|

시장보고서

상품코드

2061926

한외여과 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Ultrafiltration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

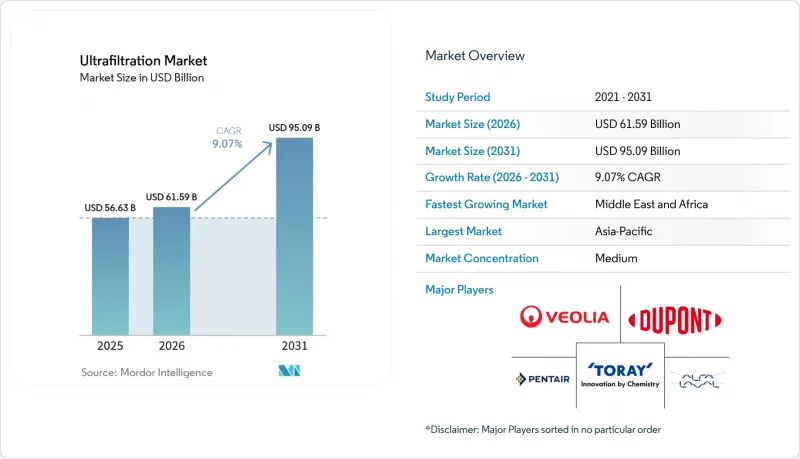

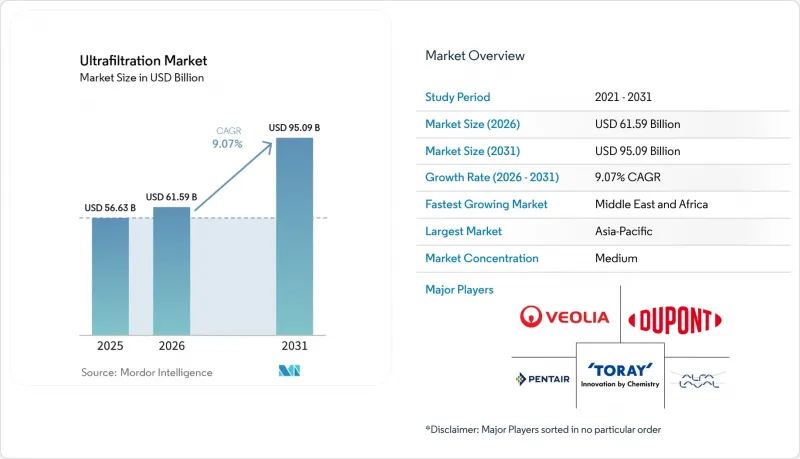

Mordor Intelligence에 의하면, 한외여과 시장 규모는 2025년 566억 3,000만 달러로 평가되었습니다. 2026년에는 615억 9,000만 달러로 확대되어 2026-2031년 CAGR은 9.07%를 나타내, 2031년에는 950억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 막의 유형(폴리머, 세라믹 등), 모듈 유형(중공사, 나선형 권선 등), 용도(상하수도 처리, 마이크로전자공학 등), 최종 사용자 산업(지자체, 산업용 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 한외여과 시장 동향 및 인사이트

상하수도 처리 수요 증가

물 부족이라는 과제에 직면한 상수도 유틸리티자들은 기존의 모래 여과 방식에서 벗어나, 대신 첨단 막 정화 기술을 도입하고 있습니다. 이러한 전환을 통해 엄격한 탁도 기준을 준수할 수 있을 뿐만 아니라, 저수지와 관련된 막대한 비용을 절감할 수도 있게 됩니다. 중국에서는 이우 제3정수장이 선구적인 노력을 기울이고 있으며, 대규모 수처리에 세라믹 모듈을 활용하고 있습니다. 해당 시설의 조사 결과에 따르면, 오염으로 인한 가동 중단 시간을 고려하더라도 세라믹 시스템은 폴리머 시스템과 경제적으로 동등한 수준인 것으로 나타났습니다. 한편, 칭다오 동가구에서는 다른 시설이 한외여과와 역삼투를 결합함으로써 유지보수의 필요성을 줄이고 운영 비용의 효율화를 실현하고 있습니다. 중동에서도 진전이 나타나고 있으며, 향후 몇 년 동안 해수 담수화 능력을 확대할 계획입니다. 흥미롭게도, 이러한 입찰 안건 중 상당수는 한외여과를 통한 전처리를 중시하는 경향을 보이고 있습니다. 이러한 한외여과의 동향은 해수 담수화에 그치지 않고, 산업용 재이용 분야에서도 그 기세를 더해가고 있습니다. 예를 들어, 브라질 Veolia의 비토리아 공장에서 주요 철강 제조업체에 공정용수를 공급하고 있습니다. 이 성과는 해당 플랜트의 운영 효율이 높음을 보여줄 뿐만 아니라, 이미 가뭄 문제에 직면해 있는 지역에서 담수 소비량이 현저히 감소했음을 의미합니다.

역삼투 및 해수 담수화의 전처리로 한외여과 통합

현재, 해수 담수화 플랜트에서는 듀얼 멤브레인 트레인이 표준으로 채택되어 있습니다. 이는 역삼투막의 보증 조건에 따라, 여과 전처리수에 한외여과가 필수로 규정되어 있기 때문입니다. Toray의 2025년형 고제거율 중공사막은 후공정에서의 오염을 3분의 1로 줄이고, 화학 세정을 통한 이산화탄소 배출량을 30% 감축합니다. 듀폰의 2026년형 초고압 필터 카트리지는 배수량을 최소화하는 것을 목표로 하며, 돌이킬 수 없는 막힘을 방지하기 위해 한외여과 방식을 채택하고 있습니다. 바레인의 시트라(Sitra) 및 히드(Hidd)에서 진행 중인 20억 달러 규모의 확장 프로젝트에서는 탁도를 0.1 네페로메트릭 탁도 단위 미만으로, 실트 밀도 지수를 3.0 미만으로 제한하고 있으며, 본격적인 가동 개시 전에 한외여과가 확실히 도입되도록 하고 있습니다. 에너지 모델링에 따르면, 0.5-2 바의 한외여과를 도입함으로써 역삼투의 유량이 10-15% 향상되는 것으로 밝혀졌습니다. 이러한 성능 향상으로 인해 필터의 수명을 최대 2년까지 연장할 수 있으며, 순현재가치(NPV)를 기준으로 한 투자 회수가 기대됩니다. 그 효과성을 뒷받침하듯, 업계 단체들은 이러한 설계를 모범 사례 매뉴얼에 반영하고 있어, 전 세계적으로 빠르게 보급될 수 있는 길이 열리고 있습니다.

막의 오염 및 세척 비용

높은 탁도나 고농도의 용존 유기물로 인해 어려움을 겪고 있는 지표수 처리 시설은 오염 현상으로 인해 막대한 경제적 부담을 안고 있습니다. 표백제, 산, 계면활성제를 사용한 정기적인 처리는 고분자 섬유를 산화시켜, 그 결과 유효 수명을 단축시킵니다. 세라믹 모듈은 가혹한 세척 조건에도 견딜 수 있지만, 가격이 비싸기 때문에 고급 시장에 한정되어 있습니다. 단계적 투과성을 자랑하는 Pall사의 ‘Gradient Permeability Integrated Cartridge’ 설계는 유제품 분야 시험에서 세척 빈도를 현저히 줄였으나, 이제야 비로소 광범위한 시장에 진출하기 시작한 단계입니다. 산화 그래핀 코팅에 대한 연구는 실험실 규모의 급수 시스템에서 투과율 저하를 억제할 가능성이 있음을 시사하고 있으나, 적절한 파일럿 데이터가 부족하여 실용화가 지체되고 있습니다. 중동에서는 유기물 부하를 줄이기 위해 자외선을 이용한 예비 산화나 용존 공기 부상법 실험이 진행되고 있지만, 이는 설비 투자의 복잡화를 수반합니다.

부문별 분석

2025년에는 폴리머 막이 비용 면에서의 우위를 바탕으로 매출의 67.20%를 차지했습니다. 그러나 세라믹 대체품은 경쟁사들을 앞지르는 기세로 성장하고 있으며, 2026년부터 2031년까지의 한외여과 시장에서 연평균 성장률(CAGR) 10.56%를 나타낼 것으로 전망됩니다. 중공사 폴리머 유닛은 지방자치단체의 표준 감가상각 일정에 맞추어 전략적으로 가격이 책정되어 있습니다. 한편, 식품 및 제약 가공업체들은 더 고가의 세라믹 유닛을 선택하고 있습니다. 이러한 선택은 세라믹이 지닌 뛰어난 내열성 및 내화학성에 기인하며, 그로 인해 수명이 현저히 연장됩니다. Pall의 신제품인 GP-IC 세라믹은 기존에 제기되었던 수율 저하 우려를 해소했으며, 현재는 유단백질 회수율이 매우 높다는 장점을 자랑하고 있습니다. 또한, 중국 이우 공장의 사례에서 볼 수 있듯이, 오염으로 인한 가동 중단에 따른 장기적인 비용을 고려하면 세라믹은 폴리머 소재 옵션의 경제성과 경쟁할 수 있습니다.

금속계 및 기타 무기막은 시장 점유율이 제한적이지만, 주로 반도체용 초순수 루프에 활용되고 있습니다. 이 전문 분야에서 미세 입자를 제거하는 능력은 칩의 수율을 현저히 향상시킬 수 있습니다. Asahi Kasei의 OAT 시리즈는 특정 제조 공정 노드로 제한되지만, 이러한 엄격한 기준을 충족하도록 설계되었습니다. 동시에, 유럽에서 퍼플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질에 대한 감시가 강화됨에 따라, 업계의 관심은 이러한 화합물을 포함하지 않는 세라믹으로 쏠리고 있습니다. 이러한 변화를 상징하듯, 모듈당 표면적을 확대한 나노스톤(Nanostone)사의 ‘세라믹 한외여과 흐름(Ceramic Ultrafiltration Flow)’은 특히 엄격한 규정 준수 요건을 부과받는 유틸리티자들 사이에서 세라믹 제품으로의 조달 경향을 이끌고 있습니다.

2025년에는 중공사 모듈이 시장을 장악하며 도입 점유율의 51.45%를 차지했습니다. 이 모듈들은 1입방미터당 최대 1,200제곱미터의 막을 충전할 수 있는 능력을 자랑하며, 아웃사이드-인 유동을 통해 고형물을 효과적으로 처리했습니다. 한편, 나선형 권선 구조는 역삼투에서 한외여과로 전환되어 식품 및 제약 분야의 위생 요건을 충족시켰습니다. 특히 주목할 만한 것은 Alfa Laval의 ‘DuroLac’ 스파이럴 모듈로, 혁신적인 외피 형상 개선을 통해 투과 유량을 15% 향상시켰습니다. 관형 모듈은 전단력을 통해 부착물을 제거할 수 있는 특성 덕분에 양조장이나 고형분 함량이 높은 도시 하수 처리 시설의 개보수 공사에서 선호되고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 10.24%를 나타낼 것으로 전망됩니다. 이 기술의 우수성을 입증하는 사례로, 중국 이우에서는 초속 3미터의 횡류 유속을 달성하여 조류를 효과적으로 방제하는 세라믹 관형 모듈의 도입 사례가 소개되었습니다. 일회용 생명공학 분야에서는 플레이트 앤 프레임형 캡슐이 빠르게 보급되고 있습니다. 예를 들어, 머크(Merck)의 코크 공장에서는 세척 검증 절차를 생략할 뿐만 아니라 배치 전환 시간을 단축시켜 주는 ‘펠리콘(Pellicon)’ 장치를 제조하고 있습니다.

지역별 분석

2025년, 아시아·태평양 지역은 전 세계 매출의 38.31%를 차지했습니다. 이는 중국의 해수 담수화 사업, 싱가포르의 NEWater(재생수) 사업 확대, 그리고 인도의 백신 생산이 주도한 결과입니다. 특히, 칭다오 동가구에서 실시된 한외여과 전처리 공정은 에너지 효율의 새로운 기준을 제시했습니다. 싱가포르의 예측 세척 기술은 놀라운 에너지 절감 효과를 가져오고 있으며, 데이터 기반 운영의 위력을 입증하고 있습니다. 또한, 하이데라바드와 벵갈루루의 제약 거점에서는 수입된 일회용 카세트의 도입이 증가하고 있으며, 이는 국내 공급업체에게 시장 기회를 시사하고 있습니다.

2026년부터 2031년에 걸쳐 중동 및 아프리카는 연평균 성장률(CAGR) 10.74%라는 견조한 성장세를 보이며 시장을 주도할 것으로 전망됩니다. 사우디아라비아 국립수자원공사는 카심 주에서 대규모 사업을 주도하고 있으며, 바레인도 시트라 및 히드 프로젝트에 막대한 투자를 하고 있습니다. 특히, 해당 지역에서 최근 진행된 많은 해수 담수화 입찰에서 한외여과 방식이 채택되면서, 물 안보 측면에서 이 방식이 수행하는 중요한 역할이 부각되고 있습니다. 남아프리카에서는 지방 자치 단체가 가뭄 문제를 해결하기 위한 비용 효율적인 해결책으로 컨테이너형 스키드의 도입을 검토하고 있습니다.

유럽과 북미는 전 세계 매출에서 큰 비중을 차지하고 있지만, 그 성장은 기존 설비의 개보수 및 교체에 중점을 두고 있어 제한되고 있습니다. 유럽연합(EU)의 도시 하수 지침에서는 영양염류와 미세 플라스틱의 제거가 중시되고 있습니다. 또한, 2026년까지 새로운 퍼플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질(PFAS)에 대한 규제 기준이 도입될 예정인 만큼, 막 기술의 발전이 급속도로 가속화되고 있습니다. 알파 라발의 살프스보르그 공장은 2027년까지 이러한 규제 기준을 충족할 전망입니다. 북미에서는 설비 투자 사이클이 둔화되고 있음에도 불구하고, 바이오프로세스 확장에 힘입어 안정적인 수요가 나타나고 있습니다. 그 대표적인 예가 조지아주에 위치한 Meissner의 신공장으로, 이 공장은 일회용 시스템 생산뿐만 아니라 많은 일자리를 창출하고 있습니다. 한편, 남미에서는 시장 점유율이 낮긴 하지만, 브라질 베올리아(Veolia)의 비토리아 시설은 해당 지역에서 산업용수의 재사용 가능성을 여실히 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the ultrafiltration market size is expected to grow from USD 56.63 billion in 2025 to USD 61.59 billion in 2026 and is forecast to reach USD 95.09 billion by 2031 at 9.07% CAGR over 2026-2031.

This report is Segmented by Membrane Type (Polymeric, Ceramic, and More), Module Type (Hollow Fiber, Spiral Wound, and More), Application (Water and Wastewater Treatment, Micro-Electronics and More), End-User Industry (Municipal, Industrial, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Ultrafiltration Market Trends and Insights

Growing Demand for Water and Wastewater Treatment

Utilities, facing challenges of water scarcity, are moving away from traditional sand filtration methods, opting instead for advanced membrane clarification. This transition not only enables them to adhere to strict turbidity standards but also sidesteps the significant expenses tied to reservoirs. In China, the Yiwu Third Water Plant is at the forefront, utilizing ceramic modules for extensive water processing. Their research indicates that, even accounting for fouling downtimes, ceramic systems are economically comparable to polymeric systems. Meanwhile, in Qingdao Dongjiakou, another facility is combining ultrafiltration with reverse osmosis, resulting in reduced maintenance needs and improved operational cost efficiency. The Middle-East is also advancing, with plans to expand desalination capacities in the coming years. Interestingly, a large portion of these tenders is leaning toward ultrafiltration pretreatment. This trend of ultrafiltration isn't confined to desalination; it's gaining traction in industrial reuse too. For example, Veolia's Vitoria station in Brazil is supplying process water to major steel manufacturers. This achievement not only emphasizes the station's operational efficiency but also signifies a marked decrease in freshwater consumption for a region already grappling with drought challenges.

Integration of Ultrafiltration as Pretreatment for Reverse Osmosis and Desalination

Seawater plants now standardize dual-membrane trains, as reverse-osmosis warranties mandate ultrafiltration feedwater. Toray's 2025 high-removal hollow fiber cuts downstream fouling by a third and reduces carbon output from chemical cleaning by 30%. DuPont's 2026 ultra-high-pressure element, aiming for minimal liquid discharge, depends on ultrafiltration to avert irreversible compaction. Bahrain's USD 2 billion expansions at Sitra and Hidd set turbidity limits under 0.1 nephelometric turbidity units and a silt density index below 3.0, ensuring ultrafiltration is in place before major operations commence. Energy modeling reveals that implementing 0.5-2 bar ultrafiltration boosts reverse-osmosis flux by 10%-15%. This enhancement can prolong the lifespan of the elements by as much as two years, leading to a favorable net-present-value payback. As a testament to its efficacy, industry associations have incorporated these designs into their best-practice manuals, paving the way for a swift global adoption.

Membrane Fouling and Cleaning Costs

Surface-water plants grappling with high turbidity and elevated dissolved organics face a significant financial drain due to fouling. Regular treatments using bleach, acid, and surface-active agents oxidize polymeric fibers, consequently shortening their effective lifespan. While ceramic modules can withstand rigorous cleaning, their elevated price confines them to upscale markets. Pall's Gradient Permeability Integrated Cartridge design, boasting graduated permeability, has notably cut down cleaning frequency in dairy trials, yet it is just now entering wider markets. Research on graphene-oxide coatings indicates potential in curbing flux decline in laboratory feeds; however, the absence of timely pilot data hampers field adoption. In the Middle East, operators are experimenting with ultraviolet pre-oxidation and dissolved-air flotation to lessen organic loads, though this comes with increased capital complexity.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption in Food and Beverage Product-Recovery Loops

- Decentralized Ultrafiltration Skids for Smart-City and Remote Installations

- Competition From Membrane Bioreactor and Next-Generation Low-Pressure Membranes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, polymeric membranes secured 67.20% of the revenue, capitalizing on their cost advantages. However, ceramic alternatives are set to outpace the competition, boasting a projected CAGR of 10.56% in the ultrafiltration market from 2026 to 2031. Hollow fiber polymeric units are strategically priced to align with standard municipal budget depreciation schedules. On the other hand, food and pharmaceutical processors opt for the pricier ceramic units. This choice stems from ceramics' enhanced heat and chemical tolerance, which markedly prolongs their service life. Pall's new GP-IC ceramic has addressed previous yield loss concerns, now boasting a high recovery rate for dairy proteins. Furthermore, China's Yiwu plant illustrates that when factoring in long-term pricing for fouling downtime, ceramics can rival the economic viability of polymeric options.

Metallic and other inorganic membranes command a modest market share, predominantly catering to semiconductor ultrapure water loops. In this specialized arena, the capability to eliminate minuscule particles can markedly boost chip yield. Asahi Kasei's OAT series rises to meet these exacting standards, albeit for a select fabrication node. Concurrently, heightened scrutiny on per- and polyfluoroalkyl substances in Europe has pivoted the industry's attention towards ceramics devoid of these compounds. Emphasizing this shift, Nanostone's Ceramic Ultrafiltration Flow, boasting an augmented surface area per module, is swaying procurement choices towards ceramics, especially among utilities with rigorous compliance mandates.

In 2025, hollow fiber modules dominated the landscape, accounting for 51.45% of deployments. These modules boasted the capability to pack up to 1,200 square meters of membrane per cubic meter and effectively managed solids through an outside-in flow. Meanwhile, spiral-wound designs transitioned from reverse osmosis to ultrafiltration, catering to sanitary needs in the food and pharmaceutical sectors. Notably, Alfa Laval's DuroLac spiral, with its innovative envelope geometry tweaks, achieved a 15% boost in permeate. Tubular modules, favored for breweries and high-solids municipal retrofits due to their ability to scour foulants with shear, are projected to grow at a 10.24% CAGR from 2026 to 2031. A testament to this technology's prowess, Yiwu in China showcased a ceramic tubular installation achieving crossflow velocities of 3 meters per second, effectively warding off algae. In the realm of single-use biotech, plate-and-frame capsules are flourishing. Merck's Cork plant, for instance, produces Pellicon devices that not only sidestep cleaning validation but also expedite batch turnover.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.31% of global revenue, fueled by China's desalination initiatives, Singapore's NEWater expansion, and India's vaccine manufacturing. Notably, an ultrafiltration pretreatment in Qingdao Dongjiakou has set a new standard for energy efficiency. Singapore's predictive cleaning techniques have yielded impressive energy savings, underscoring the power of data-driven operations. Additionally, pharmaceutical centers in Hyderabad and Bangalore are increasingly opting for imported single-use cassettes, signaling a market opportunity for domestic suppliers.

From 2026 to 2031, the Middle-East and Africa are poised to lead with a robust 10.74% CAGR. The Saudi National Water Company is spearheading a major initiative in Qassim, and Bahrain is heavily investing in its Sitra and Hidd projects. Notably, many recent desalination tenders in the region are now featuring ultrafiltration, highlighting its crucial role in water security. In South Africa, municipalities are exploring containerized skids as a budget-friendly solution to drought challenges.

While Europe and North America command a significant share of global revenue, their growth is tempered by a focus on retrofits and replacements. The European Union's Urban Wastewater Directive emphasizes the removal of nutrients and microplastics. Furthermore, with new per- and polyfluoroalkyl substance limits set to kick in by 2026, there is a surge in membrane technology advancements. Alfa Laval's Sarpsborg plant is on track to meet these regulatory standards by 2027. In North America, even as the capital cycle slows, there is a steady demand driven by bioprocessing expansions. A case in point is Meissner's new plant in Georgia, which not only produces single-use systems but also generates significant employment. Meanwhile, in South America, despite a smaller market presence, Veolia's Vitoria station in Brazil underscores the region's potential for industrial water reuse.

- 3M

- Alfa Laval

- Aquatech

- Asahi Kasei Corporation

- DuPont

- GEA Group Aktiengesellschaft

- Hydranautics (Nitto Group)

- Kovalus Separation Solutions

- Kubota Corporation

- LG Chem Ltd.

- MANN+HUMMEL

- Membranium

- Mitsubishi Chemical Aqua Solutions

- Nanostone

- Ovivo Inc.

- Pall Corporation (Danaher)

- Pentair

- Sartorius AG

- Toray Industries, Inc.

- Toyobo Co., Ltd.

- Veolia

- Xylem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for water and wastewater treatment

- 4.2.2 Integration of UF as pretreatment for RO and desalination

- 4.2.3 Rising adoption in food and beverage product-recovery loops

- 4.2.4 Decentralised UF skids for smart-city and remote installations

- 4.2.5 Regulatory push for micro-plastics removal in drinking water

- 4.3 Market Restraints

- 4.3.1 Membrane fouling and cleaning costs

- 4.3.2 Competition from MBR and next-gen low-pressure membranes

- 4.3.3 End-of-life polymer-membrane disposal uncertainty

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Membrane Type

- 5.1.1 Polymeric Membranes

- 5.1.2 Ceramic Membranes

- 5.1.3 Metallic and Other Inorganic Membranes

- 5.2 By Module Type

- 5.2.1 Hollow Fiber

- 5.2.2 Spiral Wound

- 5.2.3 Tubular

- 5.2.4 Plate and Frame

- 5.3 By Application

- 5.3.1 Water and Wastewater Treatment

- 5.3.2 Food and Beverage Processing

- 5.3.3 Pharmaceuticals and Biotechnology

- 5.3.4 Chemicals and Petrochemicals

- 5.3.5 Micro-electronics

- 5.4 By End-user Industry

- 5.4.1 Municipal

- 5.4.2 Industrial

- 5.4.3 Healthcare

- 5.4.4 Agriculture

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Southeast Asia

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alfa Laval

- 6.4.3 Aquatech

- 6.4.4 Asahi Kasei Corporation

- 6.4.5 DuPont

- 6.4.6 GEA Group Aktiengesellschaft

- 6.4.7 Hydranautics (Nitto Group)

- 6.4.8 Kovalus Separation Solutions

- 6.4.9 Kubota Corporation

- 6.4.10 LG Chem Ltd.

- 6.4.11 MANN+HUMMEL

- 6.4.12 Membranium

- 6.4.13 Mitsubishi Chemical Aqua Solutions

- 6.4.14 Nanostone

- 6.4.15 Ovivo Inc.

- 6.4.16 Pall Corporation (Danaher)

- 6.4.17 Pentair

- 6.4.18 Sartorius AG

- 6.4.19 Toray Industries, Inc.

- 6.4.20 Toyobo Co., Ltd.

- 6.4.21 Veolia

- 6.4.22 Xylem

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Technological Advancements in Membrane Performance

- 7.3 Opportunities in Emerging Water-scarce Markets