|

시장보고서

상품코드

2061942

법률 및 규제기술 분야 에이전트 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI In Legal And Regulatory Tech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

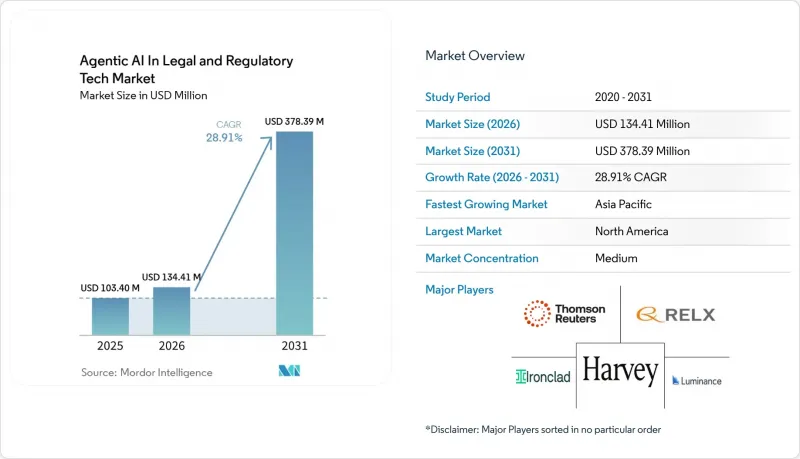

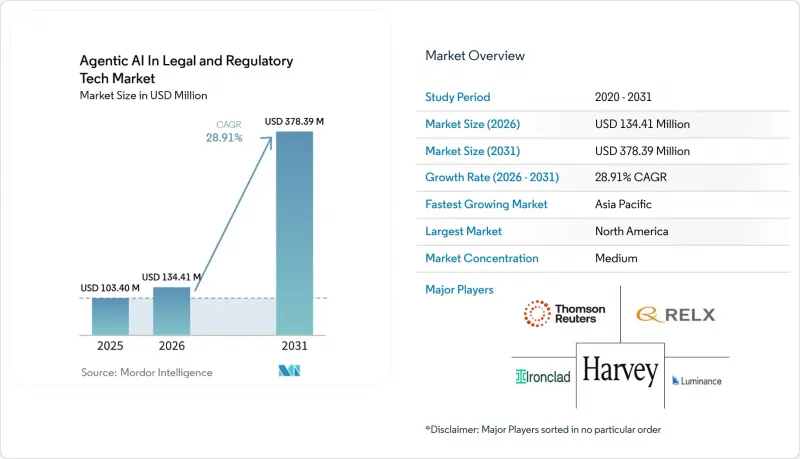

법률 및 규제기술 분야 에이전트 AI 시장은 2025년 1억 340만 달러로 평가되었고, 2026년에는 1억 3,441만 달러로 추정되고, 2026-2031년 CAGR 28.91%로 성장을 지속할 전망이며, 2031년까지 4억 7,839만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도별(계약 수명주기 관리 에이전트, e-디스커버리 및 문서 검토 에이전트 등), 도입 모델별(클라우드 기반 등), 최종 사용자 산업별(법률 사무소, 기업 법무 부서 등), 핵심 기술별(머신러닝 및 예측 모델 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

법률 및 규제기술 분야 에이전트 AI 시장 동향 및 인사이트

법무 워크플로우에서 생성형 AI 도구의 주류화가 가속화되고 있습니다.

Corporate Legal Operations Consortium의 데이터에 따르면, 2025년에는 기업 법무팀의 52%가 실제 운영 단계의 생성형 AI 시스템을 도입할 것으로 예상되며, 이는 전년 대비 2배 이상 증가한 수치입니다. 또한, 85%가 정책을 수립하는 사내 AI 위원회를 설치해 두었습니다. 이러한 위원회의 광범위한 설치는 일회성 시범 사업이 아니라, 상설적인 예산이 확보되어 있음을 시사합니다. 톰슨 로이터는 현재 법무 전문가의 40%가 생성형 AI를 활용하고 있으며, 53%는 12개월 이내에 완전 자율형 에이전트를 도입할 계획이라고 지적했습니다. 이러한 급속한 보급은 LLM(대규모 언어 모델)이 최소한의 맞춤형 코딩만 필요로 하기 때문에 중견 기업들도 과거에는 대기업의 전유물이었던 기능에 즉시 접근할 수 있게 되었습니다는 점에서 특히 주목할 만합니다.

외부 변호사 비용의 급등에 따른 비용 절감의 필요성

톰슨 로이터는 2024년 외부 변호사의 평균 수임료가 8.3% 상승했다고 보고했으며, 이에 따라 기업 법무 담당자들은 사내 팀을 확충하고, 복잡도가 낮은 외부 업무를 대체할 AI 기반 검토 도구의 도입을 추진하고 있습니다. 변호사 500명 규모의 로펌에서는 AI를 활용한 사건 선별 시스템을 도입한 결과, 사건 접수에 소요되는 시간이 48시간에서 5분으로 단축되어 파트너의 업무 시간을 줄이는 동시에 대응 속도를 높일 수 있었습니다. 법무 운영 부문에서는 비용 관리와 인재 전략을 연계하여, 인재 유지를 위한 요인으로 기술력 습득을 점점 더 중요시하고 있습니다.

클라우드 호스팅형 LLM 추론과 관련된 데이터 개인정보 보호 및 변호사와 의뢰인 간의 비밀 유지에 대한 우려

2026년 2월의 ‘미국 대 헵너’ 판결에서는 계약상 보호 조치가 수반되지 않는 소비자용 챗봇의 사용은 변호사와 의뢰인 간의 비밀 유지 특권을 포기하는 것으로 선언되었습니다. 이 판결에 따라, 데이터 보유 제로, 지역별 데이터 보관 장소 관리, 그리고 SOC 2 Type II 인증을 약속하는 엔터프라이즈급 서비스로의 전환이 가속화되었습니다. 현재 47개 주의 변호사협회는 기밀 데이터를 AI 도구에 입력하기 전에 의뢰인의 서면 동의를 의무화하고 있습니다. 의료 및 금융 업계의 리스크 회피 성향이 강한 법무 담당자들은 벤더가 온프레미스 또는 하이브리드형 옵션을 제공할 때까지 도입을 미루고 있습니다.

부문별 분석

2025년, e-디스커버리 및 문서 검토 에이전트는 법률 및 규제기술 분야 에이전트 AI(인공지능) 시장 점유율의 34.89%를 차지했습니다. 이러한 우위는 사건마다 100만 달러를 넘는 경우도 드물지 않은 증거개시 예산을 절감할 수 있는 능력에 기반을 두고 있습니다. Relativity사의 ‘aiR for Review’는 특권 정보 분류에서 90%의 정확도를 달성하여, 수동 검토 시간을 절반으로 줄였습니다. 소송 결과 예측 에이전트는 현재 규모는 작지만 연평균 성장률(CAGR) 30.11%를 나타낼 것으로 예측되며, 2031년까지 법률 및 규제기술 분야 에이전트 AI 시장에 상당한 규모 확대를 가져올 전망입니다.

예측 분석의 급속한 확산은 데이터에 기반한 합의금 범위와 재판지 선정 전략을 모색하는 기업들 덕분입니다. Lex Machina의 판사 분석 모듈은 현재 AmLaw 200에 선정된 로펌의 60%에서 표준으로 채택되고 있습니다. 동시에, 계약 수명주기 관리 에이전트는 협상 주기 단축을 희망하는 기업의 법무 부서의 관심을 끌고 있으며, Ironclad의 1억 5,000만 달러 규모 시리즈 F 자금 조달도 이를 입증하고 있습니다. 컴플라이언스 인텔리전스 및 지적재산권 관리 에이전트 역시 수요를 뒷받침하고 있으며, 특히 규제 대응이 까다로운 업계나 대규모 특허 포트폴리오를 보유한 업계에서 수요가 증가하고 있습니다.

2025년에는 클라우드 플랫폼이 매출의 61.89%를 차지한 것으로 평가되었으며, 대다수의 구매자가 구독형 비즈니스 모델과 지속적인 모델 업그레이드를 선호한다는 사실이 입증되었습니다. 따라서 법률 및 규제기술 분야 에이전트 AI는 하이퍼스케일러의 GPU 가용성과 여전히 밀접하게 연결되어 있습니다. 하지만 국경을 넘어선 M&A 등 기밀 데이터는 기업의 방화벽에 보관해야 하므로, 엣지 및 임베디드형 도입은 CAGR 29.71%로 확대되고 있습니다. 이러한 변화에 따라, 하드웨어에 최적화된 추론 어플라이언스를 위한 법률 및 규제기술 분야 에이전트 AI 시장 규모가 확대되고 있습니다.

하이브리드 아키텍처에서는 일상 업무를 클라우드에 남겨두면서 기밀 데이터는 온프레미스에서 처리할 수 있지만, API 중복으로 인한 비용도 발생합니다. 구식 문서 관리 시스템을 보유한 대형 AmLaw(미국 로펌)은 기존 기록과 통합하기 위해 온프레미스 클러스터를 선택하는 경우가 많습니다. 한편, 업무 관리 벤더는 경량 LLM을 탑재하고 있어, 이를 통해 소규모 사무실에서도 여러 계정을 전환할 필요 없이 에이전트형 기능을 이용할 수 있게 되었습니다.

지역별 분석

2025년 법률 및 규제기술 분야 에이전트 AI 매출액 중 북미가 41.89%를 차지했습니다. AmLaw 100에 선정된 로펌과 포춘 500대 기업의 법무 부서는 계약 수명주기 관리 및 규정 준수 대응 솔루션을 업무 전반에 걸쳐 도입함으로써 수요를 주도하고 있습니다. 2026년 2월 미국 뉴욕 남부 지방 연방 법원이 변호사와 의뢰인 간의 비밀 유지 의무를 명확히 한 것을 계기로, 기업에서의 도입이 급증했습니다. 캐나다의 성장은 더욱 꾸준합니다. 토론토의 법률 사무소들은 미국 내 동종 업계와의 경쟁력을 유지하기 위해 e-디스커버리 에이전트를 선호하여 채용하고 있는 반면, 멕시코에서는 주로 미국·멕시코·캐나다 협정(USMCA)을 준수하는 다국적 기업의 자회사들 사이에서 도입이 진행되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 29.91%를 나타낼 것으로 예측되며, 이는 세계에서 가장 빠른 성장 속도입니다. 중국의 ‘스마트 법원’에서는 AI를 활용한 사건 배정 및 양형 지원을 통해 연간 3,000만 건 이상의 사건을 처리하고 있습니다. 일본에서는 기업 거래의 현대화를 위해 법무성이 AI를 활용한 계약서 검토를 시범 운영하고 있는 반면, 인도의 디지털 법원 프로젝트는 비용 효율이 높은 조사 대행사에 대한 수요를 높이고 있습니다. 싱가포르의 ‘스마트 네이션’ 전략과 반도체·금융 분야의 복잡한 한국 규제 역시 추가적인 호재로 작용하고 있습니다.

유럽은 다소 뒤처져 있지만, GDPR(EU 개인정보보호규정) 시행과 활발한 국경 간 M&A의 혜택을 받아 EU 내 법규 및 기술 분야의 에이전트형 AI 시장이 확대되고 있습니다. 런던의 매직 서클 로펌은 다중 관할권에 걸친 실사를 관리하기 위해 오케스트레이션 플랫폼을 도입한 반면, 독일의 한 로펌은 EU AI법에 대한 규정 준수 감사에 주력하고 있습니다. 프랑스의 스타트업 업계에서는 대륙법 체계에 맞춘 계약 협상 에이전트가 개발되고 있습니다. 아랍에미리트(UAE)와 사우디아라비아가 주도하는 중동에서는 규정 준수 및 분쟁 해결 도구를 구현하기 위해 국가 주도의 AI 도입 방침이 채택되고 있습니다. 아프리카에서는 다른 지역의 인프라 격차로 인해 도입이 남아프리카공화국과 이집트에 집중되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the agentic AI market in the legal and regulatory tech market is expected to grow from USD 103.4 million in 2025 to USD 134.41 million in 2026, and is forecast to reach USD 478.39 million by 2031 at a 28.91% CAGR over 2026-2031.

This report is Segmented by Application (Contract Lifecycle Management Agents, Ediscovery and Document Review Agents, and More), Deployment Model (Cloud-Based, and More), End-User Industry (Law Firms, Corporate Legal Departments, and More), Core Technology (Machine-Learning and Predictive Models, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Legal And Regulatory Tech Market Trends and Insights

Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows

Corporate Legal Operations Consortium data show that 52% of corporate legal teams had production-grade generative AI systems in 2025, more than double the prior year, and 85% had an internal AI committee guiding policy. Widespread committees signal permanent budget lines rather than one-off pilots. Thomson Reuters noted that 40% of legal professionals now use generative AI and 53% expect to add fully autonomous agents within 12 months. The steep curve is unique because LLMs require minimal custom coding, giving mid-market firms immediate access to capabilities once reserved for the exclusive domain of large firms.

Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees

Thomson Reuters reported an 8.3% blended-rate increase for outside counsel in 2024, prompting corporate legal heads to expand in-house teams and adopt AI-driven review tools that replace low-complexity external work. A 500-attorney firm documented a drop in intake time from 48 hours to 5 minutes after deploying AI-supported triage, cutting partner hours and improving responsiveness. Legal operations groups increasingly rank technology proficiency as a talent-retention factor, linking cost control to workforce strategy.

Data-Privacy And Privilege Concerns Over Cloud-Hosted LLM Inference

A February 2026 ruling in US v. Heppner declared that using consumer chatbots without contractual protections waived attorney-client privilege. The decision accelerated migration to enterprise-grade tiers that promise zero-retain data handling, regional residency controls, and SOC 2 Type II attestations. Forty-seven state bars now require written client consent before confidential data passes through AI tools. Risk-averse general counsel in healthcare and finance are delaying deployments until vendors deliver on-premises or hybrid options.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-First Digital-Transformation Initiatives Across Legal Operations

- Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation

- Hallucination Liability And Ethical-Competence Obligations For Attorneys

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, eDiscovery and document review agents secured 34.89% of the agentic AI (artificial intelligence) market share in the legal and regulatory tech market, a dominance driven by their ability to cut discovery budgets that often exceed USD 1 million per matter. Relativity's aiR for Review reached 90% accuracy in privilege classification, halving human review hours. Litigation outcome prediction agents, though smaller today, are forecast to expand at a 30.11% CAGR, adding significant volume to the agentic artificial intelligence market in legal and regulatory tech by 2031.

Rapid adoption of predictive analytics stems from firms seeking data-backed settlement ranges and venue strategies. Lex Machina's judge analytics module is now standard among 60% of AmLaw 200 practices. At the same time, contract-lifecycle agents attract corporate legal departments eager to shorten negotiation cycles, as evidenced by Ironclad's USD 150 million Series F funding. Compliance-intelligence and IP-management agents round out demand, especially in sectors with intensive regulatory duties or large patent estates.

Cloud platforms accounted for 61.89% of revenue in 2025, confirming that most buyers prefer subscription economics and continuous model upgrades. The agentic artificial intelligence in legal and regulatory tech market therefore remains closely tied to hyperscaler GPU availability. However, edge and embedded deployments are growing at a 29.71% CAGR because sensitive data, such as cross-border M&A, must remain within firm firewalls. This shift is expanding the agentic artificial intelligence in the legal and regulatory tech market size for hardware-optimized inference appliances.

Hybrid architectures allow routine work to stay in the cloud while confidential data is processed on-premises, but they also introduce API duplication costs. Large AmLaw firms with legacy document systems often choose on-premises clusters to integrate with existing records. Meanwhile, practice-management vendors embed lightweight LLMs so that small firms can gain agentic features without juggling multiple logins.

Geography Analysis

North America accounted for 41.89% of 2025 revenue for agentic AI in the legal and regulatory tech market. AmLaw 100 firms and Fortune 500 legal operations drive volume through cross-practice rollout of contract lifecycle and compliance agents. Enterprise adoption surged after the US District Court for the Southern District of New York clarified privilege obligations in February 2026. Canada's growth is steadier; Toronto firms favor eDiscovery agents to stay competitive with U.S. counterparts, while Mexico sees uptake mainly among multinational subsidiaries complying with the United States-Mexico-Canada Agreement.

Asia-Pacific is projected to record a 29.91% CAGR through 2031, the fastest worldwide. China's Smart Courts handle more than 30 million cases annually using AI case-routing and sentencing support. Japan's ministry pilots AI-enabled contract review to modernize corporate transactions, while India's digital court projects raise demand for budget-friendly research agents. Singapore's Smart Nation strategy and South Korea's regulatory complexity in semiconductors and finance add further momentum.

Europe trails slightly but benefits from GDPR enforcement and active cross-border M&A, expanding the agentic AI market within the bloc's legal and regulatory tech. Magic Circle firms in London buy orchestration platforms to manage multi-jurisdictional due diligence, while German practices focus on EU AI Act compliance audits. France's start-up scene cultivates contract negotiation agents tuned to civil-law systems. The Middle East, led by the United Arab Emirates and Saudi Arabia, is adopting sovereign-AI mandates to implement compliance and dispute-resolution tools. In Africa, adoption is concentrated in South Africa and Egypt due to infrastructure gaps elsewhere.

- Thomson Reuters Corporation

- RELX PLC

- LexisNexis Legal & Professional

- Harvey AI Inc.

- Ironclad Inc.

- Luminance Technologies Ltd.

- Casetext Inc.

- Everlaw Inc.

- DISCO Inc.

- Relativity ODA LLC

- Icertis Inc.

- ContractPod Technologies Ltd.

- Kira Systems Inc.

- Exterro Inc.

- Reveal-Brainspace Inc.

- Evisort Inc.

- SirionLabs Pte. Ltd.

- LinkSquares Inc.

- SpotDraft Inc.

- Onit Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Mainstream Adoption of GenAI Tools Within Legal Workflows

- 4.2.2 Cost-Reduction Imperatives Amid Rising Outside-Counsel Fees

- 4.2.3 Cloud-First Digital-Transformation Initiatives Across Legal Operations

- 4.2.4 Increasing Regulatory Scrutiny Demanding Audit-Ready Compliance Automation

- 4.2.5 Under-Served Demand for Multi-Agent Orchestration in Cross-Border Matters

- 4.2.6 Emerging VC-Backed Point Solutions Targeting Niche Litigation Tasks

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Privilege Concerns Over Cloud-Hosted LLM Inference

- 4.3.2 Hallucination Liability and Ethical-Competence Obligations for Attorneys

- 4.3.3 Fragmented Legacy Systems Limiting Seamless AI Integration

- 4.3.4 Under-Reported Shortage of Legal-Domain AI Talent for Model Fine-Tuning

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Contract Lifecycle Management Agents

- 5.1.2 eDiscovery and Document Review Agents

- 5.1.3 Legal Research and Analytics Agents

- 5.1.4 Compliance and Regulatory Intelligence Agents

- 5.1.5 Litigation Outcome Prediction Agents

- 5.1.6 IP-Management Agents

- 5.2 By Deployment Model

- 5.2.1 Cloud-based

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.2.4 Edge / Embedded

- 5.3 By End-User Industry

- 5.3.1 Law Firms

- 5.3.2 Corporate Legal Departments

- 5.3.3 Financial-Services Compliance Units

- 5.3.4 Government and Regulatory Bodies

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Insurance

- 5.3.7 Technology and Telecom

- 5.4 By Core Technology

- 5.4.1 Machine-Learning and Predictive Models

- 5.4.2 Rule-based Expert Systems

- 5.4.3 Large-Language-Model (GenAI) Agents

- 5.4.4 Multi-agent Orchestration Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thomson Reuters Corporation

- 6.4.2 RELX PLC

- 6.4.3 LexisNexis Legal & Professional

- 6.4.4 Harvey AI Inc.

- 6.4.5 Ironclad Inc.

- 6.4.6 Luminance Technologies Ltd.

- 6.4.7 Casetext Inc.

- 6.4.8 Everlaw Inc.

- 6.4.9 DISCO Inc.

- 6.4.10 Relativity ODA LLC

- 6.4.11 Icertis Inc.

- 6.4.12 ContractPod Technologies Ltd.

- 6.4.13 Kira Systems Inc.

- 6.4.14 Exterro Inc.

- 6.4.15 Reveal-Brainspace Inc.

- 6.4.16 Evisort Inc.

- 6.4.17 SirionLabs Pte. Ltd.

- 6.4.18 LinkSquares Inc.

- 6.4.19 SpotDraft Inc.

- 6.4.20 Onit Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment