|

시장보고서

상품코드

2061983

입상 요소 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Granular Urea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

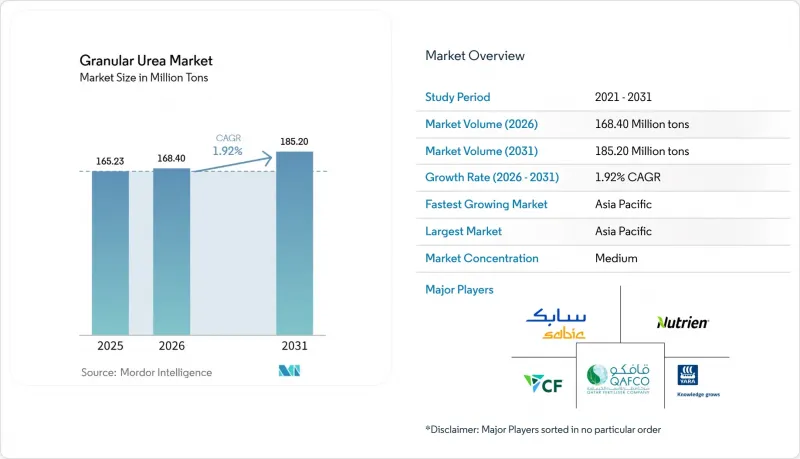

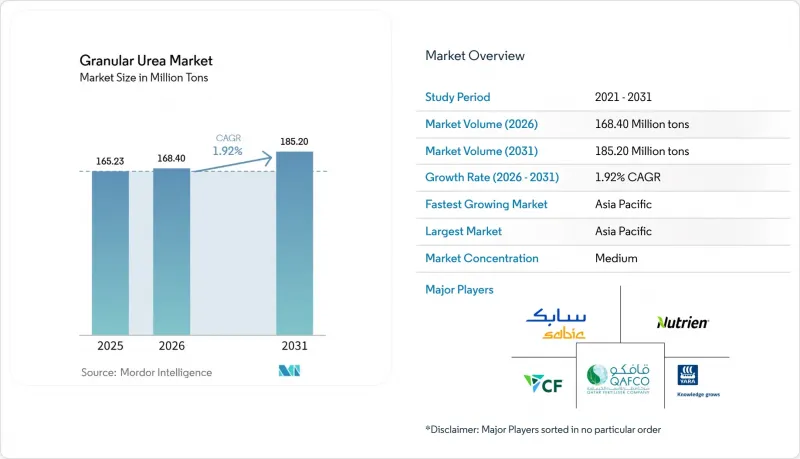

Mordor Intelligence에 의하면, 입상 요소 시장 규모는 2025년 1억 6,523만 톤, 2026년 1억 6,840만 톤으로부터, 2031년까지 1억 8,520만 톤으로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 1.92%를 나타낼 것으로 예측됩니다.

본 보고서는 등급(농업용 등급, 산업용 등급), 용도(농업(곡물 및 기타 곡류), 산업(접착제 및 수지, 화학제품, 기타 산업용도)), 그리고 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 입상 요소 시장 동향 및 분석

질소계 비료 수요 증가

2025년, 전 세계 곡물 및 유지종자의 재배 면적은 210만 헥타르 증가했으며, 이로 인해 120만 톤의 질소 수요가 추가되었습니다. 과립 제제는 분진 발생량이 줄어들어 호흡기 문제를 완화할 뿐만 아니라, 미국과 유럽연합(EU)이 정한 엄격한 산업위생 기준도 충족하기 때문에 인기를 끌었습니다. 2025년, 인도의 질소비료 수입량은 2024년 대비 28% 급증하여 총 410만 톤에 달했습니다. 이러한 급증은 주로 몬순의 불안정성으로 인한 것으로, 파종 기간이 단축된 데다 속용성 입상 비료에 대한 수요가 증가한 것이 원인입니다. 미국 내 옥수수 및 대두 재배지에서 정밀 농업 도입률이 42%까지 급증했습니다. 가변 시비를 가능하게 하는 이 기법 덕분에 과잉 시비가 최대 18% 감소한 반면, 공기식 살포기와 원활하게 연동되는 균일한 입상 비료에 대한 수요도 동시에 증가했습니다. 또한, 베트남, 태국, 인도네시아에서의 안정적인 벼 재배 주기가 구매 패턴을 더욱 안정화시켰습니다. 이러한 농업 동향들이 맞물려 질소 소비량 증가를 주도하고 있습니다.

정부의 보조금 및 비료 지원 프로그램

인도는 2025-2026 회계연도에 약 130억 달러 규모의 비료 보조금을 편성하고, 요소의 소매 가격을 45kg당 266루피로 상한선을 설정했습니다. 이 조치는 세계 가격이 CFR(운임 포함) 기준 톤당 400달러를 넘어선 상황에서도 시행된 것으로, 원자재 가격 변동으로부터 소규모 농가를 보호하기 위한 전략입니다. 한편, 브라질의 ‘플라노 사프라 2025-2026’에서는 4,005억 9,000만 레알(약 800억 달러)에 달하는 막대한 규모의 농촌 지원 대출이 발표되었습니다. 이러한 재정 지원 덕분에, 2026년 1월 페트로브라스가 세르지페주와 바이아주 소재의 요소 생산 설비를 재가동했음에도 불구하고 수입 수요는 여전히 견조한 추세를 보이고 있습니다. 아르헨티나에서는 우대 대출 조치로 인해 질소 비료 수입량이 28%라는 현저한 증가세를 보이며 410만 톤에 달했습니다. 이러한 노력은 현재 기초적인 수요를 지탱하고 있지만, 정책 입안자들은 나노 액체 비료와 억제제 코팅 제품에 대한 자금 배분을 점점 더 늘리고 있습니다. 이러한 전환은 아산화질소 배출을 억제하기 위한 것으로, 입상 요소 시장의 호조가 2028년 이후 둔화될 가능성이 있음을 시사합니다.

천연가스 및 암모니아 원료 비용의 변동

2025년, 유럽의 가스 가격은 1MMBtu당 6달러에서 14달러 사이에서 변동했습니다. 이러한 변동은 암모니아 비용에 반영되었으며, 이는 요소 생산에 드는 현금 지출의 70-80%를 차지했습니다. 그 결과, 가격이 급등하여 이익률이 사라지자 생산자들은 겨울철 생산량을 줄였습니다. 한편, 미국 멕시코만 연안 지역에서는 암모니아 가격이 2025년 1분기 톤당 450달러에서 10월까지 620달러로 급등했습니다. 이러한 급등은 허리케인 프란신으로 인한 루이지애나주 공장 가동 중단에 이어, 하류 부문인 입상 요소의 이익률을 압박했습니다. 이러한 높은 변동성으로 인해 장기 공급 계약의 매력은 줄어들고 있습니다. 실제로, 가격 급등을 피하려는 브라질의 수입업체들은 2025년 요소 조달량의 60%를 현물 거래로 조달하고 있으며, 이는 2024년의 40%에서 크게 증가한 수치입니다. 이러한 불확실성은 생산 능력 확충도 지연시키고 있습니다. CF 인더스트리즈나 야라와 같은 기업들은 현재 기존의 확장보다 탄소국경조정제도(CBAM) 준수를 확실히 하기 위한 ‘블루 암모니아’ 투자를 우선시하고 있습니다.

부문별 분석

2025년에는 농업용 입상 요소가 수요의 77.23%를 차지하며 수요를 주도했습니다. 이는 인도의 칼리프(가을) 및 라비(겨울) 작기 동안 2,800만 톤이 소비된 데 더해, 브라질에서 대두 및 옥수수 재배에 620만 톤이 사용된 것이 원인입니다. 이러한 막대한 수요에도 불구하고, 입상 요소 시장의 농업 부문은 2031년까지 완만한 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다. 이러한 완만한 성장은 기존 질소 비료의 30-50%를 대체하는 것을 목표로 하는 인도의 나노 액체 비료 보급 확대와, EU의 사용 상한선 강화에 기인한 것입니다. 농가들은 기계식 파종기에 사용할 때 입상 비료의 분진이 적다는 점을 높이 평가하고 있지만, 보조금 지원에 힘입은 서방형 제품이나 억제제 코팅 제품의 인기가 시장 확대를 저해하고 있습니다.

2025년 기준으로, 시장 점유율이 낮은 산업용 등급의 과립은 연평균 성장률(CAGR) 2.31%를 나타낼 것으로 전망됩니다. 이러한 성장은 포름알데히드계 목재 복합재, 멜라민 수지, 그리고 선택적 촉매 환원(SCR)용 시약에 대한 수요에 힘입은 것입니다. 이들 모두 입자 크기가 균일하고 비우렛 함량이 적은 과립을 필요로 합니다. 산업 분야에서 이러한 과립을 도입함으로써 생산자들을 농업 보조금의 변동으로부터 보호할 뿐만 아니라, 15-25%의 가격 프리미엄을 유지할 수 있게 되었습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 총량의 45.22%를 차지하며, 연평균 성장률(CAGR) 2.19%로 성장을 주도했습니다. 중국의 일시적인 수출 할당 조치로 인해 국내 공급은 안정적이지만, 인도의 수입량은 보조금 예산의 제약에도 불구하고 2025년에 13% 증가했습니다. 호주에서는 국내 공장 폐쇄로 인해 2024년 첫 8개월 동안 수입량이 335만 톤으로 사상 최고치를 기록했으며, 이는 기상 조건이나 생산 능력 중단이 지역 무역 흐름에 얼마나 신속하게 영향을 미치는지를 보여줍니다.

북미는 저비용 셰일가스의 혜택을 누리고 있으며, 세계적으로 경쟁력 있는 FOB 비용을 실현하고 있어, 이것이 라틴아메리카로의 수출을 뒷받침하고 있습니다. CF 인더스트리즈 한 회사만으로도 지역 내 과립 생산 능력의 약 42%를 차지하고 있으며, 2024년에는 22억 8,000만 달러의 조정 EBITDA를 달성했습니다. 또한, 미국은 기존 암모니아·요소 생산 라인에 병설된 탄소 포집 프로젝트를 시범적으로 시행하고 있으며, 탄소 발자국 표시 기준이 공식적으로 제정되면 해당 지역은 프리미엄 시장을 겨냥해 저탄소 제품을 판매할 수 있는 체제를 갖추고 있습니다.

유럽은 에너지 가격 급등과 환경 규제 강화라는 이중의 과제에 직면해 있습니다. 가스 가격 급등으로 인해 2024년에는 요소 환산 기준 290만 톤에 달하는 암모니아 생산 감축을 피할 수 없게 되었으며, CBAM 관세 도입이 임박한 가운데 알제리, 이집트, 카타르로부터의 수입이 촉진되었습니다. 동유럽, 특히 폴란드와 루마니아는 파이프라인 가스를 공급받을 수 있다는 점으로 인한 비용 우위를 유지하고 있어, 서유럽에서의 생산 중단을 부분적으로 상쇄하고 있습니다.

브라질과 아르헨티나를 비롯한 남미 지역에서는 철도 및 항만 시설 확충으로 내륙 지역의 가격 격차가 줄어들면서 농지의 급격한 용도 변경이 계속되고 있습니다. 이 지역의 요소 수요는 연평균 2.6%의 성장률을 보이고 있으며, 이는 전 세계 입상 요소 시장의 연평균 성장률(CAGR)을 소폭 상회하는 수치입니다. 중동 및 아프리카는 풍부한 천연가스를 활용하고 있으며, 사우디아라비아와 카타르는 전 세계 해상 운송 요소의 약 3분의 1을 수출하는 반면, 이집트는 대규모 관개 프로젝트를 통해 국내 소비를 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the granular urea market size is projected to expand from 165.23 Million tons in 2025 and 168.40 Million tons in 2026 to 185.20 Million tons by 2031, registering a CAGR of 1.92% between 2026 to 2031.

This report is Segmented by Grade (Agricultural Grade, Industrial Grade), Application (Agriculture [Cereals and Grains, and More], Industrial [Adhesives and Resins, Chemicals, Other Industrial Applications]), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Granular Urea Market Trends and Insights

Rising Demand for Nitrogen-based Fertilizers

In 2025, global cereal and oilseed acreage grew by 2.1 million hectares, leading to an additional demand of 1.2 million tons of nitrogen. Granular formulations gained popularity, as their reduced dust levels not only lessen respiratory issues but also align with the stringent occupational health standards set by the U.S. and the European Union. In 2025, India saw a 28% surge in nitrogen fertilizer imports, totaling 4.1 million tons, up from 2024. This spike was largely due to erratic monsoons, which compressed planting windows and heightened the preference for quick-dissolving granules. Adoption of precision agriculture soared to 42% across U.S. corn and soybean fields. This approach, allowing for variable-rate placement, has curtailed over-application by as much as 18%, simultaneously boosting the demand for uniform granules that work seamlessly with pneumatic spreaders. Additionally, the consistent rice cycles in Vietnam, Thailand, and Indonesia have further stabilized purchasing patterns. Together, these agricultural trends have driven up nitrogen consumption.

Government Subsidies and Fertilizer Support Programs

India allocated approximately USD 13 billion for fertilizer subsidies in FY 2025-2026, setting a retail cap of INR 266 per 45 kg for urea. This move comes even as global prices surged past USD 400 per ton CFR, a strategy aimed at shielding smallholders from the volatility of feedstock costs. Meanwhile, Brazil's "Plano Safra 2025-2026" unveiled a substantial BRL 400.59 billion (around USD 80 billion) in rural credit. This financial boost has kept import demand robust, even with Petrobras reactivating its urea units in Sergipe and Bahia in January 2026. In Argentina, preferential credit measures led to a notable 28% surge in nitrogen imports, reaching 4.1 million tons. While these initiatives currently support baseline demand, policymakers are increasingly directing funds towards nano-liquid and inhibitor-coated products. This shift aims to mitigate nitrous oxide emissions, suggesting that the uplift in the granular urea market may wane post-2028.

Volatile Natural-Gas and Ammonia Feedstock Costs

In 2025, European gas prices fluctuated between USD 6 and USD 14 per MMBtu. These swings translated into ammonia costs, which accounted for 70-80% of urea's cash expenses. Consequently, when prices spiked and margins were erased, producers cut back on winter production. Meanwhile, at the U.S. Gulf Coast, ammonia prices surged from USD 450 per ton in Q1 2025 to USD 620 per ton by October. This spike followed Hurricane Francine's closure of Louisiana plants, tightening margins for downstream granules. Such high volatility has made long-term offtake contracts less appealing. In fact, Brazilian importers, aiming to sidestep peak prices, sourced 60% of their 2025 urea on spot terms, a jump from 40% in 2024. This uncertainty has also stalled capacity expansions. Companies like CF Industries and Yara are now favoring investments in blue ammonia, which ensures compliance with the Carbon Border Adjustment Mechanism (CBAM), over traditional expansions.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Granular Over Prilled Urea for Better Handling

- Automated Bulk-Blending Facilities Favor Dust-Free Granules

- Environmental Impacts of Nitrate Leaching and Eutrophication

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, agricultural-grade granules dominated demand capturing 77.23%, driven by India's consumption of 28 million tons during the kharif and rabi seasons, alongside Brazil's application of 6.2 million tons for soybeans and corn. Despite this substantial demand, the agricultural segment of the granular urea market is projected to grow at a modest CAGR through 2031. This tempered growth is attributed to India's push for nano-liquid alternatives, which aim to replace 30-50% of conventional nitrogen, and tightening usage caps in the EU. While farmers value the granules for their low dust content in mechanized seeders, the allure of controlled-release and inhibitor-coated products, bolstered by subsidy support, has moderated the market's expansion.

In 2025, industrial-grade granules occupied a smaller market share but are on track to grow at a 2.31% CAGR. This growth is driven by demand from formaldehyde-based wood composites, melamine feed, and selective catalytic reduction reagents, all of which require consistently sized, low-biuret granules. The industrial sector's adoption of these granules not only insulates producers from the volatility of farm subsidies but also allows them to maintain a pricing premium of 15-25%.

Geography Analysis

Asia-Pacific commanded 45.22% of global volume in 2025, and leads growth at a 2.19% CAGR. China's temporary export quotas stabilize domestic supply, while India's imports rose 13% in 2025 despite subsidy-budget constraints. Australia set an import record at 3.35 million tons in the first eight months of 2024 after local plant closures, illustrating how weather and capacity outages quickly swing regional trade flows.

North America benefits from low-cost shale gas, enabling globally competitive FOB costs that underpin exports to Latin America. CF Industries alone holds roughly 42% of regional granulation capacity and achieved USD 2.28 billion adjusted EBITDA in 2024. The United States also pilots carbon-capture projects attached to existing ammonia-urea lines, positioning the region to sell low-carbon products into premium markets once carbon-footprint labeling standards formalize.

Europe faces twin hurdles of elevated energy prices and tightening environmental caps. High gas costs forced ammonia production curtailments equal to 2.9 million tons of urea in 2024, prompting imports from Algeria, Egypt, and Qatar despite looming CBAM tariffs. Eastern Europe, especially Poland and Romania, retains cost advantages from pipeline gas access, partially offsetting Western shutdowns.

South America, led by Brazil and Argentina, continues rapid farmland conversion as rail and port build-outs compress inland basis values. The region's urea demand grows 2.6% annually, slightly above the global granular urea market CAGR. Middle East and Africa leverage abundant natural gas, with Saudi Arabia and Qatar exporting nearly one-third of global seaborne urea while Egypt ramps domestic consumption through irrigation megaprojects.

- Acron

- BASF

- CF Industries Holdings, Inc.

- Dangote Fertiliser Limited.

- EuroChem Group

- Grupa Azoty S.A.

- IFFCO

- Indorama Corporation

- Koch Fertilizer, LLC.

- Nutrien

- OCI

- PETRONAS Chemicals Group Berhad

- PhosAgro Group

- SABIC

- Uralchem

- Qatar Fertiliser Company (QAFCO)

- Yara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for nitrogen fertilizers

- 4.2.2 Government subsidies and fertilizer support programs

- 4.2.3 Shift to granular over prilled urea for better handling

- 4.2.4 Automated bulk-blending facilities favour dust-free granules

- 4.2.5 Digital ag-marketplaces enabling micro-batch procurement

- 4.3 Market Restraints

- 4.3.1 Volatile natural-gas and ammonia feed-stock costs

- 4.3.2 Tightening regulations on nitrate runoff and eutrophication

- 4.3.3 European Union quotas mandating enhanced-efficiency urea share

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Agricultural Grade

- 5.1.2 Industrial Grade

- 5.2 By Application

- 5.2.1 Agriculture

- 5.2.1.1 Cereals and Grains

- 5.2.1.2 Fruits and Vegetables

- 5.2.1.3 Oilseeds and Pulses

- 5.2.1.4 Other Agricultural Applications

- 5.2.2 Industrial

- 5.2.2.1 Adhesives and Resins

- 5.2.2.2 Chemicals

- 5.2.2.3 Other Industrial Applications

- 5.2.1 Agriculture

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Acron

- 6.4.2 BASF

- 6.4.3 CF Industries Holdings, Inc.

- 6.4.4 Dangote Fertiliser Limited.

- 6.4.5 EuroChem Group

- 6.4.6 Grupa Azoty S.A.

- 6.4.7 IFFCO

- 6.4.8 Indorama Corporation

- 6.4.9 Koch Fertilizer, LLC.

- 6.4.10 Nutrien

- 6.4.11 OCI

- 6.4.12 PETRONAS Chemicals Group Berhad

- 6.4.13 PhosAgro Group

- 6.4.14 SABIC

- 6.4.15 Uralchem

- 6.4.16 Qatar Fertiliser Company (QAFCO)

- 6.4.17 Yara

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment