|

시장보고서

상품코드

2061928

자동차용 경량 소재 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Lightweight Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

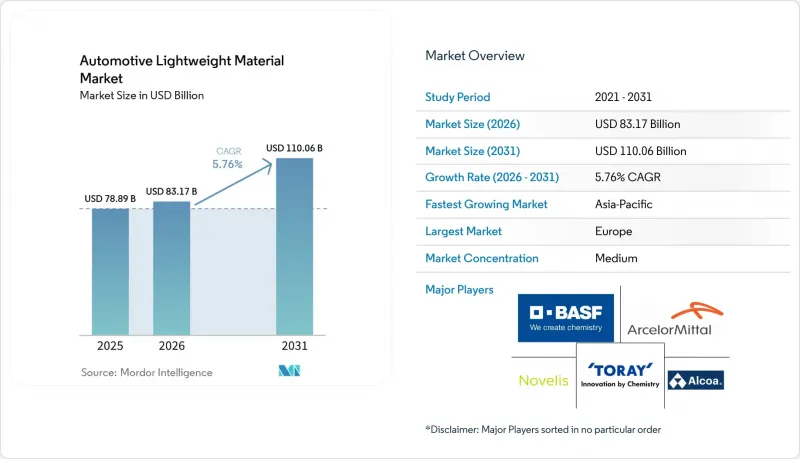

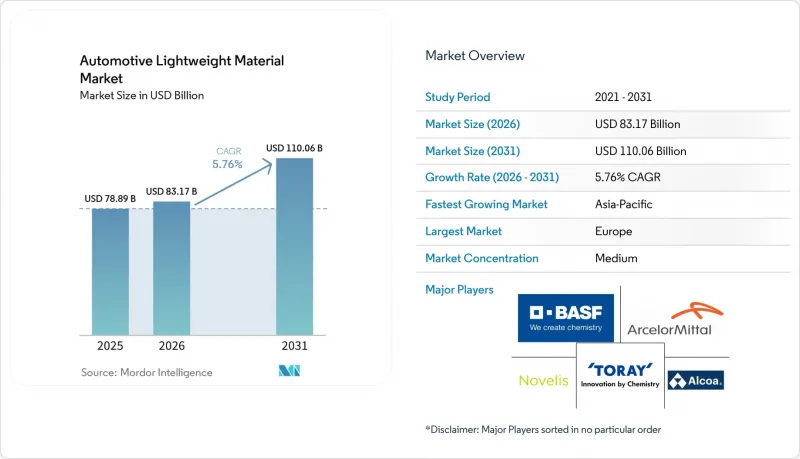

Mordor Intelligence에 의하면, 자동차용 경량 소재 시장 규모는 2025년 788억 9,000만 달러로 평가되었습니다. 2026년 831억 7,000만 달러에서 2031년까지 1,100억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.76%를 나타낼 것으로 예측됩니다.

본 보고서는 소재 유형(금속, 폴리머 및 복합재료, 기타), 용도(화이트 바디, 섀시 및 서스펜션, 파워트레인 및 드라이브트레인, 기타), 차량 유형(승용차, 소형 상용차, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자동차용 경량 소재 시장 동향 및 분석

연비 효율과 CO2 감축에 대한 수요 증가

라이프사이클 탄소 회계에서는 현재 저탄소 에너지로 생산되고 재활용률이 높은 소재가 우선적으로 고려되고 있습니다. 유럽연합(EU)은 2030년까지 자동차의 이산화탄소 배출량을 대폭 감축하겠다는 목표를 설정했습니다. 중요한 점은 유럽연합이 2027년 이후 슈퍼크레딧을 단계적으로 폐지할 예정이며, 이에 따라 자동차 제조업체들은 규제의 허점을 이용하는 대신 배출량을 실질적으로 감축해야 할 압박을 받게 될 것입니다. 이러한 추세를 뒷받침하는 사례로, 메르세데스-벤츠는 자사의 전기식 소형 고급차에 저배출 알루미늄을 채택하여 차량의 수명 주기 전반에 걸친 배출량을 현저히 줄였습니다. 중국의 이중 크레딧 제도에서는 차량 중량이 가벼운 배터리식 전기차 모델에 대해 추가 점수가 부여됩니다. 이러한 인센티브 덕분에 소형 플랫폼에서 마그네슘 다이캐스팅 및 열가소성 복합재료의 사용이 촉진되고 있습니다. 도요타는 2030년부터 재활용 소재 사용량(중량 기준)을 늘리겠다고 약속하며, 재활용의 전략적 중요성을 강조하고 있습니다. 배터리식 전기차의 무게를 줄이면 주행 거리가 늘어나고 배터리 비용이 절감되어 총 소유 비용(TCO) 측면에서 경쟁력이 높아집니다.

전기차 및 하이브리드차의 보급 확대

배터리 팩은 소재 경제의 양상을 변화시키고 있습니다. 유럽의 배터리식 전기차에서는 특히 차체와 모터 하우징에서 알루미늄 사용량이 증가할 것으로 전망됩니다. 기가캐스팅 기술을 통해 여러 개의 프레스 부품이 단일 리어 플로어 모듈로 통합되어, 대폭적인 경량화와 용접 공정의 간소화가 실현되었습니다. 복합재로 제작된 배터리 케이스의 사용도 증가하고 있으며, 탄소섬유 강화 폴리머는 강철에 비해 대폭적인 경량화를 실현할 뿐만 아니라 전자기 차폐 기능도 갖추고 있습니다. 중국의 자동차 제조업체들은 기존의 화이트 바디 생산 라인을 생략하고 첨단 대용량 프레스 기계를 도입함으로써 제품 주기를 대폭 단축하고 있습니다. 엔진과 배터리를 모두 탑재한 하이브리드 차량의 경우, 이중 파워트레인으로 인한 중량 증가를 상쇄하기 위해 경량 도어 패널이나 첨단 고장력 강판 구조의 채택이 필수적입니다.

첨단 복합재료 및 합금의 높은 비용

고장력 강철보다 훨씬 비싼 탄소섬유 강화 폴리머는 주로 시장의 고가 대에 속하는 고급차에 사용되고 있습니다. 도레이의 혁신적인 프레스 성형 기술은 생산 시간을 대폭 단축하지만, 여전히 알루미늄보다 비용이 높기 때문에 그 보급은 제한적입니다. 마그네슘 다이캐스팅은 현저한 경량화를 실현하지만, 비용이 높기 때문에 그 용도는 주로 센서 하우징으로 한정되어 있습니다. 인도에서는 OEM 업체들이 차량 경량화와 합리적인 가격 유지 사이의 균형을 맞추기 위해 첨단 고장력강과 알루미늄을 선택적으로 사용하는 데 주력하고 있으며, 이는 해당 지역의 가격 민감도를 반영하고 있습니다.

부문별 분석

2025년에는 폴리머 및 복합재료가 자동차용 경량 소재 시장의 66.25%를 차지하며 주도적인 위치를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.56%를 나타낼 것으로 전망됩니다. 알루미늄보다 훨씬 가벼운 탄소섬유 재질의 인클로저는 전기차의 주행 거리를 늘리고 배터리의 소형화를 실현합니다. 폴리머 및 복합 소재에 중점을 둔 자동차용 경량 소재 시장은 주류 모델에 유리섬유로 제작된 실드, 휠 아치 라이너, 언더바디 패널이 채택되는 것을 원동력으로 삼아, 금세기 후반부터 2030년대 초반에 걸쳐 상당한 성장이 예상됩니다. 폴리아미드나 폴리프로필렌과 같은 엔지니어링 플라스틱은 BASF의 화학적 재활용 원료인 ‘Cycled’의 혜택을 받아, 재인증 절차 없이도 순환형 컨텐츠 의무 요건을 충족할 수 있습니다.

최근 몇 년간 금속은 상당한 시장 점유율을 차지해 왔지만, 여전히 적용 단계에 있습니다. 알루미늄은 확립된 공급망과 뛰어난 열전도성 덕분에 생산량 면에서 선두를 달리고 있으며, 배터리 하우징의 유력한 후보로 떠오르고 있습니다. 탁월한 인장 강도로 알려진 첨단 고장력강은 현재 충돌 안전에 중요한 기둥이나 레일에 우선적으로 채택되고 있으며, 용접성을 저해하지 않으면서 국부적인 판 두께를 얇게 만들 수 있게 해줍니다. 마그네슘 합금은 시장 점유율은 낮지만, 스티어링이나 센서 하우징과 같은 틈새 용도로 활용되고 있습니다. 다만, 산화 제어가 필요하기 때문에 주조 비용은 높아집니다. 티타늄은 비용이 비싸기 때문에 슈퍼카에만 사용되는 고급 소재입니다. 2030년대 초반을 내다보면, 차세대 합금이나 탄소 제로 제련과 같은 기술 혁신이 복합재료와의 탄소 배출량 격차를 해소함에 따라, 금속은 자동차용 경량 소재 시장에서 여전히 큰 비중을 차지할 것으로 전망됩니다.

지역별 분석

2025년 자동차용 경량 소재 시장 규모의 35.70%를 유럽이 차지했으며, 독일의 OEM 업체들은 동일한 플랫폼에서 알루미늄 제 기가캐스트 리어 구조, 첨단 고장력강 제 크래시 존, 복합재 제 리프트 게이트를 도입함으로써 성능 대비 비용 효율을 최적화하고 있습니다. BMW의 iX3는 휠 캐리어 주조 부품에 재활용 알루미늄을 대량으로 채택하고 있으며, 고품질 스크랩을 인공지능(AI) 기반 결함 감지 기술과 결합함으로써 안전상 매우 중요한 기준을 충족할 수 있음을 입증하고 있습니다. 이러한 움직임은 유럽연합(EU)이 야심 찬 자동차 차량군의 이산화탄소 배출 감축 목표를 설정하고, 탄소 집약적인 수입품에 관세를 부과하며, 2020년대 말까지 제조 과정에서 재활용 소재 사용을 확대하도록 의무화하는 가운데 진행되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.12%로 성장할 것으로 전망됩니다. 1차 알루미늄 생산량이 막대한 중국은 공급 상한선을 계속해서 강화하고 있습니다. 그러나 이 나라는 BYD, NIO, 샤오미의 공장에서 대용량 프레스 기계를 활용하여 대규모 주조 사업에서 주도적인 입지를 차지하고 있습니다. 향후 몇 년간 배터리식 전기차(BEV) 플랫폼의 채택 확대에 힘입어, 자동차용 프로파일의 압출 성형 능력은 크게 증가할 것으로 예측됩니다. 일본은 열가소성 복합재료의 고속 용접 기술 개발을 추진하고 있습니다. 한편, 2030년까지 전기차 보급률에서 상당한 점유율을 확보하는 것을 목표로 하는 인도는 현지 공급망을 강화하기 위해 첨단 고장력강의 냉간 압연 및 알루미늄 생산에 투자하고 있습니다.

북미는 미국·멕시코·캐나다 협정(USMCA)에 따른 현지 조달 의무와 인플레이션 억제법(IRA)을 통해 도입된 배터리 조달 인센티브에 힘입어 시장에서 큰 점유율을 확보했습니다. Novelis는 향후 10년 후반에 미국에서 대규모 제철소를 가동할 예정이며, 테슬라, 제너럴 모터스, 포드 등 주요 제조업체에 자동차용 강판 및 인클로저용 소재를 공급하게 될 것입니다. 멕시코는 지역 공급망을 뒷받침하는 대규모 주조 사업의 중요한 거점으로 부상하고 있습니다. 한편, 캐나다는 ELYSIS 이니셔티브의 일환으로 탄소 제로 제련 기술의 시범 운영을 진행 중이며, 내재 탄소(embodied carbon) 지표를 바탕으로 타사와의 차별화를 꾀하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the automotive lightweight material market size is projected to expand from USD 78.89 billion in 2025 and USD 83.17 billion in 2026 to USD 110.06 billion by 2031, registering a CAGR of 5.76% between 2026 and 2031.

This report is Segmented by Material Type (Metals, Polymers and Composites, and More), Application (Body-In-White, Chassis and Suspension, Powertrain and Drivetrain, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Lightweight Material Market Trends and Insights

Growing Demand for Fuel-Efficiency and CO2-Reduction

Lifecycle-carbon accounting now prioritizes materials made with low-emission energy and a high recycled content. The European Union has set a target to significantly cut fleet carbon dioxide emissions by 2030. Importantly, the European Union will phase out super-credits after 2027, pushing automakers to make real reductions in emissions rather than depending on regulatory loopholes. In a move underscoring this trend, Mercedes-Benz has integrated low-emission aluminum into its electric compact luxury automobile, leading to a marked decrease in the vehicle's lifecycle emissions. China's dual-credit system offers extra points for battery-electric models with lower curb weight. This incentive promotes the use of magnesium die castings and thermoplastic composites in compact platforms. Toyota has committed to increasing the use of recycled material by weight starting in 2030, highlighting the strategic importance of recycling. Reducing the weight of a battery-electric vehicle enhances its range and lowers battery costs, improving overall cost-of-ownership advantages.

Rising Adoption of Electric and Hybrid Vehicles

Battery packs are reshaping material economics: European battery-electric vehicles are set to increase aluminum usage, particularly in enclosures and motor housings. Giga-casting technology is consolidating multiple stamped parts into a single rear-floor module, leading to notable weight reductions and simplified welding. The use of composite battery enclosures is on the rise, with carbon fiber reinforced polymer providing significant weight savings over steel and added electromagnetic shielding. Chinese automakers are skipping traditional body-in-white lines in favor of advanced high-capacity presses, greatly speeding up their product cycles. With hybrids featuring both an engine and a battery, adopting lightweight closures and Advanced High-Strength Steel structures becomes vital to counterbalance the extra weight from the dual powertrain.

High Cost of Advanced Composites and Alloys

Carbon-fiber polymers, which are significantly more expensive than high-strength steel, are primarily used in premium cars priced at the higher end of the market. Toray's innovative press-molding technique reduces production time considerably; however, it remains costlier than aluminum, limiting its broader adoption. Magnesium die castings provide notable weight reduction but are more expensive, restricting their application mainly to sensor housings. In India, original equipment manufacturers focus on advanced high-strength steel and selective use of aluminum to achieve a balance between reducing vehicle weight and maintaining affordability, reflecting the region's sensitivity to pricing.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Global and Regional Vehicle-Weight Legislation

- Lightweighting for AI-Sensor Payload in Autonomous Cars

- Manufacturing and Repair Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymers and Composites dominated with 66.25% of the automotive lightweight material market share in 2025 and are projected to post a 6.56% CAGR from 2026 to 2031. Carbon-fiber enclosures, lighter than aluminum by a significant percentage, boost electric-vehicle range and reduce battery size. The automotive lightweight material market, focusing on polymers and composites, is expected to experience substantial growth from the latter part of this decade into the early 2030s, driven by the adoption of glass-fiber shields, wheel-arch liners, and underbody panels in mainstream models. Engineering plastics like polyamide and polypropylene benefit from BASF's chemically recycled Cycled feedstock, aligning with circular-content mandates without the need for requalification.

While metals held a notable share in recent years, they are still adapting. Aluminum leads in volume, thanks to established supply chains and its superior thermal conductivity, making it a top choice for battery housings. Advanced high-strength steels, known for their exceptional tensile strength, are now prioritized for crash-critical pillars and rails, allowing for localized thickness reduction without compromising weldability. Magnesium alloys, with a modest share, find their niche in steering and sensor housings, though oxidation control inflates casting costs. Due to its high cost, titanium is a luxury reserved for supercars. Looking ahead to the early 2030s, metals are set to maintain a significant portion of the automotive lightweight material market, as innovations like next-generation alloys and carbon-free smelting bridge the carbon gap with composites.

Geography Analysis

With Europe accounting for 35.70% of the automotive lightweight material market size in 2025, German original equipment manufacturers are optimizing performance to-cost ratios by rolling out aluminum giga-cast rear structures, advanced high-strength steel crash zones, and composite liftgates on the same platform. BMW's iX3 demonstrates that high-quality scrap, when paired with artificial intelligence defect detection, can meet safety-critical standards, as it incorporates a significant proportion of recycled aluminum in its wheel-carrier castings. These moves come as the European Union sets ambitious fleet carbon dioxide emission reduction targets, imposes tariffs on carbon-intensive imports, and mandates increased use of recycled content in manufacturing by the end of the decade.

Asia-Pacific will expand at a 7.12% CAGR from 2026 to 2031. China, with a significant primary-aluminum output, continues to tighten its supply ceiling. Yet, the nation leads in large-scale casting operations, utilizing high-capacity presses at plants for BYD, NIO, and Xiaomi. Over the coming years, extrusion capacity for automotive profiles is expected to grow substantially, driven by the increasing adoption of battery electric vehicle platforms. Japan is advancing techniques for the rapid welding of thermoplastic composites. Meanwhile, India, aiming to achieve a notable share of electric vehicle penetration by the end of the decade, is investing in advanced high-strength steel cold-rolling and aluminum production to strengthen its localized supply chain.

North America captured a significant portion of the market, supported by local-content mandates under the United States-Mexico-Canada Agreement and incentives for battery sourcing introduced by the Inflation Reduction Act. Novelis is set to commission a major mill in the United States in the latter half of the decade, which will supply automotive sheet and enclosure stock to leading manufacturers such as Tesla, General Motors, and Ford. Mexico is emerging as a key hub for large-scale casting operations to support regional supply chains. At the same time, Canada is piloting carbon-free smelting technology under the ELYSIS initiative, aiming to differentiate itself based on embodied-carbon metrics.

- Alcoa Corporation

- ArcelorMittal

- BASF

- Constellium SE

- Covestro AG

- Dow Inc.

- Hexcel Corporation

- Hydro Aluminium ASA

- JFE Steel Corporation

- Jushi Group Co., Ltd.

- LyondellBasell Industries N.V.

- Nippon Steel Corporation

- Novelis

- Owens Corning

- POSCO

- SABIC

- SGL Carbon SE

- Solvay S.A.

- Tata Steel Ltd.

- Teijin Ltd.

- Thyssenkrupp AG

- Toray Industries, Inc.

- UACJ Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for fuel-efficiency and CO2-reduction

- 4.2.2 Rising adoption of electric and hybrid vehicles

- 4.2.3 Stringent global and regional vehicle-weight legislation

- 4.2.4 Lightweighting for AI-sensor payload in autonomous cars

- 4.2.5 Circular-economy credits for embedded-carbon reduction

- 4.3 Market Restraints

- 4.3.1 High cost of advanced composites and alloys

- 4.3.2 Manufacturing and repair complexity

- 4.3.3 Supply-chain volatility in critical minerals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Metals

- 5.1.1.1 Aluminum

- 5.1.1.2 High-Strength Steel (AHSS/UHSS)

- 5.1.1.3 Magnesium Alloys

- 5.1.1.4 Titanium Alloys

- 5.1.2 Polymers and Composites

- 5.1.2.1 Carbon-Fiber-Reinforced Polymer (CFRP)

- 5.1.2.2 Glass-Fiber-Reinforced Polymer (GFRP)

- 5.1.2.3 Engineering Plastics

- 5.1.3 Elastomers

- 5.1.1 Metals

- 5.2 By Application

- 5.2.1 Body-in-White

- 5.2.2 Chassis and Suspension

- 5.2.3 Powertrain and Drivetrain

- 5.2.4 Interior Components

- 5.2.5 Exterior/Trim

- 5.2.6 Battery Enclosures and Thermal Systems

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Electric and Hybrid Vehicles

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 ArcelorMittal

- 6.4.3 BASF

- 6.4.4 Constellium SE

- 6.4.5 Covestro AG

- 6.4.6 Dow Inc.

- 6.4.7 Hexcel Corporation

- 6.4.8 Hydro Aluminium ASA

- 6.4.9 JFE Steel Corporation

- 6.4.10 Jushi Group Co., Ltd.

- 6.4.11 LyondellBasell Industries N.V.

- 6.4.12 Nippon Steel Corporation

- 6.4.13 Novelis

- 6.4.14 Owens Corning

- 6.4.15 POSCO

- 6.4.16 SABIC

- 6.4.17 SGL Carbon SE

- 6.4.18 Solvay S.A.

- 6.4.19 Tata Steel Ltd.

- 6.4.20 Teijin Ltd.

- 6.4.21 Thyssenkrupp AG

- 6.4.22 Toray Industries, Inc.

- 6.4.23 UACJ Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Advances in Multi-material Joining Technologies

- 7.3 Lightweighting of EV Platforms and Powertrains