|

시장보고서

상품코드

2061991

드론 소프트웨어 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Drone Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

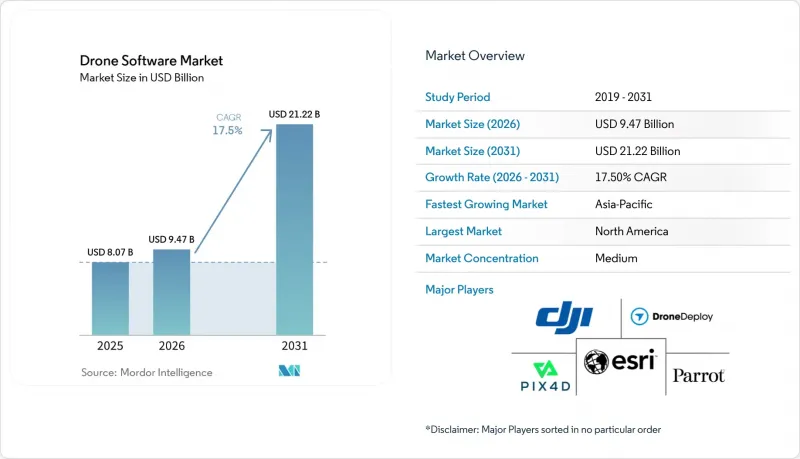

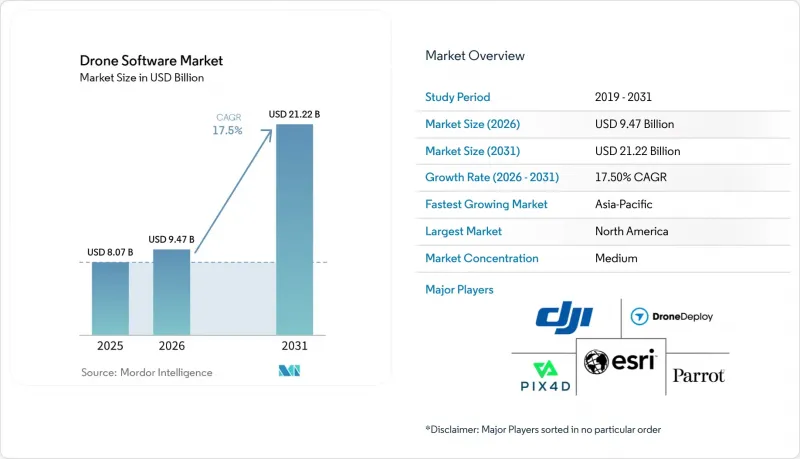

Mordor Intelligence에 의하면, 드론 소프트웨어 시장은 2025년에 80억 7,000만 달러, 2026년에 94억 7,000만 달러로 평가되었고 2031년까지 212억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 17.50%로 성장할 전망입니다.

본 보고서는 아키텍처(오픈소스 및 클로즈드 소스), 용도(매핑, 측량, 점검, 유지보수, 데이터 처리 및 분석 등), 최종 사용자(농업, 건설 및 광업, 에너지 및 유틸리티 등), 도입 형태(기재형 및 지상형), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 드론 소프트웨어 시장 동향과 인사이트

FAA Part 108 BVLOS 프레임워크가 명확한 소프트웨어 대상 시장을 창출

FAA가 BVLOS(시야등) 운항을 보다 공식적인 규제 체계로 전환함에 따라, 드론 소프트웨어 시장의 상업적 전망이 더욱 명확해지고 있습니다. FAA는 2025년 8월 Part 108에 대한 NPRM(규제안)을 발표하여, 저위험 및 고위험 운항을 위한 성능 기반 로드맵 외에도 전략적 충돌 회피, 적합성 모니터링 및 제3자 데이터 서비스와 관련된 소프트웨어 요건을 개괄적으로 설명했습니다. 이 점이 중요한 이유는 드론 소프트웨어 시장의 규정 준수 요건이 더 이상 비행 제어에만 국한되지 않고, 보고, 이벤트 로그, 그리고 운영자의 감독까지 확대되고 있기 때문입니다. Skydio가 공공 부문 사용자로부터 획득한 다중 드론 운용 승인은 한 명의 조종사가 여러 대의 기체를 감독할 수 있음을 입증하며, 함대 관리 및 상황 인식 소프트웨어의 필요성을 강조하고 있습니다.

또한, 월별 보고 및 사고 공개 요건은 일회성 라이선스 판매보다 구독 모델과 더 잘 맞기 때문에 이 규정은 지속적인 소프트웨어 수요를 창출합니다. 최종 규정이 2026년 2월의 법정 기한을 맞추지 못했기 때문에 단기적인 구매 결정은 여전히 신중한 태도를 보이고 있지만, 규제의 방향성은 여전히 드론 소프트웨어 시장에서 확장 가능한 자율성을 뒷받침하고 있습니다.

낮은 BOM 비용으로 에지 AI를 통합하여 기내 기능을 재구축

또한, 상용 항공기 군에서 기내 추론 처리가 경제적으로 실현 가능해짐에 따라, 드론 소프트웨어 시장은 더욱 에지 네이티브한 아키텍처로 전환되고 있습니다. 연산 비용의 감소로 인해 클라우드에 항상 의존하지 않고도 장애물 회피, 물체 분류, 자율 항행이 가능해지고 있으며, 이에 따라 벤더들은 기체 소프트웨어와 기업 워크플로우 모두의 설계 방식을 변경할 수밖에 없게 되었습니다. 또한, 소프트웨어 팀이 원격 처리 계층이 아닌 기체 측에 더 많은 기능을 탑재할 수 있게 됨에 따라, 드론 소프트웨어 시장에서 가치를 창출하는 영역도 변화하고 있습니다. 동시에, 기내에 더 많은 데이터를 보관함으로써 국경을 넘는 데이터 전송과 관련된 규제 위험을 줄일 수 있습니다. 그러나 한편으로는 소프트웨어 벤더들이 클라우드 분석을 중심으로 구축해 온 중앙 집중형 데이터 우위의 일부도 약화시키고 있습니다. 그 결과, 즉각적인 의사결정은 기내 인텔리전스가 처리하고, 집계, 오케스트레이션 및 장기적인 분석은 외부 시스템이 관리하는 하이브리드 아키텍처가 시장에서 점점 더 중요시되고 있습니다.

사이버 주권에 관한 규제가 전 세계 소프트웨어 아키텍처를 분열시키고 있습니다.

사이버 주권에 관한 규제로 인해 드론 소프트웨어 시장은 국경을 넘어 균일성을 잃어가고 있습니다. 2025년 미국의 정책 조치에 따라 연방 정부의 조달 및 수출 관리는 국내 기준을 준수하는 무인항공기(UAS) 시스템으로 전환되고 있으며, 소프트웨어 공급업체들은 단일 세계 플랫폼이 아닌 개별적인 규정 준수 스택의 관점에서 접근할 수밖에 없게 되었습니다. 이로 인해 규제 대상 구성 요소가 관련된 경우, 클라우드 통합, 펌웨어 지원, 로깅 기능, 업데이트 파이프라인을 모두 재검토해야 하므로 드론 소프트웨어 시장에서 불필요한 업무가 발생하고 있습니다. 이러한 부담이 가장 큰 곳은 여러 관할 구역에 걸쳐 정부, 인프라, 물류 관련 계약을 취급하는 사업자입니다. 이러한 고객들은 미국 내 공공 계약, 유럽의 데이터 거주 요건, 중국의 식별 규정 등에 맞추어 각각 다른 규정 준수 체계를 필요로 하는 경우가 늘고 있습니다. 이로 인해 중소 벤더의 비용이 증가함에 따라, 드론 소프트웨어 시장은 각 지역의 규제 요건을 충족시킬 수 있는 미들웨어 및 규정 준수 도구로 점차 전환되고 있습니다.

부문별 분석

2025년 기준으로 오픈소스 아키텍처는 드론 소프트웨어 시장 점유율의 61.18%를 차지하며 가장 큰 아키텍처 유형이 되었습니다. 이 리드는 농업, 검사, 공공 안전 등 각 분야의 맞춤형 상용 시스템의 기반 계층으로서 PX4와 ArduPilot이 널리 채택되고 있음을 반영합니다. 오픈소스 선택의 장점은 라이선스 비용이 저렴하다는 점에만 그치지 않습니다. 혼합 기기를 운영하는 사업자들도 하드웨어에 구애받지 않는 상호 운용성과 개발자의 유연성을 중요하게 여기기 때문입니다. 드론 소프트웨어 업계에서 이러한 장점은 중요합니다. 왜냐하면 기업의 항공기 편대는 여러 제조업체의 기체를 조합하는 경우가 많으며, 그럼에도 불구하고 공통된 임무 로직과 제어 방식이 필요하기 때문입니다. 또한, 이 부문은 구매자가 단일 하드웨어 공급업체에 의존하도록 강요하지 않으면서도 신속한 테스트, 맞춤화 및 모듈 확장을 지원하는 탄탄한 개발자 생태계의 혜택을 누리고 있습니다.

비공개 소스 플랫폼은 2031년까지 연평균 성장률(CAGR) 19.94%를 나타낼 것으로 예측되며, 드론 소프트웨어 시장에서 가장 빠르게 성장하는 아키텍처 부문이 될 전망입니다. 이러한 변화를 주도하고 있는 것은 기업 고객들입니다. 이들은 공급업체의 책임 명확화, 계약에 기반한 지원, 그리고 비행 제어 기능 위에 구축된 감사 가능한 보안 계층을 요구하고 있기 때문입니다. Auterion 시장 포지셔닝은 이러한 추세를 반영하고 있으며, 오픈소스 코어 위에 독자적인 관리 레이어를 구축하고, 2025년 9월에 발표된 1억 3,000만 달러 규모의 시리즈 B 자금 조달을 바탕으로 하고 있습니다. FAA가 제안한 항공 적합성 승인 절차는 이러한 추세를 더욱 가속화할 가능성이 있습니다. 문서화된 규정 준수 및 추적성은 관리된 릴리스와 명확한 책임 체계를 제공할 수 있는 공급업체에게 유리하게 작용하기 때문입니다. 장기적으로 드론 소프트웨어 시장은 두 가지 모델을 모두 유지할 것으로 보이며, 오픈소스는 개발 기반으로 남고, 클로즈드 소스 계층이 규제 대상 기업 지출에서 더 큰 비중을 차지하게 될 것입니다.

2025년 기준으로 데이터 처리 및 분석은 드론 소프트웨어 시장의 43.35%를 차지하며 가장 큰 응용 분야로 부상했습니다. 이 리드는 건설, 유틸리티, 농업 분야에 이미 도입된 사진측량, 원격탐사 및 검사 워크플로의 성숙도를 반영하고 있습니다. 이 부문은 부피 측정, 작물 분석, 열화상 검사, 손해배상 청구 문서화 등에 이르기까지 다른 응용 분야보다 더 폭넓은 이용 사례에 적합합니다. DroneDeploy는 2025년 10월, Progress AI, Safety AI, Inspection AI를 출시함으로써 이 가치 영역을 확대했습니다. 여기에는 50건 이상의 동시 진행 중인 건설 프로젝트의 진행 상황 추적, 보고서 작성 속도 향상, 9만 건 이상의 안전 위험 요인 파악 등이 포함됩니다. 또한, 분석 결과가 단순히 화면 캡처로 끝나는 것이 아니라 ERP, 자산 관리 및 보고 시스템에 직접 연동되는 경우가 늘어나고 있어, 이 용도는 더 고액의 계약 체결을 지원하는 데에도 기여합니다.

배송 및 물류 분야는 2031년까지 연평균 성장률(CAGR) 17.85%를 나타낼 것으로 예측되며, 드론 소프트웨어 시장에서 가장 빠르게 성장하는 응용 분야가 될 것입니다. 이러한 성장은 BVLOS(시야 외 비행) 기술의 발전에 달려 있습니다. 왜냐하면 경로 최적화, 교통 충돌 회피, 다중 드론 파견은 운영자가 조종사의 시야 범위 내에서만 수행되는 임무를 넘어 운영할 수 있게 되어야 비로소 규모를 확대할 수 있기 때문입니다. 매핑 및 측량 분야는 인프라 및 프로젝트 문서화 워크플로우 덕분에 규제 환경 속에서도 수요가 안정적이어서, 여전히 안정적인 수익원으로 자리 잡고 있습니다. 또한, 다중 드론 운용 승인이 확대됨에 따라 비행 제어 및 함대 운용 소프트웨어 시장도 성장세를 보이고 있으며, 이에 따라 오케스트레이션 도구와 실시간 모니터링 기능에 대한 필요성이 높아지고 있습니다. 또한, 드론 소프트웨어 업계가 Part 108에 기반한 공식적인 운용, 보고 및 훈련 요건에 적응해 나감에 따라, 훈련 및 시뮬레이션 분야의 중요성도 더욱 커질 것입니다.

지역별 분석

2025년, 북미는 드론 소프트웨어 시장 점유율의 39.93%를 차지하며 최대 지역 시장이 되었습니다. 이 지역은 주요 경제국 중 가장 선진적인 상업용 무인항공기(UAS) 운용 환경을 갖추고 있을 뿐만 아니라, 건설, 유틸리티, 보험, 공공안전 등 각 분야의 강력한 기업 수요의 혜택을 누리고 있습니다. FAA의 파트 108안은 전략적 충돌 회피, 적합성 모니터링, 제3자 데이터 서비스 등 BVLOS(시야등) 소프트웨어에 대한 요건을 명확한 제품 범주로 정의하고 있다는 점에서 특히 중요합니다. 국내 요건을 충족하는 드론 시스템에 대한 미국의 정책 지원 또한 공급업체 선정 및 조달 활동에 영향을 미치고 있으며, 규정 준수 및 추적성을 문서화할 수 있는 소프트웨어 공급업체가 우대받고 있습니다. 이러한 규제 구조, 기업의 예산, 방위 관련 분야의 조화가 맞물려 북미는 드론 소프트웨어 시장의 중심적 지위를 유지하고 있습니다.

유럽은 2025년 드론 소프트웨어 시장에서 중요한 위치를 차지하고 있으며, 규제 및 조달 기준을 통해 빠르게 발전하고 있습니다. EASA 규정은 여전히 운영의 기반이 되고 있지만, 인프라 관리에 디지털 트윈을 도입하는 것이 보다 직접적인 소프트웨어 수요를 촉발하고 있습니다. A2D Cloud는 AI를 활용한 결함 감지 기능과 인프라 사용자를 위한 국내 호스팅형 디지털 트윈 워크플로를 결합함으로써, 이 지역 특유의 요구 사항을 명확히 반영하고 있습니다. 또한, GDPR(EU 개인정보보호규정) 및 새롭게 제정되고 있는 EU AI법에 따라 벤더들은 ‘프라이버시 바이 디자인(Privacy by Design)’ 기능 도입을 요구받고 있으며, 이로 인해 규정 준수 비용은 증가하는 반면, 안전하고 주권적인 분석 아키텍처에 대한 수요는 높아지고 있습니다.

아시아태평양은 드론 소프트웨어 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 20.26%로 전망됩니다. 이 지역의 성장 양상은 북미와 달리, 도입이 민간 기업 수요에만 의존하는 것이 아니라 정책 주도 수요 창출에 의해 더욱 강력하게 견인되고 있습니다. 2025년 말에 공포되어 2026년 5월 1일부터 시행되는 중국의 운영 식별 및 실명 등록에 관한 국가 기준은 제조업체와 소프트웨어 제공업체에게 규정 준수 대응을 위한 직접적인 업그레이드 주기를 초래하고 있습니다. 또한, 인도의 농업 지원 프로그램 역시 보다 광범위한 하드웨어 기반을 구축하고 있으며, 이는 향후 분석 및 계획 도구에 대한 수요로 이어질 것으로 보입니다. 한편, 남미와 중동 및 아프리카는 전체 규모 면에서는 여전히 작지만, 특히 대규모 농업이 정밀 농업 소프트웨어와의 친화성을 높여가고 있는 지역에서는 여전히 성장 여지가 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the drone software market was valued at USD 8.07 billion in 2025, USD 9.47 billion in 2026, and is projected to reach USD 21.22 billion by 2031, growing at a CAGR of 17.50% over 2026-2031.

This report is Segmented by Architecture (Open-Source and Closed-Source), Application (Mapping and Surveying, Inspection and Maintenance, Data Processing and Analytics, and More), End-User (Agriculture, Construction and Mining, Energy and Utilities, and More), Deployment Mode (Onboard and Ground-Based), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Drone Software Market Trends and Insights

FAA Part 108 BVLOS Framework Is Creating a Defined Software Addressable Market

The drone software market is gaining a clearer commercial path as the FAA moves BVLOS operations into a more formal rule structure. The FAA published its Part 108 NPRM in August 2025, outlining performance-based pathways for lower- and higher-risk operations, along with software requirements for strategic deconfliction, conformance monitoring, and third-party data services. This matters because compliance in the drone software market is no longer limited to flight control and now extends to reporting, event logging, and operator oversight. Skydio's multi-drone operating approvals with public-sector users demonstrate that one operator can supervise multiple aircraft, underscoring the need for fleet management and situational awareness software.

The rule also creates recurring software demand, as monthly reporting and incident disclosure requirements align better with subscription models than with one-time license sales. The final rule missed its February 2026 statutory deadline, so near-term buying decisions remain cautious, but the regulatory direction still supports scalable autonomy in the drone software market.

Edge AI Integration at Low Bill-of-Materials Cost Is Reshaping Onboard Capability

The drone software market is also moving toward a more edge-native architecture as onboard inference becomes affordable for commercial fleets. Lower compute costs are making obstacle avoidance, object classification, and autonomous navigation viable without constant reliance on the cloud, which changes how vendors design both aircraft software and enterprise workflows. It also shifts where value is captured in the drone software market, as software teams can push more functionality into the aircraft rather than into remote processing layers. At the same time, keeping more data on the aircraft reduces exposure to cross-border data transfer rules. Still, it also weakens some of the centralized data moats that software vendors built around cloud analytics. The result is a market that increasingly rewards hybrid architecture, with onboard intelligence handling immediate decisions and external systems managing aggregation, orchestration, and long-cycle analysis.

Cyber-Sovereignty Mandates Are Fragmenting Global Software Architecture

Cyber-sovereignty rules are making the drone software market less uniform across borders. US policy actions in 2025 moved federal procurement and export controls toward domestically aligned UAS systems, pushing software vendors to think in terms of separate compliance stacks rather than a single global platform, creating extra work in the drone software market because cloud integration, firmware support, logging functions, and update pipelines may all need review when regulated components are involved. The burden is highest for operators that work across government, infrastructure, and logistics contracts in more than one jurisdiction. These customers increasingly need one stack for US public contracts, another for European data residency, and another for Chinese identification rules. That raises costs for smaller vendors and pushes the drone software market toward middleware and compliance tools that can bridge local regulatory demands.

Other drivers and restraints analyzed in the detailed report include:

- APAC Agri-Tech Subsidies Are Building a Software Demand Foundation

- Insurance-Linked Imagery Workflows Are Expanding Commercial Use Cases

- Certified UAS Software Talent Gaps Are Constraining Scale-Up

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Open-source architecture held 61.18% of the drone software market share in 2025, making it the largest architecture type. This lead reflects the wide adoption of PX4 and ArduPilot as base layers for custom commercial systems across agriculture, inspection, and public safety. The strength of open-source options extends beyond lower licensing costs, as mixed-fleet operators also value hardware-agnostic interoperability and developer flexibility. That advantage matters in the drone software industry because enterprise fleets often combine aircraft from multiple manufacturers and still need a common mission logic and control approach. The segment also benefits from a deep developer ecosystem that supports rapid testing, customization, and module extension without forcing buyers to rely on a single hardware supplier.

Closed-source platforms are projected to grow at a 19.94% CAGR through 2031, making them the fastest-growing architecture segment in the drone software market. Enterprise clients are driving that shift because they want stronger vendor accountability, contractual support, and auditable security layers that sit above flight control functions. Auterion's commercial positioning reflects this pattern, with a proprietary management layer built on top of an open-source core and backed by a USD 130 million Series B announced in September 2025. The FAA's proposed Airworthiness Acceptance process is likely to further support this movement, as documented compliance and traceability favor vendors that can deliver controlled releases and clear responsibility chains. Over time, the drone software market is likely to keep both models, with open-source remaining the development substrate and closed-source layers capturing a larger share of regulated enterprise spending.

Data processing and analytics accounted for 43.35% of the drone software market in 2025, making it the largest application segment. Its lead reflects the maturity of photogrammetry, remote sensing, and inspection workflows that are already embedded in construction, utilities, and agricultural operations. The segment spans volumetric measurement, crop analysis, thermal inspection, and claims documentation, making it suitable for a broader range of use cases than other applications. DroneDeploy expanded this value layer in October 2025 by launching Progress AI, Safety AI, and Inspection AI, including progress tracking across more than 50 concurrent construction projects, faster report generation, and the identification of more than 90,000 safety risks. The application also supports higher contract values because analytics outputs increasingly move directly into ERP, asset, and reporting systems rather than stopping at image capture.

Delivery and logistics are projected to grow at a 17.85% CAGR through 2031, making it the fastest-growing application in the drone software market. That growth depends on BVLOS progress because route optimization, traffic deconfliction, and multi-drone dispatch only scale when operators can move beyond pilot-visible missions. Mapping and surveying remain a stable revenue stream because infrastructure and project documentation workflows keep demand consistent across regulated environments. Flight control and fleet operations software is also gaining ground as multi-drone operating approvals expand, which raises the need for orchestration tools and real-time oversight layers. Training and simulation should also gain weight as the drone software industry adapts to formal operating, reporting, and training expectations under Part 108.

Geography Analysis

North America held 39.93% of the drone software market share in 2025, making it the largest regional market. The region benefits from the most advanced commercial UAS operating environment among major economies and from strong enterprise demand across construction, utilities, insurance, and public safety. The FAA's Part 108 proposal is especially important because it defines BVLOS software needs as distinct product categories, including strategic deconfliction, conformance monitoring, and third-party data services. US policy support for domestically aligned drone systems is also influencing vendor selection and procurement behavior, which favors software suppliers that can document compliance and traceability. This combination of regulatory structure, enterprise budgets, and defense-related alignment keeps North America at the center of the drone software market.

Europe held a meaningful position in the drone software market in 2025 and continues to evolve quickly through regulation and procurement standards. EASA rules remain the operating backbone, but digital twin adoption in infrastructure management is becoming the more direct software demand trigger. A2D Cloud clearly shows this regional preference by combining AI-driven defect detection with domestically hosted digital twin workflows for infrastructure users. GDPR and the emerging EU AI Act are also pushing vendors toward privacy-by-design features, which raise compliance costs but strengthen demand for secure, sovereign analytics architectures.

Asia-Pacific is the fastest-growing region in the drone software market, with a projected CAGR of 20.26% through 2031. The region's growth pattern differs from North America's because adoption is driven more by policy-led volume creation than by private enterprise pull alone. China's national standards on operational identification and real-name registration, issued in late 2025 and effective from May 1, 2026, are creating a direct compliance upgrade cycle for manufacturers and software providers. India's agricultural support programs are also building a broader hardware base that should translate into future demand for analytics and planning tools. At the same time, South America, the Middle East, and Africa remain smaller in total but still offer room for expansion, especially where large-scale farming creates a strong fit for precision agriculture software.

- SZ DJI Technology Co., Ltd.

- DroneDeploy, Inc.

- Pix4D SA

- Esri Global, Inc.

- Parrot Drones SAS

- Skydio, Inc.

- DELAIR SAS

- Skycatch, Inc.

- SPH Engineering

- Airobotics (Ondas Holdings Inc.)

- AgEagle Aerial Systems Inc.

- Trimble Inc.

- Auterion LLC

- Aloft Technologies, Inc.

- FlytBase, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FAA BVLOS rulemaking slated for 2026

- 4.2.2 On-drone edge-AI chips priced under USD 30 in the Bill of Materials

- 4.2.3 Rapid fall in Li-ion battery cost per kWh enabling longer missions

- 4.2.4 Wave of agri-tech subsidies in emerging APAC economies

- 4.2.5 Mandatory digital twins for infrastructure projects in EU starting in 2026

- 4.2.6 Insurance-premium discounts tied to automated claims imagery

- 4.3 Market Restraints

- 4.3.1 Shortage of certified UAS software talent

- 4.3.2 Tighter cyber-sovereignty laws restricting data export

- 4.3.3 Persistent public-privacy litigation in EU and US

- 4.3.4 Rising spectrum-management fees for commercial drone links

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Open-Source

- 5.1.2 Closed-Source

- 5.2 By Application

- 5.2.1 Mapping and Surveying

- 5.2.2 Inspection and Maintenance

- 5.2.3 Data Processing and Analytics

- 5.2.4 Delivery and Logistics

- 5.2.5 Flight Control and Fleet Ops

- 5.2.6 Training and Simulation

- 5.3 By End-User

- 5.3.1 Agriculture

- 5.3.2 Construction and Mining

- 5.3.3 Energy and Utilities

- 5.3.4 Logistics and Transportation

- 5.3.5 Media and Entertainment

- 5.3.6 Environmental Monitoring and Insurance

- 5.4 By Deployment Mode

- 5.4.1 Onboard

- 5.4.2 Ground-Based

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 DroneDeploy, Inc.

- 6.4.3 Pix4D SA

- 6.4.4 Esri Global, Inc.

- 6.4.5 Parrot Drones SAS

- 6.4.6 Skydio, Inc.

- 6.4.7 DELAIR SAS

- 6.4.8 Skycatch, Inc.

- 6.4.9 SPH Engineering

- 6.4.10 Airobotics (Ondas Holdings Inc.)

- 6.4.11 AgEagle Aerial Systems Inc.

- 6.4.12 Trimble Inc.

- 6.4.13 Auterion LLC

- 6.4.14 Aloft Technologies, Inc.

- 6.4.15 FlytBase, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment