|

시장보고서

상품코드

2061985

이산화황 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Sulfur Dioxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

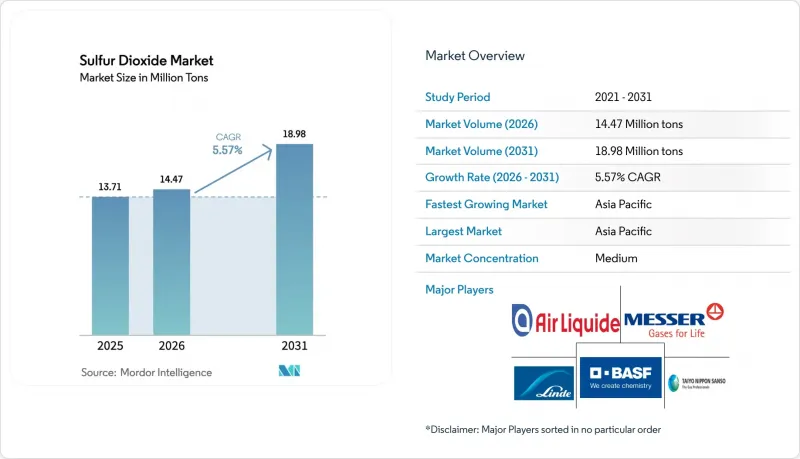

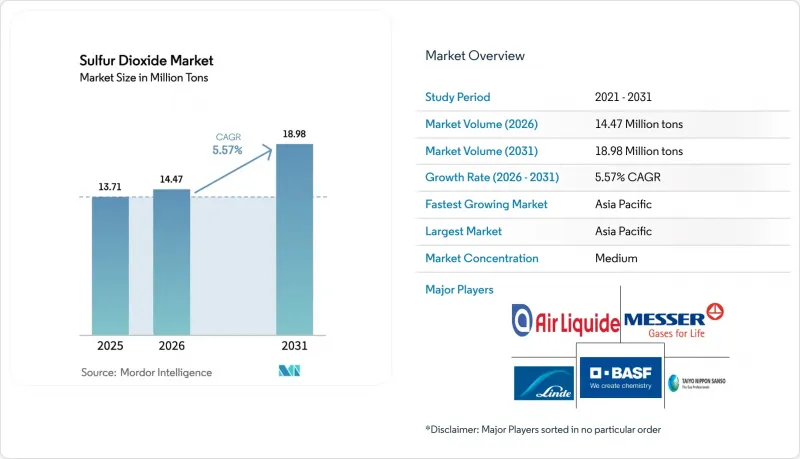

Mordor Intelligence에 의하면, 이산화황 시장 규모는 2025년에 1,371만 톤으로 평가되었고 2026년 1,447만 톤에서 2031년까지 1,898만 톤에 이르며 예측 기간(2026-2031년) CAGR은 5.57%를 나타낼 전망입니다.

본 보고서는 형태(기체, 액체, 고체), 순도 등급(99% 미만, 99.0%-99.9%, 99.9% 초과), 용도(화학 중간체, 식품 및 음료 보존, 의약품 합성, 펄프 및 종이 표백 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 이산화황 시장 동향 및 분석

황산 및 화학제품 분야에서의 활용 확대

황산 제조는 인산 비료의 산 처리나 구리 광석의 침출 과정에서 대체 수단이 없기 때문에 전 세계 이산화황(SO₂) 수요의 기반을 이루고 있습니다. 인도에서는 2024년부터 2025년에 걸쳐 콜로만델 인터내셔널, 파라딥 포스페이트, 구자라트 비료 등 각사에서 연간 120만 톤 규모의 신규 황산 생산 능력이 추가되었습니다. 이것들은 각각 자사용 암석 인산염의 전환과 관련이 있습니다. 중동산 황산 수출이 위축됨에 따라, 중국의 황산 현물 가격은 2025년 1분기 400위안/톤(54.50달러/톤)에서 12월까지 520위안/톤(73.78달러/톤)으로 상승했습니다. 모로와리와 웨다 만의 니켈 라텔라이트 습식 제련(침출) 과정에서 2025년에 80만 톤의 황산이 소비되었습니다. 이는 전기차용 황산니켈 생산량 증가에 따라 전년 대비 33% 증가한 수치입니다. 순도 99.9% 이상의 SO₂로 제조되는 반도체용 등급의 산은 테크니컬 등급보다 3-5배 높은 가격에 거래되고 있으며, 이에 따라 BASF는 2025년 4월 루트비히스하펜에서 초고순도 산의 생산 능력을 확대했습니다. 대량 생산되는 비료 용도와 고수익률의 전자기기 용도로 양극화됨에 따라, 이산화황 시장은 2031년까지 지속될 양극 구조로 굳어졌습니다.

펄프 및 종이의 표백 능력 확대

아시아와 남미의 펄프 공장은 유럽과 미국의 공장 폐쇄 속도를 웃도는 속도로 가동을 이어가고 있으며, 이로 인해 이산화황 수요가 증가하고 있습니다. 그라심(Grassim)사의 빌라얏 공장에 있는 일일 750톤 규모의 용해 펄프 생산 라인은 비스코스 섬유용 아황산 펄프 생산 공정을 통합하고 있으며, 한편, 산동 보후이사는 2025년에 이산화황 공정을 도입하여 연간 50만 톤의 표백 크라프트 펄프 생산 능력을 추가했습니다. Norske Skog사의 Skogn 공장은 스크러버를 개량하여 2025년에 SO₂의 단위 배출량을 공기 건조 톤당 12.3kg으로 줄였습니다. 누리온과 아라우코는 브라질에서 폐쇄형 아황산염 재생 시범 사업을 진행 중이며, 신규 황 사용량을 30% 감축하는 것을 목표로 하고 있습니다. EU의 산업 배출 지침이나 중국의 부문별 규제 등 규제 체계에 따라 배기가스 스크러버 설치가 의무화되어 있으며, 이것이 중기적인 성장을 뒷받침하고 있습니다.

건강 피해와 복잡한 취급

SO2는 강력한 호흡기 자극 물질입니다. OSHA(직업안전보건청)는 8시간 노출 한계치를 5ppm으로 설정하고 있지만, 국립직업안전보건연구소(NIOSH)는 2ppm을 권장하고 있습니다. 2024년 12월 EPA(환경보호청)의 규제로 인해 1시간 대기 기준이 강화되고 감시 대상이 확대됨에 따라, 유황 연소 시설에는 추가 비용이 발생하고 있습니다. 반도체 제조 공장은 SEMI S2(반도체 제조 장비) 기준을 충족해야 하며, 일상적인 배출량을 직업적 노출 한계치의 1% 미만으로 억제하고, 장비 1대당 50만-200만 달러의 비용이 드는 배출 억제 장치를 설치해야 합니다. 이러한 규정 준수 부담으로 인해 소규모 이용자들은 시장 진입을 주저하고 있으며, 전용 EHS(환경·보건·안전) 시스템을 운영하는 대규모 산업 고객들에게 수요가 집중되고 있습니다.

부문별 분석

2025년 기준으로, 이산화황(SO2) 시장 점유율의 56.18%를 기상 SO2가 차지했습니다. 이는 황산탑, 스크러버 및 파브가 지속적인 가스 공급을 필요로 하기 때문입니다. 이 부문은 확립된 인프라의 혜택을 누리고 있지만, 더욱 엄격해진 대기질 기준에 따라 규정 준수 비용 증가에 직면해 있습니다. 고체(아황산염/메타아황산염 유도체) 시장은 규모는 작지만, 식품 보존 업체와 제약 공장이 보험료 지출을 줄일 수 있는 저압으로 운송 가능한 원료를 선호함에 따라 연평균 성장률(CAGR) 5.87%로 성장하고 있습니다. 고체 이산화황 시장 규모는 아세안 지역 수요를 바탕으로 2031년까지 꾸준히 확대될 것으로 예상되지만, 대규모 산 제조 공장이 주를 이루는 중국과 인도에서는 여전히 기체 제품이 과반수의 점유율을 차지하고 있습니다.

액체 SO₂는 물류 측면에서 중간적인 위치를 차지하며, 배치식 특수 화학제품 제조업체나 지자체 시설에 공급되고 있습니다. Chemtrade의 Polytec 인수는 북미 전역에 걸친 액체 실린더 및 아황산염 혼합물 유통 체계를 강화하는 것입니다. 베트남과 태국의 규제 압박으로 인해 소규모 사용자들은 가스에서 고체 연료로 전환하고 있지만, 대량 생산을 하는 산업 시설에서는 공정 연속성을 유지하기 위해 계속해서 벌크 가스를 발주할 것으로 보입니다.

지역별 분석

2025년, 아시아태평양은 이산화황 시장에서 50.46%의 점유율을 차지하며 시장을 주도했습니다. 또한, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 6.04%를 나타낼 것으로 전망됩니다. 중국의 황산 현물 가격 급등은 유황 공급 부족을 시사하는 반면, 인도에서는 연간 120만 톤의 생산 능력 확충으로 인해 비료 부문 수요가 견조합니다. 대만, 일본, 한국은 반도체 노드용 초고순도 제품에 대한 수요를 견인하고 있으며, 아세안(ASEAN)의 규제는 사용 현장에서의 배출 저감 시스템에 대한 수요를 촉진하여 간접적으로 아황산염 판매를 뒷받침하고 있습니다.

북미는 멕시코만 연안의 황산 클러스터와 애리조나주 및 텍사스주의 신규 팹 프로젝트를 배경으로 2위를 차지했습니다. 린데(Linde)사가 루이지애나주에 건설하는 4억 달러 규모의 공기 분리 장치(ASU)는 액체 SO2를 병행 생산할 예정이며, 켐트레이드(ChemTrade)사의 폴리텍(Polytech)사 인수는 턴키 방식의 수처리 솔루션 제공 범위를 확대할 것입니다. EPA의 1시간 대기 기준 강화는 규정 준수 비용을 증가시키는 한편, 대형 공급업체에 유리한 폐쇄형 시스템으로의 기술 전환을 가속화하고 있습니다.

유럽은 석탄 화력 발전소의 폐쇄로 인해 자가 소비용 FGD(배연 탈황) 스트림이 사라지면서 수요 증가세가 뒤처지고 있습니다. 그러나 BASF의 루트비히스하펜 초고순도 제품 라인 확장은 해당 지역에 들어서는 첨단 노드 반도체 공장을 겨냥한 정밀 화학 분야로의 전환을 여실히 보여주고 있습니다. 북유럽의 펄프 사업에서는 틈새 시장용도로 아황산염의 사용이 유지되고 있지만, 합성 석고의 부족으로 인해 천연 석고의 수입이 증가하고 있습니다. 남미 수요는 폐쇄형 아황산염 재생 방식을 채택한 브라질의 유칼립투스 제재소가 주도하고 있으며, 중동 및 아프리카 수요량은 정유시설의 황 회수 및 남아프리카의 광업에 따라 좌우됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제8장 CEO을 위한 중요 전략적 과제

KTH 26.06.19According to Mordor Intelligence, the sulfur dioxide market size was valued at 13.71 million tons in 2025 and is estimated to grow from 14.47 million tons in 2026 to reach 18.98 million tons by 2031, at a CAGR of 5.57% during the forecast period (2026-2031).

This report is Segmented by Form (Gas, Liquid, and Solid), Purity Grade (Less Than 99%, 99. 0% - 99. 9%, and Greater Than 99. 9%), Application (Chemical Intermediate, Food and Beverage Preservation, Pharmaceutical Synthesis, Pulp and Paper Bleaching, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Sulfur Dioxide Market Trends and Insights

Growing Use in Sulfuric-Acid and Chemicals

Sulfuric-acid manufacturing anchors global SO2 offtake because no substitute exists for phosphate-fertilizer acidulation or copper-ore leaching. India added 1.2 million tons per annum of new acid capacity across Coromandel International, Paradeep Phosphates, and Gujarat State Fertilizers during 2024-2025, each tied to captive rock-phosphate conversion. China's spot sulfuric-acid price rose from CNY 400/ton (USD 54.50/ton) in Q1 2025 to CNY 520/ton (USD 73.78/ton) by December as Middle-East sulfur exports tightened. Hydrometallurgical nickel laterite leaching at Morowali and Weda Bay consumed 800,000 tons of acid in 2025, up 33% on higher EV-grade nickel-sulfate output. Semiconductor-grade acid, derived from more than 99.9% SO2, commands 3 to 5 times technical-grade pricing, prompting BASF to expand ultra-pure capacity at Ludwigshafen in April 2025. The dichotomy of high-volume fertilizer cycles versus high-margin electronics uses is locking the Sulfur dioxide market into a two-track structure that persists through 2031.

Expansion of Pulp and Paper Bleaching Capacity

Pulp mills in Asia and South America are outpacing Western closures, driving incremental SO2 demand. Grasim's 750 tons per day dissolving-pulp line at Vilayat integrates sulfite pulping for viscose fiber, while Shandong Bohui added 500,000 tons per annum bleached-kraft output adopting SO2 sequences in 2025. Norske Skog's Skogn mill cut specific SO2 emissions to 12.3 kg per air-dried ton in 2025 via scrubber upgrades. Nouryon and Arauco are piloting closed-loop bisulfite regeneration in Brazil, targeting a 30% cut in fresh sulfur. Regulatory frameworks such as the EU Industrial Emissions Directive and China's sector rules necessitate flue-gas scrubbers, reinforcing medium-term growth.

Health Hazards and Complex Handling

SO2 is a severe respiratory irritant; OSHA (Occupational Safety and Health Administration) caps 8 hours of exposure at 5 parts per million (ppm), while the National Institute for Occupational Safety and Health (NIOSH) recommends 2 parts per million (ppm). December 2024 EPA rules tightened the 1-hour ambient standard and expanded monitors, adding cost for sulfur-burn facilities. Semiconductor fabs must meet SEMI S2 (Semiconductor Manufacturing Equipment), keeping routine emissions below 1% of occupational limits and installing abatement costing USD 0.5-2 million per tool. These compliance burdens deter small users and consolidate volume with large industrial customers that maintain dedicated EHS (Environment, Health, and Safety) systems.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Disinfectant and Fumigant Adoption

- Surge in Synthetic Gypsum for Green Building

- Phase-Out of Coal Power Curbing Captive Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gas-phase SO2 accounted for 56.18% of the Sulfur Dioxide market share in 2025 as sulfuric-acid towers, scrubbers, and fabs require continuous gas feed. The segment benefits from entrenched infrastructure but faces heightened compliance costs under stricter ambient standards. Solid (Bisulfite/Metabisulfite Derivatives), though smaller, are growing at 5.87% CAGR as food-preservers and pharma plants favor low-pressure, transportable inputs that cut insurance premium outlays. The Sulfur Dioxide market size for solids is projected to rise steadily through 2031 on ASEAN demand, while gas retains a majority share in China and India, where large-scale acid plants dominate.

Liquid SO2 occupies a logistic midpoint, serving batch specialty-chemical makers and municipal plants. Chemtrade's Polytec acquisition strengthens its distribution of liquid cylinders and bisulfite blends across North America. Regulatory pressures in Vietnam and Thailand steer small users from gas toward solids, yet high-volume industrial sites will continue ordering bulk gas to maintain process continuity.

Geography Analysis

Asia-Pacific dominated the Sulfur Dioxide market in 2025 with 50.46% share and is projected to log 6.04% CAGR during the forecast period (2026-2031). China's sulfuric-acid spot price escalation signaled tight sulfur availability, while India's 1.2 million tons per annum capacity additions firm fertilizer-sector pull. Taiwan, Japan, and Korea anchor ultra-high-purity uptake for semiconductor nodes, and ASEAN regulations spur demand for point-of-use abatement systems, indirectly boosting bisulfite sales.

North America ranked second on the back of Gulf Coast sulfuric-acid clusters and new fab projects in Arizona and Texas. Linde's USD 400 million Louisiana ASU (Air Separation Unit) will co-produce liquid SO2, and Chemtrade's Polytec buyout broadens turnkey water-treatment offerings. EPA's tighter 1-hour ambient standard raises compliance expenses but also accelerates technology refresh toward closed-loop systems that favor large suppliers.

Europe trails on volume because coal retirements erase captive FGD streams; however, BASF's Ludwigshafen ultra-pure expansion highlights a pivot toward precision chemistry targeting the region's nascent advanced-node fabs. Nordic pulp operations maintain niche bisulfite use, while synthetic-gypsum scarcity is hiking natural-gypsum imports. South America's demand is led by Brazilian eucalyptus mills adopting closed-loop bisulfite regeneration, and Middle East & Africa volumes hinge on refinery sulfur recovery and South African mining.

- AIR LIQUIDE

- Air Products and Chemicals Inc.

- Atul Ltd.

- BASF

- Chemtrade Logistics

- Grillo-Werke AG

- INEOS

- Linde plc

- Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- Tokyo Chemical Industry (India) Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing use in sulfuric-acid and chemicals

- 4.2.2 Expansion of pulp and paper bleaching capacity

- 4.2.3 Industrial disinfectant and fumigant adoption

- 4.2.4 Surge in synthetic gypsum for green building

- 4.2.5 Emerging SO2-based battery electrolyte additives

- 4.3 Market Restraints

- 4.3.1 Health hazards and complex handling

- 4.3.2 Phase-out of coal power curbing captive supply

- 4.3.3 Electrochemical substitutes in semiconductor etching

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Gas

- 5.1.2 Liquid

- 5.1.3 Solid (Bisulfite/Metabisulfite Derivatives)

- 5.2 By Purity Grade

- 5.2.1 Less than 99% (Technical Grade)

- 5.2.2 99.0% - 99.9% (Food and Pharma Grade)

- 5.2.3 Greater than 99.9% (Ultra-high purity)

- 5.3 By Application

- 5.3.1 Chemical Intermediate (Sulfuric Acid)

- 5.3.2 Food and Beverage Preservation

- 5.3.3 Wine and Brewing Stabilization

- 5.3.4 Pulp and Paper Bleaching

- 5.3.5 Metal and Mining (Ore Leaching/Processing)

- 5.3.6 Waste- and Wastewater Treatment

- 5.3.7 Semiconductor Cleaning and Etching

- 5.3.8 Pharmaceutical Synthesis

- 5.3.9 Other Applications (Fumigation and Disinfection and Synthetic Gypsum Production)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AIR LIQUIDE

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 Atul Ltd.

- 6.4.4 BASF

- 6.4.5 Chemtrade Logistics

- 6.4.6 Grillo-Werke AG

- 6.4.7 INEOS

- 6.4.8 Linde plc

- 6.4.9 Messer Group GmbH

- 6.4.10 Taiyo Nippon Sanso Corporation

- 6.4.11 Tokyo Chemical Industry (India) Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment