다중 공정 통합, 재현성 있는 모따기, 인증 가능한 에지 품질이 가장 중요시되는 분야에서는 HD 시스템이 계속해서 부가가치를 창출해 나갈 것이며, 반면 비용 효율성이나 현장 수리가 필요한 상황에서는 기존 유닛이 시장 점유율을 유지하게 될 것입니다. 2025년 시점에서 플라즈마 절단기 시장 점유율의 56.71%를 기존 시스템이 차지하고 있었으나, 보다 중량급 용도에서 HD 시스템의 도입이 확대됨에 따라 설치 대수 기준 규모와 시장 가치 확보 간의 격차는 더욱 확대될 전망입니다. 플라즈마 절단기 시장은 절단 품질 기준과, 사용자가 생산 수요 및 예산에 맞추어 현대화 시기를 조정할 수 있는 업그레이드 경로를 따라 계속해서 세분화될 것입니다.

지역별 분석

2025년, 아시아태평양은 플라즈마 절단기 시장 점유율의 28.71%를 차지했으며, 중국의 전기차 생산 거점과 자동차 및 산업용 가공 분야에 대한 꾸준한 투자가 이를 주도하고 있습니다. 남미는 자동차 산업의 확대와 열절단 장비 도입 대수 증가를 배경으로, 2031년까지 연평균 성장률(CAGR) 5.42%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 이는 북미와 남미에서 자동화 및 설비 포트폴리오 확대를 목표로 하는 기업 투자에 힘입은 것입니다. 중국의 전기차 판매 호조와 더 광범위한 아시아태평양공급망은 중후판 및 후판 분야 모두에서 유연한 플라즈마 가공 능력에 대한 수요를 지속적으로 뒷받침하고 있습니다. 북미에서는 해양 정책 제안 및 조선소 자본 재구축에 따라, 두꺼운 해군용 강재와 알루미늄을 가공할 수 있는 대형 시스템에 대한 투자가 촉진되어야 하며, 이를 통해 대규모 제조 프로그램에 참여하는 공급업체들이 지원을 받게 될 것입니다. 남미의 플라즈마 절단기 시장 규모는 비용 효율이 높은 플랫폼이 자동화를 처음 도입하는 구매자들 사이에서 지지를 얻음에 따라, 2031년까지 연평균 성장률(CAGR) 5.42%로 확대될 것으로 전망됩니다.

유럽에서는 양극화된 추세가 나타나고 있습니다. 서유럽의 주요 지역에서는 자동차 및 항공우주 공급망을 대상으로 HD 플라즈마 기술과 엄격한 공차가 중시되는 반면, 중동유럽에서는 구조용 및 일반 제조 분야에서 비용 효율성과 기존 설비의 업그레이드가 중시되고 있습니다. EU의 산업·해사 전략은 회원국 전체 조선소의 현대화 및 디지털화 노력을 강화하고 있으며, 이를 통해 두꺼운 강판이 여전히 주요 작업량을 차지하는 분야에서 더욱 자동화된 플라즈마 모따기 절단 및 통합 셀이 지원됩니다. 서유럽이 더 높은 정밀도와 추적성을 추구하는 반면, 동유럽에서는 예산 제약과 업그레이드 간의 균형을 맞추어 기존의 플라즈마 절단기를 지속적으로 활용하면서 HD(고해상도) 기술로의 단계적 도입을 추진하고 있습니다. 따라서 유럽의 플라즈마 절단기 시장은 서부의 인증 중심형 HD부터 동부의 수명 주기를 중시하는 개조형에 이르기까지, 앞으로도 구매자의 우선순위 차이를 계속 반영할 것입니다.

중동 및 아프리카에서는 여전히 상황이 제각각입니다. 만안 국가들에서는 해양 및 에너지 관련 프로젝트로 인해 고전류 수요가 유지되고 있는 반면, 사하라 이남 시장에서는 전력망과 인프라의 불안정성으로 인해 휴대용 장치가 선호되고 있습니다. 남아시아에서는 인도의 첨단 제조 로드맵이 로봇 공학과 디지털 트윈을 우선순위로 두고 있어, 이에 따라 중소기업 및 소규모 기업(MSME) 클러스터와 공유 시설 내에서 중-고전류 CNC 플라즈마 절단기의 단계적 도입이 촉진되고 있습니다. 북미에서는 공공 프로그램이 계속해서 수천 개에 달하는 기관의 연구개발(R&D) 및 인재 양성을 지원하고 있으며, 이를 통해 최첨단 플랫폼에서 자동화 및 실시간 품질 관리 시스템을 도입하려는 중소기업의 위험이 완화되고 있습니다. 이러한 지역별 경향은 정책 지원, 업계 연수, 공급망 요건이 복합적으로 작용하여 자동화 및 교체 주기의 타당성이 인정되는 지역에서 플라즈마 절단기 시장이 가장 빠르게 성장하고 있음을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the plasma cutting machine market size is projected to be USD 1.81 billion in 2025, USD 1.89 billion in 2026, and reach USD 2.32 billion by 2031, growing at a CAGR of 4.23% from 2026 to 2031.

This report is Segmented by Technology Type (Conventional, Advanced HD), by Automation Level (Manual/Handheld, Automated & CNC, Hybrid), by Power Capacity (<=120 Amp, 121-300 Amp, Above 300 Amp), by End-User Industry (Automotive & Transportation, Construction, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Global Plasma Cutting Machine Market Trends and Insights

Rising Adoption of Automation and Industry 4.0 Integration

National programs and public-private partnerships are lowering barriers to digital adoption in fabrication, which accelerates the shift toward CNC and sensor-rich plasma systems in production settings. Manufacturing USA reported engagement with more than 150,700 learners and workers and supported 920 applied R&D projects, reinforcing a pipeline of digital skills and demonstrators that shorten the path from pilot to scale. NIST's Smart Manufacturing Systems Design and Analysis initiative is building reference architecture and assurance methods for cyber-physical systems, which helps integrators improve interoperability across controllers, robots, and cutting platforms. Equipment vendors are aligning with open interfaces and standardized data models to satisfy fabricators' requirements for ERP and MES connectivity; a trend reflected in supplier communications and technology showcases. The NSF's FY2026 request allocates dedicated funding for advanced manufacturing, including AI-enabled digital twins that can assist with real-time process control and quality documentation during cutting operations. Parallel to these initiatives, U.S. manufacturers reported rapid AI adoption in operations in 2025 and expect further integration by 2027, signaling rising demand for CNC plasma systems that embed analytics and closed-loop monitoring.

Increasing Demand for High-Definition (HD) Plasma Technology

Demand for HD plasma is supported by applications that require tight angularity and weld-ready edges on thicker materials, where lasers face constraints in speed, edge quality, or duty cycle. HD platforms maintain productivity advantages on coated and oxidized stock because plasma tolerates surface conditions that would otherwise require time-consuming preparation steps with lasers. In thick-plate fabrication, HD plasma's ability to sustain throughput and manage heat-affected zones supports downstream workflow efficiency in heavy equipment, shipbuilding, and structural steel. Fabricators also favor systems that integrate cleanly with CNC controllers and plant IT, since Ethernet-based interfaces and standards-driven data exchange simplify integration into connected shops. As buyers compare thick-plate productivity, coated-material tolerance, and certification workflows, HD plasma remains a practical choice for many high-mix, mid-to-thick metal operations.

Intense Competition from Fiber Laser Cutting Technology

Fiber lasers have expanded quickly in thin-to-mid thickness bands due to speed and efficiency, which reshapes purchase choices for fabricators focused on sheet and thin plate. Industry comparisons point to higher wall-plug efficiency and much faster thin-gauge speeds for fiber lasers, along with broader adoption across cutting workflows since 2016. Suppliers are scaling fiber power levels beyond 20 kW with advanced beam quality, which supports cleaner cutting and higher velocities on thicker materials in automated systems. Technical reviews note that plasma retains advantages on mild steel above certain thickness thresholds and on coated or rusty stock, while very high laser powers can face duty cycle and heat distortion concerns in production. Diversified machine builders continue to invest in fiber portfolios for welding and cutting, including EV battery joining applications, which strengthens the case for lasers in adjacent workflows that once defaulted to plasma.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Automotive and Aerospace Manufacturing Demand

- Cost-Effectiveness and Superior Speed for Medium-to-Thick Metal Processing

- Shortage of Skilled Operators and Training Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional plasma cutting machines commanded 56.71% share in 2025, supported by entrenched installed bases in general fabrication, construction service centers, and maintenance operations, and lower capital budgets guide choices. Advanced high-definition platforms are gaining popularity as users pursue tighter tolerances and more consistent bevel quality on thicker sections, with the fastest cohort forecast at a 6.41% CAGR through 2031. As OEM quality thresholds rise, many fabricators are repositioning to HD plasma for structural components and EV battery enclosures where stable edge quality, reduced secondary finishing, and robust thick-plate throughput matter. Conventional platforms will continue to ship in high volumes, but share erosion is likely as buyers weigh productivity gains, consumable life, and weld-readiness benefits in HD systems. This shift is more pronounced in markets where shipbuilding and aerospace cutting requirements tighten, since these use cases depend on reliable results in thicker materials and coated stock, areas where plasma sustains process advantages.

Across industrial use cases, modernization strategies often favor upgrading tables and controls rather than full machine replacement, which sustains demand for retrofit kits and advanced consumables. A 2026 modernization project at Grosschadl Stahl illustrates how fabricators refresh legacy assets with improved torches, motion systems, and software while preserving existing footprints. In naval and commercial shipyards, policy support for maritime capacity expansion and modernization tilts investment toward high-amperage plasma that can cut thick naval steels and corrosion-resistant alloys at industrial throughput. Given these needs, HD systems will continue to capture incremental value where multi-process integration, repeatable bevels, and certifiable edge quality matter most, while conventional units retain volume in cost-conscious and field-repair contexts. Conventional systems held 56.71% of the plasma cutting machines market share in 2025, and the gap between installed-base volume and value capture will widen as HD adoption steps up in heavier applications. The plasma cutting machines market continues to segment along cut-quality thresholds and upgrade pathways that let users time modernization to production demands and budgets.

Geography Analysis

Asia-Pacific held 28.71% of the plasma cutting machines market share in 2025, led by China's EV manufacturing base and steady investment in automotive and industrial fabrication. South America is the fastest-growing region at a 5.42% CAGR through 2031 on the back of automotive expansions and a rising installed base for thermal cutting, aided by corporate investments that broaden automation and equipment portfolios in the Americas. China's EV sales strength and broader APAC supplier networks continue to support demand for flexible plasma capacity in both mid and high thickness ranges. In North America, maritime policy proposals and yard recapitalization need to favor investments in heavy-duty systems that can process thick naval steel and aluminum, which supports suppliers serving large fabrication programs. The plasma cutting machines market size in South America is projected to expand at a 5.42% CAGR through 2031 as cost-effective platforms gain traction among first-time automation buyers.

Europe shows a dual-speed profile. Western centers emphasize HD plasma technology and tight tolerances for automotive and aerospace supply chains, while Central and Eastern Europe emphasize cost-effectiveness and installed-base upgrades in structural and general fabrication. The EU's industrial maritime strategy strengthens modernization and digitization initiatives in yards across member states, which supports more automated plasma bevel cutting and integrated cells where thick steel remains a core workload. As Western Europe pursues higher precision and traceability, Eastern Europe balances upgrades with budget constraints, keeping conventional plasma relevant alongside gradual HD adoption. The plasma cutting machines market in Europe will therefore continue to reflect distinct buyer priorities, from certification-driven HD in the west to lifecycle-focused retrofits in the east.

The Middle East and Africa remain mixed, with offshore and energy projects in the Gulf countries sustaining high-amperage demand, while sub-Saharan markets favor portable units due to grid and infrastructure variability. In South Asia, India's advanced manufacturing roadmap prioritizes robotics and digital twins, which support incremental adoption of mid-to-high amperage CNC plasma within MSME clusters and shared-use facilities. In North America, public programs continue to back R&D and workforce development across thousands of organizations, which reduces risk for SMEs pursuing automation and real-time quality systems on cutting-edge platforms. These regional patterns reinforce that the plasma cutting machines market grows fastest where policy support, industry training, and supply-chain requirements intersect to justify automation and upgrade cycles.

- Hypertherm

- ESAB Corporation

- Lincoln Electric

- Komatsu NTC

- Messer Cutting Systems

- TRUMPF

- Koike Aronson

- Hornet Cutting Systems

- Jinan Style CNC

- Huayuan Electric

- GCE Holding

- Shanghai Friendess Electronic (StarFire CNC)

- Technocrats Plasma Systems

- ProArc Welding & Cutting

- FastCut CNC

- Thermadyne Holdings (Victor Technologies)

- Vanad 2000 a.s.

- Arcbro CNC

- Wuhan Huagong Laser Engineering

- Boss Tables

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Automation and Industry 4.0 Integration

- 4.2.2 Increasing Demand for High-Definition (HD) Plasma Technology

- 4.2.3 Expanding Automotive and Aerospace Manufacturing Demand

- 4.2.4 Cost-Effectiveness and Superior Speed for Medium-to-Thick Metal Processing

- 4.2.5 Rapid Infrastructure Development and Construction Growth

- 4.2.6 Growth of Shipbuilding, Marine, and Offshore Industries

- 4.3 Market Restraints

- 4.3.1 Intense Competition from Fiber Laser Cutting Technology

- 4.3.2 High Initial Investment and Total Cost of Ownership

- 4.3.3 Shortage of Skilled Operators and Training Requirements

- 4.3.4 Precision and Cut Quality Limitations for High-Tolerance Applications

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Industry Transformation Through Digital Integration

5 Market Size & Growth Forecasts(Value, In USD Billion)

- 5.1 By Technology Type

- 5.1.1 Conventional Plasma Cutting Machines

- 5.1.2 Advanced (HD) Plasma Cutting Machines

- 5.2 By Automation Level

- 5.2.1 Manual / Handheld Plasma Cutting Machines

- 5.2.2 Automated & CNC Plasma Cutting Machines

- 5.2.3 Hybrid Plasma Cutting Machines

- 5.3 By Power Capacity

- 5.3.1 <=120 Amp

- 5.3.2 121-300 Amp

- 5.3.3 Above 300 Amp

- 5.4 By End-User Industry

- 5.4.1 Automotive & Transportation

- 5.4.2 Industrial Machinery & Heavy Equipment

- 5.4.3 Shipbuilding & Offshore

- 5.4.4 Construction & Infrastructure

- 5.4.5 Aerospace & Defense

- 5.4.6 Others (general metal fabrication, energy & power, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Hypertherm

- 6.4.2 ESAB Corporation

- 6.4.3 Lincoln Electric

- 6.4.4 Komatsu NTC

- 6.4.5 Messer Cutting Systems

- 6.4.6 TRUMPF

- 6.4.7 Koike Aronson

- 6.4.8 Hornet Cutting Systems

- 6.4.9 Jinan Style CNC

- 6.4.10 Huayuan Electric

- 6.4.11 GCE Holding

- 6.4.12 Shanghai Friendess Electronic (StarFire CNC)

- 6.4.13 Technocrats Plasma Systems

- 6.4.14 ProArc Welding & Cutting

- 6.4.15 FastCut CNC

- 6.4.16 Thermadyne Holdings (Victor Technologies)

- 6.4.17 Vanad 2000 a.s.

- 6.4.18 Arcbro CNC

- 6.4.19 Wuhan Huagong Laser Engineering

- 6.4.20 Boss Tables

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment