|

시장보고서

상품코드

2061967

승객용 드론 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Passenger Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

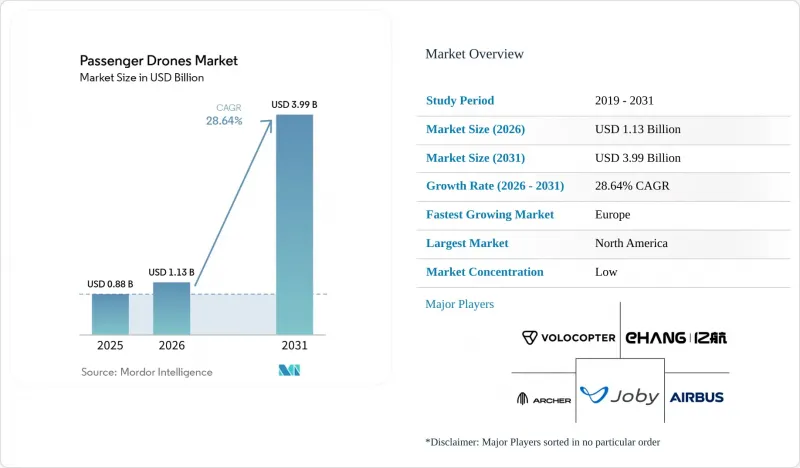

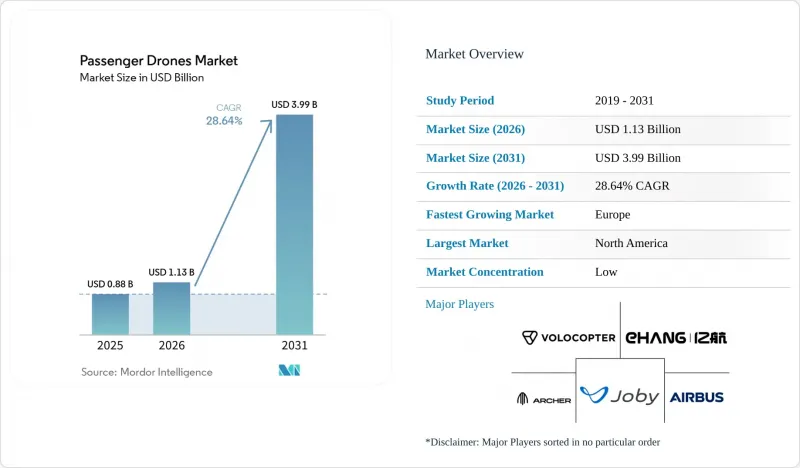

Mordor Intelligence에 의하면, 승객용 드론 시장 규모는 2025년 8억 8,000만 달러로 평가되었습니다. 2026년 11억 3,000만 달러에서 2031년까지 39억 9,000만 달러로 확대되어 예측 기간 중 연평균 복합 성장률(CAGR)은 28.64%를 나타낼 것으로 전망됩니다.

본 보고서는 드론의 유형(멀티콥터, 틸트로터 등), 승객 수(1인승 등), 운용 모드(유인, 반자율 등), 추진 방식(전전기식 등), 용도(도시형 에어택시, 도시 간 셔틀 등), 지역(북미, 유럽, 아시아태평양 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 승객용 드론 시장 동향과 인사이트

도시 지역의 교통 체증이 도시형 항공 모빌리티 수요를 촉진하고 있습니다.

도시 지역의 교통 정체는 대도시에서 단거리 항공 이동 수단의 경제적 타당성을 높여주며, 승객용 드론 시장이 본격적인 상용화에 한 걸음 더 다가가는 데 기여하고 있습니다. 노선 계획은 더 이상 항공기 제조업체만 결정하는 것이 아니라, 공항 당국, 교통 기관, 부동산 개발업체가 승객의 승하차, 착륙, 충전 시설의 설치 위치에 영향을 미치게 되었습니다. 단기적으로 가장 유력한 징후는 드론 기체가 대규모로 보급되기 전에 인프라가 점차 갖춰지고 있다는 점이며, 이로 인해 승객용 드론 시장에서 인증 획득과 서비스 개시 사이의 간격이 좁혀지고 있습니다. 두바이 도로교통국과 스카이포트 인프라스트럭처는 2026년 4월, 두바이 국제공항에서 세계 최초의 상업용 버티포트 기술 완성을 발표했습니다. 이는 두바이 마리나, 두바이 몰, 팜 주메이라를 포함한 4개 거점의 네트워크와 연계되어 있습니다. 이러한 네트워크에서 선두를 달리는 도시들은 운항 면에서 우위를 점하고 있으며, 일단 운항권, 부동산 접근성, 파트너 생태계가 갖춰지면 후발 주자 시장이 이를 따라잡기는 어려울 것입니다.

배터리 에너지 밀도 향상 및 비용 절감

배터리 개선은 승객용 드론 시장에서 여전히 가장 중요한 기술적 요소입니다. 왜냐하면 항로의 경제성, 적재량, 회전 시간, 기체 구성 등 모든 것이 이에 달려 있기 때문입니다. 또한, 에너지 밀도의 향상은 제로 에미션 구동 시스템에서 전환할 필요 없이 주행 거리를 늘릴 수 있게 해주므로, 도시 지역에서의 서비스에 있어 완전 전기 플랫폼의 실용성을 높여줍니다. EHang사는 에너지 밀도 480 Wh/kg의 EH216-S 기체를 사용하여 2024년 11월 세계 최초로 eVTOL용 고체 배터리 비행 시험을 완료했다고 발표했습니다. 이 성과는 중요합니다. 왜냐하면 고밀도 배터리 시스템은 도시 지역의 단거리 노선에서 상용화의 가능성을 넓혀주고, 이미 인증 획득을 눈앞에 둔 제조업체의 입지를 강화할 수 있기 때문입니다. 승객용 드론 시장에서 이러한 호재를 가장 먼저 체감하게 될 곳은 배터리 공급망, 기체 제조 및 인증 작업이 이미 병행되어 진행되고 있는 지역일 것으로 보입니다.

인증 및 안전 기준의 불확실성

인증은 여전히 승객용 드론 시장의 가장 큰 구조적 장벽으로 남아 있습니다. 이는 항공기 개발자들이 주요 관할 구역마다 서로 다른 기술적 접근 방식을 마주하고 있기 때문입니다. 특정 규제 체계에서 성과를 거둔 제조업체라 하더라도, 다른 체계로의 원활하고 신속한 전환을 기대할 수 없으며, 그 결과 비용이 증가하고 시장 진입이 지연될 수밖에 없습니다. EASA의 2025년 운영 프레임워크는 유럽에 있어 중요한 한 걸음이었지만, FAA, EASA, CAAC, JCAB의 각기 다른 접근 방식이 공존하는 상황은 여전히 전 세계 프로그램에 있어 규정 준수 부담을 높은 수준으로 유지하고 있습니다. 그 결과, 제조업체들은 여러 주요 시장에 동시에 진출하기보다는 승인 절차를 순차적으로 진행하는 경우가 많아지고 있습니다. 이로 인해 기체 도입이 지연되고 자금 수요가 증가하면서, 승객용 드론 시장은 장기간에 걸친 인증 절차를 견뎌낼 수 있는 소수의 기업군에 의존하는 상황이 지속되고 있습니다.

부문별 분석

2025년 기준으로 멀티콥터는 승객용 드론 시장 점유율의 42.24%를 차지했으며, 이러한 우위는 초기 상용 운항 단계에서 더 단순한 기계적 구조, 더 짧은 검증 주기, 그리고 더 낮은 훈련 난이도를 반영한 결과입니다. 이러한 구성은 장거리 순항 효율보다 안정적인 이착륙 성능이 중시되는 단거리 도시 노선에 적합합니다. 규제 당국이 파워 리프트 방식의 결함 및 운항 안전성을 엄격하게 심사하고 있기 때문에 이 점이 멀티콥터에 단기적인 실용적 인증상의 우위를 가져다주고 있습니다. EHang사의 EH216-S는 멀티콥터 설계로, 중국민용항공국(CAAC)으로부터 상업용 형식인증 및 제조인증을 획득한 최초의 eVTOL 플랫폼이 되었으며, 이는 이러한 추세를 뒷받침하고 있습니다.

틸트로터는 승객용 드론 시장에서 가장 빠르게 성장하고 있는 드론 유형으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 30.12%를 나타낼 것으로 전망됩니다. 그 장점은 고속 주행 시 연비가 뛰어나다는 점에 있으며, 단거리 도시 간 이동을 넘어서는 장거리 노선에 적합합니다. 조비(Joby)사는 2026년에 FAA 규정을 준수하는 TIA 비행 시험 단계로 진입할 예정이며, 이를 통해 틸트로터 구조는 여전히 유럽과 미국의 인증 경쟁에서 중심적인 위치를 차지하고 있습니다. 아처(Archer)사 역시 상용화를 위한 준비 과정에서 유사한 구성을 추진하고 있으며, 이는 여객 드론 업계의 대다수가 여전히 틸트로터를 장거리 및 고밀도 노선망에 가장 적합한 설계로 간주하고 있음을 보여줍니다. 고정익 하이브리드 항공기는 이용 사례가 제한적이며, 초기 도시 지역에서의 도입보다는 도시 간 운송이나 특수 운송 임무에 더 적합하기 때문에 여전히 가장 작은 하위 부문에 머물러 있습니다.

2025년에는 4인승 이상의 기체가 여객 드론 시장의 49.23%를 차지할 것으로 예상되며, 이는 사업자와 제조업체들이 여전히 탑승률이 높아질수록 좌석당 경제성이 향상되는 형태를 목표로 하고 있음을 보여줍니다. 이 부문은 소형 개인 이동 수단 콘셉트보다는 도시형 에어택시, 도시 간 셔틀, VIP 이동, 긴급 지원과 같은 이용 사례에 더 적합합니다. 더 넓은 객실 구조는 개인 여행객뿐만 아니라 대표단 전체를 수송할 수 있어 기업 고객에게도 매력적입니다. 2025년 10월에 발표된 EHang의 VT35는 목표 항속 거리 200km를 자랑하며, 기존의 EH216-S 버티포트 인프라와 호환성을 갖추고 있어 대용량 모빌리티 프로그램의 추진을 뒷받침하고 있습니다.

2-4인승 부문은 여객 드론 시장 내에서 가장 빠르게 성장하고 있는 분야로, 2031년까지 연평균 성장률(CAGR)은 31.16%를 나타낼 것으로 예측됩니다. 이 방식은 공간이 제한적인 도시 지역의 버티포트에도 대응할 수 있을 뿐만 아니라, 상업 운항을 뒷받침하기에 충분한 편당 수익을 창출할 수 있어 실용적인 중간적 위치를 차지하고 있습니다. 아처사의 ‘미드나이트’는 이러한 논리에 따라 설계되었으며, 조종사 1명과 승객 4명을 수용하는 구성을 채택하여 공항과 도시를 연결하는 고밀도 노선 프로파일에 대응하고 있습니다. 소형 개인용 항공기는 여전히 개발이 가장 더딘 상업 부문이지만, 미국의 새로운 규제 체계 덕분에 향후 2인승 경량 파워리프트 항공기 시장에 진입하기가 더 쉬워질 가능성이 있습니다. 모든 좌석 등급을 통틀어, 승객용 드론 업계는 단순히 최대 승객 수를 추구하는 것이 아니라, 편당 경제성과 인프라 제약, 항로 길이, 인증 시기를 종합적으로 고려하여 균형을 맞추고 있습니다.

지역별 분석

2025년 북미는 시장 점유율의 38.77%를 차지했으며, 이는 해당 지역의 풍부한 민간 자본 기반, 활발한 인증 작업, 그리고 광범위한 인프라 기반을 반영하고 있습니다. 미국은 여전히 중심적인 위치를 차지하고 있으며, 이는 FAA의 상업용 규제 체계와 미국의 자본 생태계가 서방 국가들의 주요 프로그램을 계속해서 끌어들이고 있기 때문입니다. 2026년 3월, 조비(Joby)가 백악관의 eIPP(혁신적 민간 파트너십) 프로그램에 선정됨에 따라, 미국 내 조기 상용화는 단순한 미래 목표에서 최대 10개 주에 이르는 활발한 운영 경로로 전환되었습니다. 이러한 전환이 중요한 이유는 북미 승객용 드론 시장에서 연방 정부의 지원, 항공기 준비 상황, 그리고 노선 차원의 전개 계획 간의 연관성이 더욱 명확해졌기 때문입니다.

유럽은 가장 빠르게 성장하는 지역 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 29.91%를 나타낼 것으로 전망됩니다. EASA가 새로운 VTOL 규제 체계에 따라 2025년에 내린 결정은 유럽에 보다 종합적인 운영 체계를 제공함으로써, 개발자와 운항 사업자의 불확실성을 줄이는 데 기여했습니다. 또한 영국도 중요한 위치를 차지하고 있습니다. Vertical Aerospace는 승인을 받는 대로, 향후 국경을 넘어 항공기 편대가 이동할 수 있는 기반을 마련해 나가고 있기 때문입니다.

아시아태평양은 승객용 드론 시장에서 가장 상업적으로 발전된 운항이 이루어지고 있으며, 중국에서는 2026년 시점에 이미 티켓을 구매하는 방식의 자율형 여객 서비스가 운영되고 있습니다. EHang은 2026년 3월 광저우와 허페이에서 EH216-S의 상용 서비스를 시작했으며, 중국은 이 정도 규모의 수익을 창출하는 자율형 여객 드론 운항을 실현한 최초 시장이 되었습니다. 일본도 발전하고 있으며, SkyDrive는 2026년 4월 JCAB로부터 승인 설계 기관(ADO) 인증을 받은 국내 최초의 eVTOL 개발 기업이 되었습니다. 한국에서는 국가 실증 프로그램의 일환으로, 서울 최초의 UAM 버티포트 ‘KINTEX’가 2026년 3월에 착공되어 인프라 구축을 향한 새로운 진전이 있었습니다. 중동도 급속히 발전하고 있으며, 두바이에서는 바티포트가 완공되었고, UAE에서는 제한적 형식인증(RTC) 접근 방식에 따라 아처사의 ‘미드나이트’ 도입을 위한 기반이 마련되었습니다. 남미 지역은 아직 규모는 작지만, 브라질의 밀집된 도시 구조와 헬리콥터 이동 수단에 대한 친화성 덕분에, 양국 간 상호 인정 및 인증 항공기 공급 상황이 개선된다면, 향후 도입 시장으로서 중요한 위치를 계속 차지할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the passenger drones market size is projected to expand from USD 0.88 billion in 2025 and USD 1.13 billion in 2026 to USD 3.99 billion by 2031, registering a CAGR of 28.64% during the forecast period.

This report is Segmented by Drone Type (Multicopter, Tilt-Rotor, and More), Seating Capacity (Single Seater, and More), Mode of Operation (Piloted, Semi-Autonomous, and More), Propulsion Type (Full-Electric, and More), Application (Urban Air Taxi, Inter-City Shuttle, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Passenger Drones Market Trends and Insights

Urban Traffic Congestion Catalyzing Demand for Urban Air Mobility

Urban congestion is creating a stronger economic case for short-range air mobility in large cities, helping the passenger drones market move closer to regular commercial use. Route planning is no longer shaped solely by aircraft developers, as airport authorities, transit agencies, and property developers are now influencing where passenger pickup, landing, and charging assets will be located. The strongest near-term signal is that infrastructure is being built before fleets reach broad scale, which reduces the gap between certification and service launch in the passenger drones market. Dubai's Roads and Transport Authority and Skyports Infrastructure announced the technical completion of the world's first commercial vertiport at Dubai International Airport in April 2026, which is tied to a 4-node network that includes Dubai Marina, Dubai Mall, and Palm Jumeirah. Cities that move first on these networks are building operating advantages that will be difficult for slower markets to match once traffic rights, real estate access, and partner ecosystems are already in place.

Advances in Battery Energy Density and Cost Reductions

Battery improvement remains the most important technical lever for the passenger drones market because route economics, payload, turnaround time, and aircraft configuration all depend on it. Better energy density also makes full-electric platforms more practical for urban service because it extends useful range without requiring a shift away from zero-emission drivetrains. EHang stated that it completed the world's first eVTOL solid-state battery flight test in November 2024, using an EH216-S aircraft with an energy density of 480 Wh/kg. That result matters because higher-density battery systems can widen the commercial window for short urban routes and can also strengthen the position of manufacturers already close to certification. The passenger drones market is likely to feel this driver first in geographies where battery supply chains, aircraft manufacturing, and certification activity are already moving in parallel.

Certification and Safety-Standard Uncertainties

Certification remains the heaviest structural brake on the passenger drones market because aircraft developers still face different technical pathways across major jurisdictions. A manufacturer that advances in 1 regulatory system cannot assume a smooth or rapid transfer into another, which raises costs and delays market entry. EASA's 2025 operating framework was an important step for Europe, but the coexistence of separate FAA, EASA, CAAC, and JCAB approaches still keeps compliance burdens high for global programs. The result is that manufacturers often move through sequential approval queues rather than launching across multiple major markets simultaneously. That slows fleet deployment, strains capital needs, and keeps the passenger drones market dependent on a smaller group of companies that can carry long certification cycles.

Other drivers and restraints analyzed in the detailed report include:

- Supportive Regulatory Sandboxes and Pilot Programs

- Real-Estate-Backed Vertiport Ecosystems

- Cold-Weather Battery Performance Degradation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multicopters held 42.24% of the passenger drones market share in 2025, and that lead reflected a simpler mechanical layout, shorter validation cycles, and lower training complexity for early commercial operations. Their configuration is better aligned with short urban routes, where stable takeoff and landing behavior matter more than long cruise efficiency. That has given multicopters a practical certification advantage in the near term because regulators are closely examining powered-lift failure points and operational safety. EHang's EH216-S supports this pattern because it is a multicopter design and became the first eVTOL platform to secure commercial type certification and production certification from the CAAC.

Tilt-rotors are the fastest-growing drone type in the passenger drones market, with a projected CAGR of 30.12% over 2026 to 2031. Their advantage lies in better cruise efficiency at higher speeds, making them more suitable for corridor routes that extend beyond short urban hops. Joby advanced into FAA-conforming TIA flight testing in 2026, which keeps tilt-rotor architectures central to the Western certification race. Archer is also pushing the same configuration through commercial launch preparation, which shows that large parts of the passenger drone industry still see tilt-rotors as the design best suited to longer, denser route networks. Fixed-wing hybrid aircraft remain the smallest sub-segment because their use case is narrower and better fits inter-city and specialized transport missions than early urban deployment.

More than 4-seater aircraft accounted for 49.23% of the passenger drone market in 2025, indicating that operators and manufacturers are still targeting formats where seat economics improve with higher occupancy. This segment fits urban air taxi, inter-city shuttle, VIP movement, and emergency support use cases better than smaller personal mobility concepts. Larger cabin layouts also appeal to corporate users because they can move delegations rather than single travelers. EHang's VT35, unveiled in October 2025 with a target range of 200 km and compatibility with existing EH216-S vertiport infrastructure, reinforces the push toward higher-capacity mobility programs.

The 2- to 4-seater segment is the fastest-growing part of the passenger drones market, with a 31.16% CAGR through 2031. This format sits in a practical middle ground because it can serve constrained urban vertiports while still generating enough revenue per flight to support commercial operations. Archer's Midnight is built around this logic, with a pilot-plus-four-passenger layout and a route profile designed for dense airport-to-city links. Smaller personal aircraft remain the least developed commercial segment, even though new regulatory pathways in the US may make light two-occupant powered-lift formats easier to enter over time. Across seating classes, the passenger drone industry is balancing per-flight economics with infrastructure constraints, route length, and certification timing rather than simply chasing maximum passenger count.

Geography Analysis

North America held 38.77% of the market share in 2025, reflecting the region's deep private capital base, active certification work, and broad infrastructure foundation. The US remains the center of that position because the FAA's commercial framework and the country's capital ecosystem continue to attract the leading Western programs. Joby's selection under the White House eIPP in March 2026 turned early US commercialization from a future objective into an active operating pathway across as many as 10 states. That shift matters because the passenger drones market in North America now has clearer links between federal support, aircraft readiness, and route-level deployment planning.

Europe is the fastest-growing regional segment, with a projected CAGR of 29.91% over 2026 to 2031. EASA's 2025 decisions under the new VTOL regulatory framework provided Europe with a more comprehensive operating framework and helped reduce uncertainty for developers and operators. The UK is also relevant because Vertical Aerospace is progressing on a track that can support later cross-border fleet movement once approvals are in place.

Asia-Pacific hosts the most commercially advanced operations in the passenger drones market, as China is already operating ticketed autonomous passenger services in 2026. EHang launched EH216-S commercial services in Guangzhou and Hefei in March 2026, making China the first market to have revenue-generating autonomous passenger drone operations at this scale. Japan is also moving forward, and SkyDrive became the country's first eVTOL developer to receive Approved Design Organization certification from JCAB in April 2026. South Korea added another infrastructure signal when the first Seoul metro UAM vertiport, KINTEX, broke ground in March 2026 under the national demonstration program. The Middle East is developing rapidly, with Dubai's completed vertiport and the UAE's pathway for Archer's Midnight under a Restricted Type Certificate approach. South America remains small, but Brazil's dense urban structure and familiarity with helicopter mobility keep it relevant as a future adoption market once bilateral recognition and the availability of certified aircraft improve.

- Joby Aero, Inc.

- Volocopter GmbH

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Archer Aviation Inc.

- Vertical Aerospace Group Ltd.

- Wisk Aero LLC

- Airbus SE

- Aurora Flight Sciences (The Boeing Company)

- Supernal, LLC (Hyudai Motor Group)

- Textron Inc.

- Eve Holding, Inc. (Embraer S.A.)

- AutoFlight Co. Ltd.

- SkyDrive Inc.

- BETA Technologies, Inc.

- Ascendance Flight Technologies S.A.S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban traffic congestion catalyzing demand for UAM

- 4.2.2 Advances in battery energy density and cost reductions

- 4.2.3 Supportive regulatory sandboxes and pilot programs

- 4.2.4 Real-estate-backed vertiport ecosystems

- 4.2.5 Defense-derived autonomous flight-control breakthroughs

- 4.2.6 Corporate environmental, social, and governance -driven demand for zero-emission executive mobility

- 4.3 Market Restraints

- 4.3.1 Certification and safety-standard uncertainties

- 4.3.2 Cold-weather battery performance degradation

- 4.3.3 Payload-range trade-offs driven by battery mass

- 4.3.4 Social-media driven reputational risk on incidents

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Drone Type

- 5.1.1 Multicopter

- 5.1.2 Tilt-rotor

- 5.1.3 Fixed-wing Hybrid

- 5.2 By Seating Capacity

- 5.2.1 Single Seater

- 5.2.2 2 to 4 Seater

- 5.2.3 More than 4 Seater

- 5.3 By Mode of Operation

- 5.3.1 Piloted

- 5.3.2 Semi-Autonomous

- 5.3.3 Fully Autonomous

- 5.4 By Propulsion Type

- 5.4.1 Full-Electric

- 5.4.2 Hybrid-Electric

- 5.4.3 Hydrogen Fuel Cell

- 5.5 By Application

- 5.5.1 Urban Air Taxi

- 5.5.2 Inter-City Shuttle

- 5.5.3 Air Tourism

- 5.5.4 Emergency Medical Services

- 5.5.5 VIP Transport

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Joby Aero, Inc.

- 6.4.2 Volocopter GmbH

- 6.4.3 Guangzhou EHang Intelligent Technology Co. Ltd.

- 6.4.4 Archer Aviation Inc.

- 6.4.5 Vertical Aerospace Group Ltd.

- 6.4.6 Wisk Aero LLC

- 6.4.7 Airbus SE

- 6.4.8 Aurora Flight Sciences (The Boeing Company)

- 6.4.9 Supernal, LLC (Hyudai Motor Group)

- 6.4.10 Textron Inc.

- 6.4.11 Eve Holding, Inc. (Embraer S.A.)

- 6.4.12 AutoFlight Co. Ltd.

- 6.4.13 SkyDrive Inc.

- 6.4.14 BETA Technologies, Inc.

- 6.4.15 Ascendance Flight Technologies S.A.S

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment