|

시장보고서

상품코드

2061998

식수용 흡착제 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Drinking Water Adsorbents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

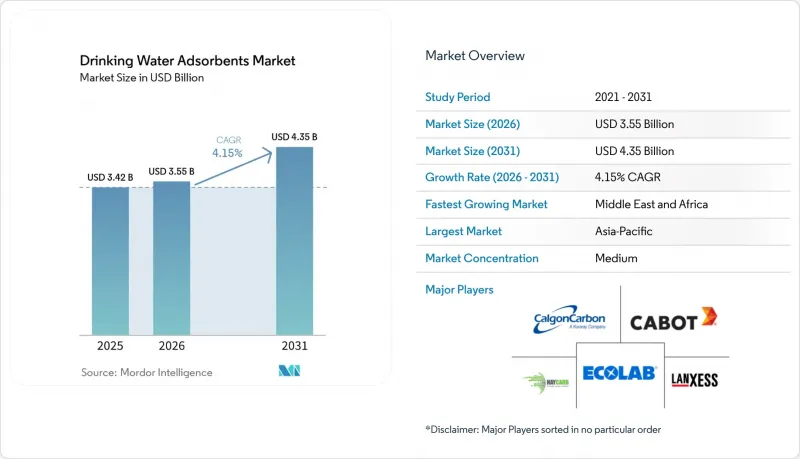

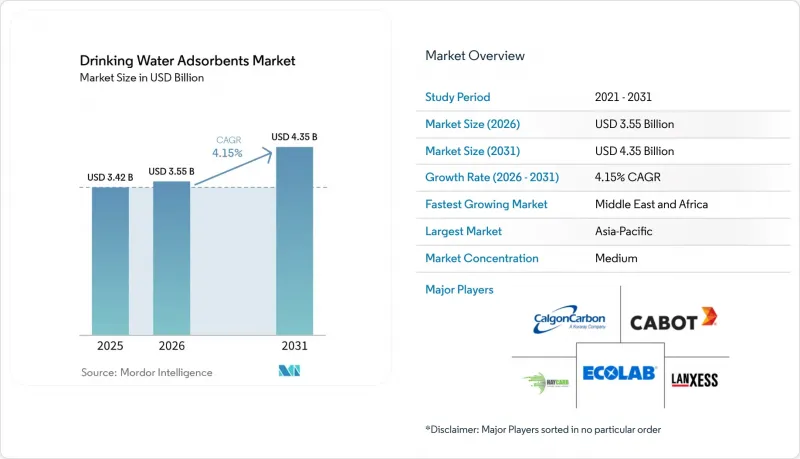

Mordor Intelligence에 의하면, 식수용 흡착제 시장 규모는 2025년 34억 2,000만 달러로 평가되었습니다. 2026년 35억 5,000만 달러로 확대되어 2031년까지 43억 5,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 4.15%를 나타낼 전망입니다.

본 보고서는 재료의 유형(활성탄, 제올라이트 등), 형태(분말 등), 대상 오염 물질(유기 미량 오염 물질, PFAS·불소화 화합물 등), 용도(상수도 처리, 주택용 POU/POE 시스템 등), 지역(북미, 아시아태평양, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 식수용 흡착제 시장 동향 및 인사이트

물의 순도와 건강 및 안전에 대한 우려가 커지고 있습니다.

미세플라스틱 및 나노플라스틱이 심혈관계와 신장에 부담을 주는 것과 관련이 있다는 과학적 증거가 밝혀짐에 따라, 수돗물과 생수의 품질에 대한 일반 시민들의 감시가 강화되었습니다. 이에 따라 북미 및 서유럽 가정에서는 NSF/ANSI 53 및 401 인증을 획득한 싱크대 하부 설치형 GAC 카트리지의 도입이 가속화되었으며, 포화 상태에 가까워지면 사용자에게 경고를 보내는 연결형 POU(사용 지점) 장치의 소매 시장 침투가 확대되었습니다. 음료 브랜드들도 이에 대응하여, 네슬레 워터스는 펜실베이니아주 공장에서 역삼투막을 이용한 최종 정수 과정에 앞서 서브마이크론 크기의 플라스틱 입자를 걸러내기 위해 대나무 숯 프리필터를 도입했습니다. 세계보건기구(WHO)는 지침을 개정하여 미세플라스틱 모니터링을 포함시켰지만, 법적 구속력이 있는 기준치가 설정되어 있지 않아 프리미엄 제품의 차별화를 꾀할 여지가 남아 있습니다. 이러한 소비자 주도적인 추세는 1µm 이하의 입자를 제거하는 능력을 기준으로 공급업체를 평가하게 된 수도 유틸리티자의 입찰에도 영향을 미치고 있으며, 이에 따라 해당 식수용 흡착제 시장이 확대되고 있습니다.

지자체 및 산업용 처리 시설에서 수요 증가

인도, 인도네시아, 사우디아라비아에서 연간 3% 이상의 도시화 속도는 기존 인프라에 부담을 주고 있으며, 수천 개의 시설에서 GAC(과립 활성탄), 이온 교환 및 고도 산화 처리 단계의 개보수를 진행하고 있습니다. 중국에서 제4류 지표수 기준의 시행에 따라, 베이징 기업수무집단이 주도하는 형태로 허베이성과 산둥성에 오존-GAC 컨택터의 설치가 이미 촉진되고 있습니다. 산업 시설, 특히 반도체 및 제약 업계에서는 비저항이 18 MΩ·cm를 초과하는 초순수가 필요합니다. 2024년 하반기부터 가동을 시작한 대만 반도체 제조 회사(TSMC)의 애리조나 캠퍼스에서는 해당 사양을 충족하기 위해 혼합 베드 수지와 GAC 폴리셔를 도입했습니다. 이러한 유틸리티 및 산업 분야의 설비 교체는 식수용 흡착제 시장의 장기적인 성장 궤도를 뒷받침하는 지속적인 수요로 이어집니다.

고급 흡착제 재료의 높은 비용

금속-유기 골격체(MOF)와 산화 그래핀의 현재 소매 가격은 1kg당 150-300달러이지만, 일반적인 석탄 유래 GAC는 2-5달러에 불과하기 때문에 이들의 채택은 높은 비용을 감당할 수 있는 반도체 및 제약 시설의 초순수 라인으로 제한되고 있습니다. 원자재 가격 변동이 이 문제를 더욱 심각하게 만들고 있습니다. 인도네시아가 2025년 하반기로 정한 코코넛 껍질 수출 할당량으로 인해 세계 가격이 18% 상승했고, Haycarb사는 스리랑카에서 건조로 개조를 거친 후 고무나무 숯의 상업화를 추진할 수밖에 없게 되었습니다(BLOOMBERG.COM). 그 때문에 가격에 민감한 남미 및 중동 및 아프리카(MEA) 지역의 소규모 상수도 유틸리티자들은 염소 소독만 사용하는 방식에서 전환하는 것을 미루고 있어, 식수용 흡착제 시장의 단기적인 성장을 둔화시키고 있습니다.

부문별 분석

2025년 매출의 56.20%를 활성탄이 차지했으며, 이는 저렴한 비용으로 맛과 냄새는 물론 광범위한 유기물을 제거한다는 활성탄의 확고한 역할을 입증하고 있습니다. 한편, 재활성화를 통해 용량의 대부분을 회복할 수 있으며, 탄소 발자국을 70% 줄일 수 있습니다. 금속-유기 골격체(MOF) 시장은 2031년까지 연평균 성장률(CAGR) 5.61%라는 최고 수준으로 성장하고 있습니다. 이온 교환 수지는 경도 및 질산염 조절이라는 틈새 시장을 공략하고 있습니다. 퓨로라이트사의 PFAS 선택성 수지 A600E는 기존 매체에 비해 40% 더 긴 수명을 자랑합니다. MOF를 이용한 식수용 흡착제 시장 규모는 여전히 작지만, 노스웨스턴 대학교의 MOF-808이 GAC보다 10분의 1에 불과한 접촉 시간으로 PFOA를 99% 제거하는 데 성공함에 따라, 시장이 급속히 확대될 것으로 전망됩니다. 상용화의 장벽은 여전히 존재하지만, 반도체 팹으로부터의 시범 주문은 규모 확대를 위한 현실적인 길을 시사하고 있습니다.

그래핀 및 탄소 나노 흡착제의 식수용 흡착제 시장에서의 장기적인 점유율은 GAC보다 50배나 높은 가격 때문에 제한받고 있으며, 그 적용은 주로 유기물의 침투로 인해 웨이퍼 수율이 저하되는 초순수 루프로 한정되어 있습니다. 대나무 숯 등 바이오 흡착제는 현재 석탄 유래 GAC의 요오드 가치의 80%에 달하며, 비용은 절반 수준이기 때문에 인도, 인도네시아 및 아프리카 일부 지역에서 해당 시장 규모가 확대되고 있습니다. 이러한 선택지들은 공급망의 다각화와 탈탄소화의 이점을 가져다주며, 소재 대체가 앞으로도 시장 역학을 형성하는 중요한 요인으로 남아 있을 것임을 시사합니다.

입자상 매체는 기존 접촉기와 원활한 호환성을 갖추고 예측 가능한 압력 손실 프로파일을 제공함으로써, 2025년 수요의 48.16%를 차지했습니다. 분말 유형은 맛이나 냄새를 ‘강하게’ 전달하는 데 사용되며, 압출 성형품이나 비드 형태의 제품은 가정용 카트리지에 적합합니다. 막 코팅 처리된 매체를 사용한 식수용 흡착제 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.56%를 나타낼 것으로 전망됩니다. 이는 반도체 파브나 해양 플랫폼에서 2025년 대만의 전자기기 공장에서 입증된 설치 면적 40% 절감 효과가 높이 평가받고 있기 때문입니다.

3M사와 맨 앤 훔멜사가 개발 중인 카본 코팅 중공사막은 입자 크기별 여과와 흡착 기능을 하나의 필터 요소에 결합함으로써 수명을 연장합니다. NSF/ANSI 61의 용출물 기준을 충족한다면 인증 장벽은 낮으며, 현장 데이터가 파일럿 시험 결과를 뒷받침한다면 신속한 상용화가 기대됩니다. 주거용 POU(Point of Use) 장치의 경우, 유지보수의 편의성이 폼 팩터 선택에 큰 영향을 미치는 경향이 점점 더 강해지고 있습니다. 트위스트 핏 방식의 하우징을 갖춘 퀵 스왑형 카본 블록이 기존의 루즈 필형 카트리지를 대체하며 시장 점유율을 확대하고 있어, 식수용 흡착제 시장의 애프터마켓 수익 구조를 재편하고 있습니다.

지역별 분석

2025년 매출의 37.90%를 차지한 아시아태평양은 인도의 ‘Jal Jeevan Mission’과 중국의 도시 차원 의무화 조치에 따라, 수천 건의 GAC(과립 활성탄) 및 이온 교환 수지 개보수 공사에 자금이 지원됨에 따라, 2031년까지 매출 1위 자리를 유지할 전망입니다. 아세안 국가들도 이에 발맞추고 있으며, 자카르타에서 베올리아사와 체결한 1억 2,000만 달러 규모의 계약을 통해 서비스 대상 인구가 250만 명으로 확대될 전망입니다. 한국과 일본의 반도체 산업 확대는 초순수용 수지 수요를 끌어올리고 있는 반면, PFOS/PFOA의 잠정 기준치인 50 ng/L는 흡착제의 추가 도입을 촉진할 것으로 보입니다.

중동 및 아프리카는 사우디아라비아의 라스 알 카일 및 쇼아이바 해수 담수화 시설에 대한 32억 달러 규모의 개보수 사업에 힘입어 2031년까지 연평균 성장률(CAGR) 5.64%를 나타낼 것으로 전망되며, 이는 세계에서 가장 빠른 성장 속도입니다. 남아프리카공화국의 랜드 워터 시설에서 진행된 18억 랜드(약 1억 1,000만 달러) 규모의 GAC(입상 활성탄) 개보수 공사는 이 대륙이 첨단 처리 기술로 전환하고 있음을 보여줍니다. 인도적 지원 수요도 두드러지며, 유니세프는 이미 가뭄 피해를 입은 케냐와 에티오피아에 5만 개의 라이프스트로를 배포하고 있습니다.

북미 시장의 성장은 EPA(미국 환경보호청)의 PFAS 규제에 힘입고 있으며, 이에 따라 연간 약 15억 달러가 처리 시설 업그레이드에 투자되고 있습니다. 칼곤 카본의 콜럼버스 공장에서 진행될 2,700만 파운드 규모의 확장 계획과 에보쿠아의 센서 탑재형 ‘SmartGuard’ 플랫폼을 통해, 국내 공급업체들은 이러한 수요를 확보할 준비를 갖추고 있습니다. 캐나다의 PFAS 지침안과 멕시코의 비소 대책 프로그램 역시 수요를 끌어올리며, 해당 지역의 안정적인 수요 기반을 더욱 공고히 하고 있습니다.

유럽은 세계에서 가장 엄격한 PFAS 상한치(100 ng/L)를 적용받고 있으며, 독일, 스페인, 이탈리아의 유틸리티체들은 GAC(활성탄) 및 수지 설비의 개보수를 서둘러 진행하고 있습니다. 케미라사의 타라고나 재활성화 허브는 연간 1만 5,000톤의 사용 후 활성탄을 처리하며, 톤당 1,000유로(약 1,170달러)가 넘는 처리 비용을 절감합니다. 미국에서는 납의 행동 기준치가 하향 조정됨에 따라, 동시에 노후 주택에 POE 필터 도입이 촉진되고 있습니다.

남미는 여전히 규모는 작지만 성장 중인 시장이며, 2025년 매출의 약 8%를 차지했습니다. 브라질 상파울루의 과라피랑가 급수 시설을 대상으로 한 5억 레알(약 9,965만 달러) 규모의 GAC(활성탄) 교체 프로젝트와, 아르헨티나에서 세계은행이 자금을 지원하는 비소 대책 프로젝트는 환경 규제가 점차 강화되고 있음을 보여줍니다. 칠레에서는 2024년에 탁도 규제가 강화되면서 산티아고 분지의 유틸리티 회사들의 설비 투자가 촉진되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the drinking water adsorbents market size is expected to increase from USD 3.42 billion in 2025 to USD 3.55 billion in 2026 and reach USD 4.35 billion by 2031, growing at a CAGR of 4.15% over 2026-2031.

This report is Segmented by Material Type (Activated Carbon, Zeolites, and More), Form Factor (Powdered, and More), Contaminant Target (Organic Micropollutants, PFAS and Fluorinated Compounds, and More), Application (Municipal Water Treatment, Residential POU/POE Systems, and More), and Geography (North America, Asia-Pacific, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Drinking Water Adsorbents Market Trends and Insights

Growing Concern Over Water Purity And Health Safety

Scientific evidence linking micro- and nanoplastics to cardiovascular and renal stress sparked heightened public scrutiny of tap and bottled water quality. In response, North American and Western European households accelerated installation of NSF/ANSI 53- and 401-certified under-sink GAC cartridges, widening retail penetration of connected point-of-use devices that alert users when saturation nears breakthrough. Beverage brands also reacted; Nestle Waters introduced bamboo-char prefilters at its Pennsylvania plant to curb sub-micron plastics before reverse-osmosis polishing. Although the World Health Organization revised its guidelines to include microplastic monitoring, the absence of binding limits leaves room for premium differentiation. This consumer-led momentum is rippling into utility tenders that now evaluate suppliers on capacity to remove particles below 1 µm, expanding the addressable drinking water adsorbents market.

Rising Demand From Municipal And Industrial Treatment Plants

Urbanization exceeding 3% annually across India, Indonesia, and Saudi Arabia is stretching legacy infrastructure, prompting thousands of plants to retrofit GAC, ion-exchange, and advanced oxidation stages. China's enforcement of Class IV surface-water standards has already driven ozone-GAC contactor installs in Hebei and Shandong provinces, spearheaded by Beijing Enterprises Water Group. Industrial facilities, particularly semiconductor and pharmaceutical, require ultrapure water with resistivity above 18 MΩ-cm; Taiwan Semiconductor Manufacturing Company's Arizona campus, operational since late 2024, relies on mixed-bed resins and GAC polishers to meet that spec. These utility and industrial upgrades translate into durable demand that underpins the long-run growth trajectory of the drinking water adsorbents market.

High Cost Of Advanced Adsorbent Materials

Metal-organic frameworks (MOFs) and graphene oxide currently retail between USD 150 and 300 per kg, compared with USD 2-5 for standard coal-based GAC, limiting adoption to ultrapure-water lines in semiconductor and pharmaceutical facilities that can absorb the premium USP.ORG. Feedstock price volatility compounds the issue; Indonesia's late-2025 coconut-shell export quota pushed global prices up 18%, forcing Haycarb to commercialize rubber-wood char after kiln retrofits in Sri Lanka BLOOMBERG.COM. Small utilities in price-sensitive South America and MEA, therefore, delay switching from chlorination-only schemes, tempering the near-term expansion of the drinking water adsorbents market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption Of POU/POE Systems

- Stringent PFAS And Emerging-Contaminant Regulations

- Disposal Challenges And Environmental Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Activated carbon secured 56.20% of 2025 revenue, underscoring its entrenched role in stripping taste, odor, and a wide spectrum of organics at low cost, while reactivation recovers most capacity with a 70% carbon-footprint saving. Metal organic frameworks are growing with highest CAGR of 5.61% through 2031. Ion-exchange resins serve hardness and nitrate control niches; Purolite's PFAS-selective A600E resin achieves 40% longer cycles than legacy media. The drinking water adsorbents market size for MOFs remains small but is forecast to widen rapidly as Northwestern University's MOF-808 achieved 99% PFOA removal with contact times one-tenth those of GAC. Commercialization hurdles persist, yet pilot orders from semiconductor fabs suggest a viable path to scale.

The long-run drinking water adsorbents market share of graphene and carbon-nano adsorbents is capped by prices fifty times higher than GAC, keeping adoption largely in ultrapure loops where organic breakthroughs ruin wafer yields . Bio-based adsorbents such as bamboo char now match 80% of coal-GAC's iodine number at half the cost, expanding addressable volume in India, Indonesia, and parts of Africa. These options diversify supply chains and offer decarbonization benefits, indicating that material substitution will remain a critical lever shaping future market dynamics.

Granular media commanded 48.16% of 2025 demand thanks to seamless drop-in compatibility with existing contactors and predictable head-loss profiles. Powdered variants serve taste-and-odor "shock" dosing, while extruded and bead formats align with residential cartridges. The drinking water adsorbents market size for integrated membrane-coated media is poised for 5.56% CAGR growth during 2026-2031 because semiconductor fabs and offshore platforms value the 40% footprint cut validated at a Taiwan electronics plant in 2025.

Carbon-coated hollow-fiber membranes under development by 3M and Mann+Hummel extend service life by combining size-exclusion filtration with adsorption in one element. Certification barriers are modest as long as NSF/ANSI 61 leachate criteria are met, so rapid commercialization is likely once field data corroborate pilot results. In residential POU units, form-factor choice increasingly hinges on maintenance convenience; quick-swap carbon blocks with twist-fit housings are gaining share at the expense of traditional loose-fill cartridges, reshaping aftermarket revenue streams in the drinking water adsorbents market.

Geography Analysis

Asia-Pacific, accounting for 37.90% of 2025 turnover, will remain the revenue leader through 2031 as India's Jal Jeevan Mission and China's city-level mandates finance thousands of GAC and ion-exchange retrofits. ASEAN countries are following suit; Jakarta's USD 120 million Veolia contract will lift coverage to 2.5 million residents. Semiconductor expansion in South Korea and Japan is boosting ultrapure-water resin demand, while provisional PFOS/PFOA targets of 50 ng/L will catalyze further adsorbent adoption.

The Middle East and Africa region is forecast to clock a 5.64% CAGR through 2031, the fastest globally, underpinned by Saudi Arabia's USD 3.2 billion upgrades at Ras Al-Khair and Shoaiba desalination complexes. South Africa's ZAR 1.8 billion (~USD 0.11 billion) GAC retrofits at Rand Water facilities highlight the continent's pivot toward advanced treatment. Humanitarian demand is also material; UNICEF has already distributed 50,000 LifeStraw units across drought-hit Kenya and Ethiopia.

North America market growth is anchored by the EPA's PFAS rule, which is funneling an estimated USD 1.5 billion per year into treatment upgrades. Calgon Carbon's 27-million-lb Columbus expansion and Evoqua's sensor-enabled SmartGuard platform position domestic suppliers to capture the spend. Canada's draft PFAS guideline and Mexico's arsenic mitigation programs add incremental volume, solidifying the region's consistent demand base.

Europe faces the strictest PFAS cap worldwide at 100 ng/L, pushing utilities in Germany, Spain, and Italy to fast-track GAC and resin retrofits. Kemira's Tarragona reactivation hub will process 15,000 tons/year of spent carbon, reducing disposal costs that exceed EUR 1,000/ton (~USD 1,170/ton). The U.K.'s lower lead action level has simultaneously driven POE filter adoption in older housing stock.

South America remains a smaller but growing market, roughly 8% of 2025 sales. Brazil's BRL 500 million (~USD 99.65 million) GAC upgrade for Sao Paulo's Guarapiranga supply and Argentina's World Bank-funded arsenic projects illustrate rising environmental stringency. Chile's turbidity rule tightened in 2024, spurring CAPEX at utilities in the Santiago basin.

- Ahlstrom

- BASF

- Cabot Corporation

- Calgon Carbon Corporation

- Donau Carbon GmbH

- Evoqua Water Technologies LLC

- Graver Technologies

- Haycarb PLC

- Jacobi Carbons AB

- Kemira

- KMI Zeolite Inc.

- Kuraray Co., Ltd.

- Kurita America Inc.

- Lanxess

- Lenntech B.V.

- Norit

- Osaka Gas Chemicals Co., Ltd.

- Purolite

- Thermax Limited

- Xylem

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Concern over Water Purity and Health Safety

- 4.2.2 Rising Demand from Municipal and Industrial Treatment Plants

- 4.2.3 Increasing Adoption of POU/POE Systems

- 4.2.4 Stringent PFAS and Emerging-Contaminant Regulations

- 4.2.5 Surge in Modular/Mobile Water Units for Disaster-Relief and Remote Areas

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Adsorbent Materials

- 4.3.2 Disposal Challenges and Environmental Burdens

- 4.3.3 Feedstock Instability for Premium Activated Carbon

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Activated Carbon

- 5.1.2 Zeolites

- 5.1.3 Ion-Exchange Resins

- 5.1.4 Graphene and Carbon-Nano Adsorbents

- 5.1.5 Metal-Organic Frameworks (MOFs)

- 5.1.6 Bio-Based Adsorbents (Biochar, Bamboo-char, etc.)

- 5.2 By Form Factor

- 5.2.1 Powdered

- 5.2.2 Granular

- 5.2.3 Extruded/Bead

- 5.2.4 Integrated Membrane-Coated Media

- 5.3 By Contaminant Target

- 5.3.1 Organic Micropollutants (VOC, Pesticides)

- 5.3.2 PFAS and Fluorinated Compounds

- 5.3.3 Heavy Metals and Radionuclides

- 5.3.4 Micro-/Nano-Plastics

- 5.4 By Application

- 5.4.1 Municipal Water Treatment

- 5.4.2 Residential POU/POE Systems

- 5.4.3 Industrial Process and Utility Water

- 5.4.4 Bottled and Packaged Drinking Water Processing

- 5.4.5 Portable and Emergency Purification Units

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ahlstrom

- 6.4.2 BASF

- 6.4.3 Cabot Corporation

- 6.4.4 Calgon Carbon Corporation

- 6.4.5 Donau Carbon GmbH

- 6.4.6 Evoqua Water Technologies LLC

- 6.4.7 Graver Technologies

- 6.4.8 Haycarb PLC

- 6.4.9 Jacobi Carbons AB

- 6.4.10 Kemira

- 6.4.11 KMI Zeolite Inc.

- 6.4.12 Kuraray Co., Ltd.

- 6.4.13 Kurita America Inc.

- 6.4.14 Lanxess

- 6.4.15 Lenntech B.V.

- 6.4.16 Norit

- 6.4.17 Osaka Gas Chemicals Co., Ltd.

- 6.4.18 Purolite

- 6.4.19 Thermax Limited

- 6.4.20 Xylem

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Advances in Nano-Structured Adsorbents and Smart Filtration Materials

- 7.3 Rising Need for Portable and Emergency-Use Purification Kits