|

시장보고서

상품코드

2061966

항공기용 펌프 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

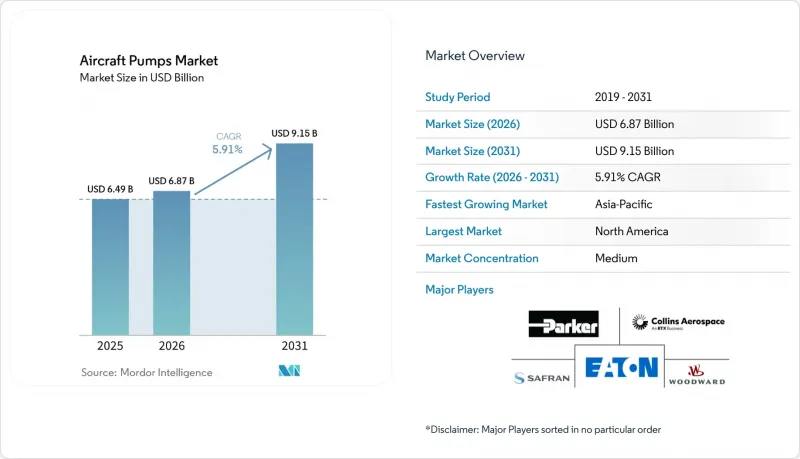

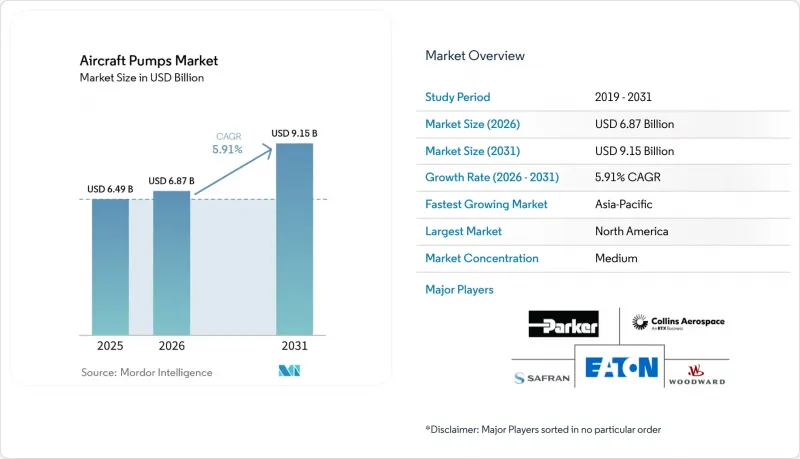

Mordor Intelligence에 의하면, 항공기용 펌프 시장 규모는 2025년 64억 9,000만 달러로 평가되었습니다. 2026년에는 68억 7,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 5.91%를 나타내, 2031년까지 91억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 펌프의 유형(연료 펌프, 유압 펌프 등), 구동 방식(엔진 구동, 전동기 구동, 공기 구동 등), 정격 압력(1,500 PSI 미만, 1,500-3,000 PSI, 3,000 PSI 이상), 항공기 유형(민간 항공, 군용 항공 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공기용 펌프 시장 동향 및 분석

항공기 시스템의 전동화

항공기용 펌프 시장은 점차 전기화되는 항공기 구조로의 꾸준한 전환에 따라 재편되고 있습니다. 이는 공급업체가 과거에는 엔진 구동 아키텍처와 밀접하게 연결되어 있던 기능을 지원해야 할 필요가 생겼기 때문입니다. 항공기용 펌프 시장의 이 분야에서는 보조 동력, 냉각 및 2차 유압 용도에서 추가적인 하드웨어 비용보다 우수한 제어성과 서브시스템의 독립성이 중시되기 때문에 전동 모터 구동 펌프가 점차 보급되고 있습니다. 리프헬(Leupheld)사가 FAUST 연구 프로그램의 일환으로 추진 중인 이 프로젝트는 분리형 유압 발전 시스템을 직접 대상으로 하고 있으며, 향후 중·단거리 플랫폼의 설계 논리가 어떻게 변화하고 있는지를 입증한다는 점에서 중요합니다. 또한, 항공기용 펌프 시장은 전동 구동 어셈블리가 펌프 기능, 제어 기능 및 로컬 전력 관리 기능을 단일 패키지로 통합함으로써, 유닛당 부가가치를 높일 수 있다는 점에서도 혜택을 보고 있습니다. 이 설계 기법이 성숙해짐에 따라, 항공기용 펌프 시장에서는 기존 제품을 단순히 1대1로 대체하는 것이 아니라, 부가가치가 더 높은 어셈블리로 구성 비율이 전환될 것으로 예측됩니다.

민간 항공기 인도 급증

민간 항공기 기단의 확대로 인해 항공기용 펌프 시장은 계속해서 단기적인 수요의 지지를 받고 있습니다. 왜냐하면 신규 항공기의 인도는 즉각적인 라인 핏 수요를 창출할 뿐만 아니라, 향후 정비 수요의 씨앗이 되기 때문입니다. 에어버스는 2025년에 91개 고객사에 793대의 항공기를 인도하여 전년 대비 4% 증가했습니다. 또한, 연말 기준 8,754대의 미인도 주문량은 협폭기 및 광폭기 각 프로그램에 걸쳐 항공기용 펌프 시장에 확실한 생산 기반을 제공합니다. 이 미결 주문이 중요한 이유는 연료, 유압, 윤활, 냉각용 펌프가 항공기 제조 주기와 밀접하게 연관되어 있는 반면, 그 수익원은 최초 탑재 시점을 훨씬 넘어 지속되기 때문입니다. 또한, 항공기용 펌프 시장은 협폭기 기단의 운용 특성 덕분에 혜택을 보고 있습니다. 단거리 노선의 반복 운항은 유체 처리 시스템에 심한 마모를 초래하며, 이러한 항공기의 운항 시간이 누적됨에 따라 정비 수요가 증가하기 때문입니다. 이러한 생산 및 사용 패턴은 OEM 및 애프터마켓 활동을 모두 강화하고 있으며, 민간 항공은 현재 예측 기간 동안 가장 확실한 수요의 주축이 되고 있습니다. OEM의 막대한 미결 주문이 계속해서 납품으로 전환되는 한, 공급망에 다소의 마찰이 남아 있다 하더라도 항공기용 펌프 시장은 안정적인 수요 전망을 유지할 수 있을 것입니다.

높은 인증 및 규정 준수 비용

항공기용 펌프 시장은 신규 시장 진출기업에게 여전히 진입이 어려운 시장입니다. 그 이유는 인증 및 지속적인 규정 준수를 위해서는 장기간에 걸친 시험 주기, 상세한 문서화, 그리고 플랫폼 고유의 품질 관리 체제가 필요하기 때문입니다. 이러한 제약은 항공기용 펌프 시장 전체에 있어 중요한 의미를 지닙니다. 왜냐하면 부품 공급업체는 민간기나 군용기에 채택되기 전에, 엄격한 항공 적합성 규정에 따라 재현 가능한 성능을 입증해야 하기 때문입니다. GE 항공 체코의 터보프롭 엔진에 대한 FAA의 2025년 감항 지침은 규제 조치가 어떻게 검사, 보고 및 정비 요건을 초래하며, 이러한 요건들이 사업자와 공급업체에게 일반적인 프로그램 계획 범위를 벗어난 부담이 되는지를 보여줍니다. 공급업체가 일단 승인을 획득하면, 이러한 비용은 기존 기업을 보호하는 장벽이 되지만, 바로 그 부담이 신규 진입을 지연시켜 항공기용 펌프 시장의 집중 상태를 유지하게 됩니다. 문제는 첫 승인뿐만이 아닙니다. 구성 변경, 재료 변경 또는 공정 변경이 있을 때마다 추가 작업이나 인증 절차가 발생할 수 있습니다. 그 결과, 항공기용 펌프 시장에서는 가격 경쟁에만 의존하는 기업보다, 규제에 관한 풍부한 경험과 폭넓은 도입 실적을 보유한 기업이 우대받는 경향이 있습니다.

부문별 분석

2025년, 연료 펌프는 매출의 42.45%를 차지하여 부문별 구성에서 가장 큰 비중을 차지했을 뿐만 아니라, 전 세계 항공기용 펌프 시장 점유율의 42.45%를 차지했습니다. 이 지위는 추진 및 연료 관리 기능 전반에서 연료 펌프가 수행하는 필수적인 역할을 반영하며, 교체 수요를 지속적으로 유지하는 대량 생산형 협폭기체 프로그램 덕분에 그중요성이 더욱 부각되고 있습니다. 에어버스는 2025년에 A320 계열 항공기 607대를 인도했는데, 이는 단기 운항 주기가 도입된 기체 전체에 걸쳐 연료 펌프에 대한 지속적인 수요를 뒷받침하고 있음을 보여줍니다. 센서 관련 조사에서도 압력 및 온도 부하 증가에 따라 항공기용 연료 펌프에 대한 모니터링 수요가 높아지고 있는 것으로 나타나고 있으며, 이는 해당 부문이 항공기용 펌프 시장의 OEM 및 애프터마켓 활동 모두에서 여전히 중심적인 위치를 차지하고 있다는 견해를 뒷받침하고 있습니다. 실용적인 관점에서 볼 때, 추진계 관련 부품은 장기간의 가동 중단을 허용할 수 없기 때문에 항공기용 펌프 시장에서 연료 펌프는 기체 신뢰성의 핵심적인 역할을 계속해서 담당하고 있습니다.

유압 펌프는 가장 빠르게 성장하는 부문으로, 2031년까지 연평균 성장률(CAGR)이 7.75%를 나타낼 것으로 예측됩니다. 고압 비행 제어 시스템 및 방위 분야의 업그레이드가 수요를 견인하고 있어, 항공기용 펌프 시장에서 이 분야의 규모는 계속해서 확대되고 있습니다. 또한, 대형 민간 및 군용 플랫폼에서 유압 시스템이 착륙 장치, 브레이크, 작동 장치 및 유틸리티 시스템에 깊이 통합되어 있다는 사실 또한 항공기용 펌프 업계에 호재가 되고 있습니다. 이튼사의 FLRAA 수주는 이러한 견해를 뒷받침합니다. 이 프로그램에는 차세대 회전익기 플랫폼용 유압 발전 및 전송 시스템이 포함되어 있기 때문입니다. 윤활 펌프는 여전히 엔진 출력과 정비 수요에 따라 움직이고 있지만, 전기화 수준이 높아진 아키텍처에서 열 관리에 대한 필요성이 커짐에 따라 냉각 펌프의 중요성이 커지고 있습니다. 다른 펌프 부문은 규모가 여전히 작지만, 객실, 유틸리티 및 특수 서브시스템의 기능을 위해서는 소량이라도 인증된 부품이 필요하기 때문에 항공기용 펌프 시장에서 여전히 중요한 위치를 차지하고 있습니다.

2025년에는 엔진 구동 시스템이 매출의 45.35%를 차지하며, 항공기용 펌프 시장의 주요 구성 요소가 되었습니다. 이는 현존하는 기체가 여전히 집중형 유압 발생 장치에 크게 의존하고 있기 때문입니다. 항공기의 레이아웃, 정비 절차 및 인증 역사가 수십 년에 걸쳐 이를 중심으로 구축되어 왔기 때문에 그 위상은 여전히 확고하며, 이로 인해 항공기용 펌프 시장 전체의 전환 비용이 높아지고 있습니다. 공기 구동식 펌프는 특정 기종에서 여전히 보조 및 비상 시의 역할을 담당하고 있으며, RAT(기내 공조 장치) 구동 유닛은 수송기에서 최후의 수단으로서 유압원을 제공하는 필수적인 존재입니다. 수동 펌프는 소규모 범주에 속하지만, 여전히 간편성이 중시되는 일반 항공 및 정비 분야에서 계속해서 활용되고 있습니다.

전기 펌프 시장은 2031년까지 연평균 성장률(CAGR) 8.37%를 나타낼 것으로 예측되며, 이 부문은 새로운 시스템 아키텍처에 따른 항공기용 펌프 시장에서 가장 뚜렷한 성장 분야 중 하나로 꼽히고 있습니다. 항공기용 펌프 시장이 이러한 방향으로 나아가고 있는 것은 분산형 전원 및 로컬 제어가 더욱 전동화된 항공기의 목표와 잘 부합하기 때문입니다. 특히, 엔진으로부터 분리됨으로써 유연성이 향상되는 하위 시스템에서 이러한 경향은 두드러집니다. 리프헬(Leupheld)사의 고효율 파워팩과 관련된 ‘FAUST’ 프로젝트는 이러한 변화를 직접적으로 뒷받침하는 것으로, 공급업체들이 이미 엔진 연동식 유압 발전 시스템에 대한 의존도가 낮은 항공기를 위해 준비를 진행하고 있음을 보여줍니다. 액추에이터에 대한 연구는 전기정수압(electro-hydrostatic) 개념이 출력 밀도와 열 성능을 어떻게 향상시킬 수 있는지를 보여줌으로써 기술적 근거를 제시하고 있으며, 이것이 항공기용 펌프 시장에서 전동 구동 펌프 어셈블리가 주목받고 있는 이유 중 하나입니다. 그렇긴 하지만, 변화의 속도는 플랫폼에 따라 다르며, 예측 기간의 대부분 동안 항공기용 펌프 시장에서는 엔진 구동 시스템과 전기 구동 시스템이 병행하여 존재할 가능성이 높습니다.

지역별 분석

2025년 기준으로 북미는 매출의 44.68%를 차지하며, 항공기용 펌프 시장에서 가장 규모가 큰 지역이자 OEM, 방위, MRO 활동 전반에 걸쳐 가장 광범위한 도입 기반을 보유했습니다. 북미의 항공기용 펌프 시장이 견조한 성장세를 유지하고 있는 것은 해당 지역이 주요 항공기 프로그램, 견고한 공급망, 확립된 인증 역량을 단일 생태계 내에 통합하고 있기 때문입니다. 방위 수요는 더욱 확고한 기반을 마련해 주고 있으며, 이튼(Eaton)사의 FLRAA(비행 지원 항공기) 분야에서의 역할은 미국의 첨단 프로그램들이 유압 발전 및 전송 시스템에 대한 수요를 지속적으로 창출하고 있음을 보여줍니다. 또한, 항공사, 군 운영사, 정비 업체 모두가 긴 서비스 주기에 걸쳐 승인된 펌프 지원에 의존하고 있기 때문에 해당 지역은 대규모 애프터마켓 인프라의 혜택도 누리고 있습니다. 이러한 조합 덕분에, 프로그램마다 생산 속도나 방위 관련 일정이 다르더라도 북미는 항공기용 펌프 시장의 중심지로서의 위치를 계속 유지하고 있습니다.

2025년 기준으로 유럽은 지역별 시장 규모에서 2위를 차지했으며, 이 지역의 항공기용 펌프 시장은 에어버스의 생산 활동과 견고한 서브시스템 공급업체 기반에 힘입어 성장하고 있습니다. 에어버스의 2025년 인도 실적은 민간 항공기 생산 분야에서 유럽의 입지를 강화하는 데 기여했으며, 이 회사의 막대한 수주 잔고는 해당 플랫폼 기반과 연계된 펌프 공급업체들에게 향후 라인 핏 수요를 전망할 수 있는 여건을 유지하고 있습니다. 또한, 각 공급업체들이 차세대 아키텍처를 향해 적극적으로 준비를 진행하고 있다는 점에서도 유럽은 항공기용 펌프 시장에서 중요한 위치를 차지하고 있습니다. Leupold사가 FAUST 및 TiReGo 프로그램에 참여하고 있다는 사실은 분리형 유압 파워팩 및 재료 사이클 개선을 위한 집중적인 노력을 보여줍니다. 이러한 노력은 단기적인 생산 수요와, 전기화가 더욱 진전되고 재료 효율이 높은 레이아웃을 지향하는 항공기 서브시스템의 장기적인 재설계를 모두 뒷받침하기 때문에 중요한 의미를 지닙니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.23%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 지역 부문이 되어 항공기용 펌프 시장 규모 확대에 크게 기여하고 있습니다. 아시아태평양의 항공기용 펌프 시장은 민간 항공기 대수 증가, 현지 플랫폼 개발에 대한 의지, 그리고 여러 국가의 방위 조달에 힘입어 성장하고 있습니다. 일본은 민간 및 방위 수요에 더해 수소 관련 항공기 개발에 대한 관심도 함께 가지고 있어 전략적 중요성이 커지고 있습니다. 한편, 광역적인 지역 전체에서는 항공기 수 증가에 따라 정비 거점이 확대되고 있는 점이 호재로 작용하고 있습니다. 남미는 여전히 규모는 작지만, 확립된 항공우주 프로그램과 연계된 항공기 생산 및 서비스 활동을 통해 지역으로서의 기여도를 유지하고 있습니다. 중동 및 아프리카도 활발한 군용기 운용과 항공 수송의 확대를 통해 수요를 끌어올리고 있습니다. 다만, 이 지역의 항공기용 펌프 시장 내 프로젝트 시기는 북미나 유럽에 비해 예산 주기의 영향을 받기 쉬운 경향이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the aircraft pumps market size is expected to grow from USD 6.49 billion in 2025 to USD 6.87 billion in 2026 and is forecast to reach USD 9.15 billion by 2031 at 5.91% CAGR over 2026-2031.

This report is Segmented by Pump Type (Fuel Pumps, Hydraulic Pumps, and More), Drive Mechanism (Engine-Driven, Electric Motor-Driven, Air-Driven, and More), Pressure Rating (Below 1, 500 Psi, 1, 500 To 3, 000 Psi, and Above 3, 000 Psi), Aircraft Type (Commercial Aviation, Military Aviation, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Pumps Market Trends and Insights

Electrification of Aircraft Systems

The aircraft pumps market is being reshaped by a steady shift toward more-electric aircraft layouts, as suppliers now need to support functions that were once closely tied to engine-driven architectures. In this part of the aircraft pumps market, electric motor-driven pumps are gaining ground in auxiliary power, cooling, and secondary hydraulic applications where better control and subsystem independence matter more than the added hardware cost. Liebherr's work under the FAUST research program is important because it directly targets decoupled hydraulic power generation, demonstrating how the design logic is changing for future short- and medium-haul platforms. The aircraft pumps market also benefits from the fact that electric-drive assemblies can deliver greater value per unit when they combine pumping, control, and local power management into a single package. As this design path matures, the aircraft pumps market is likely to see a mix shift toward higher-value assemblies rather than a simple one-for-one replacement of conventional products.

Surge in Commercial Aircraft Deliveries

The aircraft pumps market continues to draw near-term volume support from commercial fleet expansion, because every new aircraft delivery creates immediate linefit demand and also seeds future maintenance demand. Airbus delivered 793 aircraft to 91 customers in 2025, a 4% increase from the prior year, and its year-end backlog of 8,754 aircraft provides the aircraft pumps market with a visible production base across narrowbody and widebody programs. That backlog matters because fuel, hydraulic, lubrication, and cooling pumps are tied to the aircraft build cycle, yet their revenue stream extends far beyond first installation. The aircraft pumps market also benefits from the operating profile of narrowbody fleets, as repeated short-haul cycles create heavy wear on fluid-handling systems and increase overhaul demand as these aircraft accumulate service hours. This production and usage pattern strengthens both OEM and aftermarket activity, making commercial aviation the clearest volume anchor in the current forecast period. As long as large OEM backlogs continue to convert into deliveries, the aircraft pumps market should retain steady demand visibility, even with some supply chain friction remaining.

High Certification and Compliance Costs

The aircraft pumps market remains difficult for new entrants because certification and ongoing compliance require long test cycles, detailed documentation, and platform-specific quality discipline. This constraint matters across the aircraft pumps market because component suppliers must show repeatable performance under strict airworthiness rules before they can win approved content on commercial or military aircraft. The FAA's 2025 airworthiness directive for GE Aviation Czech turboprop engines illustrates how regulatory action can trigger inspection, reporting, and maintenance requirements that operators and suppliers must absorb outside normal program planning. Once a supplier has approvals in place, those costs become a barrier that protects incumbents, but the same burden slows new participation and keeps the aircraft pumps market concentrated. The issue is not only the first approval; every configuration change, material change, or process change can create additional work and qualification steps. As a result, the aircraft pumps market often rewards companies with deep regulatory experience and broad installed portfolios rather than firms that compete only on price.

Other drivers and restraints analyzed in the detailed report include:

- Military Fleet Modernization

- Predictive Maintenance Deployment

- Electromechanical Actuation Replacing Hydraulics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel pumps accounted for 42.45% of revenue in 2025, giving them the largest position in the segment mix and 42.45% of the global aircraft pumps market share. This position reflects their essential role across propulsion and fuel management functions, and it is reinforced by high-volume narrowbody programs that keep replacement demand active. Airbus delivered 607 aircraft from the A320 family in 2025, which shows why short-cycle commercial operations continue to sustain recurring fuel pump demand across the installed fleet. Research in sensors also showed that aircraft fuel pumps face increasing monitoring needs as pressure and temperature loads increase, supporting the view that this category remains central to both OEM and aftermarket activity in the aircraft pumps market. In practical terms, the aircraft pumps market keeps fuel pumps at the center of fleet reliability because propulsion-related components cannot tolerate extended downtime.

Hydraulic pumps are the fastest-growing segment, with a 7.75% CAGR through 2031, and this part of the aircraft pumps market is expanding as higher-pressure flight control systems and defense upgrades drive demand. The aircraft pumps industry also benefits from the fact that hydraulic content remains deeply embedded in landing gear, braking, actuation, and utility systems across large commercial and military platforms. Eaton's FLRAA award supports this view because the program includes hydraulic power generation and conveyance content for a next-generation rotorcraft platform. Lubrication pumps continue to track engine output and maintenance demand, while coolant pumps are gaining relevance as thermal management needs rise in more-electric architectures. Other pump categories remain smaller, but they still matter in the aircraft pumps market because cabin, utility, and specialized subsystem functions require qualified components even at lower volume.

Engine-driven systems accounted for 45.35% of revenue in 2025, making them the leading configuration in the aircraft pumps market, as the installed fleet still relies heavily on centralized hydraulic generation. Their position remains strong because aircraft layouts, maintenance routines, and certification histories have been built around them for decades, which raises switching costs across the aircraft pumps market. Air-driven pumps still support auxiliary and emergency duties on selected platforms, while RAT-driven units remain critical as last-resort hydraulic sources on transport aircraft. Manual pumps are a small category, but they continue to serve general aviation and maintenance use cases where simplicity still matters.

Electric motor-driven pumps are forecast to grow at a 8.37% CAGR through 2031, and this segment represents one of the clearest areas of expansion for the aircraft pumps market within new system architectures. The aircraft pumps market is moving in this direction because distributed power and local control align well with more-electric aircraft goals, especially in subsystems where decoupling from the engine improves flexibility. Liebherr's FAUST work on high-efficiency power packs directly supports this shift and shows that suppliers are already preparing for aircraft that depend less on engine-linked hydraulic generation. Research in actuators provides technical support by showing how electro-hydrostatic concepts can improve power density and thermal performance, which helps explain why electric-drive pump assemblies are gaining attention in the aircraft pumps market. Even so, the pace of change will vary by platform, and the aircraft pumps market is likely to carry both engine-driven and electric-drive systems in parallel for much of the forecast period.

Geography Analysis

North America accounted for 44.68% of revenue in 2025, making it the largest region in the aircraft pumps market and the broadest installed base across OEM, defense, and MRO activities. The aircraft pumps market remains strong in North America because the region combines major aircraft programs, deep supplier networks, and established certification capabilities within a single ecosystem. Defense demand adds another layer of stability, and Eaton's FLRAA role shows that advanced US programs continue to create demand for hydraulic power generation and conveyance systems. The region also benefits from a large aftermarket base, since airlines, military operators, and maintenance providers all depend on approved pump support over long service cycles. That combination keeps North America central to the aircraft pumps market even when production rates or defense timing vary by program.

Europe held the second-largest regional position in 2025, and the aircraft pumps market there is supported by Airbus production activity and a strong base of subsystem suppliers. Airbus's 2025 delivery performance reinforces Europe's role in commercial aircraft output, while the company's large backlog keeps future linefit demand visible for pump suppliers tied to its platform base. Europe is also important to the aircraft pumps market because suppliers are actively preparing for next-generation architectures, and Liebherr's participation in the FAUST and TiReGo programs shows focused work on decoupled hydraulic power packs and improved material cycles. These efforts matter because they support both near-term production needs and the longer-term redesign of aircraft subsystems toward more-electric, more-material-efficient layouts.

Asia-Pacific is forecast to grow at a 6.23% CAGR through 2031, making it the fastest-growing regional segment and a rising contributor to the aircraft pumps market size. The aircraft pumps market in Asia-Pacific is being lifted by growing commercial fleets, local platform ambitions, and defense procurement across several countries. Japan adds strategic weight because it combines civil and defense demand with interest in hydrogen-related aircraft development, while the wider region benefits from a growing maintenance base as fleet counts rise. South America remains smaller, but its regional contribution is supported by aircraft production and service activity tied to established aerospace programs. The Middle East and Africa also add demand through active military fleets and expanded air transport. However, project timing in this part of the aircraft pumps market is more exposed to budget cycles than in North America or Europe.

- Parker-Hannifin Corporation

- Eaton Corporation plc

- Safran SA

- Collins Aerospace (RTX Corporation)

- Woodward, Inc.

- Crane Aerospace & Electronics (Crane Co.)

- Honeywell International Inc.

- Triumph Group, Inc.

- Moog Inc.

- Liebherr Group

- Kawasaki Heavy Industries, Ltd.

- Hydraulics International, Inc.

- AeroControlex Group Inc.

- IHI Corporation

- ITT Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification of aircraft systems

- 4.2.2 Surge in commercial aircraft deliveries

- 4.2.3 Military fleet modernization

- 4.2.4 Lightweight composite pump designs

- 4.2.5 Predictive maintenance deployment

- 4.2.6 Hydrogen-ready fuel systems

- 4.3 Market Restraints

- 4.3.1 Electromechanical actuation replacing hydraulics

- 4.3.2 High certification and compliance costs

- 4.3.3 Aerospace-grade supply chain bottlenecks

- 4.3.4 Raw material price volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Pump Type

- 5.1.1 Fuel Pumps

- 5.1.2 Hydraulic Pumps

- 5.1.3 Lubrication Pumps

- 5.1.4 Coolant Pumps

- 5.1.5 Other Specialized Pumps

- 5.2 By Drive Mechanism

- 5.2.1 Engine-Driven

- 5.2.2 Electric Motor-Driven

- 5.2.3 Air-Driven

- 5.2.4 Ram-Air-Turbine (RAT) Driven

- 5.2.5 Manual/Hand Pumps

- 5.3 By Pressure Rating

- 5.3.1 Below 1,500 psi

- 5.3.2 1,500 to 3,000 psi

- 5.3.3 Above 3,000 psi

- 5.4 By Aircraft Type

- 5.4.1 Commercial Aviation

- 5.4.1.1 Narrowbody

- 5.4.1.2 Widebody

- 5.4.1.3 Regional Jets

- 5.4.2 Military Aviation

- 5.4.2.1 Fighter Jets

- 5.4.2.2 Transport Aircraft

- 5.4.2.3 Rotorcraft

- 5.4.3 General Aviation

- 5.4.4 Unmanned Aerial Vehicles (UAVs)

- 5.4.1 Commercial Aviation

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Parker-Hannifin Corporation

- 6.4.2 Eaton Corporation plc

- 6.4.3 Safran SA

- 6.4.4 Collins Aerospace (RTX Corporation)

- 6.4.5 Woodward, Inc.

- 6.4.6 Crane Aerospace & Electronics (Crane Co.)

- 6.4.7 Honeywell International Inc.

- 6.4.8 Triumph Group, Inc.

- 6.4.9 Moog Inc.

- 6.4.10 Liebherr Group

- 6.4.11 Kawasaki Heavy Industries, Ltd.

- 6.4.12 Hydraulics International, Inc.

- 6.4.13 AeroControlex Group Inc.

- 6.4.14 IHI Corporation

- 6.4.15 ITT Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment