|

시장보고서

상품코드

2061965

시맨틱 레이어 및 지식 그래프 분야 에이전트형 AI : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI In Semantic Layer And Knowledge Graph - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

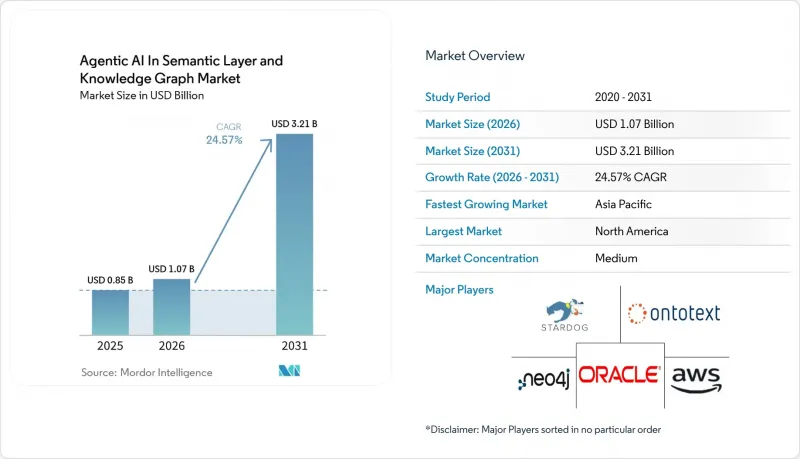

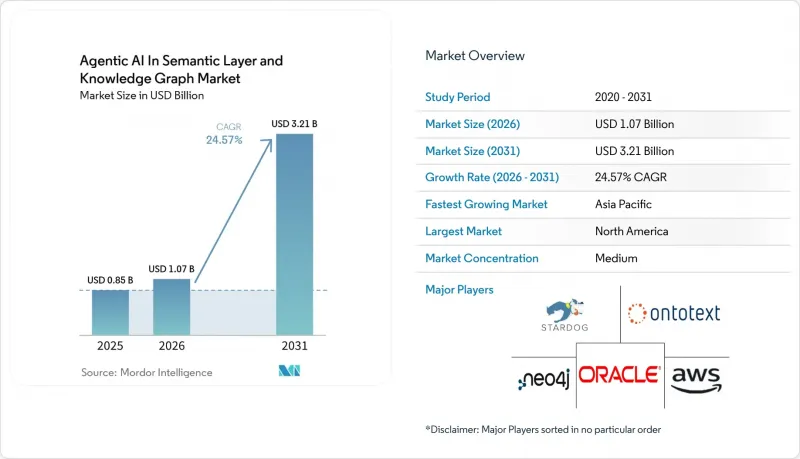

시맨틱 레이어 및 지식 그래프 분야 에이전트형 AI 시장 규모는 2025년 8억 5,000만 달러로 평가되었습니다. 2026년 10억 7,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 24.57%를 나타내, 2031년에는 32억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 지식 그래프의 유형(엔터프라이즈 지식 그래프 등), 용도(고객 및 360도 뷰 분석 등), 도입 형태(클라우드 및 On-Premise), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

시맨틱 레이어 및 지식 그래프 분야 에이전트형 AI 시장 동향과 인사이트

자율적인 워크플로우를 위한 에이전트형 AI의 기업 도입 확대

자율형 에이전트의 기업 도입은 실험 단계를 넘어섰으며, 이러한 변화에 따라 기업 시스템 전체에서 신뢰할 수 있는 기억으로서 기능하는 관리된 의미론적 구조에 대한 수요가 높아지고 있습니다. 시맨틱 레이어 및 지식 그래프용 에이전트형 AI 시장에서 이러한 변화가 중요한 이유는 에이전트가 재무, 업무, 고객 워크플로우의 모든 영역에서 작동하기 위해서는 지속적인 컨텍스트, 명확한 관계성, 추적 가능한 논리가 필요하기 때문입니다. Neo4j는 2026년 2월, AuraDB 고객을 대상으로 온톨로지 기반 자동 에이전트 구축 기능과 호스팅형 MCP 배포 기능을 갖춘 ‘Aura Agent’의 일반 제공을 시작하며, 이러한 동향을 실제 운영 단계로 한 걸음 더 가까이 다가갔습니다. 또한, 마이크로소프트도 2026년 5월, Dataverse Business Skills를 공개 프리뷰로 출시하여 엔터프라이즈 에이전트의 워크플로를 확장했습니다. 이를 통해 조직은 프로세스 및 운영 로직을 Dataverse MCP 서버를 통해 AI 에이전트가 인식할 수 있는 지침으로 인코딩할 수 있게 되었습니다. 이러한 출시 소식은 시맨틱 레이어 및 지식 그래프 분야 에이전트형 AI가 시범 운영이 아닌 실제 운영 환경의 요구에 따라 형성되고 있음을 보여줍니다. 특히, 기업이 여러 시스템에 걸쳐 감사 가능한 에이전트의 조치를 요구하는 경우, 이러한 경향은 두드러집니다.

데이터 레이크에서 시맨틱 데이터 패브릭으로의 전환 가속화

기업들은 수동적인 데이터 레이크에서 점차 벗어나고 있습니다. 왜냐하면, 원시 데이터나 단편화된 데이터 구조로는 에이전트 시스템이 신뢰성 높은 추론을 수행하는 데 필요한, 정책을 고려한 맥락을 제공할 수 없기 때문입니다. 시맨틱 레이어 및 지식 그래프 분야 에이전트형 AI는 이러한 전환의 혜택을 누리고 있습니다. 시맨틱 레이어는 에이전트를 스키마의 복잡성에 노출시키지 않고, 거버넌스가 적용된 해석 가능한 형식으로 기업 데이터를 제시할 수 있기 때문입니다. 마이크로소프트 리서치는 GraphRAG가 86%의 멀티홉 기업 쿼리 정확도를 달성했다고 보고했습니다. 이는 기준이 되는 벡터 RAG의 32%에 비해 높은 수치이며, 기업 AI 아키텍처에서 보다 풍부한 의미적 맥락의 중요성이 높아지고 있는 이유를 설명하는 한 가지 요인이 되고 있습니다. 유럽에서도 AI 거버넌스 규정에 따라 고위험 도입 환경에서 데이터 계보, 기술 문서, 설명 가능한 시스템 동작에 대한 수요가 높아지고 있어, 이러한 방향성이 더욱 강화되고 있습니다. 관련 과학 연구에서는 AI법(AI Act)의 요건과 표준 규격 간의 관계를 개방형 지식 그래프를 기반으로 매핑하는 것의 중요성이 강조되고 있으며, 이는 거버넌스가 제대로 작동하는 엔터프라이즈 AI 환경에서 시맨틱 구조가 수행하는 역할을 더욱 뒷받침해 줍니다.

대규모 지식 그래프 프로젝트의 높은 총 소유 비용

대규모 지식 그래프 프로그램은 인프라, 스키마 설계, 엔티티 해결, 큐레이션, 그리고 지속적인 거버넌스에 드는 비용이 소프트웨어 구매 결정에 드는 비용을 훨씬 초과하기 때문에 여전히 높은 소유 비용을 수반합니다. 시맨틱 계층 및 지식 그래프용 에이전트형 AI 시장에서 이러한 비용 압박은 그래프 기반 에이전트가 필요하지만 대규모 전문 팀이나 다단계 도입 프로그램을 도입하기에는 여력이 부족한 중견 기업들에게 특히 중요한 과제입니다. 벤더의 제품 설계를 통해 시장이 이러한 부담을 줄이려고 노력하고 있음을 알 수 있습니다. 예를 들어, Neo4j는 2025년 12월, 클라우드, 하이브리드, On-Premise 그래프 배포를 통합적으로 관리하는 제어 플레인으로서 ‘Fleet Manager’를 출시했습니다. 하이퍼스케일러가 제공하는 관리형 서비스 역시 운영상의 부담을 줄여주고 있습니다. 예를 들어, AWS는 Neptune Analytics를 지속적으로 확장하며, 원래라면 고객 측에서 직접 엔지니어링 작업을 수행해야 할 법한 기능을 추가하고 있습니다. 이러한 개선이 있었음에도 불구하고, 시맨틱 레이어 및 지식 그래프에 에이전트형 AI를 도입하는 속도는 여전히 더딘 편이며, 구매자들은 온톨로지 엔지니어링과 그래프의 최신성 유지를 일회성 프로젝트 과제가 아닌 장기적인 비용 센터로 간주하고 있습니다.

부문별 분석

2025년에는 소프트웨어가 매출의 62.87%를 차지하며, 전체 구성 요소에서 주도적인 위치를 유지했습니다. 이 비율은 엔터프라이즈 그래프가 운영상 유용해지기 전에 구축되어야 하는 플랫폼 라이선스, 쿼리 엔진, 온톨로지 관리 도구 및 내장 벡터 검색 기능의 비용을 반영한 것입니다. 시맨틱 계층 및 지식 그래프용 에이전틱 AI 시장에서도 여전히 많은 도입 사례가 맞춤형 스키마 설계나 통합 작업에서 시작되기 때문에 소프트웨어는 고도의 맞춤형 요구 사항 덕분에 혜택을 누리고 있었습니다. 따라서 초기 수익 구조는 보다 광범위한 서비스 생태계가 성숙하기 전에 핵심적인 그래프 인프라를 제공할 수 있는 플랫폼 공급업체에게 유리하게 작용했습니다.

서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 24.97%를 나타낼 것으로 예측되며, 이는 구매자들이 플랫폼을 구매한 후 구현 지원에 대해 점점 더 많은 비용을 지불하고 있음을 보여줍니다. 시맨틱 레이어 및 지식 그래프 업계의 에이전트형 AI 분야에서 이러한 변화는 스키마 설계, 엔티티 해결, 거버넌스 설정, 운영 모니터링이 데이터베이스 설치 자체보다 더 많은 시간이 소요된다는 현실적인 사정과 밀접한 관련이 있습니다. Neo4j가 2025년 12월에 출시한 ‘Fleet Manager’는 클라우드, 하이브리드, On-Premise 환경 전반에 걸친 라이프사이클 관리를 용이하게 하려는 요구를 반영한 것입니다. 또한 Databricks는 2026년 4월 Unity Catalog Business Semantics의 일반 제공을 시작하고, Open Semantic Interchange 이니셔티브에 참여함으로써 서비스 기회를 확대했습니다. 다만, 이를 위해서는 여전히 고객 환경 내에서 통합 작업이 필요합니다. 그 결과, 시맨틱 계층 및 지식 그래프 시장에서 에이전트형 AI는 기업들이 그래프 플랫폼을 거버넌스가 적용된 실제 운영 시스템으로 전환하기 위해 외부 지원을 요청함에 따라, 해당 서비스가 계속해서 급속히 성장할 가능성이 높다고 볼 수 있습니다.

2025년 기준으로 엔터프라이즈 지식 그래프는 시장 가치의 46.21%를 차지하며, 가장 큰 비중을 차지하는 지식 그래프 유형이 되었습니다. 이 지위는 ERP 데이터, 고객 프로파일, 제품 카탈로그, 거래 내역 등 자체 데이터를 단일 관계 구조를 인식하는 체계로 통합해야 했던 대기업들에 의해 만들어졌습니다. 에이전트형 AI 분야 중 시맨틱 레이어 및 지식 그래프 시장에서 엔터프라이즈 지식 그래프는 공개 웹 데이터만으로는 처리할 수 없는 내부 자산에 대한 추론을 지원하기 때문에 가치가 높은 것으로 평가받고 있습니다. 이러한 우위는 대기업이 자율형 에이전트를 광범위하게 도입하기 전에, 파편화된 시스템을 연동시키는 데 대한 유인이 더 크다는 사실도 반영하고 있습니다.

웹 규모의 지식 그래프는 2031년까지 연평균 성장률(CAGR) 25.17%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 유형으로 꼽히고 있습니다. 이러한 성장 추세는 엔티티 해결, 중복 제거 및 관계 추론이 매우 방대한 공개 및 준공개 정보 풀 전체에서 작동해야 하는 인터넷용 이용 사례와 밀접한 관련이 있습니다. 2025년 9월 Neo4j가 발표한 Infinigraph는 그래프 네이티브 환경에서 100TB 이상의 배포와 수십억 개의 임베디드 벡터를 지원함으로써, 해당 벤더가 이러한 규모에 어떻게 대비하고 있는지를 보여주었습니다. 클라우드 플랫폼에 대한 지원도 중요한 요소입니다. AWS와 Microsoft는 2025년부터 2026년에 걸쳐 관리형 그래프 기능을 지속적으로 확대하고 있으며, 이를 통해 매우 대규모의 그래프 워크로드에서 인프라의 부담이 경감되기 때문입니다. 이러한 조합 덕분에 엔터프라이즈 그래프는 현재도 주도적인 위치를 유지하고 있지만, 고객 대상의 검색, 추천, 추론 워크로드가 확대됨에 따라 웹 스케일 그래프도 그 세력을 넓혀가고 있습니다.

지역별 분석

2025년, 북미는 시맨틱 레이어 및 지식 그래프 분야에서 에이전트형 AI 시장 점유율의 41.63%를 차지했으며, 기업의 AI 투자 집중, 성숙한 벤더 기반, 그리고 BFSI(은행 및 금융 및 보험) 및 기술 분야의 이용 사례에 대한 조기 도입을 통해 주도적인 위치를 유지했습니다. 미국은 그래프 기반 AI 도구 및 관리형 그래프 플랫폼에 대한 투자에서 주도적인 역할을 수행했으며, 캐나다는 금융 서비스 및 헬스케어 분야에서의 도입을 통해 기여했습니다. 멕시코는 여전히 도입 초기 단계에 있었습니다. 2025년과 2026년에 마이크로소프트의 ‘Graph in Fabric’, Databricks의 시맨틱 레이어 확장, Neo4j의 플랫폼 출시와 같은 주요 제품 발표가 시장을 더욱 견인했습니다.

규모 면에서 2위를 차지하는 유럽에서는 자동차, 금융 서비스 및 공공 부문의 AI 거버넌스 프로그램에 대한 수요가 증가하는 추세를 보였습니다. 독일, 영국, 프랑스는 규제 환경 하에서 운영 데이터의 연계 및 설명 가능성에 대한 인센티브가 강했기 때문에 시장을 주도했습니다. 유럽연합(EU)의 AI법은 데이터 거버넌스 및 규정 준수 분야에서 시맨틱 레이어와 지식 그래프의 중요성을 부각시켰습니다. 이탈리아와 스페인은 금융 서비스의 자동화 및 공공 부문의 디지털 전환을 통해 기여했으나, 그 규모는 서유럽의 주요 시장에 비해 작았습니다.

아시아태평양은 중국, 인도, 한국, 일본의 디지털 전환 프로그램과 기업 및 공공 AI 시스템에서 시맨틱 추론의 활용 확대에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 25.52%를 기록하며 성장할 것으로 전망됩니다. AWS는 2025년에 뭄바이로, 2026년에는 여러 거점으로 Neptune Analytics를 확장함으로써 해당 지역에 대한 접근성을 높이고, 관리형 그래프 배포와 관련된 인프라 격차를 해소했습니다. 중동에서는 AI 분야에서의 입지가 강화되고 있으며, UAE와 사우디아라비아는 시민 데이터 통합 및 공공 서비스 분야의 AI 이니셔티브에 주력하고 있습니다. 남미와 아프리카는 여전히 소규모 시장이지만, 브라질, 남아프리카공화국, 이집트에서는 인력과 비용상의 제약이 있음에도 불구하고 금융 서비스 및 통신 분야에서의 활동이 활발해지고 있습니다. 이러한 지역에서는 서비스 주도형 도입 모델이 계속해서 중요할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the agentic AI market in the semantic layer and knowledge graph market size is expected to grow from USD 0.85 billion in 2025 to USD 1.07 billion in 2026, and is forecast to reach USD 3.21 billion by 2031 at a 24.57% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Knowledge-Graph Type (Enterprise Knowledge Graph, and More), Application (Customer and 360-View Analytics, and More ), Deployment Mode (Cloud, and On-Premises), End-User Industry (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Semantic Layer And Knowledge Graph Market Trends and Insights

Rising Enterprise Adoption of Agentic AI for Autonomous Workflows

Enterprise adoption of autonomous agents has moved beyond experimentation, and that shift is increasing demand for governed semantic structures that can serve as reliable memory across enterprise systems. In the agentic AI market for the semantic layer and knowledge graph, this change matters because agents need persistent context, clear relationships, and traceable logic before they can operate across finance, operations, and customer workflows. Neo4j moved this trend closer to production in February 2026 when it launched Aura Agent in general availability with automated ontology-driven agent construction and hosted MCP deployment for AuraDB customers. Microsoft also extended enterprise agent workflows in May 2026 by introducing Dataverse Business Skills into public preview, enabling organizations to encode processes and operational logic as instructions discoverable by AI agents via the Dataverse MCP server. These launches show why the agentic AI in the semantic layer and knowledge graph market is being shaped by production needs rather than pilot activity, especially where enterprises want auditable agent actions across many systems.

Accelerating Shift from Data Lakes to Semantic Data Fabrics

Enterprises are moving away from passive data lakes because raw and disconnected data structures do not provide the policy-aware context that agent systems need for dependable reasoning. The agentic AI in the semantic layer and knowledge graph market is benefiting from that shift because semantic layers can present enterprise data in a governed, interpretable form, rather than exposing agents to schema complexity. Microsoft Research reported that GraphRAG achieved 86% multi-hop enterprise query accuracy, compared with 32% for the baseline vector RAG, which helps explain why richer semantic context is gaining priority in enterprise AI architecture. Europe is also reinforcing this direction because AI governance rules are increasing the need for data lineage, technical documentation, and explainable system behavior in high-risk deployments. A related scientific study argued for open knowledge graph-based mapping between AI Act requirements and standards, which further supports the role of semantic structures in governed enterprise AI environments.

High Total Cost of Ownership for Large-Scale Knowledge Graph Projects

Large-scale knowledge graph programs still carry a high ownership burden because infrastructure, schema design, entity resolution, curation, and ongoing governance costs extend far beyond software purchase decisions. In the agentic AI market for the semantic layer and knowledge graph, this cost pressure is especially relevant for mid-sized organizations that may want graph-grounded agents but cannot justify large specialist teams or multi-stage implementation programs. Vendor product design shows that the market is trying to reduce this burden, with Neo4j launching Fleet Manager in December 2025 as a unified control plane for cloud, hybrid, and on-premises graph deployments. Hyperscaler-managed services are also reducing some operational overhead, as AWS continues to expand Neptune Analytics and add features that would otherwise require more direct engineering effort from customers. Even with these improvements, the agentic AI in the semantic layer and knowledge graph market still faces slower adoption, where buyers see ontology engineering and graph freshness as long-running cost centers rather than one-time project tasks.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Availability of Vector-Enabled Graph Databases

- Surging Demand for Real-Time 360-View Customer Analytics In BFSI

- Shortage of Qualified Knowledge Graph Engineers and Ontologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 62.87% of revenue in 2025, maintaining its leading position across the component mix. That weighting reflected the cost of platform licensing, query engines, ontology management tools, and embedded vector search capabilities that must be in place before an enterprise graph becomes operationally useful. In the agentic AI market for the semantic layer and knowledge graph, software also benefited from heavy customization requirements, as many deployments still begin with tailored schema design and integration work. The early revenue mix, therefore, favored platform vendors that could supply core graph infrastructure before broader service ecosystems matured.

Services are projected to grow at a 24.97% CAGR from 2026 to 2031, indicating that buyers are increasingly paying for implementation support after platform purchase. In the agentic AI in the semantic layer and knowledge graph industry, this shift is tied to the practical reality that schema design, entity resolution, governance setup, and operational monitoring take longer than database installation alone. Neo4j's December 2025 launch of Fleet Manager reflected this need for easier lifecycle management across cloud, hybrid, and on-premises estates. Databricks also widened the service opportunity in April 2026 when it pushed Unity Catalog Business Semantics into general availability and joined the Open Semantic Interchange initiative, which will still require integration work inside customer environments. As a result, the agentic AI in the continue to seethe semantic layer and knowledge graph market is likely to continue to see services grow quickly as enterprises seek outside help to turn graph platforms into governed production systems.

Enterprise knowledge graphs accounted for 46.21% of the market value in 2025, making them the largest knowledge graph type. This position came from large organizations that needed to unify proprietary records, such as ERP data, customer profiles, product catalogs, and transaction histories, into a single, relationship-aware structure. In the agentic AI space, in the semantic layer and knowledge graph market, enterprise knowledge graphs are valuable because they support reasoning over internal assets that cannot be handled with open web data alone. Their lead also reflects the fact that large enterprises have stronger incentives to connect fragmented systems before they deploy autonomous agents widely.

Web-scale knowledge graphs are projected to grow at a 25.17% CAGR through 2031, which makes them the fastest-growing type. The growth path is tied to internet-facing use cases where entity resolution, deduplication, and relationship inference must operate across very large pools of public and semi-public information. Neo4j's Infinigraph launch in September 2025 showed how vendors are preparing for this scale by supporting 100TB+ deployments and billions of embedded vectors in a graph-native environment. Cloud platform support also matters here, because AWS and Microsoft continued to expand managed graph capabilities through 2025 and 2026, which lowers some of the infrastructure burden for very large graph workloads. That combination keeps enterprise graphs in the lead today, while web-scale graphs gain momentum as customer-facing search, recommendation, and reasoning workloads expand.

Geography Analysis

North America held 41.63% of the agentic AI market share in the semantic layer and knowledge graph market in 2025, maintaining its lead due to concentrated enterprise AI investment, a mature vendor base, and early adoption across BFSI and technology use cases. The United States led with investments in graph-grounded AI tools and managed graph platforms, while Canada contributed through financial services and healthcare adoption. Mexico remained in an earlier deployment phase. Key product launches, including Microsoft's Graph in Fabric, Databricks' expansion of its semantic layer, and Neo4j's platform releases in 2025 and 2026, further supported the market.

Europe, the second-largest region, saw demand growth in automotive, financial services, and public-sector AI governance programs. Germany, the United Kingdom, and France led due to stronger incentives for operational data linkage and explainability in regulated environments. The European Union AI Act heightened the importance of semantic layers and knowledge graphs for data governance and compliance.Italy and Spain contributed through financial services automation and public digital transformation, though on a smaller scale than leading Western European markets.

Asia-Pacific is projected to grow at a 25.52% CAGR from 2026 to 2031, driven by digital transformation programs and increased use of semantic reasoning in enterprise and public AI systems in China, India, South Korea, and Japan. AWS expanded regional access by extending Neptune Analytics to Mumbai in 2025 and additional locations in 2026, addressing infrastructure gaps for managed graph deployment. The Middle East is gaining prominence in AI, with the UAE and Saudi Arabia focusing on citizen data integration and public service AI initiatives. South America and Africa remain smaller markets, but Brazil, South Africa, and Egypt are building activity in financial services and telecommunications, despite talent and cost constraints. Service-led implementation models are likely to remain critical in these regions.

- Amazon.com, Inc. (AWS)

- Neo4j, Inc.

- Oracle Corporation

- Stardog Union, Inc.

- Ontotext AD

- TigerGraph, Inc.

- IBM Corporation

- Google LLC

- Microsoft Corporation

- SAP SE

- Databricks, Inc.

- DataStax, Inc.

- GraphAware Limited

- TerminusDB

- ArangoDB GmbH

- Franz Inc.

- PoolParty (Semantic Web Company GmbH)

- Expert.ai S.p.A.

- RelationalAI, Inc.

- Cambridge Semantics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Shift from Data Lakes to Semantic Data Fabrics

- 4.2.2 Rising Enterprise Adoption of Agentic AI For Autonomous Workflows

- 4.2.3 Regulatory Push for Explainable AI In Critical Industries

- 4.2.4 Mainstream Availability of Vector-Enabled Graph Databases

- 4.2.5 Surging Demand for Real-Time 360-View Customer Analytics In BFSI

- 4.2.6 Emergence of AI-Native Knowledge Agents in Developer Toolchains

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for Large-Scale Knowledge Graph Projects

- 4.3.2 Shortage of Qualified Knowledge Graph Engineers and Ontologists

- 4.3.3 Data Sovereignty Concerns in Cross-Border Knowledge Integration

- 4.3.4 Interoperability Gaps Among Heterogeneous Graph Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Knowledge-Graph Type

- 5.2.1 Enterprise Knowledge Graph

- 5.2.2 Domain-Specific Knowledge Graph

- 5.2.3 Web-Scale Knowledge Graph

- 5.3 By Application

- 5.3.1 Customer and 360-View Analytics

- 5.3.2 Fraud Detection and Risk Management

- 5.3.3 Recommendation and Personalization Engines

- 5.3.4 Conversational / Agentic AI Assistants

- 5.3.5 Knowledge Discovery and Research

- 5.4 By Deployment Mode

- 5.4.1 Cloud

- 5.4.2 On-Premises

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and E-Commerce

- 5.5.4 Manufacturing and Supply-Chain

- 5.5.5 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon.com, Inc. (AWS)

- 6.4.2 Neo4j, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 Stardog Union, Inc.

- 6.4.5 Ontotext AD

- 6.4.6 TigerGraph, Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Google LLC

- 6.4.9 Microsoft Corporation

- 6.4.10 SAP SE

- 6.4.11 Databricks, Inc.

- 6.4.12 DataStax, Inc.

- 6.4.13 GraphAware Limited

- 6.4.14 TerminusDB

- 6.4.15 ArangoDB GmbH

- 6.4.16 Franz Inc.

- 6.4.17 PoolParty (Semantic Web Company GmbH)

- 6.4.18 Expert.ai S.p.A.

- 6.4.19 RelationalAI, Inc.

- 6.4.20 Cambridge Semantics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment