|

시장보고서

상품코드

2061916

수생 제초제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aquatic Herbicides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

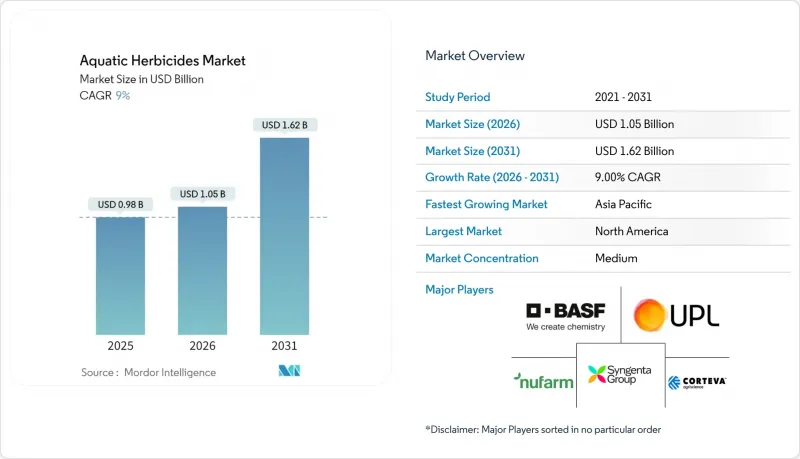

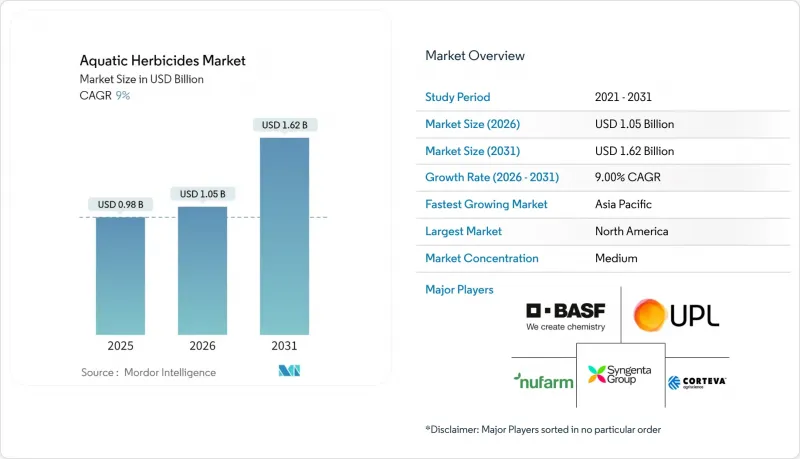

Mordor Intelligence에 의하면, 수생 제초제 시장은 2025년 9억 8,000만 달러로 평가되었습니다. 2026년에는 10억 5,000만 달러로 확대되어 2031년까지 16억 2,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 9%를 기록할 전망입니다.

본 보고서는 제품 유형(글리포세이트, 2,4-D, 기타), 작용기전(선택성 제초제, 기타), 시용 방법(엽면 살포, 기타), 최종 사용자 산업(농업용 수역, 기타), 제형(농축액, 기타), 지역(북미, 남미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 수생 제초제 시장 동향 및 분석

수력 발전용 저수지에서의 침입 외래 식물 발생

신흥 지역에서는 침입성 대형 수생 식물이 터빈의 취수구를 막아 수력 발전 시설의 발전 용량을 저하시키고 있습니다. 예를 들어, 물수련 군락은 심각한 관리상의 문제를 야기하고 있어, 지속적인 제초제 살포 프로그램이나 기계적 제거 방식의 도입을 촉진하고 있습니다. 연방 정부의 자금 지원 계획은 발전 및 레크리에이션 활동에 대한 침입 외래종이 초래하는 위협에 대한 인식이 높아지고 있음을 여실히 보여주고 있습니다. 사업자들은 사후 대응적 조치에서 벗어나, 유역 전체에 대한 지도 작성, 조기 발견을 위한 감시, 호수 전체에 대한 제초제 살포와 같은 예방적 전략으로 전환하고 있습니다. 이러한 변화가 효율적인 화학적 솔루션과 정밀 살포 시스템에 대한 수요를 이끌고 있습니다.

저위험 유효 성분의 신속한 승인

2024년, 미국 환경보호청(EPA)은 수생 환경에서의 사용을 목적으로 한 글루포시네이트-P를 승인했으며, 이는 수중 식물에 대한 처리에 있어 최초의 포스핀산계 제제 선택지가 되었습니다. FMC 코퍼레이션은 2026년에 도디렉스(Dodhylex)를 도입할 예정입니다. 유럽과 북미 간의 노출 모델 및 독성학적 평가 지표의 조화를 통해 승인 절차가 신속화되고 있으며, 이는 선택적 독성과 빠른 분해 특성을 지닌 화합물에 유리하게 작용하고 있습니다. 이러한 발전은 혁신을 촉진하는 한편, 시장 진입과 지속가능성 측면에서 엄격한 규제 준수가 필수적인, 규정 준수를 중시하는 고부가가치 시장 부문에서의 경쟁도 심화시키고 있습니다.

엄격한 독성학적 재등록

2025년, 미국 환경보호청(EPA)은 갱신된 생태학적 위험 평가를 바탕으로 다수의 농약 유효 성분에 대한 개정된 독성 기준치를 반영하여 ‘수생생물 벤치마크’를 갱신했습니다. 동시에, 유럽식품안전청(EFSA)은 유럽연합(EU)의 농약 규정에 따라 내분비 교란 작용 및 생태 독성에 관한 데이터에 대해 계속해서 엄격한 요건을 적용하고 있습니다. 이러한 규제에서는 수생 생물을 대상으로 한 고차원적이고 장기적인 연구가 의무화되는 경우가 많아지고 있습니다. 규제 기준의 발전에 따라 데이터 요구 사항이 증가하고, 승인까지 걸리는 기간이 길어지면서 제조업체의 규정 준수 비용이 증가하고 있으며, 이는 큰 진입 장벽이 되어 공급 제약의 한 원인이 되고 있습니다.

부문별 분석

2025년에는 글리포세이트가 수생 제초제 시장에서 42.5%라는 가장 높은 점유율을 차지했으나, 2026년부터 2031년까지는 이마자목스가 11.2%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예측되며, 포트폴리오의 단계적 재편이 진행되고 있음을 시사합니다. 데이터에 따르면, 이마자목스는 침수 처리 시 500ppb, 엽면 살포 시 1에이커당 32액량온스의 농도로 수생 잡초를 효과적으로 방제할 수 있는 것으로 나타났습니다. 수산물 양식 투자자들은 고부가가치 어류와 갑각류를 보호하기 위해 기존 유효 성분보다 30%-50% 더 비싼 프리미엄을 지불하는 것을 마다하지 않으며, 이마자목스에 큰 관심을 보이고 있습니다. 트리클로필과 2,4-D가 특정 수변 목본 식물의 요구를 충족시키는 반면, 지콰트는 제네릭 대체제의 유입으로 인해 이익률 압박에 직면해 있습니다.

앞으로의 추세를 살펴보면, 제제 제조업체들은 저위험 유효 성분과 보조제를 조합하는 사례가 늘어나고 있으며, 이를 통해 흡수 효율을 높이고 환경 내 유효 기간을 연장하고 있습니다. 선택성을 지닌 분자에 대한 수요가 증가함에 따라, 판매업체들은 더욱 엄격해지는 잔류 기준에 대응하기 위해 재고 구성을 재검토하고 있습니다. FMC 코퍼레이션이 2026년 출시를 예정하고 있는 새로운 작용기전을 가진 ‘도디렉스’는 글리포세이트 시장 지배력에 도전할 준비를 마쳤습니다. 요약하자면, 수생 제초제 시장은 판매량에서 부가가치로 점차 초점을 옮기고 있으며, 선택성이 높은 유효 성분이 중요시되고 있습니다.

2025년 기준, 비선택성 제초제가 수생 제초제 시장에서 55.1%라는 가장 높은 점유율을 유지했으나, 2026년부터 2031년까지는 선택성 제제가 연평균 성장률(CAGR) 9.4%라는 가장 빠른 속도로 성장할 것으로 전망됩니다. 이 선택성 제제는 방글라데시의 쌀·어류·채소 통합형 습지 농업에 적합하며, 해당국의 농가들은 벼 모종과 양식 어류를 모두 보호해야 합니다. 북미의 규제 제도에서는 선택성이 높은 제품에 대해 ‘저위험(Reduced Risk)’ 지정을 통해 우대하고 있으며, 이를 통해 라벨 승인이 가속화되어 시장 진입까지의 기간이 단축되고 있습니다.

한편, 남미에서는 수력 발전소나 관개 지역에서 비선택성 제초제가 여전히 선호되고 있습니다. 그 목적은 헥타르당 비용을 최소화하면서 송수 능력을 최적화하는 데 있습니다. 이러한 시장 역학의 변화에 대응하기 위해 각 벤더는 분할 살포 프로그램을 도입하고 있습니다. 이는 저용량의 비선택성 제초제와 그에 이어지는 선택성 제초제의 살포를 결합한 것으로, 효과, 비용 및 생태학적 고려 사항 간의 균형을 맞추고 있습니다. 이러한 혁신적인 하이브리드 전략을 통해 수생용 제초제 시장에서 선택성 제품의 선택지가 확대되는 한편, 비선택성 화학물질의 중요성도 유지될 것입니다.

지역별 분석

2025년, 북미는 수생 제초제 시장에서 35%라는 최대 시장 점유율을 차지했으며, 이는 견고한 규제 체계와 공공 자금 지원에 힘입은 결과입니다. 오대호 재생 이니셔티브에 대한 누적 투자액은 40억 달러를 넘어섰으며, 초당적 인프라 법안에 따라 생태계 복원을 위한 추가 자금이 지원되고 있습니다. 주 차원의 프로그램도 수요를 더욱 부추기고 있습니다. 또한, 미국 환경보호청(EPA)이 플로르피라옥시펜-벤질 등 새로운 제초제 유효 성분을 승인한 것은 선택성이 더 높고 환경 기준을 충족하는 화학 물질로의 전환을 반영한 것입니다.

2026년부터 2031년에 걸쳐 아시아태평양은 수생 제초제 시장에서 가장 빠른 성장세를 보일 것으로 예상되며, 연평균 성장률(CAGR)은 9.5%에 달할 전망입니다. 이러한 성장은 수산 양식 및 수자원 인프라의 확장에 기인합니다. 유엔식량농업기구(FAO)에 따르면, 아시아는 전 세계 양식 생산량의 85% 이상을 차지하고 있으며, 중국, 인도, 인도네시아, 베트남이 이에 크게 기여하고 있습니다. 수련풀과 같은 침입성 수생 잡초의 확산은 생산성에 악영향을 미치며, 제초제에 대한 의존도를 높이고 있습니다. 또한, 중국의 글리포세이트 및 디콰트 대량 생산은 비용 경쟁력을 높이고 있지만, 지역 전체에 걸친 규제 차이는 중소규모 시장 참여자들에게 과제로 대두되고 있습니다.

유럽, 남미, 중동 및 아프리카에서는 규제와 투자 동향의 영향을 받아 다양한 시장 역학이 나타나고 있습니다. 유럽에서는 유럽식품안전청(EFSA)이 내분비 교란 작용 평가를 포함한 엄격한 농약 승인 절차를 시행하고 있으며, 이것이 신규 유효 성분의 상품화를 지연시키는 요인이 되고 있습니다. 브라질에서는 수생 잡초의 관리 방법이 용도에 따라 다릅니다. 관개 수로에서는 일반적으로 화학 제초제가 사용되는 반면, 환경적으로 민감한 지역에서는 기계적인 제거가 선호됩니다. 아프리카와 중동에서는 세계은행 등의 기관이 지원하는 수력 발전 및 수자원 인프라에 대한 투자 확대가, 제초제와 모니터링 시스템을 결합한 통합 수생식물 관리 기법의 도입을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the aquatic herbicides market is projected to grow from USD 0.98 billion in 2025 to USD 1.05 billion in 2026, and is forecast to reach USD 1.62 billion by 2031, marking a 9% CAGR from 2026 to 2031.

This report is Segmented by Product Type (Glyphosate, 2, 4-D, and More), by Mode of Action (Selective Herbicides, and More), by Application Method (Foliar Application, and More), by End-User Industry (Agricultural Water Bodies, and More), by Formulation (Liquid Concentrates, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aquatic Herbicides Market Trends and Insights

Invasive-Weed Outbreaks In Hydropower Reservoirs

Invasive macrophytes are obstructing turbine intakes and reducing capacity at hydropower assets in emerging regions. For instance, water-hyacinth mats have caused significant operational challenges, prompting the adoption of continuous herbicide programs and mechanical removal. Federal funding initiatives highlight the growing recognition of the threat invasive species pose to power generation and recreation. Operators are shifting from reactive measures to proactive strategies, such as basin-wide mapping, early-detection surveillance, and whole-lake herbicide treatments. This shift is driving demand for efficient chemical solutions and precision delivery systems.

Faster Permitting Of Reduced-Risk Actives

In 2024, the United States Environmental Protection Agency (EPA) approved glufosinate-P for aquatic use, marking the first phosphinic-acid option for submersed treatments . FMC Corporation intends to introduce Dodhylex in 2026. Harmonized exposure modeling and toxicology endpoints in Europe and North America are expediting approvals, benefiting molecules with selective toxicity and rapid degradation. These advancements are fostering innovation while also increasing competition in premium, compliance-sensitive market segments, where adherence to stringent regulations is critical for market entry and sustainability.

Stringent Toxicological Re-Registration

In 2025, the United States Environmental Protection Agency (EPA) updated its Aquatic Life Benchmarks, incorporating revised toxicity thresholds for numerous pesticide active ingredients based on updated ecological risk assessments. Concurrently, the European Food Safety Authority (EFSA) continues to enforce stringent requirements for endocrine disruption and ecotoxicological data under European Union pesticide regulations. These regulations often mandate higher-tier and long-term studies on aquatic species. The evolving regulatory standards have increased data requirements, extended approval timelines, and raised compliance costs for manufacturers, creating significant entry barriers and contributing to supply constraints.

Other drivers and restraints analyzed in the detailed report include:

- Eco-Tourism And Blue-Economy Funding For Lake Restoration

- Aquaculture Acreage Expansion Driving Demand

- Price Compression From Generic Glyphosate And Diquat Oversupply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glyphosate generated the largest 42.5% market share for aquatic herbicides in 2025, while imazamox is projected to log the fastest 11.2% CAGR from 2026 to 2031, pointing to progressive portfolio realignment. Data shows that imazamox can effectively control aquatic weeds at submerged rates of 500 parts per billion and foliar rates of 32 fluid ounces per acre . Investors in aquaculture are gravitating towards imazamox, willing to pay a 30%-50% premium over traditional actives to protect their high-value fish and crustaceans. While triclopyr and 2,4-D cater to specific woody shoreline needs, diquat is facing margin pressures due to an influx of generic alternatives.

Looking ahead, formulators are increasingly combining reduced-risk actives with adjuvants, enhancing uptake efficiency and extending environmental application windows. As the demand for selective molecules rises, distributors are reshaping their inventories to meet tightening residue tolerances. FMC Corporation's upcoming launch of Dodhylex in 2026, a new mode-of-action chemistry, is poised to challenge glyphosate's market dominance. In summary, the aquatic herbicides market is gradually shifting its focus from volume to value, emphasizing high-selectivity actives.

Non-selective herbicides maintained the largest 55.1% market share for the aquatic herbicides in 2025, yet selective formulas will advance at the fastest 9.4% CAGR from 2026 to 2031. Selective options suit integrated rice-fish-vegetable wetlands in Bangladesh, where farmers need to protect both rice seedlings and stock. Regulatory regimes in North America reward selectivity with Reduced Risk designations, accelerating label clearance and shortening market entry.

Conversely, in South America, hydropower and irrigation districts continue to favor non-selective herbicides. Their goal is to optimize conveyance capacity while minimizing costs per hectare. To address the evolving market dynamics, vendors are introducing split-application programs. These combine a lower-rate non-selective knockdown with a subsequent selective application, striking a balance between efficacy, cost, and ecological considerations. Such innovative hybrid strategies ensure that while the market for aquatic herbicides expands its selective offerings, non-selective chemistry remains pertinent.

Geography Analysis

In 2025, North America held the largest market share of 35% in the aquatic herbicides market, driven by robust regulatory frameworks and public funding initiatives. The Great Lakes Restoration Initiative has seen cumulative investments exceeding USD 4 billion, with additional funding provided under the Bipartisan Infrastructure Law for ecosystem restoration. State-level programs further bolster demand. Additionally, the approval of newer herbicide actives, such as florpyrauxifen-benzyl, by the United States Environmental Protection Agency reflects a shift toward more selective and environmentally compliant chemistries.

From 2026 to 2031, the Asia-Pacific region is projected to experience the fastest growth in the aquatic herbicides market, with a CAGR of 9.5%. This growth is attributed to the expansion of aquaculture and water infrastructure. According to the Food and Agriculture Organization, Asia accounts for over 85% of global aquaculture production, with significant contributions from China, India, Indonesia, and Vietnam. The prevalence of invasive aquatic weeds, such as water hyacinth, negatively impacts productivity, increasing the reliance on herbicides. Furthermore, China's strong domestic production of glyphosate and diquat enhances cost competitiveness, although regulatory fragmentation across the region poses challenges for smaller market players.

Europe, South America, the Middle East, and Africa exhibit diverse market dynamics influenced by regulatory and investment trends. In Europe, the European Food Safety Authority enforces stringent pesticide approval protocols, including assessments for endocrine disruption, which can delay the commercialization of new active ingredients. In Brazil, aquatic weed management practices vary by application. Chemical herbicides are commonly used in irrigation canals, while mechanical removal is preferred in environmentally sensitive areas. In Africa and the Middle East, increasing investments in hydropower and water infrastructure, supported by institutions such as the World Bank, are driving the adoption of integrated aquatic vegetation management approaches that combine herbicides with monitoring systems.

- Syngenta AG

- BASF SE

- Corteva, Inc.

- UPL Limited

- Nufarm Limited

- SePRO Corporation

- Sumitomo Chemical Company, Limited (Valent USA)

- Arxada AG

- Nippon Soda Co., Ltd.

- Alligare, LLC

- Albaugh, LLC

- FMC Corporation

- Hangzhou Tianlong Biotechnology Co., Ltd.

- Aquatic Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Invasive-weed outbreaks in hydropower reservoirs

- 4.2.2 Faster permitting of reduced-risk actives

- 4.2.3 Eco-tourism and blue-economy funding for lake restoration

- 4.2.4 Aquaculture acreage expansion driving demand

- 4.2.5 Digital bathymetry and drone spraying cutting costs

- 4.2.6 Bio-based chelation carriers improving copper-herbicide efficacy

- 4.3 Market Restraints

- 4.3.1 Stringent toxicological re-registration

- 4.3.2 Price compression from generic glyphosate and diquat oversupply

- 4.3.3 Preference for mechanical harvesting in recreation lakes

- 4.3.4 Activist litigation delaying permits

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Glyphosate

- 5.1.2 2,4-D

- 5.1.3 Imazamox

- 5.1.4 Imazapyr

- 5.1.5 Triclopyr

- 5.1.6 Diquat

- 5.2 By Mode of Action

- 5.2.1 Selective Herbicides

- 5.2.2 Non-Selective Herbicides

- 5.3 By Application Method

- 5.3.1 Foliar Application

- 5.3.2 Submersed Injection

- 5.4 By End-User Industry

- 5.4.1 Agricultural Water Bodies

- 5.4.2 Recreational Water Bodies

- 5.4.3 Fisheries and Aquaculture

- 5.5 By Formulation

- 5.5.1 Liquid Concentrates

- 5.5.2 Granular/Pelletized

- 5.5.3 Tablet/Compressed Briquettes

- 5.5.4 Water Soluble Concentrates

- 5.5.5 Emulsifiable Concentrates

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta AG

- 6.4.2 BASF SE

- 6.4.3 Corteva, Inc.

- 6.4.4 UPL Limited

- 6.4.5 Nufarm Limited

- 6.4.6 SePRO Corporation

- 6.4.7 Sumitomo Chemical Company, Limited (Valent USA)

- 6.4.8 Arxada AG

- 6.4.9 Nippon Soda Co., Ltd.

- 6.4.10 Alligare, LLC

- 6.4.11 Albaugh, LLC

- 6.4.12 FMC Corporation

- 6.4.13 Hangzhou Tianlong Biotechnology Co., Ltd.

- 6.4.14 Aquatic Technologies