|

시장보고서

상품코드

2061920

트레일러 보조 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Trailer Assist System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

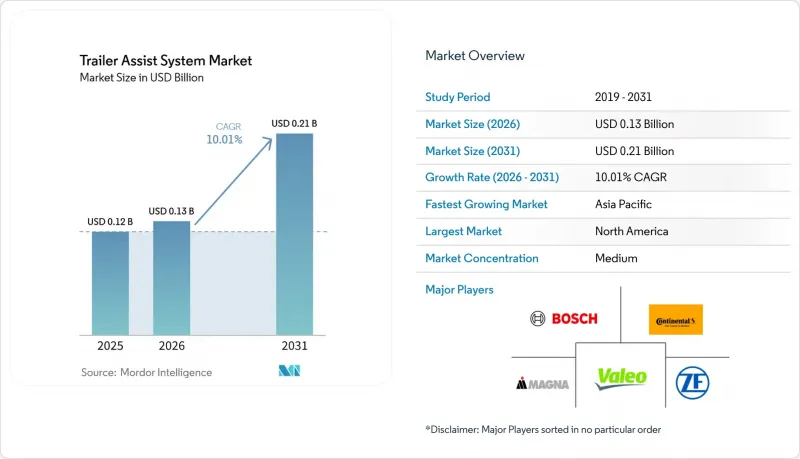

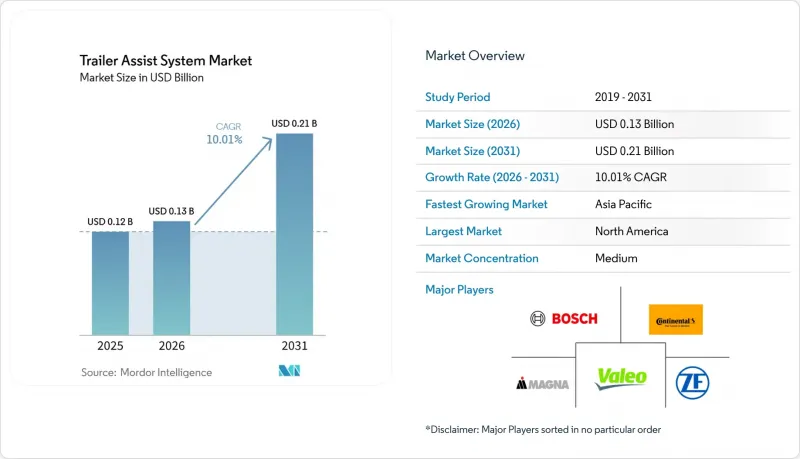

Mordor Intelligence에 의하면, 트레일러 보조 시스템 시장 규모는 2025년 1억 2,000만 달러로 평가되었습니다. 2026년 1억 3,000만 달러에서 2031년까지 2억 1,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 10.01%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소별(카메라 및 초음파 센서, 소프트웨어 모듈 및 알고리즘, ECU), 차량 유형별(승용차, 소형 상용차, 대형 상용차), 기술 수준별(준자율주행(SAE L1-L2), 고도 자율주행 및 완전 자율주행(SAE L3-L4)), 최종 시장(OEM 탑재 시스템, 애프터마켓용 개조), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 트레일러 보조 시스템 시장 동향 및 분석

트레일러 안전 기능 의무화를 위한 규제 움직임

각국 및 초국가적 기관들은 트레일러에 특화된 규정을 보다 광범위한 차량 자동화 체계에 통합하고 있으며, 자동차 제조업체들에게 카메라와 센서 군의 도입을 가속화할 것을 촉구하고 있습니다. UNECE의 GRVA(2025년 저속 주행에 관한 고성능 요건)는 트레일러의 후진 및 주차 시나리오를 암묵적으로 다루고 있습니다. 미국에서는 NHTSA가 2024년에 FMVSS 305a를 최종 확정하고, 소형 상용차용 자동 긴급 제동에 관한 규정 제정 절차를 시작했습니다. 이로 인해 서라운드 뷰 어레이를 사용하여 히치나 장애물을 감지할 수 있는 트럭이 간접적으로 우대받게 됩니다. 규정 준수 일정이 단축됨에 따라, 1차 공급업체들은 18-24개월 이내에 양산 가능한 하드웨어를 납품할 수밖에 없게 되었습니다. 또한, 새로운 규정에서는 최소 감지 범위와 오감지 허용 임계값을 규정함으로써 OEM 패키지와 애프터마켓 키트 간의 성능 격차를 줄이고 있습니다.

OEM을 통한 SAE 레벨 2-3 자동 주차 시스템으로의 전환

자동차 제조업체들은 첨단 자동 주차 시스템에 트레일러 보조 기능을 통합하는 움직임을 강화하고 있습니다. 유럽에서는 메르세데스-벤츠와 보쉬가 ‘지능형 파크 파일럿’을 발표하며, 지정된 주차장에서 작동하는 SAE 레벨 4 상용 주차 시스템의 첫 선을 보였습니다. Ford Otosan은 2024년에 트레일러 자동 주차 기술을 시연했습니다. RRT*(Rapidly-exploring Random Tree Star) 플래너와 모델 예측 제어를 통해 숙련된 운전자와 비교해 주차 효율을 대폭 향상시켰습니다. 한편, BMW의 ‘파킹 어시스턴트 프로페셔널’은 자주 이용하는 경로를 기억할 뿐만 아니라 스마트폰을 통한 조작도 가능하지만, 현행법상 운전자가 법적 책임을 지게 됩니다.

양산차의 시스템 비용 대폭 증가

트레일러 어시스트 패키지는 차량 가격을 크게 끌어올리기 때문에 보급형 트럭에는 도입이 제한되고 있습니다. 포드는 고객이 사후 장착할 수 있는 ‘트레일러 센서 키트’를 제공하고 있으며, GM은 ‘IntelliHaul 3.0’ 카메라 키트를 제공합니다. 이러한 비용에는 카메라 모듈, 하우징, 라이선스 비용이 포함되어 있으며, 공급업체는 자동 긴급 제동과 같은 주류 ADAS 기능에 비해 훨씬 적은 판매 대수로 이러한 비용을 상각해야 합니다. 예산을 중시하는 구매자들은 편의성보다 연비나 적재량을 우선시하는 경우가 많아, 그 결과 도입률은 저조한 수준에 머물고 있습니다.

부문별 분석

카메라와 초음파 센서는 2025년 매출의 47.15%를 차지하며, 히치 감지 및 장애물 회피에 필요한 정보를 제공하는 지각 계층의 기반을 이루었습니다. 그러나 소프트웨어 모듈 시장은 2031년까지 연평균 13.28%의 성장률을 나타낼 것으로 예상되며, 자체 개발 코드가 다음 가치의 물결을 주도하게 될 것입니다. 신경망 컨트롤러가 규칙 기반 알고리즘을 대체하여, 트레일러의 중량과 운전자의 운전 스타일을 학습하고 개입 방식을 최적화합니다. 2024년, 제너럴 모터스(General Motors)는 시각 정보만으로 히치의 각도를 추정하는 기술에 대한 특허를 취득했으며, 전용 요 센서가 더 이상 필요 없어짐에 따라 부품 명세서(BOM)를 간소화했습니다. 동시에, 전자 제어 장치(ECU)가 NVIDIA DRIVE와 같은 중앙 집중식 컴퓨팅 노드에 통합되는 추세가 강화됨에 따라, 개별 기능과 관련된 비용이 업계 전반에서 감소하고 있는 것으로 나타났습니다. 중국 제조업체들은 720p 무선 카메라를 경쟁력 있는 가격에 공급하기 시작하면서 하드웨어 마진에 압박을 가하고 있습니다. 구독형 무선 업데이트를 통해 멀티 트레일러 프로파일 및 예측 잭나이프 경고 등의 기능이 수익화되어, 소프트웨어의 이익률이 유지되고 있습니다. 하드웨어는 여전히 중요하지만(특히 알고리즘에 고대역폭 이미지나 레이더 입력을 제공하는 측면에서), 사용자 경험의 차별화와 지속적인 기능 향상을 주도하는 것은 소프트웨어입니다.

예측에 따르면, 트레일러 보조 시스템 시장에서 소프트웨어 분야의 성장률이 센서 분야를 상회할 것으로 전망됩니다. 이러한 급속한 성장은 주로 OEM(원청 브랜드 제조업체)이 차량 판매 후에도 기능을 수익화할 수 있게 해주는 무선 업데이트(OTA) 덕분입니다. 2024년 분석에서는 선형 2차 제어기의 효율성이 강조되었습니다. 이는 보다 복잡한 비선형 모델 예측 제어에 비해 계산 면에서 큰 이점이 있으며, 실시간 제어를 실현합니다. 이러한 효율성 덕분에, 비용 효율성을 중시하는 ECU에 도입할 수 있게 됩니다. 소프트웨어 계층이 히치 각도 인식을 위한 AI 추론 엔진을 통합함에 따라, 공급업체들은 전용 가속기를 탑재하여 신속한 응답 시간을 확보할 수 있는 체제를 갖추고 있습니다. 앞으로 알고리즘 라이선싱 및 데이터 분석을 통한 수익은 인식용 하드웨어에서 발생하는 수익을 넘어설 것으로 예측됩니다.

2025년에는 승용차가 매출의 67.04%를 차지했으며, 밀레니얼 세대가 여행용 트레일러나 보트를 견인할 수 있는 성능을 요구함에 따라 연평균 성장률(CAGR) 11.57%를 유지했습니다. Ford F-150, Chevrolet Silverado, RAM 1500 등의 모델은 트레일러용 후방 카메라, 노브식 조향 보조 장치, 스마트폰 앱을 제공하며, 브랜드 생태계를 통해 고객 충성도를 높이고 있습니다. 소형 상용차는 두 번째로 큰 시장 점유율을 차지하고 있으며, 작업 시간 단축으로 이어지는 연결 작업과 보험료 절감으로 이어지는 잭나이프 현상 방지를 원하는 도급업체들로부터 지지를 받고 있습니다. 대형 상용차는 현재 규모는 작지만, 자동화된 야드 작업을 통해 처리 능력이 향상되는 물류 센터에서 도입이 가속화되고 있습니다. 2028년 납품 계약이 체결된 Knorr-Bremse의 ‘ATLAS-L4’ 트럭은 2020년대 후반에 주류로 자리 잡을 조짐을 보이고 있습니다.

차량 함대의 표준화가 소형 상용차의 보급을 촉진하고 있습니다. 카메라 배치 방식이 통일되면 운전자 교육과 사고 원인 규명이 간소화되기 때문입니다. 레저 문화의 영향으로, 특히 북미에서는 승용차 대수가 여전히 주류를 이루고 있지만, 아시아태평양의 물류 현대화에 따라 상용차의 점유율은 상승할 것으로 보입니다. 대형 트럭용 트레일러 보조 시스템 시장 점유율은 지오펜싱이 적용된 물류 센터들이 근무 시간 단축 및 후진 시 사고 방지를 위해 레벨 4 야드 주행 기술을 신뢰하게 됨에 따라 급증할 것입니다. 전동 파워트레인은 견인으로 인한 주행 거리 손실을 상쇄하기 위해 소프트웨어를 통한 효율화가 필요하기 때문에 각 OEM 업체들의 동기 또한 일치하고 있습니다.

지역별 분석

북미는 레저 목적의 견인 문화가 뿌리 깊게 자리 잡고 있으며, 노브식 후진 시스템이 조기에 도입된 것을 배경으로 2025년 매출의 39.12%를 차지했습니다. 고급 트럭 시장의 고객층이 포화 상태에 가까워지고, 가격에 민감한 등급의 고객들이 1,000달러를 넘는 옵션 가격에 주저하고 있어 성장이 둔화되고 있습니다. 유럽은 2위를 차지했습니다. 이는 미리 정의된 구역 내에서 SAE 레벨 4의 발렛 파킹을 허용하는 규정 2022/1426과, 슈투트가르트에서 실증 실험을 가능하게 한 독일의 2021년 자율주행법에 근거한 것입니다. 아시아태평양은 중국과 인도의 차량 현대화, 물류 자동화, 그리고 ADAS 기능을 탑재한 대형 전기 트럭에 대한 정부의 인센티브에 힘입어 2031년까지 연평균 성장률(CAGR) 14.36%를 나타낼 것으로 전망됩니다.

인도에서는 2026년도 4월부터 12월까지 상용차 판매 대수가 75만 4,067대를 기록할 것으로 예상돼 전년 동기 대비 10% 증가할 것으로 전망됩니다. 또한, 견조한 GDP 성장에 힘입어 화물 수요도 확대되었습니다. 그러나 차량의 평균 사용 연수가 10년 이상에 달하기 때문에 특히 트레일러 보조 시스템이 통합된 트럭에 대한 뚜렷한 잠재 수요가 존재합니다. 한편, 중국에서는 2025년 상반기 판매 대수에서 전기 대형 트럭이 큰 비중을 차지했습니다. 구형 차량의 교체를 촉진하는 트레이드인 인센티브 덕분에, 2026년까지 이 수치는 크게 증가할 것으로 전망됩니다. 또한, 광범위한 배터리 교체소 네트워크가 구축되어 운전자의 주행 거리 걱정을 덜어주고 있습니다. 이에 따라, 특히 구내에서 차량을 운전할 때 에너지 절약을 위해 첨단 트레일러 후진 지원 시스템의 중요성이 점점 더 커지고 있습니다.

남미, 중동 및 아프리카는 레저 목적의 견인 수요가 제한적이며, 상용차 차량단 구매에 있어 비용 중시 경향이 강하기 때문에 여전히 시장은 초기 단계에 머물러 있습니다. 예측 기간 동안 정부의 안전 규제 강화와 카메라 가격 하락으로 인해 도입이 서서히 진행될 가능성은 있지만, 2031년까지는 전 세계 매출에서 차지하는 비중은 여전히 낮은 수준을 유지할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the trailer assist system market size is projected to expand from USD 0.12 billion in 2025 and USD 0.13 billion in 2026 to USD 0.21 billion by 2031, registering a CAGR of 10.01% between 2026 and 2031.

This report is Segmented by Component (Cameras and Ultrasonic Sensors, Software Modules and Algorithms, and ECU), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and HCV), Technology Level (Semi-Autonomous (SAE L1-L2), Highly and Fully Autonomous (SAE L3-L4)), End Market (OEM-Fitted Systems, Aftermarket Retrofits), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Trailer Assist System Market Trends and Insights

Regulatory Push for Mandatory Trailer Safety Features

National and supranational bodies are embedding trailer-specific rules into broader vehicle automation frameworks, compelling automakers to accelerate deployment of camera and sensor suites. UNECE's GRVA advanced performance text for low-speed maneuvers in 2025 implicitly covers trailer reversing and parking scenarios . In the United States, NHTSA finalized FMVSS 305a in 2024 and opened rulemaking on automatic emergency braking for light commercial vehicles, indirectly rewarding trucks that can detect hitches and obstacles using surround-view arrays. Compressed compliance timelines force Tier-1 suppliers to deliver production-ready hardware in 18-24 months. New rules also tighten performance parity between OEM packages and aftermarket kits by prescribing minimum detection ranges and false-positive thresholds.

OEM Move Toward SAE L2-L3 Automated Parking Suites

Automakers are increasingly integrating trailer-assist features into their advanced automated parking systems. In Europe, Mercedes-Benz and Bosch unveiled the Intelligent Park Pilot, marking the debut of an SAE Level 4 commercial parking system that operates in designated car parks. Ford Otosan demonstrated its autonomous trailer parking in 2024, significantly improving parking efficiency compared to seasoned drivers, thanks to RRT* (Rapidly-exploring Random Tree Star) planners and model-predictive control. Meanwhile, BMW's Parking Assistant Professional not only remembers frequent routes but also allows smartphone control, though drivers retain legal responsibility under existing laws.

High Incremental System Cost for Mass-Market Vehicles

Trailer-assist packages significantly increase vehicle prices, which limits their adoption in entry-level trucks. Ford offers its customer-installed Trailer Sensor Kit, while GM provides the IntelliHaul 3.0 camera kit. These costs reflect camera modules, housings, and licenses that suppliers amortize over far fewer units than mainstream ADAS features such as automatic emergency braking. Budget-conscious buyers frequently prioritize fuel efficiency or payload over convenience, resulting in subdued adoption rates.

Other drivers and restraints analyzed in the detailed report include:

- Rising Recreational Towing in North America and Europe

- Integration of Surround-View Cameras and Sensor Fusion

- Sensor Performance Limitations in Poor Weather

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cameras and ultrasonic sensors contributed 47.15% of 2025 revenue, anchoring the perception layer that feeds hitch detection and obstacle avoidance. Yet proprietary code will drive the next wave of value as software modules are forecast to compound at 13.28% through 2031. Neural-network controllers replace rule-based algorithms, learning trailer weight and driver style to refine interventions. In 2024, General Motors secured a patent for a vision-only hitch-angle estimator, streamlining its Bill of Materials (BOM) by eliminating the need for dedicated yaw sensors. At the same time, as Electronic Control Units (ECUs) increasingly integrate into centralized compute nodes like NVIDIA DRIVE, the industry witnesses a decline in costs associated with individual features. Chinese manufacturers have begun offering 720p wireless cameras at competitive prices, putting pressure on hardware profit margins. Through subscription-based over-the-air updates, features such as multi-trailer profiles and predictive jackknife warnings are now monetized, safeguarding software profit margins. While hardware remains crucial-especially with high-bandwidth imaging and radar inputs feeding algorithms-it's the software that drives differentiation in user experience and ongoing enhancements.

Forecasts indicate that the software segment of the trailer assist system market will outpace the sensor segment in growth. This surge is largely attributed to over-the-air updates, which empower Original Equipment Manufacturers (OEMs) to monetize features even after a vehicle's sale. A 2024 analysis highlighted the efficiency of linear quadratic regulators, achieving real-time control with significant computation advantages over the more complex nonlinear model predictive control. This efficiency enables deployment on budget-sensitive ECUs. As the software layer integrates AI inference engines for hitch-angle recognition, suppliers are poised to incorporate specialized accelerators, ensuring swift response times. Looking ahead, revenues from algorithm licensing and data analytics are set to eclipse those from perception hardware.

Passenger cars represented 67.04% of revenue in 2025, sustaining an 11.57% CAGR as millennials demand towing capability for travel trailers and boats. Models such as the Ford F-150, Chevrolet Silverado, and RAM 1500 offer trailer backup cameras, knob-based steering aids, and smartphone apps, creating stickiness through brand ecosystems. Light commercial vehicles make up the second-largest slice, favored by contractors seeking time-saving hookup routines and insurance-reducing jackknife prevention. Heavy commercial vehicles remain small today, yet accelerate adoption in distribution centers where automated yard handling improves throughput. Knorr-Bremse's ATLAS-L4 truck, under contract for 2028 delivery, signals mainstream adoption in the latter half of the decade .

Fleet standardization propels light commercial uptake: unified camera layouts simplify driver training and incident forensics. Recreational culture keeps passenger-car volumes dominant, especially in North America, but Asia-Pacific logistics modernization will lift the commercial share. The Trailer assist system market share for heavy trucks will jump as geofenced depots trust Level 4 yard maneuvers to cut labor hours and back-over incidents. OEM incentives align because electrified powertrains need software-enabled efficiency gains to offset towing-related range losses.

Geography Analysis

North America captured 39.12% of 2025 revenue, driven by a strong recreational towing culture and early adoption of knob-based backup systems. Growth moderates as premium truck customers near saturation and as price-sensitive trims balk at USD 1,000-plus option prices. Europe ranked second, aided by Regulation 2022/1426, which green-lights SAE Level 4 valet parking in predefined domains, and by Germany's 2021 driverless law, which enabled Stuttgart pilots. Asia-Pacific will post a 14.36% CAGR through 2031, driven by Chinese and Indian fleet modernization, logistics automation, and government incentives for electric heavy trucks that bundle ADAS features.

India recorded 754,067 commercial-vehicle sales during April-December FY2026, up 10% YoY, and freight demand expanded, coinciding with robust GDP growth. However, with an average fleet age stretching over a decade, there's a clear pent-up demand for trucks, especially those featuring integrated trailer assist systems. Meanwhile, in China, electric heavy trucks accounted for a significant share of sales in the first half of 2025. With a trade-in incentive encouraging the replacement of older vehicles, projections suggest this figure could increase substantially by 2026. Furthermore, expansive battery-swap corridors are alleviating range anxiety for drivers. This makes advanced trailer backing aids increasingly crucial, especially for conserving energy during yard maneuvers.

South America, the Middle East, and Africa remain early-stage markets because recreational towing is marginal and cost sensitivity dominates commercial fleet purchases. Over the forecast, government safety mandates and falling camera prices could spark incremental uptake, but contributions to global revenue stay small through 2031.

- Robert Bosch GmbH

- Continental AG

- Magna International

- ZF Friedrichshafen AG

- Valeo SA

- Denso Corporation

- Aptiv PLC

- Knorr-Bremse

- Westfalia-Automotive GmbH

- Haldex (SAF-Holland Group)

- Ford Motor Company

- Volkswagen AG

- Mercedes-Benz Group AG

- General Motors Company

- Toyota Motor Corporation

- Nissan Motor Co., Ltd.

- BMW AG

- Hyundai Motor Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Push for Mandatory Trailer Safety Features

- 4.2.2 OEM Move Toward SAE L2-L3 Automated Parking Suites

- 4.2.3 Rising Recreational Towing in North America and Europe

- 4.2.4 Integration of Surround-View Cameras and Sensor Fusion

- 4.2.5 Smart-Trailer Telematics Convergence

- 4.2.6 Electrified Trailer Hitch-Assist Demand

- 4.3 Market Restraints

- 4.3.1 High Incremental System Cost for Mass-Market Vehicles

- 4.3.2 Sensor Performance Limitations in Poor Weather

- 4.3.3 Liability Ambiguity for AI-Driven Trailer Collisions

- 4.3.4 Low Towing Culture in Emerging Economies

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Component

- 5.1.1 Cameras and Ultrasonic Sensors

- 5.1.2 Software Modules and Algorithms

- 5.1.3 Electronic Control Units (ECU)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCV)

- 5.2.3 Heavy Commercial Vehicles (HCV)

- 5.3 By Technology Level

- 5.3.1 Semi-Autonomous (SAE L1-L2)

- 5.3.2 Highly and Fully Autonomous (SAE L3-L4)

- 5.4 By End Market

- 5.4.1 OEM-Fitted Systems

- 5.4.2 Aftermarket Retrofits

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Poland

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Magna International

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Valeo SA

- 6.4.6 Denso Corporation

- 6.4.7 Aptiv PLC

- 6.4.8 Knorr-Bremse

- 6.4.9 Westfalia-Automotive GmbH

- 6.4.10 Haldex (SAF-Holland Group)

- 6.4.11 Ford Motor Company

- 6.4.12 Volkswagen AG

- 6.4.13 Mercedes-Benz Group AG

- 6.4.14 General Motors Company

- 6.4.15 Toyota Motor Corporation

- 6.4.16 Nissan Motor Co., Ltd.

- 6.4.17 BMW AG

- 6.4.18 Hyundai Motor Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment