|

시장보고서

상품코드

2061923

우주 쓰레기 모니터링 및 제거 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Space Debris Monitoring And Removal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

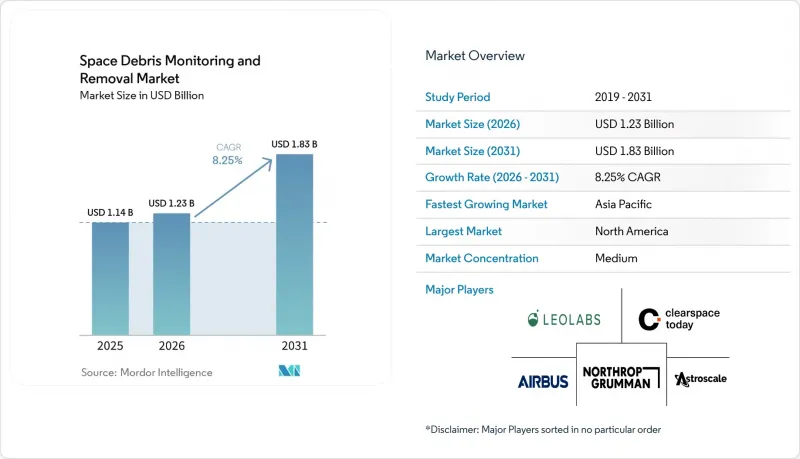

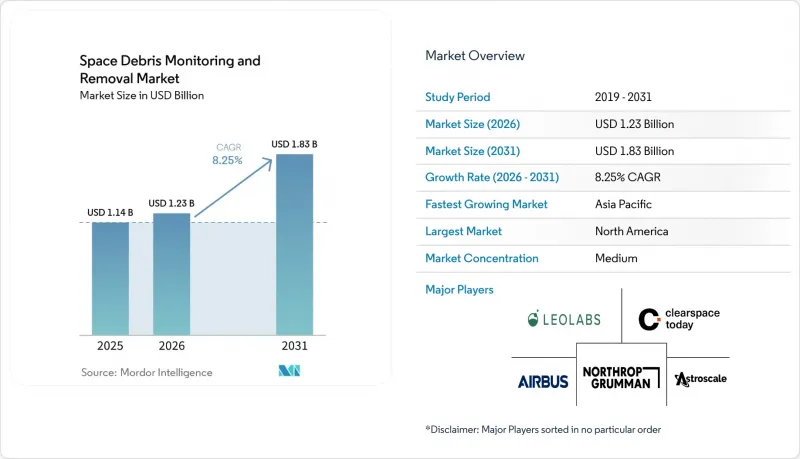

우주 쓰레기 모니터링 및 제거 시장 규모는 2025년에 11억 4,000만 달러로 평가되었고, 2026년 12억 3,000만 달러로 추정되고, 2031년까지 18억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 8.25%를 나타낼 전망입니다.

본 보고서는 궤도별(저궤도 등), 서비스 유형별(우주 쓰레기 모니터링 등), 제거 기술별(접촉식 등), 모니터링 기술별(지상 센서 등), 쓰레기 크기별(1mm-1cm 등), 최종 사용자별(정부 및 국방 등), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 우주 쓰레기 모니터링 및 제거 시장 동향과 인사이트

저궤도(LEO) 위성의 배치 확대

발사 활동이 대응 능력보다 빠르게 증가하고 있어, 우주 쓰레기 모니터링 및 제거 시장은 저지구 궤도(LEO)에서 더욱 큰 압박을 받고 있습니다. 2025년에는 4,434기의 위성이 궤도에 투입되었으며, 운용 중인 위성 수는 14,266기에 달했고, 이 중 미국이 3,529기의 상업용 페이로드를 차지했습니다. ESA의 2026년 우주 환경 평가 관련 보고서에서는 550km가 우주 쓰레기 밀도가 운용 중인 위성 밀도에 근접하고 있는 중요한 고도라고 지적되었으며, 저지구궤도(LEO)에서의 충돌 위험은 2024년 수준보다 20% 증가했습니다. 이러한 추세로 인해 우주 쓰레기 모니터링 및 제거 시장의 서비스 구매자 구성이 변화하고 있으며, 현재는 위성군 운영업체들이 근접 회피 분석 및 궤도 변경 지원에 대한 일일 수요의 대부분을 차지하고 있습니다. 또한, 민간 기업은 공공 기관보다 더 빈번하게 서비스를 구매하기 때문에 궤도 변경 건수가 늘어남에 따라 우주 쓰레기 모니터링 및 제거 시장에서 보다 안정적이고 지속적인 소프트웨어 수익을 창출할 수 있게 되었습니다.

우주 상황 인식(SSA) 이니셔티브에 대한 정부 지출 증가

정부 주도의 SSA(우주 상황 인식)에 대한 지출은 우주 쓰레기 모니터링 및 제거 시장에서 가장 확실한 수요 요인 중 하나로 자리 잡고 있습니다. LeoLabs는 2025년 계약 총액이 6,000만 달러를 넘어섰다고 보고했습니다. 이 회사에 따르면, 2025년 9월 우주상업국(Office of Space Commerce)과 미국 우주군(US Space Force)이 공동으로 발급한 라이선스에 힘입어, 미국 정부와의 계약 건수가 전년 대비 186% 증가했다고 합니다. 또한 2025년 3월, 이 회사는 2027년까지 인도-태평양 지역에 차세대 UHF 레이더를 배치하는 6,000만 달러 규모의 STRATFI 계약에 선정되었습니다. 프랑스는 2025년 10월, 오로르(Aurore) 레이더 프로젝트의 수행사로 탈레스(Thales)를 선정했습니다. 독일은 L-GUARD 프로그램의 일환으로 우주사령부용 Indra S3TSR 레이더 도입을 추진하고 있습니다. 이는 유럽 전역에서 주권적 감시 능력이 우선순위로 부상하고 있음을 보여주는 것으로, 각국 정부가 공유 공개 카탈로그에 대한 의존도를 줄이고 민간 업체와 협력하여 국내 감시 능력을 구축하려는 움직임 속에서 우주 쓰레기 모니터링 및 제거 시장의 고객 기반을 확대되고 있습니다.

우주 쓰레기의 능동적 제거에 관한 국제적으로 구속력 있는 법적 체계의 부재

우주 쓰레기 모니터링 및 제거 시장에 관한 법적 체계는 우주 물체가 쓰레기가 되어도 소유권이 소멸되지 않기 때문에 여전히 미비한 상태입니다. 현행 우주법상 관할권은 발사국에 귀속되며, 제3자에 의한 제거를 위해 물체를 유실로 선언하는 공식적인 절차는 존재하지 않습니다. 2025년 ESA 관련 조사에 따르면, 기술 전문가의 45%가 노후된 물체에 대한 인양 조항 추가를 지지했고, 50%는 ADR 보험의 의무화를 지지했으나, 정부 간 합의에는 이르지 못했습니다. 영국과 뉴질랜드는 2025년 5월, 공동 ADR 및 서비스 임무에 대한 책임 분담과 동의 절차를 명확히 하기 위해 구속력 없는 양자 간 모델을 제시했습니다. 보다 광범위한 합의 체제가 확립되기 전까지는 제거 사업자가 협력할 수 있는 대상이 제한적이기 때문에 우주 쓰레기 모니터링 및 제거 시장은 모니터링 서비스에 치우친 상태가 지속될 것입니다.

부문별 분석

2025년 기준으로 LEO(저궤도)는 우주 쓰레기 모니터링 및 제거 시장 점유율의 66.56%를 차지했습니다. 이는 가동 중인 위성의 대부분과 가장 밀집된 운용 중 우주 쓰레기 환경이 2,000km 미만의 고도에 존재하기 때문입니다. 이 궤도상의 우주 쓰레기 모니터링 및 제거 시장은 정부 자금으로 지원되는 SSA(우주 상황 인식) 프로그램과 충돌 회피 지원에 대한 상업적 수요 모두로부터 혜택을 받고 있습니다. 전 세계적으로 4만 개 이상의 천체가 목록화되어 있지만, ESA의 MASTER-8 모델에 따르면 10cm를 초과하는 천체가 약 5만 4,000개, 1cm에서 10cm 사이의 파편이 약 120만 개 존재하는 것으로 추정됩니다. 이러한 규모 때문에 접근 회피에 실패할 경우 운영상 영향이 즉각적으로 미치기 때문에 LEO는 감시 계약과 제거 임무 계획 모두에서 계속해서 핵심적인 위치를 차지하고 있습니다.

MEO는 2031년까지 연평균 성장률(CAGR)이 9.16%에 달할 전망이며, 가장 빠르게 성장하는 궤도 부문이 될 것으로 전망됩니다. 영국의 2025년 COPUOS 성명에서는 MEO 우주선 폐기에 관한 규정을 포함한 IADC의 최신 지침이 강조되었으며, 이는 우주 쓰레기 모니터링 및 제거 시장에 영향을 미칠 것입니다. MEO의 항법 및 시간 동기화 자산은 임무 가치가 높기 때문에 우주 쓰레기가 소량만 증가하더라도 규정 준수 관련 비용 증가를 초래할 가능성이 있습니다. GEO의 경우 궤도상의 물량은 여전히 적지만, 단일 서비스 임무로 고부가가치의 수명 연장 및 재배치 작업이 가능하기 때문에 경제성이 매력적입니다. D-Orbit사와 체결한 1억 1,960만 유로(1억 3,869만 달러) 규모의 계약은 탑재체나 궤도 슬롯의 가치가 충분히 높다면 사업자가 전문적인 서비스 역량에 자금을 투자할 의향이 있음을 보여줍니다. 그 결과, 우주 쓰레기 모니터링 및 제거 시장은 규모 면에서 LEO(저궤도)를 중심으로 하면서도, 임무의 경제성이 표적화된 개입을 정당화하는 MEO 및 GEO로 점차 확대될 것입니다.

2025년 서비스 유형별 수요에서 우주 쓰레기 감시는 58.87%를 차지했으며, 우주 쓰레기 모니터링 및 제거 시장에서 직접적인 제거 작업을 앞지르고 있습니다. 모니터링이 주도적인 위치를 차지하는 이유는 레이더 네트워크, 광학 센서, 카탈로그 서비스, 경보 플랫폼을 보다 신속하게 구축할 수 있고, 정기 구독 형태로 판매할 수 있기 때문입니다. 또한, 이를 통해 서비스 제공업체는 단일 발사, 제한된 대상 범위, 정부의 마일스톤 달성에 의존하는 경우가 많은 제거 임무에 비해 자본 위험을 낮게 유지할 수 있습니다. 따라서 우주 쓰레기 제거 산업의 모니터링 부문은 하드웨어 집약적인 제거 프로그램에 비해 판매 주기가 짧고, 업데이트 패턴도 안정적이라는 장점이 있습니다. 규제 의무가 강화되는 가운데, 미션 재설계 없이 규정 준수 지원이 필요한 사업자들에게 있어 모니터링 서비스는 여전히 가장 먼저 선택하는 기본 솔루션으로 자리 잡고 있습니다.

우주 쓰레기 제거는 여전히 가장 빠르게 성장하는 서비스 분야이며, 제거 서비스를 포함한 우주 쓰레기 모니터링 및 제거 시장 규모는 2031년까지 연평균 성장률(CAGR) 9.91%로 확대될 것으로 전망됩니다. 이러한 변화는 파이프라인이 드디어 기술 실증 단계에서 선정된 임무의 운용 및 조달 단계로 전환되고 있음을 반영합니다. 아스트로스케일의 ADRAS-J는 293일간의 근접 운용을 마치고, 2026년 3월에 궤도 이탈을 시작했습니다. 이를 통해 비협조적 우주 쓰레기의 검사 및 접근과 관련하여, 검증된 상업적 기준이 업계에 제공되었습니다. 또한 랑데부, 근접 운용, 도킹과 같은 기술이 동일한 플랫폼에서 우주 쓰레기 포획, 수명 연장, 이송, 검사를 지원할 수 있기 때문에 우주 쓰레기 모니터링 및 제거 시장에서는 제거와 정비의 경계가 점차 모호해지고 있습니다. 이러한 중복을 통해 제공업체는 개발 비용을 여러 수익원으로 분산할 수 있습니다. 또한, 기업이 단일하고 제한적인 이용 사례만을 염두에 두고 우주선을 제조할 때 발생하는 위험도 줄어듭니다. 시간이 지남에 따라 운영업체들이 감시, 임무 계획, 개입 능력을 결합한 패키지를 구매하게 됨에 따라, 우주 쓰레기 모니터링 및 제거 시장의 서비스 조합은 이분법적인 구조에서 벗어나게 될 가능성이 있습니다.

지역별 분석

2025년, 북미는 우주 쓰레기 모니터링 및 제거 시장 점유율의 38.87%를 차지했으며, 이는 미국 우주군, NASA 및 우주상업국의 시너지 효과를 반영한 것입니다. 이 지역이 주도적인 입지를 차지하고 있는 이유는 정책, 공공 자금, 그리고 상업용 위성 군집의 규모가 다른 시장에서는 유례를 찾아볼 수 없을 정도로 긴밀하게 연계되어 있기 때문입니다. 또한 NorthStar Earth and Space사는 2026년 4월, 우주 기반 SSA(우주 상황 인식) 위성군'‘Skylark'의 확장 자금을 조달하기 위해 3억 달러 규모의 SPAC(특수목적인수회사)과의 합병을 발표했습니다. 또한 Turion Space사도 2026년 4월에 7,500만 달러 이상을 조달하고, 우주선 생산 능력을 연간 40대로 확대함으로써 이 지역의 성장세에 박차를 가하고 있습니다. 이는 자본이 더 이상 개념 개발에만 그치지 않고, 운용 함대의 확장을 뒷받침하고 있음을 보여줍니다.

유럽은 우주 쓰레기 모니터링 및 제거 시장에서 규제가 가장 활발한 지역입니다. 이는 ESA의 프로그램, EU의 규정, 그리고 각국의 국방상 우선순위가 같은 방향으로 나아가고 있기 때문입니다. '제로 데브리 헌장'은 2025년까지 19개국, 150개 이상의 서명을 확보했으며, 이는 우주 쓰레기를 발생시키지 않는 운용 관행에 대한 합의가 확대되고 있음을 보여줍니다. ClearSpace와 ESA는 2026년 1월, 상업용 궤도 서비스의 첫걸음으로 'PRELUDE' 임무를 발표했습니다. 한편, ClearSpace-1은 당초 목표가 변경되었음에도 불구하고 2029년 발사 일정을 유지하고 있습니다. 프랑스의 'Aurore' 레이더 계획이나 독일의 'L-GUARD' 프로젝트 역시 국가 주권에 기반한 감시 인프라가 병행하여 지속적으로 확대되고 있다는 점에서 유럽이 규제에만 의존하고 있지 않음을 보여주고 있습니다.

아시아태평양은 우주 쓰레기 모니터링 및 제거 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR)이 12.11%를 나타낼 것으로 전망됩니다. 2025년에 예정된 중국의 92회 궤도 투입은 지역 내 모니터링 수요에 추가적인 부담을 주고 있으며, 서태평양 전역에서 SSA(우주 상황 인식)에 대한 투자 확대를 촉진하고 있습니다. 남미, 중동 및 아프리카에서는 현재 수요가 여전히 소규모에 그치고 있습니다. 그럼에도 불구하고, UAE와 브라질의 제도적 참여는 상업 활동이 여전히 제한적인 지역에서도 우주 쓰레기 모니터링 및 제거 시장의 지역적 범위가 확대되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the space debris monitoring and removal market size was valued at USD 1.14 billion in 2025 and estimated to grow from USD 1.23 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 8.25% during the forecast period.

This report is Segmented by Orbit (Low Earth Orbit, and More), Service Type (Space Debris Monitoring, and More), Removal Technique (Contact, and More), Monitoring Technology (Ground-Based Sensors, and More), Debris Size (1 Mm To 1 Cm, and More), End User (Government and Defense, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Space Debris Monitoring And Removal Market Trends and Insights

Expansion of Low Earth Orbit (LEO) Satellite Deployments

The space debris monitoring and removal market is under stronger pressure in LEO because launch activity is rising faster than mitigation capacity. In 2025, 4,434 satellites entered orbit, and the active satellite population reached 14,266, with the US accounting for 3,529 commercially procured payloads. Reporting tied to ESA's 2026 space environment assessment identified 550 km as a critical altitude at which debris object density is nearing active satellite density, and collision risk in LEO rose by 20% from 2024 levels. That pattern is changing who buys services in the space debris monitoring and removal market, as constellation operators now generate much of the day-to-day demand for conjunction analysis and maneuver support. Commercial operators also buy more frequently than public agencies, so the space debris monitoring and removal market gains steadier recurring software revenue as maneuver volumes increase.

Increasing Government Spending on Space Situational Awareness (SSA) Initiatives

Government-backed SSA spending remains one of the clearest demand anchors for the space debris monitoring and removal market. LeoLabs reported more than USD 60 million in total contract awards in 2025. They said its US government contracts grew 186% year over year, supported by a September 2025 joint license involving the Office of Space Commerce and the US Space Force. In March 2025, the company was also selected for a USD 60 million STRATFI award to deploy next-generation UHF radar in the Indo-Pacific by 2027. France selected Thales for the Aurore radar program in October 2025. Germany moved ahead with the Indra S3TSR radar for its space command under the L-GUARD program, which shows that sovereign monitoring capacity is becoming a priority across Europe, expanding the customer base for the space debris monitoring and removal market, as governments seek to reduce reliance on shared public catalogs and build domestic monitoring capabilities in partnership with commercial providers.

Lack of Internationally Binding Legal Framework for Active Debris Removal

The legal framework for the space debris monitoring and removal market remains incomplete because ownership of space objects does not lapse when they become debris. Current space law leaves jurisdiction with the launching state, and there is no formal mechanism to declare an object abandoned for third-party removal. A 2025 ESA-linked survey found that 45% of technical experts supported adding a salvage clause for older objects and 50% supported mandatory ADR insurance, but no intergovernmental consensus followed. The UK and New Zealand presented a non-binding bilateral model in May 2025 to clarify liability sharing and consent procedures for joint ADR and servicing missions. Until broader consent frameworks emerge, the space debris monitoring and removal market will remain tilted toward monitoring services, as removal providers can pursue only a limited set of cooperative targets.

Other drivers and restraints analyzed in the detailed report include:

- Stricter International Regulations for Post-Mission Satellite Disposal

- Growing Adoption of In-Orbit Servicing and Satellite Recycling Models

- High Capital Investment and Uncertain Return on Investment for Debris Removal Missions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LEO held 66.56% of the space debris monitoring and removal market share in 2025 because most active satellites and the densest operational debris environment sit below 2,000 km. The space debris monitoring and removal market in this orbit benefits from both government-funded SSA programs and commercial demand for collision avoidance support. More than 40,000 objects are cataloged globally, while ESA's MASTER-8 model estimated around 54,000 objects larger than 10 cm and nearly 1.2 million fragments in the 1 cm to 10 cm range. That volume keeps LEO at the center of both monitoring contracts and removal mission planning because the operational consequences of a missed conjunction are immediate.

MEO will be the fastest-growing orbit segment with a CAGR of 9.16% through 2031. The UK's 2025 COPUOS statement highlighted updated IADC guidance that includes disposal provisions for MEO spacecraft, affecting the space debris monitoring and removal market. Navigation and timing assets in MEO carry high mission value, so even limited debris growth can trigger higher compliance spending. GEO remains smaller in volume, but the economics are attractive because single-servicing missions can support high-value life-extension or relocation work. D-Orbit's EUR 119.6 million (USD 138.69 million) contract shows that operators will fund specialized servicing capability when the payload and orbital slot values are high enough. The result is a space debris monitoring and removal market that stays centered on LEO by volume while slowly broadening into MEO and GEO, where mission economics justify targeted intervention.

Space debris monitoring accounted for 58.87% of the 2025 service type demand, keeping it ahead of direct removal work in the space debris monitoring and removal market. Monitoring leads because radar networks, optical sensors, catalog services, and alert platforms can be deployed more quickly and sold as recurring subscriptions. That also gives providers lower capital exposure than removal missions, which often depend on a single launch, a narrow target set, and government-backed milestones. The monitoring side of the space debris removal industry, therefore, benefits from shorter sales cycles and steadier renewal patterns than hardware-intensive removal programs. As regulatory obligations tighten, monitoring remains the default first purchase for operators that need compliance support without taking on mission redesign.

Space debris removal is still the fastest-growing service category, with the space debris monitoring and removal market size for removal services projected to expand at a 9.91% CAGR through 2031. The shift reflects a pipeline that is finally moving from technology demonstration toward operational procurement in selected missions. Astroscale's ADRAS-J completed 293 days of proximity operations and began deorbit in March 2026, providing the sector with a validated commercial benchmark for inspection and close approach of non-cooperative debris. The space debris monitoring and removal market is also blurring the line between removal and servicing because rendezvous, proximity operations, and docking can support debris capture, life extension, relocation, and inspection from the same platform. That overlap helps providers spread development costs across several revenue streams. It also reduces the risk that a company builds a spacecraft for only one narrow use case. Over time, the service mix in the space debris monitoring and removal market is likely to become less binary as operators buy packages that combine monitoring, mission planning, and intervention capability.

Geography Analysis

North America held 38.87% of the space debris monitoring and removal market share in 2025, which reflects the combined pull of the US Space Force, NASA, and the Office of Space Commerce. The region leads because policy, public funding, and the scale of the commercial constellation are aligned in ways few other markets can match. NorthStar Earth and Space also announced a USD 300 million SPAC merger in April 2026 to fund the expansion of its Skylark space-based SSA constellation. Turion Space added to that regional momentum by raising more than USD 75 million in April 2026 to scale spacecraft output to 40 vehicles a year, which shows that capital is now backing operational fleet growth rather than only concept development.

Europe is the most regulation-active region in the space debris monitoring and removal market because ESA programs, EU rules, and national defense priorities are moving in the same direction. The Zero Debris Charter reached more than 150 signatories across 19 countries by 2025, which shows growing alignment around debris-neutral operating practices. ClearSpace and ESA announced the PRELUDE mission in January 2026 as a step toward commercial in-orbit services, while ClearSpace-1 remained scheduled for a 2029 launch after its earlier target change. France's Aurore radar program and Germany's L-GUARD effort also show that Europe is not relying solely on regulation, as sovereign surveillance infrastructure continues to expand in parallel.

Asia-Pacific is the fastest-growing region in the space debris monitoring and removal market, with a 12.11% CAGR projected through 2031. China's 92 orbital launches in 2025 are adding pressure on regional monitoring needs, encouraging wider SSA investment across the western Pacific. South America, the Middle East, and Africa remain smaller in current demand. Still, institutional engagement from the UAE and Brazil shows that the regional footprint of the space debris monitoring and removal market is broadening, even where commercial activity remains limited.

- Astroscale Holdings Inc.

- ClearSpace

- Northrop Grumman Corporation

- LeoLabs, Inc.

- Lockheed Martin Corporation

- NorthStar Earth & Space Inc.

- Airbus SE

- OHB SE

- SKY Perfect JSAT Group

- ExoAnalytic Solutions, Inc.

- D-Orbit S.p.A.

- Kayhan Space Corp.

- Neuraspace Lda.

- Kall Morris Inc.

- Turion Space Corp.

- The Boeing Company

- Surrey Satellite Technology Limited

- Plextek Services Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of LEO satellite deployments

- 4.2.2 Increasing government spending on Space Situational Awareness (SSA) initiatives

- 4.2.3 Stricter international regulations for post-mission satellite disposal

- 4.2.4 Rising influence of orbital debris risk on space insurance premiums

- 4.2.5 Growing adoption of in-orbit servicing and satellite recycling models

- 4.2.6 Advancements in high-precision tracking technologies for small-scale debris

- 4.3 Market Restraints

- 4.3.1 Lack of internationally binding legal framework for Active Debris Removal (ADR)

- 4.3.2 High capital investment and uncertain return on investment for debris removal missions

- 4.3.3 Export control and regulatory barriers on dual-use space surveillance technologies

- 4.3.4 Skilled workforce shortages in orbital mechanics and space robotics fields

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Orbit

- 5.1.1 Low Earth Orbit (LEO)

- 5.1.2 Medium Earth Orbit (MEO)

- 5.1.3 Geostationary Orbit (GEO)

- 5.2 By Service Type

- 5.2.1 Space Debris Monitoring

- 5.2.2 Space Debris Removal

- 5.3 By Removal Technique

- 5.3.1 Contact

- 5.3.2 Contactless

- 5.4 By Monitoring Technology

- 5.4.1 Ground-based Sensors

- 5.4.2 Space-based Sensors

- 5.4.3 Analytics and Collision-avoidance Software

- 5.5 By Debris Size

- 5.5.1 1 mm to Less than 1 cm

- 5.5.2 1 cm to Less than 10 cm

- 5.5.3 More than 10 cm

- 5.6 By End User

- 5.6.1 Government and Defense

- 5.6.2 Commercial Satellite Operators

- 5.6.3 Academic and Research Organizations

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 France

- 5.7.2.3 Germany

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Astroscale Holdings Inc.

- 6.4.2 ClearSpace

- 6.4.3 Northrop Grumman Corporation

- 6.4.4 LeoLabs, Inc.

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 NorthStar Earth & Space Inc.

- 6.4.7 Airbus SE

- 6.4.8 OHB SE

- 6.4.9 SKY Perfect JSAT Group

- 6.4.10 ExoAnalytic Solutions, Inc.

- 6.4.11 D-Orbit S.p.A.

- 6.4.12 Kayhan Space Corp.

- 6.4.13 Neuraspace Lda.

- 6.4.14 Kall Morris Inc.

- 6.4.15 Turion Space Corp.

- 6.4.16 The Boeing Company

- 6.4.17 Surrey Satellite Technology Limited

- 6.4.18 Plextek Services Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment